# http://polarismarketresearch.com llms-full.txt

## Market Research Insights

- [Press Releases](https://www.polarismarketresearch.com/press-releases)

- [Blog](https://www.polarismarketresearch.com/blogs)

- [About](https://www.polarismarketresearch.com/#)

[Who We Are](https://www.polarismarketresearch.com/who-we-are) [Why Select Us](https://www.polarismarketresearch.com/why-select-us) [Careers](https://www.polarismarketresearch.com/careers)

- [Contact](https://www.polarismarketresearch.com/contact)

- Services

[Consulting](https://www.polarismarketresearch.com/services/consulting) [Other Services](https://www.polarismarketresearch.com/services/other-services) [Research](https://www.polarismarketresearch.com/services/research)

- We are present worldwide

- 1000+ Satisfied clients

- Data in excel

- Quality assured

- Uninterrupted services commitment

- Information security

# From Research to Results

Polaris Market Research equips you with in-depth insights on current and future industry trends and opportunities. Our intelligence and up-to-date data assist you in making effective business decisions, which would help you move faster and achieve measurable outcomes.

## Market Intelligence

Having access to reliable market intelligence is highly important in the modern world. Polaris Market Research specializes in providing customized reports with in-depth insights. With our comprehensive reports, we help you make informed decisions and take advantage of emerging opportunities.

## Research Solutions

Polaris Market Research provides syndicated reports covering in-depth analysis of global industries and markets. Our team of expert researchers and analysts tracks all the major market shifts to provide accurate insights. Using our research solutions, companies can develop data-backed strategies.

## Strategic Guidance and Customized Solutions

Our professional consulting services offer actionable recommendations to help your business expand Our consultation offers insights on emerging opportunities, which would help improve decision-making capabilities. We recognize that each business is unique, and our experts create solutions specially designed to meet your specific business model. Our tailored reports take into account your organization’s specific requirements so you can make clear, meaningful decisions.

## Our Clients

Polaris Market Research has supported over 500 organizations in making profitable, data-backed decisions. With deep industry knowledge and accurate forecasting, our research solutions help businesses uncover untapped potential and drive measurable growth.

## Why Choose Polaris Market Research?

Polaris Market Research keeps your business one step ahead of the competition with clear and actionable market insights.

## What Our Reports Provide?

- Our reports cover the latest information on all market segments and primary products and services.

- We provide in-depth geographic analysis for each region and country covered in the report.

- Research reports consist of information on the current and future trends and how they impact your business.

- Our studies utilize more than 70 reliable data sources to provide comprehensive and accurate insights.

## How Do We Support You?

- We aim to achieve results that are timely, effective, and meaningful.

- Our solutions are crafted to lead successful digital transformations tailored to your specific requirements.

## Your Data is Secure with Us

- We maintain rigorous data security protocols to protect your data.

- Your sensitive data is always secure with us.

## Clients Testimonials

Thank you very much for receiving useful information. Thanks to you and your report, I was able to create a very useful report! I think there is something to ask in the future as well.

- Arthur D Little

It was a genuine happiness to work with such a proficient team. Everything went very pleasingly, right from the first contact, whose reply was immediate and transparent, to the implementation of the report, which we greatly appreciated! Thanks to Polaris Market Research and their qualified team for this hassle-free project.

- Client Relations Director

Polaris Market Research is a very talented research association that can offer you quality, trustworthy, and timely data. With a strong knowledge of research and analysis, balanced with a real-world understanding of the industry, they have helped us drive our sales forward!

- Customer Insights Manager

Quick, adaptable, and comfortable to work with. Polaris Market Research provided us with an excellent level of survey development, analysis, and research ahead of the agenda. Ultimately, the team delivers as promised and more. We look forward to working with them in the future, and it is also highly advised to everyone looking for research and analysis services.

- Market Development Team

We thank you and the entire team once again for all the help in dragging our research project together recently. Multiple factors of this project made it challenging. However, the Polaris Market Research team overcame them and delivered significant market insights. Thank you all for all your support. We are glad we worked together.

- Customer & Employee Experience Head

A big thanks to the Polaris Market Research. Your team thoroughly understood what we wanted to accomplish right from the beginning of the project. The data provided to us was concise yet complete. Also, the report you delivered not only covered the details we had specified but also possessed additional observations that would be beneficial to us. We highly recommend Polaris Market Research to everyone out there.

- Leading Pharmaceutical Company

Thank you very much for receiving useful information. Thanks to you and your report, I was able to create a very useful report! I think there is something to ask in the future as well.

- Arthur D Little

It was a genuine happiness to work with such a proficient team. Everything went very pleasingly, right from the first contact, whose reply was immediate and transparent, to the implementation of the report, which we greatly appreciated! Thanks to Polaris Market Research and their qualified team for this hassle-free project.

- Client Relations Director

Polaris Market Research is a very talented research association that can offer you quality, trustworthy, and timely data. With a strong knowledge of research and analysis, balanced with a real-world understanding of the industry, they have helped us drive our sales forward!

- Customer Insights Manager

Quick, adaptable, and comfortable to work with. Polaris Market Research provided us with an excellent level of survey development, analysis, and research ahead of the agenda. Ultimately, the team delivers as promised and more. We look forward to working with them in the future, and it is also highly advised to everyone looking for research and analysis services.

- Market Development Team

We thank you and the entire team once again for all the help in dragging our research project together recently. Multiple factors of this project made it challenging. However, the Polaris Market Research team overcame them and delivered significant market insights. Thank you all for all your support. We are glad we worked together.

- Customer & Employee Experience Head

A big thanks to the Polaris Market Research. Your team thoroughly understood what we wanted to accomplish right from the beginning of the project. The data provided to us was concise yet complete. Also, the report you delivered not only covered the details we had specified but also possessed additional observations that would be beneficial to us. We highly recommend Polaris Market Research to everyone out there.

- Leading Pharmaceutical Company

Thank you very much for receiving useful information. Thanks to you and your report, I was able to create a very useful report! I think there is something to ask in the future as well.

- Arthur D Little

- 1

- 2

- 3

- 4

- 5

- 6

## Latest Published Reports

-

[**Automated Guided Vehicle (AGV) Market Share, Size, Trends, Industry Analysis Report, By Type (Tow Ve ...**](https://www.polarismarketresearch.com/industry-analysis/automated-guided-vehicle-market)

What is the Current Market Size?

The global automated guided vehicle (AGV) market was valued at USD 6.34 Billion in 2024 and is expected to grow at ...

[Read More](https://www.polarismarketresearch.com/industry-analysis/automated-guided-vehicle-market)

-

[**Unmanned Surface Vehicle Market Share, Size, Trends, Industry Analysis Report, By Size (Extra-Large ...**](https://www.polarismarketresearch.com/industry-analysis/unmanned-surface-vehicle-market)

What is the Current Market Size?

The global unmanned surface vehicle market size and share was valued at USD 2.99 billion in 2024 and is expected t ...

[Read More](https://www.polarismarketresearch.com/industry-analysis/unmanned-surface-vehicle-market)

-

[**Large Molecule Drug Substance CDMO Market Size, Share, Trends, Industry Analysis Report By Product ( ...**](https://www.polarismarketresearch.com/industry-analysis/large-molecule-drug-substance-cdmo-market)

Overview

The global large molecule drug substance CDMO market size was valued at USD 51.89 billion in 2024, growing at a CAGR of 7.64% from 2025 to ...

[Read More](https://www.polarismarketresearch.com/industry-analysis/large-molecule-drug-substance-cdmo-market)

-

[**Non-specific Endonucleases Market Size, Share, Trends, Industry Analysis Report By Product (Recombin ...**](https://www.polarismarketresearch.com/industry-analysis/non-specific-endonucleases-market)

Overview

The global non-specific endonucleases market size was valued at USD 353.60 million in 2024, growing at a CAGR of 6.15% from 2025 to 2034. ...

[Read More](https://www.polarismarketresearch.com/industry-analysis/non-specific-endonucleases-market)

-

[**AI in Radiology Market Size, Share, Trends, Industry Analysis Report By Component, By Modality, By D ...**](https://www.polarismarketresearch.com/industry-analysis/ai-in-radiology-market)

Overview

The global AI in radiology market size was valued at USD 1.55 billion in 2024, growing at a CAGR of 38.31% from 2025 to 2034. Growing prev ...

[Read More](https://www.polarismarketresearch.com/industry-analysis/ai-in-radiology-market)

-

[**NUT Midline Carcinoma Treatment Market Size, Share, Trends, Industry Analysis Report By Treatment (C ...**](https://www.polarismarketresearch.com/industry-analysis/nut-midline-carcinoma-treatment-market)

Overview

The global NUT midline carcinoma treatment market size was valued at USD 21.30 billion in 2024, growing at a CAGR of 14.3% from 2025 to 20 ...

[Read More](https://www.polarismarketresearch.com/industry-analysis/nut-midline-carcinoma-treatment-market)

[Browse All Published Reports](https://www.polarismarketresearch.com/publish-report-list)

[Browse All Press Releases](https://www.polarismarketresearch.com/press-releases)

© 2025 Polaris Market Research and Consulting. All rights reserved

## SBR Latex Applications

- [Press Releases](https://www.polarismarketresearch.com/press-releases)

- [Blog](https://www.polarismarketresearch.com/blogs)

- [About](https://www.polarismarketresearch.com/blog/styrene-butadiene-rubber-latex-is-a-versatile-material-for-modern-manufacturing#)

[Who We Are](https://www.polarismarketresearch.com/who-we-are) [Why Select Us](https://www.polarismarketresearch.com/why-select-us) [Careers](https://www.polarismarketresearch.com/careers)

- [Contact](https://www.polarismarketresearch.com/contact)

- Services

[Consulting](https://www.polarismarketresearch.com/services/consulting) [Other Services](https://www.polarismarketresearch.com/services/other-services) [Research](https://www.polarismarketresearch.com/services/research)

# Why Styrene Butadiene Rubber (SBR) Latex is A Versatile Material for Modern Manufacturing?

Published Date:

19-May-2025

In the diverse landscape of synthetic rubber products, styrene butadiene rubber (SBR) latex has gained prominence as a go-to synthetic emulsion. With its superior mechanical properties and wide-ranging application potential, SBR latex has become indispensable in sectors such as construction, paper manufacturing, and textiles. Its unique combination of durability, flexibility, and affordability continues to open new avenues for innovation, especially amid growing sustainability and performance demands.

In this blog post, we explore the composition, production process, and key characteristics of SBR latex. In addition, we highlight the recent trends and innovations in SBR latex and their expanding applications across various industries. Read on!

## What Is SBR Latex?

SBR latex is a synthetic compound made by chemically combining styrene and butadiene monomers. It's a liquid, water-based emulsion, meaning it's mixed with water to create a slurry. In SBR latex, the polymer chains are modified with carboxyl groups to help them bond with the inorganic materials in concrete and cement.

The ratio of styrene to butadiene in SBR latex is often adjusted to get specific properties such as flexibility, tensile strength, and chemical resistance. Higher styrene content offers improved hardness and strength, while more butadiene enhances elasticity and low-temperature performance. As a result, manufacturers can easily tailor SBR latex for specific industrial applications.

## Key Properties of SBR Latex

Latex made from **[styrene butadiene rubber](https://www.polarismarketresearch.com/industry-analysis/styrene-butadiene-rubber-sbr-market)** possesses several desirable characteristics that make it an ideal material for various industrial and commercial applications. These include:

**Excellent Adhesion**: SBR latex offers excellent adhesion to a wide variety of substrates, including metal, concrete, fabric, and paper. The polar styrene groups in SBR latex interact favorably with various surfaces, forming a strong and durable bond. This makes it especially beneficial in the construction, textiles, and packaging industries.

**High Flexibility and Elongation**: The butadiene content enables SBR latex to retain exceptional flexibility and elongation properties even after curing or drying. This makes SBR latex highly resistant to cracking under stress or movement, which is ideal for applications where surfaces undergo expansion, contraction, or vibration.

**Abrasion and Wear Resistance**: Another desirable property of SBR latex is its high resistance to physical wear and abrasion. This makes it suitable for coatings and composites exposed to surface stress, rough contact, or mechanical movement.

**Water Resistance and Moisture Barrier**: Although SBR latex is a water-based emulsion, its hydrophobic film gives it water-resistant properties. This is critical in waterproofing systems, cement admixtures, and coatings designed to reduce permeability.

**Chemical Resistance**: While SBR latex is less resistant to oils and hydrocarbons compared to **[nitrile butadiene rubber (NBR)](https://www.polarismarketresearch.com/industry-analysis/nitrile-butadiene-rubber-market)**, it exhibits moderate resistance to dilute acids, bases, and salts. The chemical stability of this polymer emulsion in various pH environments makes it reliable for applications in coatings and adhesives exposed to mild chemical conditions.

**Low Temperature Flexibility**: SBR latex can maintain its flexibility in low-temperature conditions. This property makes the material suitable for use in colder climates or in applications where temperature fluctuations are frequent.

## Industrial Uses of SBR Latex

The versatility of SBR latex is evident in its wide range of applications across various sectors. Below, we’ve detailed some of the most common uses:

**Paper Coating**: SBR latex finds widespread usage in the paper industry as a coating binder. Its use improves the printability, brightness, and smoothness of paper surfaces. In addition, its high binding strength ensures uniform pigment distribution, making it a staple for coated and glossy paper products.

**Carpet Backing**: SBR latex acts as a critical backing adhesive in carpet manufacturing. It offers the required elasticity and strength to keep the carpet intact when exposed to repeated stress. Additionally, it imparts dimensional stability in carpets and makes them resistance to wear and tear.

**Construction and Cement Modification**: SBR latex plays a crucial role in cementitious applications, such as concrete repair, waterproofing membranes, and tile adhesives. The ability of the synthetic compound to improve bonding, flexural strength, and water resistance makes it an essential additive in **[concrete repair mortars](https://www.polarismarketresearch.com/industry-analysis/concrete-repair-mortars-market).**

**Textile Industry**: In the textile industry, the compound finds applications as a binder for nonwoven fabrics and as a finishing agent to improve performance. It enhances texture, durability, and resistance to environmental factors in various textile applications.

**Adhesives and Sealants**: SBR latex is also used in the production of pressure-sensitive adhesives and general-purpose sealants due to its strong bonding ability and water resistance. Its use helps achieve a balance between adhesion and flexibility.

## Recent Innovations and Trends

Here’s a look at some recent trends and innovations shaping the SBR latex landscape:

**Bio-Based Alternatives**: In recent years, a greater emphasis has been given to using partially bio-based styrene and butadiene monomers to lower the carbon footprint of SBR latex production. While commercial-scale implementation remains a challenge, bio-based SBR formulations are gaining interest.

**Nanotechnology Integration**: The incorporation of nanomaterials like nano-silica and graphene is being explored to improve the thermal and mechanical properties of SBR latex composites. These hybrid formulations offer excellent crack resistance and strength for demanding construction applications.

**Digital Printing and Specialty Coatings**: With digital printing technology gaining increased traction, paper coatings need to be fast-drying inks and smooth finishes. Manufacturers are modifying the properties of SBR latex to cater to these changing requirements.

**Low-VOC and Odor-Free Formulations**: The implementation of stricter environmental regulations and shifting consumer preferences have prompted manufacturers to develop low-VOC, odorless SBR latex products for indoor applications.

## The Road Ahead

The demand for SBR latex is growing, driven by innovation and evolving consumer needs. With enhancements in formulations and processing techniques and a rising focus on environmental compliance, the material is expected to gain more traction in high-performance and sustainable applications. For businesses across the textile, automotive, paper, and construction sectors, SBR latex remains a valuable and adaptable material worth investing in.

* * *

#### **Related Blogs**

Published Date:

27-Oct-2025

[Drinking Water Adsorbents Market: Providing Safe and Clean Drinking Water](https://www.polarismarketresearch.com/blog/drinking-water-adsorbents-market-providing-safe-and-clean-drinking-water)

[Read More](https://www.polarismarketresearch.com/blog/drinking-water-adsorbents-market-providing-safe-and-clean-drinking-water)

Published Date:

29-Apr-2025

[Profiling Top 10 Companies Offering Advanced and Energy-Efficient HVAC Systems in 2025](https://www.polarismarketresearch.com/blog/top-10-companies-offering-advanced-and-energy-efficient-hvac-systems)

[Read More](https://www.polarismarketresearch.com/blog/top-10-companies-offering-advanced-and-energy-efficient-hvac-systems)

Published Date:

08-Jan-2025

[Top 5 Companies Driving Change in Carbon Nanotube Market in 2025](https://www.polarismarketresearch.com/blog/top-5-companies-driving-change-in-carbon-nanotube-market-in-2025)

[Read More](https://www.polarismarketresearch.com/blog/top-5-companies-driving-change-in-carbon-nanotube-market-in-2025)

Published Date:

23-Nov-2023

[Dissolving Pulp Market: An Innovative Procedure for Manufacturing Paper and Rayon](https://www.polarismarketresearch.com/blog/dissolving-pulp-market-share)

[Read More](https://www.polarismarketresearch.com/blog/dissolving-pulp-market-share)

Published Date:

30-Oct-2025

[Fresh Food Packaging Market: Minimizing Nutrient Loss](https://www.polarismarketresearch.com/blog/fresh-food-packaging-market-minimizing-nutrient-loss)

[Read More](https://www.polarismarketresearch.com/blog/fresh-food-packaging-market-minimizing-nutrient-loss)

Published Date:

27-Aug-2024

[Building Better Futures: How MDI Manufacturers Are Redefining Foam Insulation](https://www.polarismarketresearch.com/blog/mdi-manufacturers)

[Read More](https://www.polarismarketresearch.com/blog/mdi-manufacturers)

Published Date:

27-Oct-2025

[Drinking Water Adsorbents Market: Providing Safe and Clean Drinking Water](https://www.polarismarketresearch.com/blog/drinking-water-adsorbents-market-providing-safe-and-clean-drinking-water)

[Read More](https://www.polarismarketresearch.com/blog/drinking-water-adsorbents-market-providing-safe-and-clean-drinking-water)

Published Date:

29-Apr-2025

[Profiling Top 10 Companies Offering Advanced and Energy-Efficient HVAC Systems in 2025](https://www.polarismarketresearch.com/blog/top-10-companies-offering-advanced-and-energy-efficient-hvac-systems)

[Read More](https://www.polarismarketresearch.com/blog/top-10-companies-offering-advanced-and-energy-efficient-hvac-systems)

Published Date:

08-Jan-2025

[Top 5 Companies Driving Change in Carbon Nanotube Market in 2025](https://www.polarismarketresearch.com/blog/top-5-companies-driving-change-in-carbon-nanotube-market-in-2025)

[Read More](https://www.polarismarketresearch.com/blog/top-5-companies-driving-change-in-carbon-nanotube-market-in-2025)

Published Date:

23-Nov-2023

[Dissolving Pulp Market: An Innovative Procedure for Manufacturing Paper and Rayon](https://www.polarismarketresearch.com/blog/dissolving-pulp-market-share)

[Read More](https://www.polarismarketresearch.com/blog/dissolving-pulp-market-share)

Published Date:

30-Oct-2025

[Fresh Food Packaging Market: Minimizing Nutrient Loss](https://www.polarismarketresearch.com/blog/fresh-food-packaging-market-minimizing-nutrient-loss)

[Read More](https://www.polarismarketresearch.com/blog/fresh-food-packaging-market-minimizing-nutrient-loss)

Published Date:

27-Aug-2024

[Building Better Futures: How MDI Manufacturers Are Redefining Foam Insulation](https://www.polarismarketresearch.com/blog/mdi-manufacturers)

[Read More](https://www.polarismarketresearch.com/blog/mdi-manufacturers)

Published Date:

27-Oct-2025

[Drinking Water Adsorbents Market: Providing Safe and Clean Drinking Water](https://www.polarismarketresearch.com/blog/drinking-water-adsorbents-market-providing-safe-and-clean-drinking-water)

[Read More](https://www.polarismarketresearch.com/blog/drinking-water-adsorbents-market-providing-safe-and-clean-drinking-water)

Published Date:

29-Apr-2025

[Profiling Top 10 Companies Offering Advanced and Energy-Efficient HVAC Systems in 2025](https://www.polarismarketresearch.com/blog/top-10-companies-offering-advanced-and-energy-efficient-hvac-systems)

[Read More](https://www.polarismarketresearch.com/blog/top-10-companies-offering-advanced-and-energy-efficient-hvac-systems)

Published Date:

08-Jan-2025

[Top 5 Companies Driving Change in Carbon Nanotube Market in 2025](https://www.polarismarketresearch.com/blog/top-5-companies-driving-change-in-carbon-nanotube-market-in-2025)

[Read More](https://www.polarismarketresearch.com/blog/top-5-companies-driving-change-in-carbon-nanotube-market-in-2025)

- 1

- 2

## Industries

## [Healthcare](https://www.polarismarketresearch.com/industries/healthcare)

## [Chemicals & Material](https://www.polarismarketresearch.com/industries/chemicals-and-material)

## [Energy Power & Utilities](https://www.polarismarketresearch.com/industries/energy-power-and-utilities)

## [Information & Communication Technology](https://www.polarismarketresearch.com/industries/information-and-communication-technology)

## [Electronics & Semiconductors](https://www.polarismarketresearch.com/industries/electronics-and-semiconductors)

## [Automotive & Transportation](https://www.polarismarketresearch.com/industries/automotive-and-transportation)

## [Food & Beverages](https://www.polarismarketresearch.com/industries/food-and-beverages)

## [Construction & Mining](https://www.polarismarketresearch.com/industries/construction-and-mining)

## [Aerospace & Defense](https://www.polarismarketresearch.com/industries/aerospace-and-defense)

## [Consumer Goods & Services](https://www.polarismarketresearch.com/industries/consumer-goods-and-services)

## [Nextgen Technology](https://www.polarismarketresearch.com/industries/nextgen-technology)

#### Latest Blogs

04-Nov-2025

[Healthcare Command Centers Market: Streamlining Operations](https://www.polarismarketresearch.com/blog/healthcare-command-centers-market-streamlining-operations)

04-Nov-2025

[Event Management Market: Creating Enjoyable Experiences](https://www.polarismarketresearch.com/blog/event-management-market-creating-enjoyable-experiences)

04-Nov-2025

[Small Modular Reactor Market: Providing Clean Energy](https://www.polarismarketresearch.com/blog/small-modular-reactor-market-providing-clean-energy)

© 2025 Polaris Market Research and Consulting. All rights reserved

## Edge AI Market Insights

- [Press Releases](https://www.polarismarketresearch.com/press-releases)

- [Blog](https://www.polarismarketresearch.com/blogs)

- [About](https://www.polarismarketresearch.com/industry-analysis/edge-ai-market#)

[Who We Are](https://www.polarismarketresearch.com/who-we-are) [Why Select Us](https://www.polarismarketresearch.com/why-select-us) [Careers](https://www.polarismarketresearch.com/careers)

- [Contact](https://www.polarismarketresearch.com/contact)

- Services

[Consulting](https://www.polarismarketresearch.com/services/consulting) [Other Services](https://www.polarismarketresearch.com/services/other-services) [Research](https://www.polarismarketresearch.com/services/research)

# Edge AI Market Size, Share, Trends, & Industry Analysis By Component (Hardware, Network, Edge Cloud Infrastructure, Software, and Support Services), By Industry, and By Region – Market Forecast, 2025–2034

- Published Date:Jul-2025

- Pages: 129

- Format: PDF

- Report ID: PM5936

- Base Year: 2024

- Historical Data: 2020-2023

- [Description](https://www.polarismarketresearch.com/industry-analysis/edge-ai-market)

- [Table of\\

Contents](https://www.polarismarketresearch.com/industry-analysis/edge-ai-market/toc)

- [Analysis Type](https://www.polarismarketresearch.com/industry-analysis/edge-ai-market/analysis-type)

- [Research\\

Methodology](https://www.polarismarketresearch.com/research-methodology)

- [Request Free Sample](https://www.polarismarketresearch.com/industry-analysis/edge-ai-market/request-for-sample)

## MarketOverview

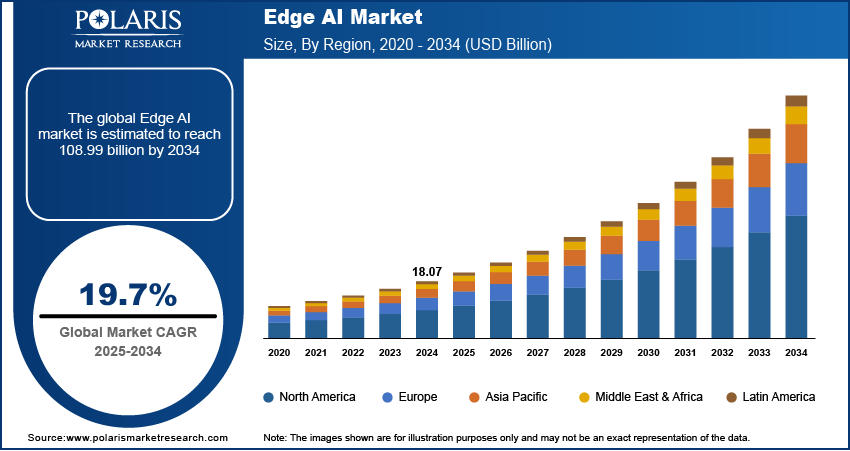

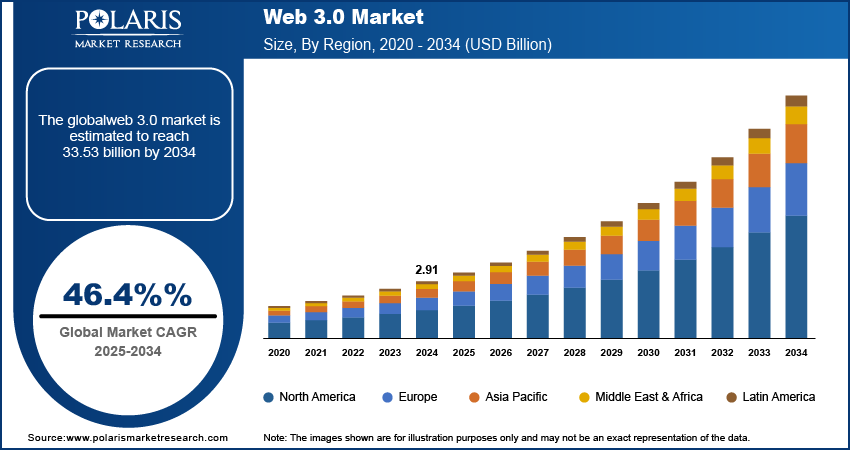

The edge AI market size was valued at USD 18.07 billion in 2024, growing at a CAGR of 19.7% during 2025–2034. Rise of 5G and next-gen connectivity coupled with global semiconductor and AI R&D investment is driving the market growth.

Edge AI refers to the deployment of [**artificial intelligence**](https://www.polarismarketresearch.com/industry-analysis/artificial-intelligence-market) algorithms locally on hardware devices, allowing real-time data processing without relying on cloud infrastructure. It enables devices such as smartphones, sensors, surveillance cameras, drones, and [**industrial robotics**](https://www.polarismarketresearch.com/industry-analysis/industrial-robotics-market) to execute AI models directly on the device itself. This reduces latency, lowers bandwidth costs, and enhances data privacy. These capabilities make edge AI suitable for critical applications where immediate decision-making is essential, including autonomous vehicles, predictive maintenance, and remote healthcare diagnostics.

The growing reliance on intelligent systems in sectors such as manufacturing, [**automotive**](https://www.polarismarketresearch.com/industry-analysis/automotive-market), and healthcare is fueling the need for distributed AI architecture. Edge AI offers decentralized intelligence, which ensures real-time responsiveness and uninterrupted operation even during network failures. In healthcare, wearable and diagnostic devices edge AI track vitals and deliver alerts without cloud dependence. Also, in manufacturing environments, edge AI enables predictive analytics and process automation that significantly reduces downtime and increases operational efficiency.

**To Understand More About this Research:** [Request a Free Sample Report](https://www.polarismarketresearch.com/industry-analysis/washed-silica-sand-market/request-for-sample)

Governments worldwide are focusing on strengthening urban infrastructure through digitalization initiatives, which in turn is increasing the demand for edge AI technologies in public systems. For instance, Indonesia launched the “100 Smart Cities Movement” as part of its comprehensive urban digitalization strategy. This program is designed to improve quality of life in cities through data-centric approaches, while addressing the country's projected urbanization challenge by 2045, nearly 83% of Indonesia’s population is expected to reside in urban areas. Also, in August 2024, the Government of India approved 12 new industrial smart city projects with a combined infrastructure development cost of USD 3.43 billion. These projects are aimed at building advanced trunk infrastructure to support technology-led urban growth. The integration of edge AI into such initiatives allows public service systems to function more autonomously, securely, and efficiently, further propelling its adoption in national smart city programs.

In addition, the rising demand for intelligent automation and real-time decision-making is further accelerating the edge AI market growth. Organizations are investing in edge AI platforms to modernize legacy infrastructure, reduce operational risks, and support predictive and autonomous operations. This shift is improving overall process control and data visibility across decentralized networks.

## Industry Dynamics

### Rise of 5G and Next-Gen Connectivity

The global rollout of 5G infrastructure is laying a transformative foundation for the deployment of edge AI across numerous time-sensitive applications. According to 5G Americas, global 5G connections rose sharply to 1.76 billion in 2023, with a net increase of 700 million connections in that year alone. This number is forecast to grow to 7.9 billion by 2028, reflecting a substantial acceleration in infrastructure expansion and network accessibility. These connectivity advancements are strengthening the viability of deploying AI algorithms directly on devices, reducing the need for cloud round-trips. Thus, edge AI is becoming integral to enabling more intelligent, localized, and autonomous system behaviors across critical environments that requires high performance, strong security, and continuous uptime.

The increased bandwidth and reduced latency offered by [**5G services**](https://www.polarismarketresearch.com/industry-analysis/5g-services-market) are allowing edge devices to collect, process, and act on information with minimal delay. This capability is helping industries to optimize operations through predictive maintenance, real-time quality control, and dynamic system adjustments. Additionally, the growing shift toward [**Industry 4.0**](https://www.polarismarketresearch.com/industry-analysis/industry-4-market), combined with rising adoption of smart infrastructure and remote monitoring, is further propelling the growth of the market. Enterprises prioritizing faster insights and lower data transfer costs are driving the demand for 5G and edge AI, providing high responsiveness, improved efficiency, and scalable solutions across real-time applications.

### Global Semiconductor and AI R&D Investment

The surge in investments in semiconductor technologies and artificial intelligence research and development is accelerating the market growth. According to the United Nations Conference on Trade and Development (UNCTAD), the global AI market is projected to reach approximately USD 4.8 trillion by 2033, a twenty-five-fold expansion in a decade. This growth reflects the increasing importance of AI in transforming operational models across industries and reinforces the need for robust edge AI infrastructure. Legislative frameworks such as the US CHIPS and Science Act and the EU’s Digital Europe Programme are contributing to the development of advanced fabrication capabilities, AI accelerators, and application-specific integrated circuits (ASICs) designed for edge environments. Therefore, the rising funding, policy support, and technological advancement is boosting the edge AI market growth.

The convergence of AI and semiconductor advancements is unlocking new possibilities for real-time analytics, smart sensing, and autonomous system control outside traditional data centers. Edge AI, supported by cutting-edge semiconductors, allows data to be processed closer to the source, reducing latency and increasing operational security. The expanding innovation through R&D, venture funding, and public programs is enabling AI-ready edge devices to perform complex machine learning tasks independently. Thus, edge AI is becoming a practical and scalable solution for industries looking to improve efficiency, responsiveness, and data privacy in real-world applications.

## Segmental Insights

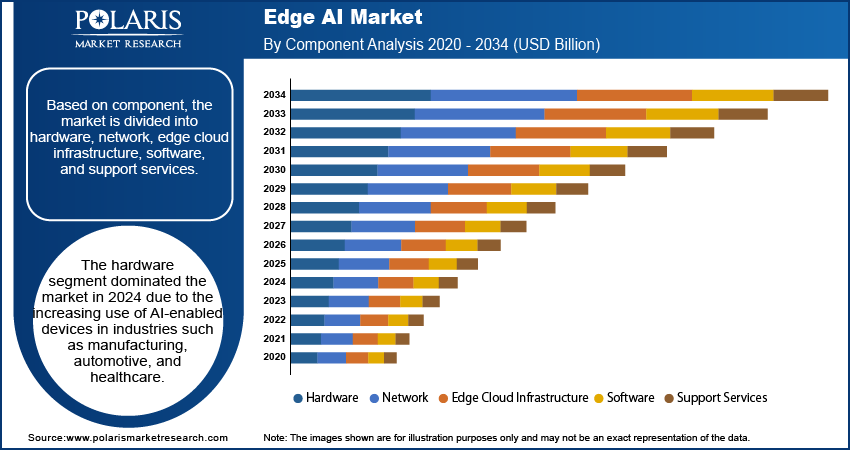

### Component Analysis

The segmentation, based on component includes, hardware, network, edge cloud infrastructure, software, and support services. The hardware segment dominated the market in 2024 due to the increasing use of AI-enabled devices in industries such as manufacturing, automotive, and healthcare. Companies are adopting edge AI chips, sensors, and processing units that allow machines and equipment to analyze data locally without relying on the cloud. These components are essential in running real-time operations, requiring quick decision-making is needed. The growing number of smart cameras, drones, and robots is contributing to the strong demand for edge AI hardware.

The edge cloud infrastructure segment is expected to grow at the fastest rate during the forecast period. Businesses are increasingly combining on-site data processing with cloud-based tools to improve flexibility and data control. This shift is driving the need for edge cloud platforms that support faster decision-making, better data security, and seamless connectivity. Companies in sectors such as logistics and energy are investing in such hybrid infrastructure to support smart operations, optimize workflows, and reduce downtime.

### Industry Analysis

The segmentation, based on industry includes, automotive, manufacturing, healthcare, energy & utility, retail & consumer goods, it & telecom, and others. The automotive segment dominated the market in 2024. This dominance is attributed to the increasing adoption of edge AI into vehicles to support features such as driver assistance, navigation, and in-car personalization. These systems help vehicles process information instantly from sensors and cameras, improving safety and responsiveness. The push toward autonomous driving and connected mobility is pushing manufacturers to invest in edge AI for faster and more secure data processing inside the vehicle. For instance, in October 2024, Infineon introduced the DEEPCRAFT brand for Edge AI software solutions, launching new Ready Models including "directional sound arrival detection" that can trigger various safety enhancements or enable autonomous driving.

The healthcare segment is projected to grow at the fastest pace in the coming years. This growth is attributed to the rising adoption of edge AIin patient monitoring, diagnostics, and portable medical devices. Hospitals and healthcare providers are adopting AI-enabled tools that deliver real-time insights at the point of care. For instance, in June 2024, Anumana collaborated with InfoBionic.Ai integrated Anumana's ECG-AI algorithms validated with Mayo Clinic into InfoBionic’s MoMe ARC platform for remote cardiac telemetry. This integration empowered edge AI in patient monitoring by enabling real-time detection of cardiac conditions such as low ejection fraction directly from wearable ECG devices. These tools help doctors make faster decisions, reduce delays in treatment, and enhance patient outcomes. The growing demand for home-based and remote healthcare services is fueling the need for edge AI solutions that operate independently without constant internet access.

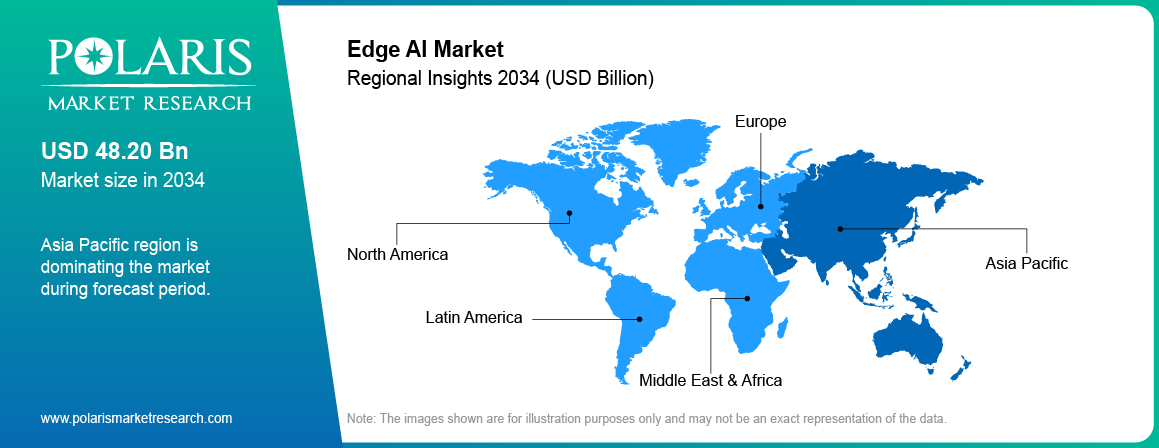

## Regional Analysis

North America Edge AI market accounted for largest global revenue share in 2024, driven by strong presence of large technology firms and a vibrant startup ecosystem. Companies such as Google, Amazon, NVIDIA, and Microsoft are investing heavily in edge-based AI platforms to support real-time computing in sectors including healthcare, retail, automotive, and manufacturing. These organizations are developing AI chips, edge servers, and software frameworks tailored for localized processing, allowing enterprises to deploy intelligent systems with minimal latency. In addition, the rising adoption of edge AI in defense and aerospace is fueling the growth of the market in the region. Defense agencies and military contractors are deploying AI-enabled edge devices for real-time surveillance, secure communication, and autonomous threat detection. This demand is further propelled by national defense modernization programs aimed at integrating AI into tactical and operational platforms.

### The US Edge AI Market Insight

The US, in particular, dominated the regional share in 2024 due to strong support from federal and state-level funding initiatives. Public-private partnerships and R&D grants are fueling innovation in AI-enabled infrastructure across healthcare, transportation, and defense sectors. Government programs are supporting startups and research institutions working on edge AI applications for diagnostic tools, smart public services, and autonomous platforms. For instance, in January 2025 the US government partnered with OpenAI, Oracle, SoftBank, and others to launch the “Stargate Project,” committing up to USD 500 billion over four years to build AI infrastructure starting with an initial USD 100 billion investment in data centers and power systems. These fundings are making it easier for companies to scale new technologies and bring advanced AI models closer to end users. Thus, the advanced technology ecosystem coupled with surge in investment in AI is accelerating the edge AI adoption in the country.

### Asia Pacific Edge AI Market

The Asia Pacific Edge AI market is projected to witness fastest growth during the forecast period attributed to the government-led smart nation programs in countries such as China, India, and Singapore. These countries are integrating AI at the edge into public systems including transport networks, utility grids, and security infrastructure. For instance, in 2024, Singapore introduced Smart Nation 2.0, building on the foundation of Smart Nation 1.0. The updated vision shifts from broad capability development to a more focused approach, using technology to drive national transformation and collective progress. These programs are focused on improving efficiency, citizen safety, and sustainability, and edge AI enables real-time monitoring, autonomous decision-making, and secure data handling. Urban development projects and national digitalization strategies are further expanding the market growth in the region.

Additionally, surge in adoption of industrial automation is further fueling the market growth in the region. Countries such as Japan, South Korea, and China are home to leading manufacturing hubs where companies are adopting edge AI to improve production efficiency, reduce downtime, and manage energy usage. AI-enabled sensors and controllers deployed at the machine level allow factories to detect failures, monitor workflows, and adjust operations in real time. These applications are helping manufacturers stay competitive while meeting high standards for productivity and quality.

### Europe In Edge AI Market Overview

The Europe edge AI market is projected to reach at significant revenue share by 2034. The large-scale funding and [digital transformation](https://www.polarismarketresearch.com/industry-analysis/digital-transformation-market) strategies in the region is propelling the growth of the market. The European Union’s Horizon Europe and Digital Europe Programme are directing capital toward AI research, development, and deployment including edge computing infrastructure. For example, in May 2025, the European Commission committed more than USD 8.25 billion through its Horizon Europe work programme for 2025 to boost the region’s research and innovation landscape. The investment aims to advance scientific breakthroughs, support the EU’s green and digital transitions, and strengthen Europe’s global competitiveness. These initiatives are enabling businesses and research institutions to build specialized edge platforms for use in healthcare, transport, energy, and manufacturing. Investments in edge AI are supporting local innovation ecosystems and helping small to mid-sized enterprises adopt intelligent automation.

Strict data privacy and compliance requirements in Europe are further shaping the adoption of edge AI. Regulations such as the General Data Protection Regulation (GDPR) require that sensitive data be processed and stored locally, which limits reliance on centralized cloud services. Edge AI solutions enable real-time, on-device processing that helps businesses comply with data sovereignty laws while reducing the risk of data breaches. This growing emphasis on regulatory compliance is pushing organizations to implement AI models that operate within controlled, secure environments making edge AI a preferred approach in sectors handling personal or confidential information.

## Key Players & Competitive Analysis Report

The edge AI market is highly competitive and evolving rapidly as companies focus on developing faster, smarter, and more energy-efficient solutions that operate close to data sources. Industry leaders are actively investing in the development of edge-native AI hardware and software tools that handle real-time processing with minimal reliance on centralized data centers. Major players are expanding product portfolios, forming technology alliances, and acquiring specialized AI startups that offer complementary capabilities. Companies are also prioritizing industry-specific solutions tailored to applications in automotive, industrial automation, healthcare, and smart devices. In addition, the integration of 5G, IoT, and [**machine learning platform**](https://www.polarismarketresearch.com/press-releases/machine-learning-platforms-market) is pushing organizations to deliver AI solutions that balance speed, security, and performance at the network edge.

Prominent players operating in the edge AI market include Amazon Web Services, Inc., Apple Inc., Google LLC (Alphabet Inc.), Huawei Technologies Co., Ltd., IBM Corporation, Intel Corporation, MediaTek Inc., Microsoft Corporation, NVIDIA Corporation, Qualcomm Technologies, Inc., Samsung Electronics Co., Ltd., Siemens AG, Synaptics Incorporated, Tesla, Inc., and Xilinx, Inc.

## Key Players

- Amazon Web Services, Inc.

- Apple Inc.

- Google LLC (Alphabet Inc.)

- [Huawei Technologies Co., Ltd.](https://www.huawei.com/en/)

- IBM Corporation

- Intel Corporation

- [MediaTek Inc.](https://www.mediatek.com/)

- Microsoft Corporation

- NVIDIA Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Siemens AG

- Synaptics Incorporated

- Tesla, Inc.

- Xilinx, Inc.

## Industry Developments

**June 2025:** Google introduced the Gemma 3n lightweight generative AI model that runs offline on edge devices with 2 GB RAM, supporting multimodal tasks including image, audio, video, and text processing. This enabled secure, privacy-preserving AI use in low-resource environments such as mobile devices and IoT nodes.

**May 2025:** EDGE Group launched the Group AI Accelerator to scale AI innovation across defense and industrial manufacturing sectors via a centralized Centre of Excellence. The program also aimed to nurture local AI talent and accelerate product readiness in harsh and security-sensitive environments.

**December 2024:** Synopsys and SiMa.ai announced a strategic partnership to deliver a silicon and software platform for automotive edge AI applications accelerating SoC development for ADAS and infotainment systems. The joint solution targeted low-latency inferencing and energy efficiency, critical for autonomous features in next-gen vehicles.

**July 2024:** NTT DATA launched its Ultralight Edge AI platform, offering a fully managed service that auto-discovers IT/OT devices and orchestrates lightweight AI agents for real-time insights. It supported real-time anomaly detection, predictive maintenance, and seamless cloud integration with edge scalability.

## Edge AI Market Segmentation

**By Component Outlook (Revenue, USD Billion, 2020** **–** **2034)**

- Hardware

- Network

- Edge Cloud Infrastructure

- Software

- Support Services

**By Industry Outlook (Revenue, USD Billion, 2020–2034)**

- Automotive

- Manufacturing

- Healthcare

- Energy & Utility

- Retail & Consumer Goods

- IT & Telecom

- Others

**By Regional Outlook (Revenue, USD Billion, 2020–2034)**

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

## Edge AI Market Report Scope

| | |

| --- | --- |

| **Report Attributes** | **Details** |

| **Market Size in 2024** | USD 18.07 Billion |

| **Market Size in 2025** | USD 21.55 Billion |

| **Revenue Forecast by 2034** | USD 108.99 Billion |

| **CAGR** | 19.7% from 2025 to 2034 |

| **Base Year** | 2024 |

| **Historical Data** | 2020–2023 |

| **Forecast Period** | 2025–2034 |

| **Quantitative Units** | Revenue in USD Billion and CAGR from 2025 to 2034 |

| **Report Coverage** | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| **Segments Covered** | - By Component

- By Industry |

| **Regional Scope** | - North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa |

| **Competitive Landscape** | - Edge AI Industry Trend Analysis (2024)

- Company Profiles/Industry participants profiling includes company overview, financial information, product/service benchmarking, and recent developments |

| **Report Format** | - PDF + Excel |

| **Customization** | Report customization as per your requirements with respect to countries, regions, and segmentation. |

### FAQ's

1\. What are the edge AI market statistics?

The global market size was valued at USD 18.07 billion in 2024 and is projected to grow to USD 108.99 billion by 2034.

2\. What is the growth rate of the edge AI market value?

The global market is projected to register a CAGR of 19.7% during the forecast period.

3\. Which region dominated the global market share in 2024?

North America dominated the market share in 2024.

4\. Who are the key players in the market?

A few of the key players in the market are Amazon Web Services, Inc., Apple Inc., Google LLC (Alphabet Inc.), Huawei Technologies Co., Ltd., IBM Corporation, Intel Corporation, MediaTek Inc., Microsoft Corporation, NVIDIA Corporation, Qualcomm Technologies, Inc., Samsung Electronics Co., Ltd., Siemens AG, Synaptics Incorporated, Tesla, Inc., and Xilinx, Inc.

5\. Which segment, by component, dominated the edge AI market revenue share in 2024?

The hardware segment dominated the market share in 2024.

6\. Which segment, by industry, is expected to witness the fastest growth during the forecast period?

The automotive segment is expected to witness the fastest growth during the forecast period.

### Table of Contents

**1\. Introduction**

1.1. Report Description

1.1.1. Objectives of the Study

1.1.2. Market Scope

1.1.3. Assumptions

1.2. Stakeholders

**2\. Executive Summary**

2.1. Market Highlights

**3\. Research Methodology**

3.1. Overview

3.1.1. Data Mining

3.2. Data Sources

3.2.1. Primary Sources

3.2.2. Secondary Sources

**4\. Global Edge AI Market Insights**

4.1. Edge AI Market – Market Snapshot

4.2. Edge AI Market Dynamics

4.2.1. Drivers and Opportunities

4.2.1.1. Rise of 5G and Next-Gen Connectivity

4.2.1.2. Global Semiconductor and AI R&D Investment

4.2.2. Restraints and Challenges

4.2.2.1. High Hardware and Development Costs

4.2.2.2. Data Privacy and Security Risks

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers (Moderate)

4.3.2. Threats of New Entrants: (Low)

4.3.3. Bargaining Power of Buyers (Moderate)

4.3.4. Threat of Substitute (Moderate)

4.3.5. Rivalry among existing firms (High)

4.4. PESTEL Analysis

4.5. Edge AI Market Trends

4.6. Value Chain Analysis

**5\. Global Edge AI Market, by Component**

5.1. Key Findings

5.2. Introduction

5.2.1. Global Edge AI Market, by Component, 2020-2034 (USD Billion)

5.3. Hardware

5.3.1. Global Edge AI Market, by Hardware, by Region, 2020-2034 (USD Billion)

5.4. Network

5.4.1.1. Global Edge AI Market, by Network, by Region, 2020-2034 (USD Billion)

5.4.2. Global Edge AI Market, by Component, 2020-2034 (USD Billion)

5.5. Edge Cloud Infrastructure

5.5.1.1. Global Edge AI Market, by Edge Cloud Infrastructure, by Region, 2020-2034 (USD Billion)

5.6. Software

5.6.1. Global Edge AI Market, by Software, by Region, 2020-2034 (USD Billion)

5.7. Support Services

5.7.1. Global Edge AI Market, by Support Services, by Region, 2020-2034 (USD Billion)

**6\. Global Edge AI Market, by Industry**

6.1. Key Findings

6.2. Introduction

6.2.1. Global Edge AI Market, by Industry, 2020-2034 (USD Billion)

6.3. Automotive

6.3.1. Global Edge AI Market, by Automotive, by Region, 2020-2034 (USD Billion)

6.4. Manufacturing

6.4.1. Global Edge AI Market, by Manufacturing, by Region, 2020-2034 (USD Billion)

6.5. Healthcare

6.5.1. Global Edge AI Market, by Healthcare, by Region, 2020-2034 (USD Billion)

6.6. Energy & Utility

6.6.1. Global Edge AI Market, by Energy & Utility, by Region, 2020-2034 (USD Billion)

6.7. Retail & Consumer Goods

6.7.1. Global Edge AI Market, by Retail & Consumer Goods, by Region, 2020-2034 (USD Billion)

6.8. IT & Telecom

6.8.1. Global Edge AI Market, by IT & Telecom, by Region, 2020-2034 (USD Billion)

6.9. Others

6.9.1. Global Edge AI Market, by Others, by Region, 2020-2034 (USD Billion)

**7\. Global Edge AI Market, by Geography**

7.1. Key Findings

7.2. Introduction

7.2.1. Edge AI Market Assessment, By Geography, 2020-2034 (USD Billion)

7.3. Edge AI Market – North America

7.3.1. North America: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.3.2. North America: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.3.3. Edge AI Market – U.S.

7.3.3.1. U.S.: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.3.3.2. U.S.: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.3.4. Edge AI Market – Canada

7.3.4.1. Canada: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.3.4.2. Canada: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4. Edge AI Market – Europe

7.4.1. Europe: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.2. Europe: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.3. Edge AI Market – UK

7.4.3.1. UK: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.3.2. UK: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.4. Edge AI Market – France

7.4.4.1. France: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.4.2. France: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.5. Edge AI Market – Germany

7.4.5.1. Germany: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.5.2. Germany: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.6. Edge AI Market – Italy

7.4.6.1. Italy: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.6.2. Italy: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.7. Edge AI Market – Spain

7.4.7.1. Spain: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.7.2. Spain: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.8. Edge AI Market – Netherlands

7.4.8.1. Netherlands: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.8.2. Netherlands: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.9. Edge AI Market – Russia

7.4.9.1. Russia: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.9.2. Russia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.4.10. Edge AI Market – Rest of Europe

7.4.10.1. Rest of Europe: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.4.10.2. Rest of Europe: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5. Edge AI Market – Asia Pacific

7.5.1. Asia Pacific: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.2. Asia Pacific: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.3. Edge AI Market – China

7.5.3.1. China: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.3.2. China: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.4. Edge AI Market – India

7.5.4.1. India: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.4.2. India: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.5. Edge AI Market – Malaysia

7.5.5.1. Malaysia: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.5.2. Malaysia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.6. Edge AI Market – Japan

7.5.6.1. Japan: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.6.2. Japan: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.7. Edge AI Market – Indonesia

7.5.7.1. Indonesia: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.7.2. Indonesia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.8. Edge AI Market – South Korea

7.5.8.1. South Korea: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.8.2. South Korea: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.9. Edge AI Market – Australia

7.5.9.1. Australia: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.9.2. Australia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.5.10. Edge AI Market – Rest of Asia Pacific

7.5.10.1. Rest of Asia Pacific: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.5.10.2. Rest of Asia Pacific: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.6. Edge AI Market – Middle East & Africa

7.6.1. Middle East & Africa: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.6.2. Middle East & Africa: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.6.3. Edge AI Market – Saudi Arabia

7.6.3.1. Saudi Arabia: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.6.3.2. Saudi Arabia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.6.4. Edge AI Market – UAE

7.6.4.1. UAE: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.6.4.2. UAE: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.6.5. Edge AI Market – Israel

7.6.5.1. Israel: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.6.5.2. Israel: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.6.6. Edge AI Market – South Africa

7.6.6.1. South Africa: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.6.6.2. South Africa: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.6.7. Edge AI Market – Rest of Middle East & Africa

7.6.7.1. Rest of Middle East & Africa: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.6.7.2. Rest of Middle East & Africa: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.7. Edge AI Market – Latin America

7.7.1. Latin America: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.7.2. Latin America: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.7.3. Edge AI Market – Mexico

7.7.3.1. Mexico: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.7.3.2. Mexico: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.7.4. Edge AI Market – Brazil

7.7.4.1. Brazil: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.7.4.2. Brazil: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.7.5. Edge AI Market – Argentina

7.7.5.1. Argentina: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.7.5.2. Argentina: Edge AI Market, by Industry, 2020-2034 (USD Billion)

7.7.6. Edge AI Market – Rest of Latin America

7.7.6.1. Rest of Latin America: Edge AI Market, by Component, 2020-2034 (USD Billion)

7.7.6.2. Rest of Latin America: Edge AI Market, by Industry, 2020-2034 (USD Billion)

**8\. Competitive Landscape**

8.1. Expansion and Acquisition Analysis

8.1.1. Expansion

8.1.2. Acquisitions

8.2. Partnerships/Collaborations/Agreements/Exhibitions

**9\. Company Profiles**

9.1. Amazon Web Services, Inc.

9.1.1. Company Overview

9.1.2. Financial Performance

9.1.3. Product Benchmarking

9.1.4. Recent Development

9.2. Apple Inc.

9.2.1. Company Overview

9.2.2. Financial Performance

9.2.3. Product Benchmarking

9.2.4. Recent Development

9.3. Google LLC (Alphabet Inc.)

9.3.1. Company Overview

9.3.2. Financial Performance

9.3.3. Product Benchmarking

9.3.4. Recent Development

9.4. Huawei Technologies Co., Ltd.

9.4.1. Company Overview

9.4.2. Financial Performance

9.4.3. Product Benchmarking

9.4.4. Recent Development

9.5. IBM Corporation

9.5.1. Company Overview

9.5.2. Financial Performance

9.5.3. Product Benchmarking

9.5.4. Recent Development

9.6. Intel Corporation

9.6.1. Company Overview

9.6.2. Financial Performance

9.6.3. Product Benchmarking

9.6.4. Recent Development

9.7. MediaTek Inc.

9.7.1. Company Overview

9.7.2. Financial Performance

9.7.3. Product Benchmarking

9.7.4. Recent Development

9.8. Microsoft Corporation

9.8.1. Company Overview

9.8.2. Financial Performance

9.8.3. Product Benchmarking

9.8.4. Recent Development

9.9. NVIDIA Corporation

9.9.1. Company Overview

9.9.2. Financial Performance

9.9.3. Product Benchmarking

9.9.4. Recent Development

9.10. Qualcomm Technologies, Inc.

9.10.1. Company Overview

9.10.2. Financial Performance

9.10.3. Product Benchmarking

9.10.4. Recent Development

9.11. Samsung Electronics Co., Ltd.

9.11.1. Company Overview

9.11.2. Financial Performance

9.11.3. Product Benchmarking

9.11.4. Recent Development

9.12. Siemens AG

9.12.1. Company Overview

9.12.2. Financial Performance

9.12.3. Product Benchmarking

9.12.4. Recent Development

**List of Tables:**

Table 1 Global Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 2 Global Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 3 North America: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 4 North America: Edge AI Market, by Distribution Channel, 2020-2034 (USD Billion)

Table 5 U.S.: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 6 U.S.: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 7 Canada: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 8 Canada: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 9 Europe: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 10 Europe: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 11 UK: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 12 UK: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 13 France: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 14 France: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 15 Germany: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 16 Germany: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 17 Italy: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 18 Italy: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 19 Spain: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 20 Spain: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 21 Netherlands: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 22 Netherlands: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 23 Russia: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 24 Russia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 25 Rest of Europe: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 26 Rest of Europe: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 27 Asia Pacific: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 28 Asia Pacific: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 29 China: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 30 China: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 31 India: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 32 India: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 33 Malaysia: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 34 Malaysia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 35 Japan: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 36 Japan: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 37 Indonesia: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 38 Indonesia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 39 South Korea: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 40 South Korea: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 41 Australia: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 42 Australia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 43 Rest of Asia Pacific: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 44 Rest of Asia Pacific: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 45 Middle East & Africa: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 46 Middle East & Africa: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 47

Table 48 Saudi Arabia: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 49 Saudi Arabia: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 50 UAE: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 51 UAE: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 52 Israel: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 53 Israel: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 54 South Africa: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 55 South Africa: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 56 Rest of Middle East & Africa: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 57 Rest of Middle East & Africa: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 58 Latin America: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 59 Latin America: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 60 Mexico: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 61 Mexico: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 62 Brazil: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 63 Brazil: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 64 Argentina: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 65 Argentina: Edge AI Market, by Industry, 2020-2034 (USD Billion)

Table 66 Rest of Latin America: Edge AI Market, by Component, 2020-2034 (USD Billion)

Table 67 Rest of Latin America: Edge AI Market, by Industry, 2020-2034 (USD Billion)

**List of Figures:**

Figure 1. Global Edge AI Market, 2020-2034 (USD Billion)

Figure 2. Integrated Ecosystem

Figure 3. Research Methodology: Top-Down & Bottom-Up Price

Figure 4. Market by Geography

Figure 5. Porter’s Five Forces

Figure 6. Market by Component

Figure 7. Global Edge AI Market, by Component, 2024 & 2034 (USD Billion)

Figure 8. Market by Industry

Figure 9. Global Edge AI Market, by Industry, 2024 & 2034 (USD Billion)

### Report Scope

**Edge AI Market, Component Outlook (Revenue - USD Billion, 2020-2034)**

- Hardware

- Network

- Edge Cloud Infrastructure

- Software

- Support Services

**Edge AI Market, Industry Outlook (Revenue - USD Billion, 2020-2034)**

- Automotive

- Manufacturing

- Healthcare

- Energy & Utility

- Retail & Consumer Goods

- IT & Telecom

- Others

**Edge AI Market, Regional Outlook (Revenue - USD Billion, 2020-2034)**

- North America

- Component Outlook

- Hardware

- Network

- Edge Cloud Infrastructure

- Software

- Support Services

- Industry Outlook

- Automotive

- Manufacturing

- Healthcare

- Energy & Utility

- Retail & Consumer Goods

- IT & Telecom

- Others

- Europe

- Component Outlook

- Hardware

- Network

- Edge Cloud Infrastructure

- Software

- Support Services

- Industry Outlook

- Automotive

- Manufacturing

- Healthcare

- Energy & Utility

- Retail & Consumer Goods

- IT & Telecom

- Others

- Asia Pacific

- Component Outlook

- Hardware

- Network

- Edge Cloud Infrastructure

- Software

- Support Services

- Industry Outlook

- Automotive

- Manufacturing

- Healthcare

- Energy & Utility

- Retail & Consumer Goods

- IT & Telecom

- Others

- Latin America

- Component Outlook

- Hardware

- Network

- Edge Cloud Infrastructure

- Software

- Support Services

- Industry Outlook

- Automotive

- Manufacturing

- Healthcare

- Energy & Utility

- Retail & Consumer Goods

- IT & Telecom

- Others

- Middle East & Africa

- Component Outlook

- Hardware

- Network

- Edge Cloud Infrastructure

- Software

- Support Services

- Industry Outlook

- Automotive

- Manufacturing

- Healthcare

- Energy & Utility

- Retail & Consumer Goods

- IT & Telecom

- Others

## Qualitative Analysis

- Industry overview

- Industry trends

- Market drivers and restraints

- Market size

- Growth prospects

- Porter’s analysis

- PESTEL Analysis

- Value Chain Analysis

- Key market opportunities prioritized

- Competitive landscape

- Overview

- Financials

- Component benchmarking

- Latest strategic developments

- Price Trend Analysis

## Quantitative Analysis

- Market size, estimates, and forecasts from 2020-2034

- Market revenue estimates for Component from 2034

- Market revenue estimates for Industry from 2034

- Regional market size and forecast from 2034

- Company financials

### Request Free Sample

Select Country \*AF - AfghanistanAL - AlbaniaDZ - AlgeriaAS - American SamoaAD - AndorraAO - AngolaAI - AnguillaAQ - AntarcticaAG - Antigua And BarbudaAR - ArgentinaAM - ArmeniaAW - ArubaAU - AustraliaAT - AustriaAZ - AzerbaijanBS - Bahamas TheBH - BahrainBD - BangladeshBB - BarbadosBY - BelarusBE - BelgiumBZ - BelizeBJ - BeninBM - BermudaBT - BhutanBO - BoliviaBA - Bosnia and HerzegovinaBW - BotswanaBV - Bouvet IslandBR - BrazilIO - British Indian Ocean TerritoryBN - BruneiBG - BulgariaBF - Burkina FasoBI - BurundiKH - CambodiaCM - CameroonCA - CanadaCV - Cape VerdeKY - Cayman IslandsCF - Central African RepublicTD - ChadCL - ChileCN - ChinaCX - Christmas IslandCC - Cocos (Keeling) IslandsCO - ColombiaKM - ComorosCG - Republic Of The CongoCD - Democratic Republic Of The CongoCK - Cook IslandsCR - Costa RicaCI - Cote D'Ivoire (Ivory Coast)HR - Croatia (Hrvatska)CU - CubaCY - CyprusCZ - Czech RepublicDK - DenmarkDJ - DjiboutiDM - DominicaDO - Dominican RepublicTP - East TimorEC - EcuadorEG - EgyptSV - El SalvadorGQ - Equatorial GuineaER - EritreaEE - EstoniaET - EthiopiaXA - External Territories of AustraliaFK - Falkland IslandsFO - Faroe IslandsFJ - Fiji IslandsFI - FinlandFR - FranceGF - French GuianaPF - French PolynesiaTF - French Southern TerritoriesGA - GabonGM - Gambia TheGE - GeorgiaDE - GermanyGH - GhanaGI - GibraltarGR - GreeceGL - GreenlandGD - GrenadaGP - GuadeloupeGU - GuamGT - GuatemalaXU - Guernsey and AlderneyGN - GuineaGW - Guinea-BissauGY - GuyanaHT - HaitiHM - Heard and McDonald IslandsHN - HondurasHK - Hong Kong S.A.R.HU - HungaryIS - IcelandIN - IndiaID - IndonesiaIR - IranIQ - IraqIE - IrelandIL - IsraelIT - ItalyJM - JamaicaJP - JapanXJ - JerseyJO - JordanKZ - KazakhstanKE - KenyaKI - KiribatiKP - Korea NorthKR - Korea SouthKW - KuwaitKG - KyrgyzstanLA - LaosLV - LatviaLB - LebanonLS - LesothoLR - LiberiaLY - LibyaLI - LiechtensteinLT - LithuaniaLU - LuxembourgMO - Macau S.A.R.MK - MacedoniaMG - MadagascarMW - MalawiMY - MalaysiaMV - MaldivesML - MaliMT - MaltaXM - Man (Isle of)MH - Marshall IslandsMQ - MartiniqueMR - MauritaniaMU - MauritiusYT - MayotteMX - MexicoFM - MicronesiaMD - MoldovaMC - MonacoMN - MongoliaMS - MontserratMA - MoroccoMZ - MozambiqueMM - MyanmarNA - NamibiaNR - NauruNP - NepalAN - Netherlands AntillesNL - Netherlands TheNC - New CaledoniaNZ - New ZealandNI - NicaraguaNE - NigerNG - NigeriaNU - NiueNF - Norfolk IslandMP - Northern Mariana IslandsNO - NorwayOM - OmanPK - PakistanPW - PalauPS - Palestinian Territory OccupiedPA - PanamaPG - Papua new GuineaPY - ParaguayPE - PeruPH - PhilippinesPN - Pitcairn IslandPL - PolandPT - PortugalPR - Puerto RicoQA - QatarRE - ReunionRO - RomaniaRU - RussiaRW - RwandaSH - Saint HelenaKN - Saint Kitts And NevisLC - Saint LuciaPM - Saint Pierre and MiquelonVC - Saint Vincent And The GrenadinesWS - SamoaSM - San MarinoST - Sao Tome and PrincipeSA - Saudi ArabiaSN - SenegalRS - SerbiaSC - SeychellesSL - Sierra LeoneSG - SingaporeSK - SlovakiaSI - SloveniaXG - Smaller Territories of the UKSB - Solomon IslandsSO - SomaliaZA - South AfricaGS - South GeorgiaSS - South SudanES - SpainLK - Sri LankaSD - SudanSR - SurinameSJ - Svalbard And Jan Mayen IslandsSZ - SwazilandSE - SwedenCH - SwitzerlandSY - SyriaTW - TaiwanTJ - TajikistanTZ - TanzaniaTH - ThailandTG - TogoTK - TokelauTO - TongaTT - Trinidad And TobagoTN - TunisiaTR - TurkeyTM - TurkmenistanTC - Turks And Caicos IslandsTV - TuvaluUG - UgandaUA - UkraineAE - United Arab EmiratesGB - United KingdomUS - United StatesUM - United States Minor Outlying IslandsUY - UruguayUZ - UzbekistanVU - VanuatuVA - Vatican City State (Holy See)VE - VenezuelaVN - VietnamVG - Virgin Islands (British)VI - Virgin Islands (US)WF - Wallis And Futuna IslandsEH - Western SaharaYE - YemenYU - YugoslaviaZM - ZambiaZW - Zimbabwe

We take great pride in "Delivering game-changing business opportunities reports with

report customizations", so please don't hesitate to share with us your unique interests and business

difficulties in much more detail.

By using this form

you agree with the storage and handling of your data by this

website.

reCAPTCHA

Recaptcha requires verification.

I'm not a robot

reCAPTCHA

[Privacy](https://www.google.com/intl/en/policies/privacy/) \- [Terms](https://www.google.com/intl/en/policies/terms/)

Please fill out the captcha.

Submit

This website is secure and your personal details are safe. [Privacy Policy](https://www.polarismarketresearch.com/privacy-policy)

© 2025 Polaris Market Research and Consulting. All rights reserved

reCAPTCHA

## Meditation Apps Market Overview

- [Press Releases](https://www.polarismarketresearch.com/press-releases)

- [Blog](https://www.polarismarketresearch.com/blogs)

- [About](https://www.polarismarketresearch.com/industry-analysis/mindfulness-meditation-apps-market#)

[Who We Are](https://www.polarismarketresearch.com/who-we-are) [Why Select Us](https://www.polarismarketresearch.com/why-select-us) [Careers](https://www.polarismarketresearch.com/careers)

- [Contact](https://www.polarismarketresearch.com/contact)

- Services

[Consulting](https://www.polarismarketresearch.com/services/consulting) [Other Services](https://www.polarismarketresearch.com/services/other-services) [Research](https://www.polarismarketresearch.com/services/research)

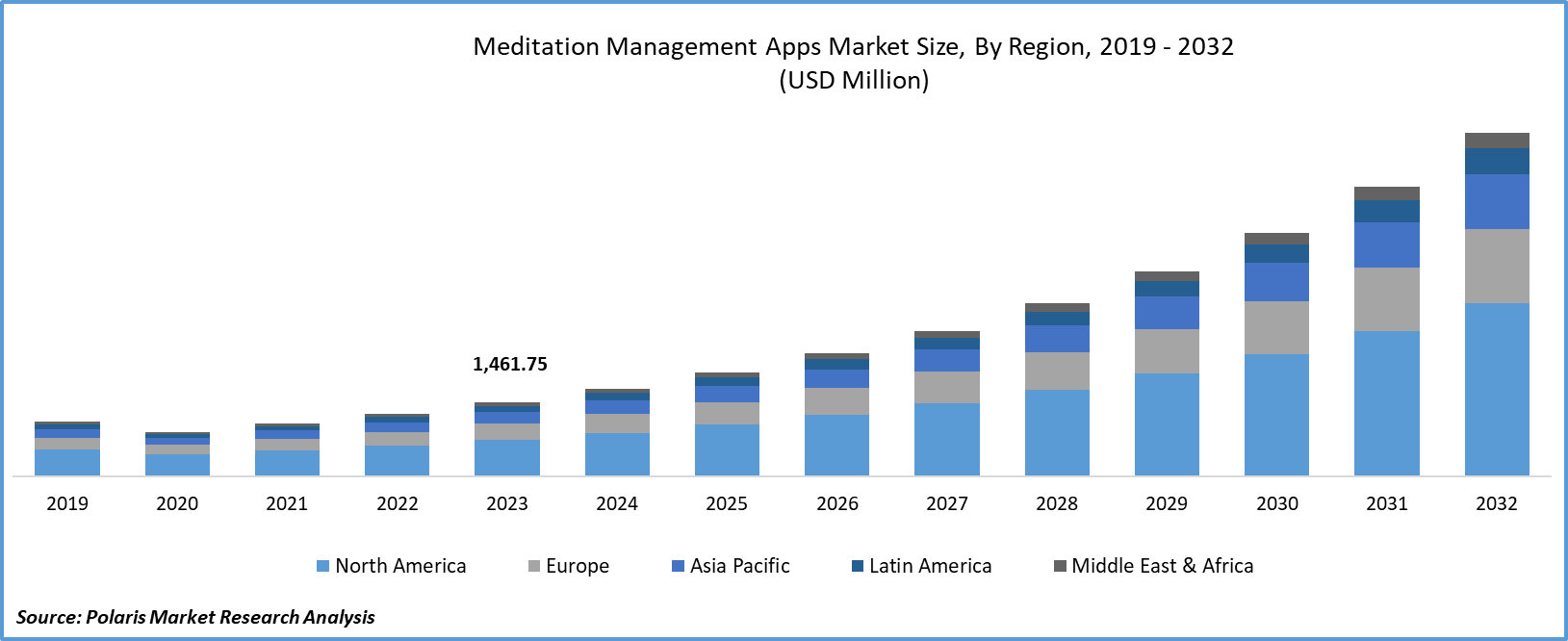

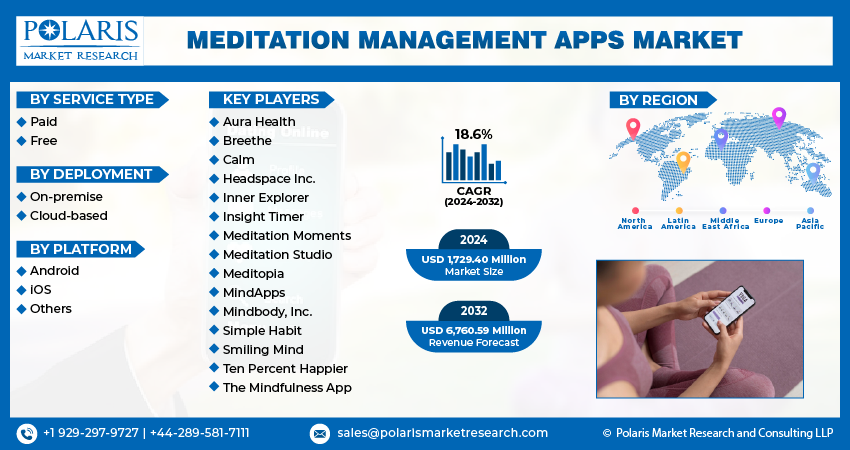

# Meditation Management Apps Market Share, Size, Trends, Industry Analysis Report

By Service Type (Paid, Free); By Platform; By Deployment; By Region; Segment Forecast, 2024- 2032

- Published Date:Jan-2024

- Pages: 117

- Format: PDF

- Report ID: PM1729

- Base Year: 2023

- Historical Data: 2019 – 2022

- [Description](https://www.polarismarketresearch.com/industry-analysis/mindfulness-meditation-apps-market)

- [Table of\\

Contents](https://www.polarismarketresearch.com/industry-analysis/mindfulness-meditation-apps-market/toc)

- [Analysis Type](https://www.polarismarketresearch.com/industry-analysis/mindfulness-meditation-apps-market/analysis-type)

- [Research\\

Methodology](https://www.polarismarketresearch.com/research-methodology)

- [Request Free Sample](https://www.polarismarketresearch.com/industry-analysis/mindfulness-meditation-apps-market/request-for-sample)

## Report Outlook

Meditation Management Apps Market size was valued at USD 1,461.75 million in 2023.

The market is anticipated to grow from USD 1,729.40 billion in 2024 to USD 6,760.59 million by 2032, exhibiting the CAGR of 18.6% during the forecast period.

## **Market Introduction**

The meditation management apps market surges forward on the wave of the global wellness trend. As individuals worldwide prioritize holistic well-being, meditation apps become integral to self-care routines. Aligned with the rising trend, these apps offer accessible tools for mindfulness and stress reduction. With health-conscious consumers seeking comprehensive wellness solutions, the market experiences heightened demand. The global wellness movement further amplifies the adoption of meditation management apps, emphasizing a collective shift towards proactive mental well-being. This trend positions these apps as essential components in the broader spectrum of global health and wellness initiatives, catering to a growing audience.

In addition, companies operating in the mindfulness meditation apps market are concentrating on developing new solutions to cater to the growing market demand.

For instance, in July 2023, Live Nation unveiled a novel mobile application that seamlessly integrates music into the meditation experience. Exclusive to iPhone users, Mindful Nation features sessions led by expert trainers focusing on mindfulness, sleep, and everyday life.

The mindfulness meditation applications market flourishes with the widespread proliferation of smartphones. Increased global smartphone penetration ensures that a vast population has instant access to meditation apps, making mindfulness practices readily available. The convenience of engaging in guided meditation sessions anytime anywhere resonates with users seeking flexibility. As smartphones become ubiquitous, the market witnesses heightened adoption, reaching diverse demographics. The accessibility and ease of incorporating meditation into daily routines, facilitated by smartphone usage, drive the meditation management apps' market expansion. This increased connectivity empowers individuals worldwide to prioritize mental well-being through the seamless integration of meditation management apps into their digital lifestyles.