High Temperature Insulation Market Share, Size, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

High Temperature Insulation Market Summary

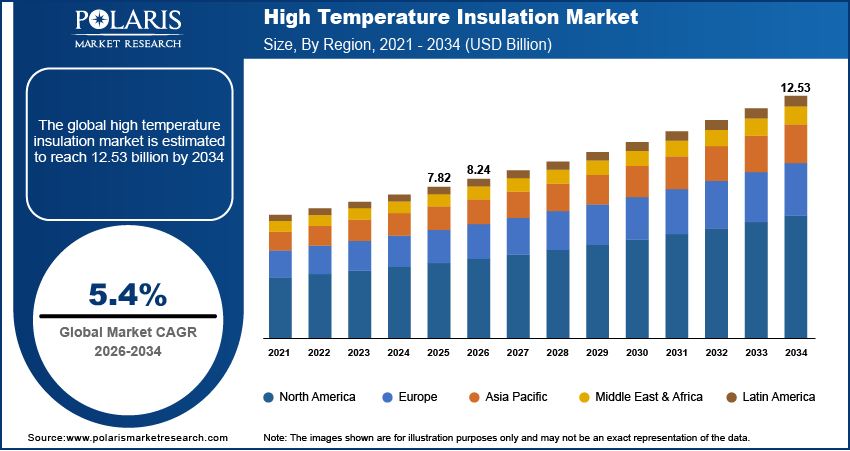

The global high temperature insulation market is estimated around USD 7.82 billion in 2025 with consistent growth anticipated during 2026 to 2034. Energy efficiency mandates and industrial capacity expansion are driving high temperature insulation demand. The market is projected to grow at a CAGR of 5.4% during the forecast.

Market Statistics

Key Takeaways

- Refractory ceramic fiber dominated the 2025 market share due to widespread use in high temperature furnaces.

- Microporous insulation is the fastest growing segment due to high energy efficiency.

- Asia Pacific led the 2025 market, driven by large scale steel, cement, and chemical manufacturing.

- North America is expected to record the highest CAGR, driven by furnace retrofit activity and energy efficiency regulations.

Industry Dynamics

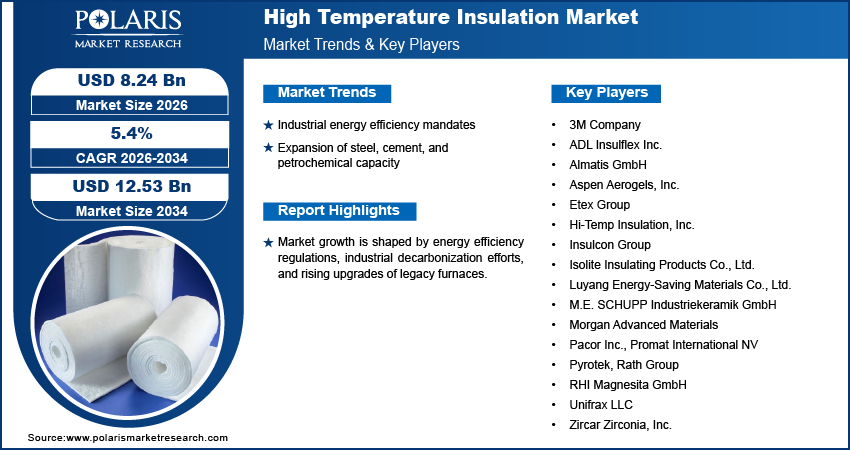

- Energy efficiency mandates are increasing adoption of high temperature insulation.

- Expansion of energy intensive industries is supporting demand.

- High upfront material cost limits rapid adoption.

- Shift toward low biopersistence insulation materials creates opportunity for the market.

High Temperature Insulation Market Overview

High temperature insulation refers to specialized thermal insulation materials engineered to operate in environments exceeding 800°C. These materials different differ from conventional industrial insulation due to their ability to maintain structural integrity, thermal stability, and low heat conductivity under extreme temperatures. High temperature insulation materials are commonly available in forms such as blankets, boards, bricks, and prefabricated modules, which support flexible insulation across high heat industrial systems. Industrial high-temperature insulation is critical in heat loss management, enhanced process efficiency, and the protection of hot machinery.

The high-temperature insulation market range covers ceramic fiber insulation, insulating fiber bricks, calcium silicate microporous insulation, and other advanced refractory insulation materials used for high-temperature thermal insulation above 800°C. The market excludes standard mineral wool and low temperature insulation products that operate below defined thermal thresholds. Market jurisdictions remain oriented towards applications in industry instead of the commercial and residential sectors due to varying demands in respect of performance, safety standards, and operational conditions. This helps in a proper distinction in the overall thermal insulation market.

Source: Polaris Market Research Analysis

High temperature insulation materials are widely deployed across heavy Industries, including metal processing, cement, glass petrochemicals, power generation and advanced manufacturing. Applications include furnaces, kilns, industrial boiler, reactors, and reformers, in which high temperature insulation is important. Insulation materials for furnaces are important in maintaining the stability of the processes, reducing the usage of energy, or maintaining the long lifespan of the furnace within severe temperature conditions.

Increasing energy efficiency and the call for decarbonization are strengthening the role of high-temperature insulation in industry. As of October 2025, close to 145 countries, including China, the EU, and India, had either announced or were considering setting net-zero goals, which account for almost 77% of global emissions.

Drivers & Opportunities

Industrial Energy Efficiency Mandates: Global regulations for the efficient use of industry energy among the leading nations are boosting the use of high-temperature insulation in energy-intensive processes. According to the IEA, the industry accounts for the consumption of 37% of the total final energy globally and to achieve the target efficiency by 2030, there will be the necessity for even higher energy intensity and the increase in the use of electricity from 23% in 2022 to 30% by 2030. Carbon target compliance and heat loss constraint are boosting the use of high-temperature insulation above 800°C.

Expansion of Steel, Cement, and Petrochemical Capacity: Adding capacity in steel, cement, and petrochemicals in the Asia Pacific and Middle Eastern regions is contributing to the growth of the industrial insulation market. As per the IEA, global petrochemicals production capacity increased sharply from 4.5 mt/year in 2019 to 13.1 mt/year in 2024, reflecting a 191% rise over the 2019–2024 period. New and Brownfield plants emphasize the use of industrial high temperature insulation materials for better process efficiency and meeting performance standards set by the authority.

Replacement Demand in Aging Furnaces: Older generation furnace and kiln installations made over the past two decades are currently under the process of insulation up-gradation. Replacing the insulation used in older generation furnaces is helping improve the efficiency of the equipment. This factor is expected to improve the forecast for the high temperature insulation market.

Restraints & Challenges

Health and Safety Concerns Related to RCF: Health and safety regulations associated with refractory ceramic fibers are increasing compliance and handling requirements. Stricter workplace exposure standards are influencing material selection and limiting the use of conventional RCF-based insulation, which is constraining high temperature insulation market CAGR in certain regions.

High Upfront Cost of Advanced Insulation Materials: High-temperature insulation materials of an advanced type, along with microporous insulation and next-generation ceramic insulation, require high capital expenditures compared to traditional insulation materials. Cost-sensitivity in medium-sized industries is currently slowing down their adoption rate, especially in the context of retrofitted applications involving limited capital budgets.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the high temperature insulation market by material type, temperature range and end-use industry to help readers identify the fastest expanding and most attractive demand segments.

By Material Type

-

Refractory Ceramic Fiber (RCF)

By material type, the refractory ceramic fiber insulation segment accounted for the largest share of the high-temperature insulation market in 2025, owing to its wide temperature capability above 1,200°C and the wide deployment across furnaces, kilns, and petrochemical heaters. Established supply chains, proven thermal performance, and cost efficiency supported large-scale adoption across steel, cement, and refining industries.

-

Alkaline Earth Silicate (AES) Wool

In terms of material type, the microporous insulation materials segment is projected to grow at the fastest CAGR during the forecast period, due to rising demand for superior energy efficiency and reduced heat loss in compact industrial equipment. With increased emphasis on reducing emissions and operating cost, there is acceleration toward microporous insulation in new installations and selective retrofit projects.

-

Insulating Firebricks (IFB)

Insulating firebricks operate in the range of 1,000°C to 1,600°C depending on grade and composition. The major benefits offered by these bricks include high mechanical strength, stability, and long life when subjected to load-bearing capacity. Some common uses include furnace walls, kiln lining, and combustion chambers. The market for insulating firebricks continues to demonstrate constant demand in heavy industries needing long-lasting insulation.

-

Calcium Silicate

Operating temperatures of calcium silicate insulation are usually up to 1,000° C. The main benefits include water resistance, dimensional stability, and ease of processing. Its main applications are in boilers, piping, and secondary insulation in furnaces. The usage is current in power plants and process industries, where its strength is a preference.

-

Microporous Insulation

The temperature range that these microporous insulation products sustain is up to 1,200°C, and they also offer low thermal conductivity. The most important benefits include advanced control over heat loss and thinner insulation, hence greater equipment efficiency. Their application ranges; these include high-performance furnaces, space products, and advanced reactors. The use is also on the increase, particularly in energy-intensive industries that emphasize energy conservation and green products.

-

Aerogel-Based Insulation

The temperature range that high-temperature aerogel insulation operates effectively is up to 650-1,000 Degrees centigrade, depending on the type. The key benefits include very low density, high thermal performance, and flexibility in design. The applications include petrochemical piping, high-temperature vessels, and high-temperature industrial equipment. The current trend is to apply this technology in high-end applications where weight and thermal performance are important enough to warrant high material expenses.

By Temperature Range

-

800°C–1100°C

The 800°C–1100°C range is expanding by calcium silicate, AES insulation wool, and selected aerogel systems. These materials perform well under moderate high heat while meeting industrial safety and handling requirements. Calcium silicate insulation is preferred in boilers and pipework because of its compression strength and water-resistance properties. AES insulation wool becomes popular in backup insulation and process heaters because of the aspect of compliance with regulation and standards.

-

1100°C–1500°C

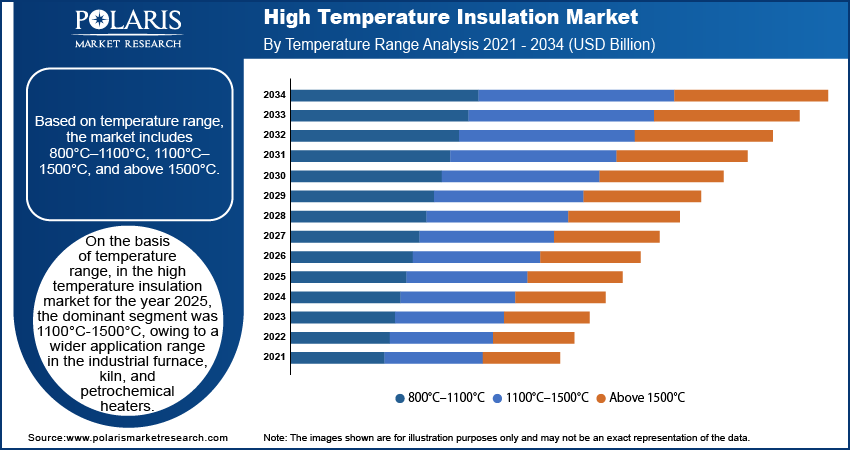

On the basis of temperature range, in the high temperature insulation market for the year 2025, the dominant segment was 1100°C-1500°C, owing to a wider application range in the industrial furnace, kiln, and petrochemical heaters. This temperature range matches the prime working range for the steel, cement, and oil industries. The wider use of refractory ceramic fiber insulation and insulating firebrick worked in favor of the dominant segment of this market.

-

Above 1500°C

In terms of temperature range, the above 1500°C segment is projected to grow at the fastest CAGR during the forecast period, due to rising deployment of ultra-high temperature processes in advanced metallurgy and specialty materials manufacturing. The growing use of the electric arc furnace and high purity glass melters is propelling the demand for ultra-high temperature insulation. The increasing use of process electrification and efficiency improvements is pushing the market towards the use of high-end refractory and composite insulation. Yet again, the industry is still limited to high-end sectors.

By End-Use Industry

-

Iron & Steel

By end use industry, the iron and steel market was leading in the high temperature insulation market in 2025. This can be ascribed to the large installed capacity of furnaces in the industries along with high operating temperatures. Large scale industries require constant relining and replacement of insulation. Continuous operation cycles support recurring demand for furnace insulation for steel industry applications. This segment accounts for the largest installed base globally.

-

Cement

The cement industry requires cement kiln insulation for rotary kilns, preheaters, and clinker coolers. The type of insulation used in this industry is mainly characterized by its ability to withstand abrasion, chemical, and high temperatures. Insulating fire bricks and calcium silicate insulation are common types of insulation used in kiln shells and auxiliary equipment.

-

Petrochemicals & Refining

In terms of end use industry, the petrochemicals and refining segment is projected to grow at the fastest CAGR during the forecast period, due to capacity expansion and rising focus on energy efficiency. The use of modern insulation materials is increasing to lower the generation of heat. New projects of the cracker and reformer parts are contributing to increased use of insulation per unit. Process optimization projects are accelerating the use of modern materials in the segment.

-

Power Generation

The insulation of high temperatures in power plants is realized mainly in the boilers, turbines, and heat recovery systems. Mechanical properties together with compliance to safety standards prop calcium silicate and insulation wool-AES to dominance. Applications focus more on steam generation and thermal loss reduction than extreme temperature exposure. Adoption has been stable with further incremental upgrades in thermal power facilities.

-

Glass Manufacturing

Glass manufacturing employs high-temperature insulation in melting furnaces, in forehearths, and in regenerators. Both insulating firebricks and refractory ceramic fiber are dominant, simply due to the sustained high heat and corrosive atmospheres. Furnace campaigns are expected to drive periodic replacement demand. Growth fits with flat glass and container glass production trends.

-

Others

Other sectors include non-ferrous metals and specialty chemicals. Tailored insulation solutions are required based on temperature ranges and chemical exposure. Microporous insulation and aerogel insulation demonstrate selective use in high-value processes. Demand in this market niche remains technology-driven.

Material Selection Matrix (Material × Temperature × End Use)

| Material Type | Typical Temperature Range | Primary End Use Industries | Key Selection Rationale |

| Refractory Ceramic Fiber (RCF) | 1,100°C–1,500°C | Iron and steel, petrochemicals, glass | High thermal stability and resistance to thermal cycling |

| AES Insulation Wool | 800°C–1,200°C | Cement, power generation, chemicals | Regulatory compliance and ease of handling |

| Insulating Firebricks (IFB) | 1,000°C–1,600°C | Steel, cement, glass | Structural strength and long service life |

| Calcium Silicate | Up to 1,000°C | Power generation, refineries | Mechanical strength and moisture resistance |

| Microporous Insulation | Up to 1,200°C | Advanced furnaces, specialty manufacturing | Ultra-low thermal conductivity and space efficiency |

| Aerogel Based Insulation | 650°C–1,000°C | Petrochemicals, specialty equipment | Weight reduction and superior thermal performance |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

Asia Pacific Market Assessment

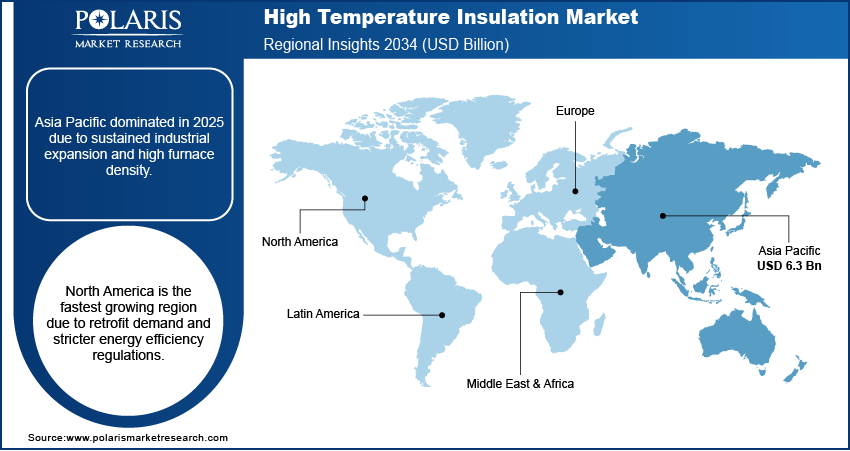

Asia Pacific held a leading share of the high temperature insulation market in 2025, due to rapid industrial expansion across steel, cement, and chemical manufacturing. Large scale furnace installations and continuous capacity additions are increasing demand for industrial high temperature insulation materials. China’s National Bureau of Statistics reported that in March, output rose year on year for 405 of 623 industrial products, including rolled steel at 134.42 million tons up 8.3%, cement at 157.88 million tons up 2.5%, and non-ferrous metals at 6.92 million tons up 3.7%. The Asia Pacific high temperature insulation market continues to benefit from sustained infrastructure and manufacturing growth.

North America High Temperature Insulation Market Insights

North America is projected to witness the fastest growth in the high temperature insulation market over the forecast period. Strong retrofit demand across aging furnaces and boilers is driving replacement of legacy insulation systems. Energy efficiency regulations and carbon reduction targets are accelerating adoption of advanced insulation materials. Under the Trump administration, US emissions are projected to fall 19% to 30% below 2005 levels by 2030, excluding LULUCF emissions. The North America industrial insulation market is supported by modernization of steel, refining, and power generation assets.

Europe High Temperature Insulation Market Overview

The demand for high-temperature insulation in Europe is driven by material substitution on account of safety and sustainable considerations. The regulatory policies, which emphasize labor safety, are promoting a transition from traditional refractory ceramic fibers to alternative, compliant materials. The decarbonization of industries is raising emphasis on thermal efficiency in energy-intensive sectors. The European Union’s Clean Industrial Deal plans to mobilize over USD 117 billion in funding, including up to USD 59 billion via InvestEU guarantees, to support clean manufacturing, industrial decarbonization, and clean technology deployment.

MEA High Temperature Insulation Market Overview

The Middle East and Africa high temperature insulation market is growing steadily due to petrochemical, refining, and power generation investments. Industrial Center stated that KSA holds 4.7% of global chemicals volume and is expected to outpace MEA growth, with chemicals capacity reaching 8.7 MTPA and plastics and elastomers conversion capacity rising to 11.5 MTPA by 2034. Emerging new industry projects are increasing the demand for insulation of furnaces and processes. A focus on durability and energy saving in the design phase of the product is influencing material choice. Thus, project-related growth continues with a focus on longer-term asset performance.

Regional Demand Heat Map

| Region | Demand Intensity | Key Demand Drivers | Dominant End Use |

| Asia Pacific | High | Industrial expansion and capacity additions | Steel, cement, chemicals |

| North America | Medium–High | Retrofit demand and energy efficiency mandates | Steel, refining, power |

| Europe | Medium | Safety driven material substitution and sustainability focus | Chemicals, glass, metallurgy |

| Middle East & Africa | Medium | Petrochemical investments and infrastructure projects | Refining, power |

| Latin America | Low–Medium | Project led industrial development | Cement, metals |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The high-temperature insulation segment is moderately fragmented, and global players are at the forefront of standardized materials, whereas regional players have been competing through the development of application-specific solutions. The products have been focusing on ceramic fibers, calcium silicate insulation, microporous insulation, and, more recently, aerogel insulation technologies. Competitive rivalry is based on performance, compliance, and technical support services.

Some of the main corporations in the high temperature insulation industry include 3M Company; Morgan Advanced Materials; RHI Magnesita GmbH; Luyang Energy-Saving Materials Co., Ltd.; Etex Group; ADL Insulflex Inc.; Zircar Zirconia, Inc.; Unifrax LLC; Almatis GmbH; Rath Group; Aspen Aerogels, Inc.; Hi-Temp Insulation, Inc.; Insulcon Group; Isolite Insulating Products Co., Ltd.; Pacor Inc.; Promat International NV; Pyrotek; M.E. SCHUPP Industriekeramik GmbH; among others.

Competitive Positioning Table

| Company Type | Product Breadth | Technology Focus | Competitive Strength |

| Global Manufacturers | Wide | RCF, IFB, microporous | Scale and certification |

| Regional Specialists | Medium | AES, calcium silicate | Application specific expertise |

| Advanced Material Players | Narrow–Medium | Microporous, aerogel | High performance differentiation |

| EPC Aligned Suppliers | Medium | System level insulation | Early stage project integration |

Source: Polaris Market Research Analysis

Strategic Trends in the High Temperature Insulation Market

| Strategic Trend | Description | Primary Materials Impacted | End Use Focus | Strategic Rationale |

| Shift toward low biopersistence materials | Manufacturers are prioritizing insulation materials with improved bio solubility to align with stricter worker safety and handling regulations | AES insulation wool, low biopersistence ceramic fibers | Steel, cement, petrochemicals, power generation | Regulatory compliance and reduction of occupational health risk |

| Investment in advanced microporous insulation | Increased development of microporous insulation materials with ultra low thermal conductivity and reduced thickness | Microporous insulation materials | High efficiency furnaces, reactors, specialty industrial systems | Improved thermal efficiency and lower energy consumption |

| Development of next generation insulation systems | Focus on composite insulation systems that combine fibers, boards, and microporous layers | Hybrid insulation systems, advanced ceramic materials | Industrial furnaces, kilns, reformers | Enhanced performance across wider temperature ranges |

| Capacity expansion in high growth regions | Manufacturers are expanding production facilities and supply chains in Asia Pacific and the Middle East | Ceramic fibers, firebricks, calcium silicate | Steel, cement, chemicals, refining | Proximity to large scale industrial customers and reduced logistics cost |

| Partnerships with furnace OEMs and EPC contractors | Strategic collaborations are increasing to integrate insulation solutions at the design and construction stage | System level insulation solutions | New build and retrofit furnace projects | Early specification and long term supply positioning |

| Material substitution driven by regulation | Gradual replacement of conventional RCF with compliant alternatives in regulated markets | AES wool, microporous insulation | Europe and North America heavy industries | Alignment with safety standards and sustainability objectives |

| Performance driven differentiation | Competitive positioning based on heat loss reduction, durability, and lifecycle performance | Premium insulation materials | Energy intensive industrial processes | Differentiation beyond price in competitive landscape high temperature insulation market |

Source: Polaris Market Research Analysis

Key Players

- 3M Company

- ADL Insulflex Inc.

- Almatis GmbH

- Aspen Aerogels, Inc.

- Etex Group

- Hi-Temp Insulation, Inc.

- Insulcon Group

- Isolite Insulating Products Co., Ltd.

- Luyang Energy-Saving Materials Co., Ltd.

- M.E. SCHUPP Industriekeramik GmbH

- Morgan Advanced Materials

- Pacor Inc.

- Promat International NV

- Pyrotek

- Rath Group

- RHI Magnesita GmbH

- Unifrax LLC

- Zircar Zirconia, Inc.

Heat Loss Reduction and Energy Savings Estimation Table

| Insulation Type | Relative Heat Loss Reduction | Energy Saving Potential | Typical Impact on Operating Cost |

| Conventional Insulation | Baseline | Low | Limited efficiency improvement |

| AES Wool Systems | Medium | Moderate | Gradual fuel cost reduction |

| RCF Based Systems | High | High | Significant efficiency gains |

| Microporous Insulation | Very High | Very High | Substantial long term cost savings |

| Aerogel Based Systems | High | High | Premium efficiency improvement |

Source: Polaris Market Research Analysis

Industry Developments

- December 2025: Raleigh Excel Spray Foam Insulation has expanded its Roof Insulation services in Cary, NC, to reduce heat loss and moisture and improve energy efficiency for residential and commercial buildings.

- June 2025: Armacell opened a new aerogel insulation plant in India to manufacture its advanced ArmaGel XG product line.

High Temperature Insulation Market Segmentation

By Material Type Outlook (Revenue, USD Billion, 2021-2034)

- Refractory Ceramic Fiber (RCF)

- Alkaline Earth Silicate (AES) Wool

- Insulating Firebricks (IFB)

- Calcium Silicate

- Microporous Insulation

- Aerogel-Based Insulation

By Temperature Range Outlook (Revenue, USD Billion, 2021-2034)

- 800°C–1100°C

- 1100°C–1500°C

- Above 1500°C

By End-Use Industry Outlook (Revenue, USD Billion, 2021-2034)

- Iron & Steel

- Cement

- Petrochemicals & Refining

- Power Generation

- Glass Manufacturing

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 7.82 Billion |

| Market Size in 2026 | USD 8.24 Billion |

| Revenue Forecast by 2034 | USD 12.53 Billion |

| CAGR | 5.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

High Temperature Insulation Market FAQ's

The global market size was valued at USD 7.82 billion in 2025 and is projected to grow to USD 12.53 billion by 2034.

Asia Pacific dominates due to large scale steel, cement, and chemical manufacturing capacity and continuous furnace installations.

Applications include furnaces, kilns, boilers, reactors, reformers, and glass melting units across energy intensive industries.

A few of the key players in the market are 3M Company, Morgan Advanced Materials, RHI Magnesita GmbH, Luyang Energy-Saving Materials Co., Ltd., Etex Group, ADL Insulflex Inc., Zircar Zirconia, Inc., Unifrax LLC, Almatis GmbH, Rath Group, Aspen Aerogels, Inc., Hi-Temp Insulation, Inc., Insulcon Group, Isolite Insulating Products Co., Ltd., Pacor Inc., Promat International NV, Pyrotek, and M.E. SCHUPP Industriekeramik GmbH.

Growth is driven by industrial energy efficiency mandates, capacity expansion in heavy industries, and replacement demand in aging thermal systems.

Download Sample Report of High Temperature Insulation Market

Please fill out the form to request a customized copy of the research report.