Polymer Market Demand Scenario, Developments, 2026-2034

REPORT DETAILS

Polymer Market Summary

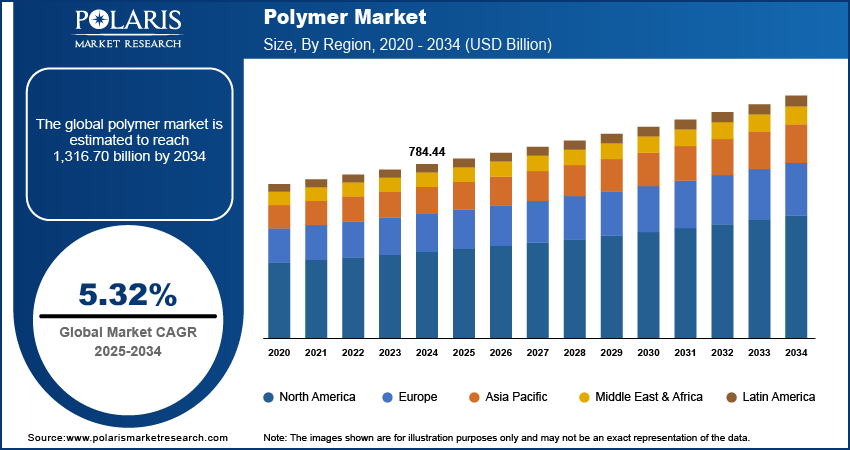

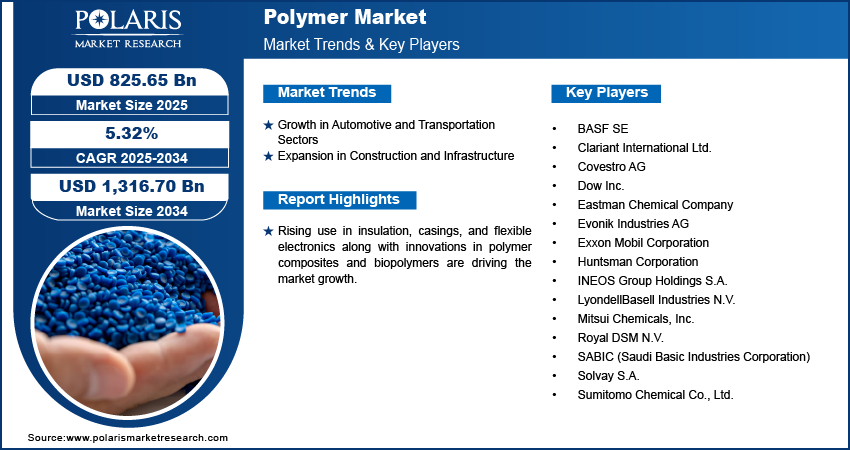

The global polymer market size was valued at USD 825.65 billion in 2025, growing at a CAGR of 5.32% from 2026 to 2034. Growth in automotive and transportation sectors coupled with expansion in construction and infrastructure is boosting the market growth.

Market Statistics

Key Takeaways

- Asia Pacific accounted for the largest share of 40.0% in the global polymer market in 2025, driven by strong industrialization and urbanization in major economies.

- In 2025, China accounted for the largest share of 45.0% in the regional market, driven by strong growth in Chinese, Indian, and Japanese automotive manufacturing.

- North America to grow at a high rate of 4.6% during the forecast period, driven by increasing emphasis on lightweight polymers in the automotive industry.

- The U.S. held 80.0% share of the NA market, propelled by the growing packaging industry, mainly fueled by growth in e-commerce and expanding food & beverage consumption.

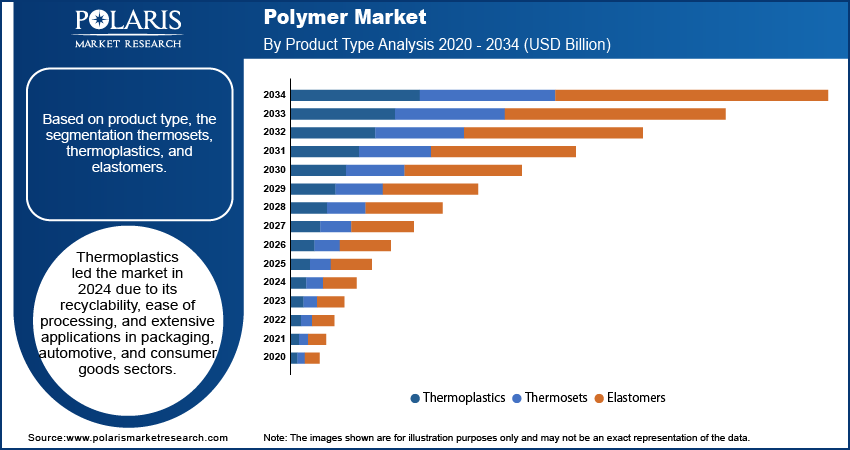

- Based on product type, the thermoplastics segment led the market with 66.0% share in 2025 due to recyclability, processibility, and extensive application across packaging, automotive, and consumer goods segments.

- In terms of material, the polypropylene segment accounted for a substantial share of 20.0% in 2025, due to its strength, resistance to chemicals, and growing application in automotive light weighting and industrial parts.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Automotive and transport sector growth is driving polymer demand in vehicle components, packaging, and industrial applications.

- Growth in construction and infrastructure development is also supporting additional demand for rugged and multi-functional polymer materials.

- Uncertainty over raw material prices is still a major constraint, influencing production and market stability.

- Innovations in biodegradable and bio-based polymers are creating new opportunities, enabling sustainability efforts and minimizing environmental footprint across markets.

What are Polymers?

Polymers are large molecules composed of repeating structural units known as monomers. They comprise various properties such as lightweight, durability, flexibility, and cost-effectiveness. They are widely used across industries, including packaging, construction, automotive, electronics, healthcare, and consumer goods. They are used in the development of products with enhanced performance, design flexibility, and material efficiency.

The polymer market includes synthetic and bio-based polymers for use in packaging, automotive, building, electronics, healthcare, and consumer products. They are widely utilized as they are flexible, durable, lightweight, and economical to make various products and components. Advances in high-performance polymers, biodegradable, and recycling technology are enhancing sustainability, thermal stability, and mechanical strength.

The demand for polymers in electrical and electronics applications is growing at an extremely high pace, driven by their use in insulation, enclosures, and flexible electronics. In September 2025, the Filament Factory and Council for Scientific and Industrial Research (CSIR) introduced a new nano-reinforced polymer composite used in high-end applications. This is a material where nanomaterials are added into a polymer matrix, enhancing mechanical strength, thermal stability, and electric conductivity. These advances are boosting polymers as critical materials in advanced electronic devices.

Source: Polaris Market Research Analysis

Innovation in polymer composites and biopolymers is enabling high-performance, sustainable, and eco-friendly alternatives to be produced. The innovations enable manufacturers to create material with high sensitivity to high-performance requirements without harming the environment. Continuous advancements in polymer technology are opening up new possibilities across different industry sectors.

Difference Between Polymers vs Traditional Materials

Polymers differ significantly from traditional materials, such as metals and glass. They are differed in terms of performance, cost, and application suitability. Polymers are generally lightweight, flexible, corrosion-resistant, and cost-effective. These features make them ideal for packaging, automotive, healthcare, and consumer applications. However, metals offer superior mechanical strength and heat resistance. In contrast, glass provides high transparency and chemical stability. However, metals are prone to corrosion and are heavier. Glass is brittle and more susceptible to breakage.

| Parameter | Polymers | Metals | Glass |

| Weight | Lightweight | Heavy | Moderate to Heavy |

| Flexibility | Highly flexible | Limited flexibility | Brittle |

| Cost | Generally cost-effective | Higher processing cost | Moderate to high |

| Corrosion Resistance | Excellent | Susceptible to corrosion | Excellent |

| Recyclability | Increasingly recyclable | Highly recyclable | Recyclable but energy-intensive |

| Durability | Good impact resistance | High mechanical strength | Fragile under impact |

| Common Applications | Packaging, electronics, healthcare | Construction, machinery, automotive | - |

Source: Polaris Market Research Analysis

Drivers & Opportunities

What are the Factors Driving the Expansion Opportunities?

Growth in automotive and transportation sectors: The rapidly growing automotive industry is significantly propelling the market growth. Automotive and transport industries are increasingly employing light-weight polymers in a bid to improve the fuel efficiency and reduce emissions. The European Automobile Manufacturers Association indicates that the sales of automobiles globally in 2024 were at 74.6 million units with an increase of 2.5% from 2023. The trend shows the growing reliance on the use of polymers to meet sustainability and performance goals in mobility solutions.

Expansion in construction and infrastructure: Polymers are becoming increasingly vital to construction and infrastructure development due to durability, resistance to corrosion, and lengthy service life in usage in pipes, coatings, and insulation. Oxford Economics predicts global construction to increase from USD 9.7 trillion in 2022 to USD 13.9 trillion by 2037, with China, the US, and India leading the way, fueled by urbanization and green infrastructure programs. This expansion is increasing the demand for high-performance, long-lasting polymer materials in building.

What are Challenges in the Polymer Market?

The polymer market faces various challenges that can adversely impact production costs. They also influence sustainability goals and overall market growth. One of the major concerns is the volatility in raw material prices. Most conventional polymers are derived from petrochemical feedstocks. The feedstocks are highly sensitive to fluctuations in crude oil and natural gas prices. There are rising environmental concerns regarding plastic waste accumulation, carbon emissions, and microplastic pollution. They intensify pressure on manufacturers to adopt sustainable and recyclable alternatives. Additionally, increasingly stringent government regulations related to single-use plastics, recycling mandates, and emission controls are creating compliance challenges for polymer producers worldwide. The industry must also address issues related to recycling infrastructure limitations. It must also work on issues such as high costs of bio-based polymers. They are required to emphasize advanced material innovation to balance performance with sustainability.

Source: Polaris Market Research Analysis

Segmental Insights

By Product Type

Based on product type, the market for polymers is divided into thermosets, thermoplastics, and elastomers. Thermoplastics led the market with 66.0% share in 2025 due to its recyclability, ease of processing, and extensive applications in packaging, automotive, and consumer goods sectors.

Thermosets are anticipated to experience rapid growth at a CAGR of 4.70% during the forecast period due to its better heat resistance and structural integrity, making them ideal for electrical, aerospace, and industrial uses.

By Material

Based on material, the market is segmented into polyethylene, polypropylene, polyvinyl chloride, polyethylene terephthalate, polystyrene, and polyurethane. Polyethylene dominated the market with 24.0% share in 2025 due to its prevalent application in flexible packaging, films, and consumer products.

Polypropylene anticipated to experience strong growth at a CAGR of 5.70% due to its strength, chemical resistance, and growing use in automotive light weighting and industrial parts.

By Process

By process, the market is segmented into injection molding, extrusion, and others. Injection molding led with 41.0% share in 2025, due to its accuracy, scalability, and applicability in bulk production of intricate polymer parts.

Extrusion is expected to see significant growth at a CAGR of 5.20%, due to its wide application in pipe making, film-making, and continuous profile applications.

By Application

By application, the market for polymers is divided into packaging, building and construction, automotive, electrical and electronics, agriculture, medical/healthcare, and others. The packaging segment dominated the market with 28.0% share in 2025 due to intense consumption of low-weight, cost-effective plastic solutions for food, beverage, and e-commerce markets.

Construction and building are likely to experience robust expansion at a CAGR of 4.80%, propelled by infrastructure growth and increasing use of high-performance polymers for durability, insulation, and fuel efficiency.

Source: Polaris Market Research Analysis

Regional Analysis

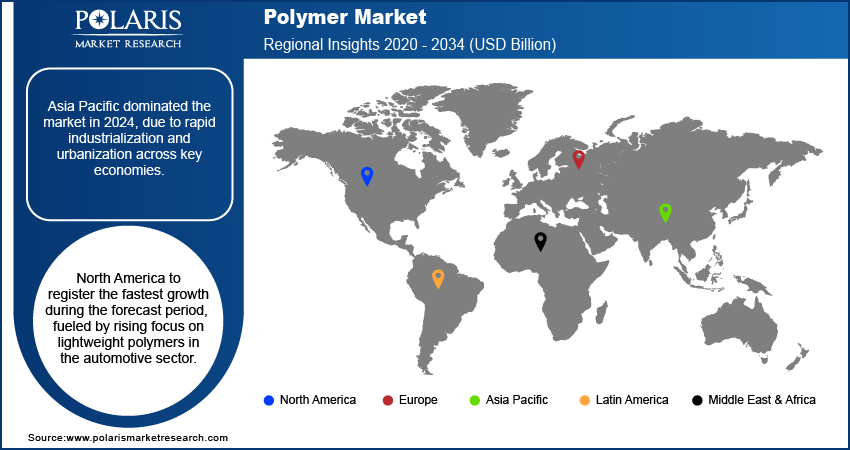

Asia Pacific dominated the polymer market with 40.0% share in 2025, propelled by high-speed industrialization and urbanization in major economies. The growth is driving aggressive demand for polymers, especially for construction, infrastructure, and consumer goods segments. Growth in manufacturing of electronics and electrical equipment is also boosting the demand for polymer-based components as industries begin to adopt lightweight and long-lasting materials.

China Polymer Market Overview

China dominated the Asia pacific market with 45.0% share in 2025, driven by strong growth in vehicle production in China, India, and Japan. As per the International Energy Agency, China remains the world's biggest electric vehicle production hub, with over 70% of the world's production in 2024. This domination is propelling demand for high-performance polymer parts in EVs and EV-related technologies.

North America Polymer Market Insights

North America is experiencing exponential growth at a CAGR of 4.6% in the polymers market driven by increasing emphasis on lightweight polymers in the automotive industry. This trend is enabling manufacturers to enhance fuel efficiency and lower emissions, while the healthcare and medical industries are increasingly using polymer-based materials to design devices, packaging, and equipment.

The U.S. Polymer Market Analysis

The U.S. dominates the market in North America with 80.0% share in 2025, due to the growth of the packaging industry, propelled by growing e-commerce and food & beverages consumption. In August 2025, the U.S. Census Bureau stated that retail e-commerce sales in Q2 2025 reached USD 304.2 billion, an increase of 1.4% compared to Q1, indicating sustained growth in packaging requirements.

Europe Polymer Market Assessment

In 2025, Europe held substantial market share of 20.0% in polymer market, driven by strong focus on high-performance and lightweight polymers for automotive and transportation use. Sustainability programs and environmental regulations are stimulating broad use of recyclable and biodegradable polymers, and continuous innovation is powering the creation of advanced polymer solutions in consumer and industrial markets.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The global polymers market is moderately competitive, with players interested in creating high-performance, sustainable, and application-focused polymer solutions. The focus of product innovation remains on lightweight materials, bio-based and recyclable polymers, and specialty formulations for packaging, automotive, electronics, construction, and medical industries. Strategic partnerships with raw material producers, end-use manufacturers, and R&D organizations are assisting players to increase their market share and speed up product development.

Key companies operating in the global polymer market include BASF SE, Clariant International Ltd., Covestro AG, Dow Inc., Eastman Chemical Company, Evonik Industries AG, Exxon Mobil Corporation, Huntsman Corporation, INEOS Group Holdings S.A., LyondellBasell Industries N.V., Mitsui Chemicals, Inc., Royal DSM N.V., SABIC (Saudi Basic Industries Corporation), Solvay S.A., and Sumitomo Chemical Co., Ltd.

Key Players

- BASF SE

- Clariant International Ltd.

- Covestro AG

- Dow Inc.

- Eastman Chemical Company

- Evonik Industries AG

- Exxon Mobil Corporation

- Huntsman Corporation

- INEOS Group Holdings S.A.

- LyondellBasell Industries N.V.

- Mitsui Chemicals, Inc.

- Royal DSM N.V.

- SABIC (Saudi Basic Industries Corporation)

- Solvay S.A.

- Sumitomo Chemical Co., Ltd.

Polymer Industry Developments

- March 2026: Z-Polymers, Inc. announced a strategic investment from Kureha Corporation. In addition, the companies signed a joint development agreement (JDA). Through the agreement, companies aims to boost the commercialization of Z-Polymers’ proprietary Tullomer liquid crystal polymer platform. (Source: globenewswire.com)

- October 2025: Clariant introduced TexCare One Terra, a next-generation multifunctional polymer engineered to enhance the performance of high-concentrate liquid laundry products, particularly laundry capsules. (Source: clariant.com)

- October 2025: BASF and International Flavors & Fragrances Inc. (IFF) announced a strategic collaboration aimed at advancing next-generation enzyme and polymer technologies. The partnership focuses on developing innovative enzyme systems and biobased polymers to enhance performance and sustainability in various applications, including fabric care, dishwashing, personal care, and industrial cleaning. (Source: basf.com)

- July 2025: AGC introduced new SF grades within its AFLAS FFKM fluoroelastomer portfolio, becoming the first in the industry to manufacture these materials without using surfactants or fluorinated polymerization solvents. The new grades retain the high performance of traditional fluoroelastomers while meeting growing demand for more environmentally responsible production processes. (Source: agc.com)

- March 2025: Abu Dhabi National Oil Company (ADNOC) and OMV reached an agreement to establish a global polyolefins leader by merging Borouge and Borealis into Borouge Group International, which will also acquire Nova Chemicals in a USD 13.4 billion transaction. (Source: adnoc.com)

Polymer Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021–2034)

- Thermoplastics

- Thermosets

- Elastomers

By Material Outlook (Revenue, USD Billion, 2021–2034)

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Polyethylene Terephthalate

- Polystyrene

- Polyurethane

By Process Outlook (Revenue, USD Billion, 2021–2034)

- Injection Molding

- Extrusion

- Others

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Packaging

- Building and Construction

- Automotive

- Electrical and Electronics

- Agriculture

- Medical/Healthcare

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Polymer Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 825.65 Billion |

| Market Size in 2026 | USD 868.49 Billion |

| Revenue Forecast by 2034 | USD 1,316.70 Billion |

| CAGR | 5.32% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion, Volume in Kilotons and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Polymer Market FAQ's

The global market size was valued at USD 825.65 billion in 2025 and is projected to grow to USD 1,316.70 billion by 2034.

The global market is projected to register a CAGR of 5.32% during the forecast period.

Asia Pacific accounted for the largest share of 40.0% in the global polymer market in 2025.

A few of the key players in the market are BASF SE, Clariant International Ltd., Covestro AG, Dow Inc., Eastman Chemical Company, Evonik Industries AG, Exxon Mobil Corporation, Huntsman Corporation, INEOS Group Holdings S.A., LyondellBasell Industries N.V., Mitsui Chemicals, Inc., Royal DSM N.V., SABIC (Saudi Basic Industries Corporation), Solvay S.A., and Sumitomo Chemical Co., Ltd.

The thermoplastics segment led the market with 66.0% share in 2025.

The polypropylene segment accounted for a substantial share of 20.0% in 2025.

Download Sample Report of Polymer Market

Please fill out the form to request a customized copy of the research report.