Automotive Market Insight, Demand & Industry Growth, 2026-2034

REPORT DETAILS

REPORT DETAILS

Automotive Market Summary

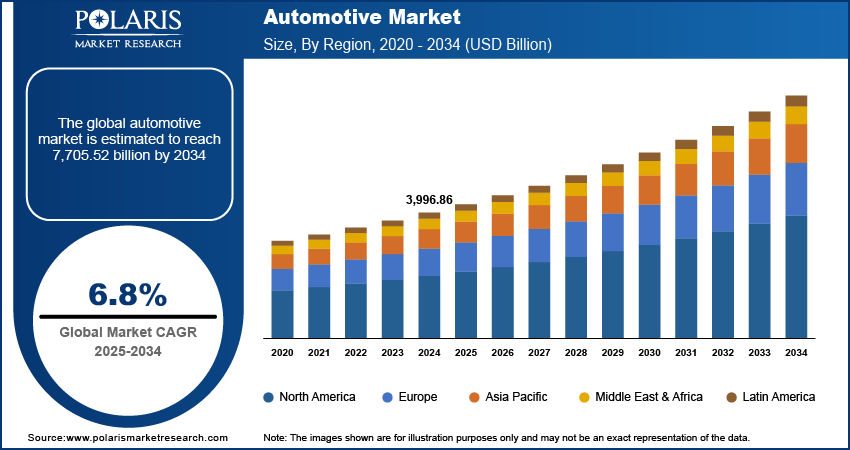

The global automotive market size was valued at USD 4,379.52 million in 2025. According to our automotive industry forecast, the market is projected to account for a CAGR of 6.3% from 2026 to 2034.

Market Statistics

Key Takeaways

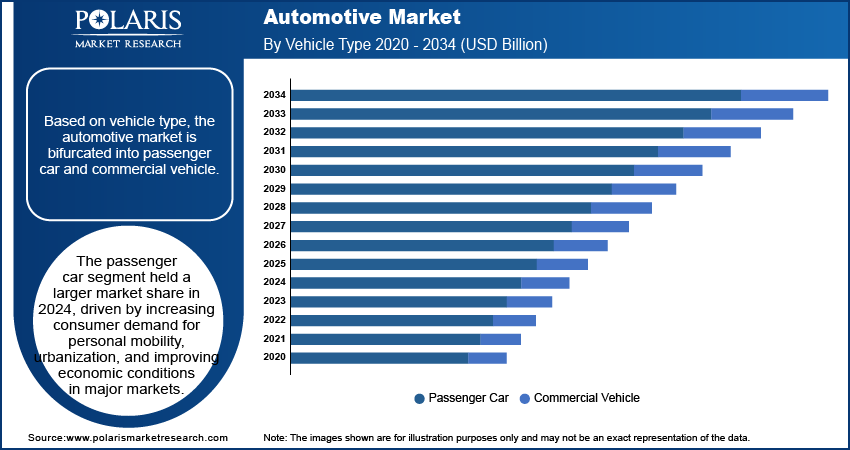

- The commercial vehicle segment led revenue in 2025, generating USD 2,070 million. It is driven by the rise in e-commerce activity and demand for LCVs for last-mile delivery services.

- The passenger car segment accounted for the second-largest revenue in 2025. This is due to increased consumer demand for passenger vehicles. The segment also benefits from improving economic conditions in key global markets.

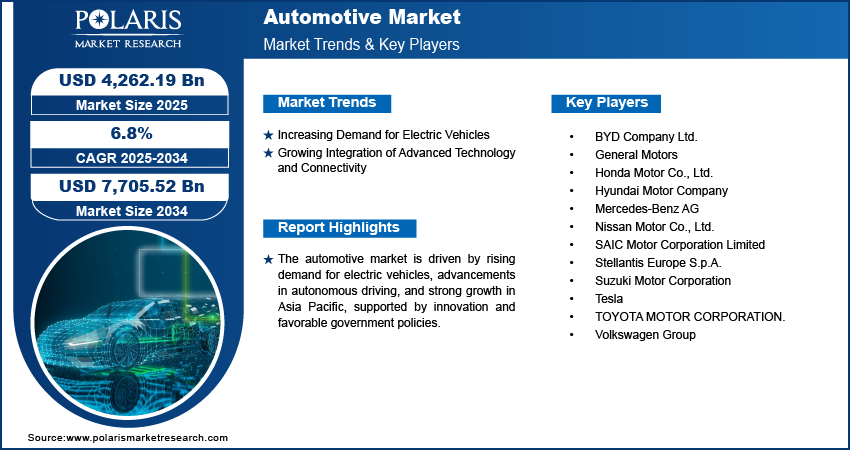

- The electric vehicle segment CAGR is expected to be 12.4% during the projection period. The segment is driven by rising environmental consciousness among consumers and the implementation of favorable government regulations on clean energy vehicles.

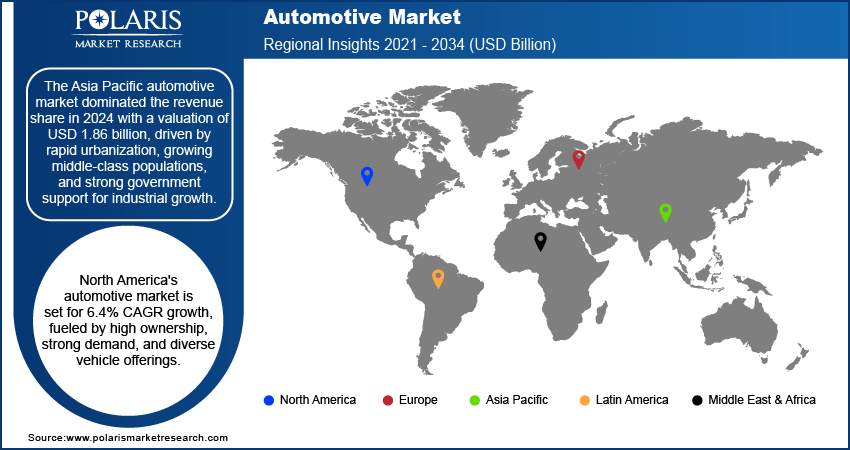

- The Asia Pacific automotive market led the global industry with USD 1,860 million in revenue in 2025. This is due to rapid urbanization and strong government industrial growth initiatives.

- The North America automotive market is projected to grow at a 6.8% CAGR. High vehicle ownership and strong consumer demand contribute to the regional market growth.

The world is witnessing a global push to reduce carbon emissions. This is resulting in a wide acceptance of electric vehicles. Various governments are providing incentives for using electric vehicles, and advancements in technology are making batteries more efficient. Many automobile manufacturers are launching a wide range of electric vehicles to reduce their carbon footprint. This is changing the traditional vehicle landscape and attracting environmentally conscious consumers.

This report includes revenue generated by both passenger and commercial vehicles, including internal combustion engine vehicles and electric vehicles. Additionally, it takes into account enabling technologies such as advanced driver assistance systems (ADAS), connected vehicle technologies, vehicle-to-everything (V2X) communication, and software-defined vehicle (SDV) platforms. Moreover, it also takes into consideration the impact of the ecosystem, including aftermarket and mobility services.

Industry Dynamics

- The demand for automotive technologies is rising due to growing consumer preference for advanced safety features and fuel efficiency. Demand is also growing due to rising urbanization and the shift towards electric and autonomous vehicles.

- There have been innovations in AI-powered driver assistance. IoT devices are also being increasingly integrated. The use of shared mobility services is improving user experience and making operations efficient. All of this is supporting market expansion.

- Challenges such as strict emission norms, high manufacturing costs, and regional policies may hinder the growth and profitability of car manufacturers and suppliers.

- Technological advancements in real-time diagnostics, V2X communication, and software updates are enhancing user experience and vehicle performance. They are also making sustainable and smart mobility solutions possible.

AI Impact on Automotive Market

- AI improves personalization in the automotive market. It can analyze the behavior, preferences, and usage patterns of the driver and provide personalized experiences in vehicles, such as infotainment, temperature, and routing.

- By integrating AI, adaptive driving assistants are achieved in vehicles. AI adjusts the cruise, lane, and braking systems according to road and traffic conditions and the driver’s actions.

- AI-based analytics help in the identification of vehicle performance and potential maintenance issues, thereby allowing predictive servicing and minimizing the risks associated with breakdowns or costly repairs.

- AI optimizes user engagement, and it achieves this by allowing voice-controlled interfaces, smart notifications, and personalized dashboard alerts, thereby improving the convenience, safety, and satisfaction of the driver.

- In addition, AI improves manufacturing yields and quality inspection, helping manufacturers identify problems with vehicles and produce higher-quality vehicles. AI is also useful in battery analytics, where it analyzes data from batteries to improve efficiency and extend battery life. AI is useful in demand forecasting, where it analyzes sales patterns and market trends to improve forecasting for companies. In addition, AI is useful in fleet optimization, where it identifies the fastest and most efficient routes for vehicles to take.

To Understand More About this Research: Download Sample Report

The automotive market refers to the designing, development, manufacturing, marketing, and selling of motor vehicles. The market comprises passenger cars, commercial vehicles, electric vehicles, and vehicle components such as engines, batteries, and electronic components. It also encompasses the integration of advanced technologies such as autonomous technologies, connectivity technologies, and mobility services. The automotive market has been growing significantly because of the innovations in the industry, the need to comply with government regulations, and the changing needs of customers. The growing trend of investing in artificial intelligence, sensor fusion technologies, and machine learning platforms has been driving the development of autonomous vehicles. Companies are already in the process of testing Level 3 and Level 4 autonomous systems. The potential for reduced accidents and optimal traffic flow is generating interest in the tech and automotive industries. The potential for saving operational costs is also a driving factor for autonomous systems. Additionally, the automotive aftermarket is growing, driven by the increasing average age of vehicles and the growing demand for personalization. People are personalizing vehicles with performance, aesthetic, and infotainment upgrades. E-commerce and digital engagement are making automotive parts more easily accessible, further contributing to a new source of revenue for the automotive industry.

The automotive market has grown in Asia, Latin America, and Eastern Europe. This is due to cost benefits and infrastructure developments in the region. Global automotive manufacturers are establishing automotive hubs in these countries to improve their presence in the region. The other aspect is to lower manufacturing costs and meet the increasing demand from the region's middle-class population. Increased awareness of road safety has led to the development of ADAS systems, such as lane departure warning, automatic emergency braking, and adaptive cruise control. Various countries have made these systems mandatory for new vehicle models. For example, the EU made it mandatory for ADAS systems to be included in all new vehicles in June 2024. This includes intelligent speed assistance, drowsiness detection, and automated braking systems. The regulations seek to save 25,000 lives and prevent 140,000 serious injuries by 2038. The automakers have to incorporate safety features, which influence vehicle design, component innovation, and the manufacturing process. As regulations vary, compliance is an essential aspect in the innovation of the industry. Demand for safe vehicles is also influencing consumer behavior.

Industry Dynamics

Rising Demand for Electric Vehicles (EVs)

Consumers as well as governments are focusing on energy-efficient modes of transport. This has led to the adoption of EVs. The 2024 IEA report showed that the sales of electric cars in 2023 rose by 3.5 million units from 2022. This is a 35% rise in the sales of electric cars. This can be attributed to the global drive towards the adoption of eco-friendly transport systems. In this respect, the need for the reduction of emissions from the use of these cars has encouraged the adoption of EVs. Moreover, the development of battery technology with the use of solid-state batteries, nickel-rich cathode materials, lithium-sulfur battery technology, and composite materials aims at increasing the efficiency of the storage of energy in compact designs. These developments are making EVs more accessible to a wider audience. They are changing the design, supply chain, and manufacturing process for vehicles. They are making EVs a key part of the industry's future. As environmental regulations become stricter, the automotive sector is accelerating its shift toward electrification to align with long-term sustainability goals. Therefore, the rising demand for EVs drives the automotive industry.

Urbanization and Infrastructure Development

The rapid expansion of urban centers is directly impacting the growth of the automotive market. With a growing need for reliable personal and public transportation systems, people are moving in large numbers to urban centers. Urbanization provides a denser population, economic opportunities, and increased disposable income, all of which contribute to a higher rate of automobile ownership. Governments and planners are responding to these changes in urban centers by investing in better road systems and improved traffic management systems. There is also a focus on increased suburbanization. For example, according to an April 2025 report by the India Brand Equity Foundation, India has the second-largest road network in the world, measuring 6.7 million km. Over 64.5% of goods and 90% of passenger traffic are transported on these roads. The constant upgrade of connectivity between urban, suburban, and rural areas has led to a steady increase in road transport. These infrastructure developments make car ownership convenient and even a necessity for daily commutes. In newly developing regions where public transport is not readily available, personal vehicle ownership is the norm.

Improved road and highway infrastructure reduces vehicle wear and tear. It makes driving more comfortable and appealing. Moreover, it can facilitate services like car sharing and hailing, which necessitate a constant flow of vehicles on the road. Hence, urbanization and the development of infrastructure contribute to the growth of the automotive market.

Segmental Insights

Vehicle Type Analysis

The segmentation, based on vehicle type, includes passenger car and commercial vehicle. The commercial vehicle segment held the largest market share, with a value of USD 2,070 million in 2025. This is because of the growth of e-commerce and logistics services. The growth has driven increased demand for LCVs for logistics and last-mile services. According to a December 2023 report by the International Trade Administration, e-commerce penetration in the German market stood at 80% in 2022. E-commerce and logistics players are adding vehicles to their fleet. Vehicle addition is being done to meet faster delivery requirements and serve growing online consumers. Moreover, increased government spending is driving industrialization and infrastructure development. The development is mainly across major regions such as Asia, North America, and Europe. This is boosting demand for medium- and heavy-duty vehicles. According to the Council on Foreign Relations, the IIJA in the U.S. included USD 550 billion in spending to upgrade physical infrastructure, including roads, bridges, railways, airports, and water systems. These vehicles are essential for moving raw materials, machinery, and products over long distances.

The passenger car segment had the second-largest revenue share in the global automotive market in 2025. The passenger car segment is growing due to the rising demand for personal mobility among consumers, urbanization, and improving economic conditions in the major markets of the world. The improving economic conditions in the world's major markets have led to an increase in the number of people owning cars, especially in emerging economies. In addition, technological advancements in safety and fuel efficiency have made passenger cars more appealing to buyers. The manufacturers of passenger cars have been introducing new passenger cars to the market to satisfy the growing demand for technological features in passenger cars. The incentives provided by governments to the owners of passenger cars have also led to the growth of the passenger car segment in the global market.

Commercial fleets are focusing on electrification and telematics. Emphasis is also being placed on route optimization. This is being done to lower delivery costs and make operations efficient. Demand for passenger vehicles is influenced by telematics adoption, ADAS integration, and availability of finance and leasing options.

Propulsion Type Analysis

Based on propulsion type analysis, the market is segmented into ICE vehicle and electric vehicle. The electric vehicle segment is expected to grow at the highest CAGR of 12.4% during the forecast period. The segment is driven by factors such as environmental awareness and the government's initiatives for promoting clean energy-based transport systems through regulatory policies. Technological developments in battery technology, as well as the decrease in the prices of electric vehicle components, are also driving the segment. Automotive companies are working on the development of electric vehicles to cater to the growing demand from consumers. The government is providing funds to build infrastructure for charging electric vehicles, and this is making it easier for consumers to buy electric vehicles. For instance, according to the Electric Vehicle Council, in April 2023, Australia’s Minister for Climate Change and Energy announced that the government would invest USD 39.3 million in expanding infrastructure for electric vehicles. This will be achieved by setting up 117 fast-charging points on Australia’s national highways. Additionally, the strict emission policies and incentives for the use of electric vehicles are contributing to the growth in this area. With the rise in carbon neutrality policies worldwide, electric vehicle adoption will accelerate.

The ICE vehicle segment dominates the market in terms of share, with a 85.6% market share in 2025. This is because of the existing infrastructure for fuel production and distribution. Gas stations for gasoline and diesel fuels are available in both urban and rural settings. They are common in regions such as North America, Asia, the Middle East, and Africa. This makes ICE vehicles convenient for long-distance drives and for use in rural settings. The affordability of ICE vehicles is another contributing factor to their popularity. The initial cost of an ICE vehicle is lower than that of an electric vehicle. Therefore, ICE vehicles are popular in regions where customers are price-sensitive. Additionally, ICE vehicles are cheaper to maintain in the long term. The parts and mechanics of ICE vehicles are available in the market. This makes their maintenance costs lower compared to electric vehicles. The performance of ICE vehicles is a contributing factor to their dominance in terms of market share. The torque and efficiency of heavy-duty diesel engines make them suitable for use in transporting goods for long distances.

EV growth rates are higher in locations with reliable infrastructure, government incentives, and decreasing battery costs, while ICE vehicles are more popular for long-distance transport, heavy-duty applications, and locations where infrastructure and costs are critical decision-making factors.

Regional Analysis

The report provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific automotive market led the market with a 1,860 million revenue share in 2025. Rapid urbanization, the growing middle-class population, and government encouragement of industrial development contribute to the regional market's growth. India, Thailand, Indonesia, and Vietnam are emerging as new manufacturing centers. This is because of the improvement in infrastructure, the rise in foreign direct investments, and the availability of cost-effective labor. According to Invest India, India achieved a Foreign Direct Investment (FDI) of USD 37.21 billion as of September 2024. There is an increasing demand for entry-level, mid-range, and premium cars, especially in urban areas, as the purchasing capacity of the population is growing in the region. According to the OECD, the per capita disposable income of the population in Australia in 2024 was USD 41,194, rising from USD 34,894 in 2020. Asia Pacific leads due to the presence of major automotive manufacturing hubs and favorable policy incentives. Asian Pacific countries' governments are providing incentives for automakers. The incentives include tax exemptions, free land, and reduced import duties on components used for manufacturing automobiles. The Indian government, as per the Ministry of Heavy Industries, offers an incentive of INR 25,938 crore under the production-linked incentive scheme, equivalent to USD 3,163.17 million. At the same time, many of the Asian Pacific countries are encouraging the use of advanced technology for vehicles. Advanced vehicle technology includes hybrid systems and fuel-efficient internal combustion engines. Moreover, free trade agreements in the region, such as RCEP (Regional Comprehensive Economic Partnership), facilitate the smooth flow of auto parts and vehicles across borders. Further, investments in digital infrastructure and smart mobility solutions are creating new opportunities in connected vehicles, thus contributing to the growth.

China Automotive Market Overview

China led the market with a 51.53% share. The market in this country is driven by robust domestic manufacturing and consumer demand. Also, a robust supply chain environment, coupled with high-end innovation in electric and smart vehicles, makes this market even stronger. Moreover, support for new energy vehicles and high-end urbanization in the country also fueled the market. Further, the country's large production capacity makes the market even stronger in terms of scaling and cost efficiencies.

North America Automotive Market Trends

The market in North America is projected to register a CAGR of 6.4% during the forecast period. The regional market is supported by high vehicle ownership rates, strong consumer demand, and a wide range of vehicle options, from pickup trucks and SUVs to electric and hybrid cars. According to the Pew Research Center, 78% of workers ages 16 and older usually drive to their jobs in a car in the U.S. A combination of consumer preferences, government regulations, and technological advancements shapes the market. The growing shift toward electric vehicles (EVs) and zero-emission vehicles is further shaping the market. Governments in the region are providing incentives for purchasing EVs and ZEVs, which is driving a rise in automotive sales. According to the Government of Canada, the government provides up to USD 5,000 at the point of sale to Canadian individuals and businesses for the purchase or lease of light-duty ZEVs. This transition is also noticeable in the U.S, where companies such as Tesla, Ford, and GM are leading the charge.

The growth of the logistics industry in North America is driving demand for light, medium, and heavy trucks. According to Data Mexico, 437,000 people were employed in the transportation and warehousing industry in the third quarter of 2024. Trade agreements, like the United States-Mexico-Canada Agreement, are also affecting the industry. These agreements are promoting international manufacturing and creating a competitive environment for manufacturers. The growth in North America is being driven by the electrification of pickups and SUVs, investments in battery manufacturing, as well as the rising demand for electric vans in commercial fleets. Government incentives and the expansion of charging infrastructure are also driving the market in the region.

U.S. Automotive Market Insights

The U.S. automotive market is growing. The market is fueled by the rising demand for technologically advanced and feature-rich vehicles. There is an increased requirement for digital integration and safety features in vehicles, and manufacturers are meeting this requirement. Regeneration of manufacturing and investment in mobility solutions is also contributing to market growth. In addition, changes in consumer behavior for hybrid and electric vehicles are impacting production strategies and creating opportunities for innovation.

Europe Automotive Market Analysis

The Europe automotive market is projected to reach USD 1,500 million by 2034. This is due to strict environmental standards, pushing automakers to invest heavily in cleaner technologies, fuel efficiency, and safety systems. The European Commission proposed a new emissions standard for road vehicles, Euro 7, in November 2022. These new rules are expected to lower air pollution from new motor vehicles introduced in the EU, both light and heavy, in line with the green deal’s zero pollution objective. The new regulations cover the entire automotive industry, from electric vehicles to different processes and engines. Despite the introduction of strict regulations, European countries continue to offer incentives to automakers for various purposes. In addition, funds are available for R&D across sectors such as autonomous driving, lightweight materials, and next-gen mobility platforms. Stricter safety and emissions regulations are prompting carmakers to increase their adoption of ADAS and invest more in software-defined vehicles. These regulations are also prompting suppliers to innovate in areas such as sensors, braking systems, and battery supply chains.

According to the European Commission, Europe has presented an Action Plan for the automotive industry. The plan is designed to expand the car industry and create jobs that drive growth. It is expected to attract private partners to invest in a joint public-private initiative of around €1 billion (USD 1.16 billion) by 2027. Moreover, the commission is expected to allocate €1.8 billion (USD 2.09 billion) to create a secure and competitive supply chain for battery raw materials to avoid dependency. Furthermore, the commission has planned to expand European Globalization Fund support to help companies and workers, as needed, address skills shortages, mismatches, and an ageing workforce in the automotive sector, driving the growth of the industry in Europe.

UK Automotive Market Outlook

The emphasis on sustainable mobility and a rising commitment to zero-emission transportation are key factors supporting the UK automotive market. Advances in technology and a strong engineering skill base are helping to place the UK on a trajectory that will enable it to become a leader in automotive innovation, especially in electric vehicles. Strategic partnerships and investments in R&D are supporting the long-term growth prospects in the automotive industry. Furthermore, consumer interest in eco-friendly transportation is creating a market for advanced-technology vehicles.

Key Players and Competitive Analysis

The automotive industry is currently undergoing a transformative change. The automotive competitive landscape is being driven by technological advancements, sustainability strategies, and geopolitical changes that are impacting supply chains. Industry leaders are using strategic investments in electrification and autonomous driving to create new revenue streams, while emerging markets offer growth opportunities. Competitive intelligence has shown that OEMs are focusing on joint ventures and mergers and acquisitions to drive innovation and reduce supply chain disruptions. Small and medium-sized businesses are also picking up pace by focusing on niche products. Developed countries are focusing on sustainable value chains and business transformation to meet changing regulations. Industry growth has shown a growing latent demand for connected vehicles. Manufacturers are focusing on fine-tuning their products and footprints in response to these shifts.

A few key players in the automotive market are BYD; General Motors; Honda Motor Company; Hyundai Motor Company; Mercedes-Benz; Nissan Motor Co., Ltd.; Stellantis N.V.; Suzuki Motor Corporation; Tesla; and Toyota Motor Corporation; and Volkswagen.

Competitive Landscape Perspective

Legacy OEM Transformation: Established automobile manufacturers are speeding up their transition to electric vehicle platforms andsoftware-defined vehicles. Focus is also on long-term battery supply agreements to remain competitive in an electrified automotive landscape.

EV-first Leaders: Electric vehicle-centric companies are gaining traction in terms of product development speed, software integration capabilities, and battery, manufacturing, and design control.

China-led Competition: Chinese car manufacturers are expanding globally, investing heavily in manufacturing and innovation for new energy vehicles (NEVs).

Supplier Battlegrounds: The competition for suppliers is increasing, especially for components such as semiconductors, power electronics, sensors, and battery materials. These components have a crucial role in determining the performance of the vehicle.

List of Key Companies

- BYD

- General Motors

- Honda Motor Company

- Hyundai Motor Company

- Mercedes-Benz

- Nissan Motor Co., Ltd.

- Stellantis N.V.

- Suzuki Motor Corporation

- Tesla

- Toyota Motor Corporation

- Volkswagen

Industry Developments

September 2025: Hyundai Motor Company revealed its 2030 Vision at CEO Investor Day. The company’s target of selling 5.55 million vehicles worldwide by 2030 was highlighted. The company also revealed its plans to expand into new segments. (Source: hyundai.com)

June 2025: General Motors announced the signing of an MoU with Redwood Materials. The agreement is aimed at improving the deployment of energy storage systems. Both second-life battery packs from GM electric vehicles and new U.S.-manufactured batteries will be used for the same. (Source: news.gm.com)

June 2025: General Motors delivered the first hand-built Cadillac CELESTIQ to its owner in a private ceremony at the General Motors Global Technical Center. (Source: news.gm.com)

May 2025: Suzuki Motor Corporation’s subsidiary in Indonesia, PT SUZUKI INDOMOBIL MOTOR, launched the new compact SUV “FRONX, based on the concept of an easy-to-handle coupe-style SUV. (Source: globalsuzuki.com)

March 2025: Nissan unveiled updated models and next-gen tech for FY25-26. This includes hybrid models such as ePOWER/PHEV, advanced EVs, and ICE models. This is to improve performance, retain customers, and promote sustainable growth while accommodating different powertrain requirements. (Source: nissannews.com)

Market Segmentation

By Vehicle Type Outlook (Revenue, USD Million, 2021–2034)

- Passenger Car

- Hatchback

- Sedan

- SUV

- MUV

- Commercial Vehicle

- LCVs

- Heavy Trucks

- Buses & Coaches

By Propulsion Type Outlook (Revenue, USD Million, 2021–2034)

- ICE Vehicle

- Electric Vehicle

By Ownership Model Outlook (Revenue, USD Million, 2021–2034)

- Individual Ownership

- Fleet Ownership

- Subscription-Based

- Shared Mobility

By Sales Channel Outlook (Revenue, USD Million, 2021–2034)

- OEM Dealers

- Independent Dealers

- Online Platforms

- Direct-to-Consumer

By Regional Outlook (Revenue, USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Automotive Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 4,379.52 million |

| Market Size in 2026 | USD 4,640.10 million |

| Revenue Forecast by 2034 | USD 7,595.99 million |

| CAGR | 6.3% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Automotive Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The automotive industry stood at USD 4,379.52 million in 2025. It is projected to reach USD 7,595.99 million by 2034.

The market is projected to account for a CAGR of 6.3% between 2026 and 2034.

The Asia Pacific automotive market led the global market in 2025. Rapid urbanization and the growing middle-class population contribute to the region’s leading market position.

A few of the key players in the market are BYD; General Motors; Honda Motor Company; Hyundai Motor Company; Mercedes-Benz; Nissan Motor Co., Ltd.; Stellantis N.V.; Suzuki Motor Corporation; Tesla; and Toyota Motor Corporation; and Volkswagen.

The commercial vehicle segment held the largest market share in 2025. This is because of the growth of e-commerce and logistics services.

Download Sample Report of Automotive Market

Please fill out the form to request a customized copy of the research report.