Liquefied Petroleum Gas (LPG) Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Liquefied Petroleum Gas (Lpg) Market Summary

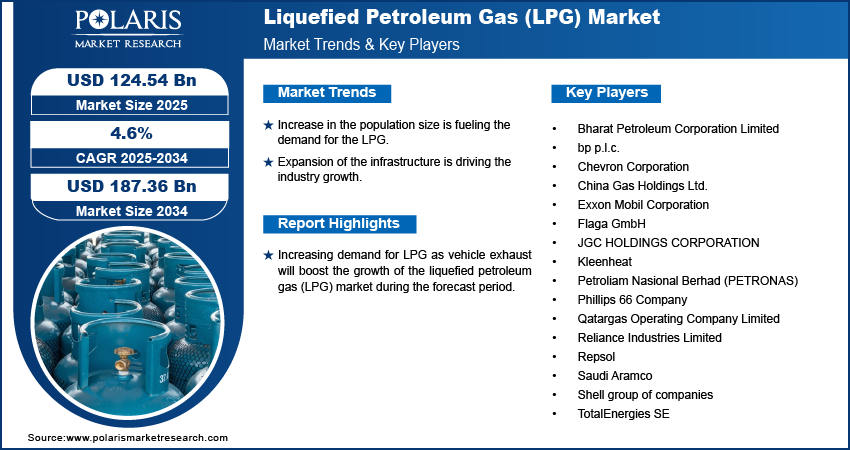

The global liquefied petroleum gas market is valued at USD 124.54 billion in 2025 and is projected to grow at a CAGR of 4.6% during the forecast period. A significant portion of GDP is spent by developing countries on expanding gas pipeline infrastructure. Increasing energy demand due to cheaper and more reliable fuel options makes the market outlook look optimistic in the near future.

Market Statistics

Key Takeaways

- Asia Pacific dominated with the largest share of 48.34% due to rising demand from the residential sector for daily activity.

- Europe is expected to witness a significant growth rate of 5.80% CAGR, driven by the government's initiative to reduce carbon emissions.

- Non-associated gas accounted for the largest revenue share of 55.13% in 2025 due to increased production of LPG from un-related gas wells.

- The commercial and residential segments accounted for the largest revenue share of 44.10% in 2025 due to government subsidies for LPG as an alternative to traditional food

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Increase in the population size is fueling the demand for the LPG.

- Expansion of the infrastructure is driving the industry growth.

- Government incentives and subsidies for LPG is boosting its adoption.

- Volatility in crude oil prices is limiting the growth.

-market-size-by-region-2020-2034.png)

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What is liquefied petroleum gas (LPG)

Liquefied Petroleum Gas (LPG) is a flammable hydrocarbon gas mixture. It is mainly composed of propane and butane. LPG is stored in liquid form under pressure. LPG includes features such as portability, lower emissions, and high energy efficiency. It is widely used as a clean, efficient fuel for cooking, heating, industrial applications, and transportation

The overall increase in LPG consumption recorded in 2021 is 7.7%, with a cumulative increase of 5.4% for the period from 20 April to 21 February. As of February 2021, among the five regions, North America has the highest share of its LPG sales at 31.8%.

The United States produced about 234,000 tons of LPG from natural gas and 10,000 tons of LPG from refineries in 2018, averaging about 91.4 billion cubic feet per day, suggesting that natural gas is the dominant source of LPG production. Increasing acceptance levels of clean and green energy sources in both developed and developing countries, and rural populations replacing LPG with traditional cooking fuels such as kerosene, wood, and coal.

Increasing demand for LPG as vehicle exhaust will boost the growth of the liquefied petroleum gas (LPG) market during the forecast period. Meanwhile, cost efficiency, fuel efficiency, emission control, trade procurement and expansion, and increased R & D activity associated with store allocations will further contribute by creating significant opportunities to the market.

LPG consumption saw a tremendous decline in the first half of 2020 as the COVID-19 pandemic continues to hinder the growth of industrial sectors around the world. Strict blockage regulations are imposed in some countries, and the demand for LPG is increasing. Petroleum as fuel is steadily declining.

Today, some market players are expected to explore opportunities beyond traditional markets to meet LNG demand in these regions. For example, as the outbreak of COVID-19 continued to reduce demand for liquefied natural gas in Europe, Russia's largest petrochemical company, Sibur, seized the opportunity to enter new markets by supplying liquefied natural gas to India.

Demand from the European Union countries may continue to be sluggish, but LNG demand from the housing and household sectors may increase in all Asia-Pacific countries despite the COVID-19 event. In addition, LNG is considered a necessity and is expected to remain firm in the future. The market is far from expected growth in 2020, but may be showing signs of recovery as of the fourth quarter of 2020. The automotive sector is expected to offer many opportunities for players involved in the market in the non-COVID-19 era.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Industry Dynamics

Growth Drivers

An increase in the world population will lead to a global increase in energy consumption. This, coupled with the growing development of infrastructure around the world, represents one of the key factors that have a positive impact on the market.

In current scenario, LPG is increasingly being used in a variety of agricultural, commercial, horticultural, industrial, and manufacturing applications as awareness of potential environmental and health benefits continues to grow. However, this is due to numerous benefits such as convenience, non-toxicity, non-poisonous, and low cost. Due to these assets in contrast to other types of fuels, the global market for LPG shows consistent growth.

As per the World Energy Council (WEC), the U.S has a total of 1,161 tcf of un-conventional gas, while China has 1,115 tcf of un-conventional gas. The U.S was the top producing country in the gas production. Some of the factors behind the growing demand for LPG are the increased consumption of LPG and the large quasi-urban and rural populations in Africa, Latin America, and the Asia Pacific. Locals in these areas use this product as fuel for cooking.

In India, for example, almost 80% of all house related energy needs depend on liquefied petroleum gas as fuel for cooking. To government scheme like (PMUY), streamline subscription processes and payments, supply cylinders, and reduce reliance on traditionally used dangerous cooking fuels such as firewood and charcoal. Initiatives such as subsidies are increasing the acceptance of gas mixtures.

Report Segmentation

The market is primarily segmented based on Source, End Use, Supply Mode, and Regions.

| By Source | By End Use | By Supply Mode | By Region |

|

|

|

|

Source: Polaris Market Research Analysis

Liquefied Petroleum Gas Market, by Source

By source, the non-associated gas accounted for the largest revenue share due to increased production of LPG from un-related gas wells. In addition, increasing demand of the LPG from several industrial applications is expected to drive market growth. Fuel sources change by region. For case, most gas generation in North America comes basically from natural gas processing provisioning, but the Asia-Pacific region depends on refineries for its gas generation. Refineries are one of the foremost imperative sources of different gasses around the world.

-market-by-source-analysis-2020-2034.png)

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

The Residential and Commercial Segments Captured a Prominent Market Share

The commercial and residential segments accounted for a largest revenue share. Promising government subsidies and initiatives to support products as the primary alternative to traditional fuels such as wood and coal are key factors contributing to the growth of this segment. It is also used as a raw material in the chemical and allied industries to produce plastics.

Comparison of Residential, Commercial, Industrial, and Transportation Applications of LPG

| End-Use Sector | Primary Application | Key Benefits | Common Examples |

| Residential | Cooking, space heating, water heating | Clean-burning fuel, easy storage, cost-effective for households | Domestic kitchen gas cylinders, home heating systems |

| Commercial | Fuel for restaurants, hotels, hospitals, and small businesses | Reliable energy supply, efficient heating, lower maintenance | Commercial kitchens, laundries, hospitality sector |

| Industrial | Process heating, metal cutting, drying, and power backup | High calorific value, operational efficiency, lower carbon emissions than coal | Manufacturing plants, furnaces, ceramic industries |

| Transportation | Alternative automotive fuel (Auto LPG) for vehicles | Reduced vehicle emissions, lower fuel cost, engine longevity | Taxis, buses, fleet vehicles, passenger cars |

Source: Polaris Market Research Analysis

Asia Pacific Region Acquires the Largest Revenue Share in 2025

The Asia Pacific region is the largest market for LPG due to the widespread acceptance of LPG as the primary fuel for home cooking and hot water supply. LPG is plentiful and forecasts predict low prices for a long time, except for major political turmoil.

The chemical sector has grown tremendously in the region in recent years, using this gas as the main raw material for the synthesis of various chemicals and plastics. The autogas (LP gas as fuel) market is developing rapidly in the Asia Pacific region. The government has demonstrated a strong and long-term political commitment to promoting LNG as a transportation fuel. This factor is also driving the market.

Europe is the second most important market and continues to be one of the regional powers of LNG. LPG is driven by the government's initiative to reduce carbon emissions and the European Union's goal of becoming carbon-neutral by 2050 in the region's construction, food, and beverage, manufacturing, housing, agriculture, and transportation industries.

GCC countries are mega contributors to LPG market share in the Middle East and Africa. As a result, the utilization of gasoline in vehicles is common in the region. Middle East Expected to Grow on LPG as Gasoline Leads to CO2 Emissions.

On the other hand, although Africa has a small market share, the region is primarily under development and is expected to grow in commercial/residential applications. Latin America is also a strong growth region due to increased investment in alternative fuels. The rapid increase in global energy demand and the construction of new facilities to respond to the sudden population explosion and rapid urbanization are expected to support the growth of the global market.

-market-trends-by-region-2020-2034.png)

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Competitive Insight

Some of the dominant players operating in the global market include Exxon Mobil Corporation, Kleenheat, bp p.l.c., Bharat Petroleum Corporation Limited, Flaga Gmbh, Repsol, Chevron Corporation, Petroliam Nasional Berhad (PETRONAS), Phillips 66 Company, JGC HOLDINGS CORPORATION, China Gas Holdings Ltd., Shell group of companies, Reliance Industries Limited, Saudi Aramco, Qatargas Operating Company Limited, Total Se, and Others.

Recent Developments

- July 2025: Keyera agreed to acquire Plains’ Canadian NGL business for USD 5.15 billion, boosting its fractionation and export capacity. (Source: inspectioneering.com)

- February 2025: OMV Petrom began construction on a EUR 750 million Petrobrazi sustainable-fuels unit to produce bio-LPG, SAF, and renewable diesel. (Source: omv.com)

Future of LPG Market

The LPG market is expected to grow at a substantial rate in the coming years. Rising demand for cleaner and more efficient fuels across residential, commercial, and industrial sectors will drive the market expansion. Expanding rural penetration, especially in developing economies, will support wider household adoption. The development of bio-LPG and renewable LPG alternatives will strengthen sustainability goals. Additionally, LPG will play a key transitional role in the global energy shift toward lower-carbon fuel solutions

Liquefied Petroleum Gas Market Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 124.54 billion |

| Market size value in 2026 | USD 130.10 billion |

| Revenue forecast in 2034 | USD 187.36 billion |

| CAGR | 4.6% from 2026 - 2034 |

| Base year | 2025 |

| Historical data | 2021 - 2024 |

| Forecast period | 2026 - 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Segments covered | By Source, By End-Use, By Supply Mode, and By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies | Exxon Mobil Corporation, Kleenheat, bp p.l.c., Bharat Petroleum Corporation Limited, Flaga Gmbh, Repsol, Chevron Corporation, Petroliam Nasional Berhad (PETRONAS), Phillips 66 Company, JGC HOLDINGS CORPORATION, China Gas Holdings Ltd., Shell group of companies, Reliance Industries Limited, Saudi Aramco, Qatargas Operating Company Limited, Total Se, and Others. |

Source: Polaris Market Research Analysis

FAQ's

• The market size was valued at USD 124.54 billion in 2025 and is projected to grow to USD 187.36 billion by 2034.

• The market is projected to register a CAGR of 4.6% during the forecast period.

• A few of the key players in the market are Exxon Mobil Corporation, Kleenheat, bp p.l.c., Bharat Petroleum Corporation Limited, Flaga Gmbh, Repsol, Chevron Corporation, Petroliam Nasional Berhad (PETRONAS), Phillips 66 Company, JGC HOLDINGS CORPORATION, China Gas Holdings Ltd., Shell group of companies, Reliance Industries Limited, Saudi Aramco, Qatargas Operating Company Limited, Total Se, and Others

• The non-associated gas segment dominated the market revenue share in 2025.

• The residential & commercial segment dominated the market revenue share.

Download Sample Report of Liquefied Petroleum Gas (LPG) Market

Please fill out the form to request a customized copy of the research report.