Medical Laser Systems Market Opportunity, Industry Share & Global Report, 2026-2034

REPORT DETAILS

Medical Laser Systems Market Summary

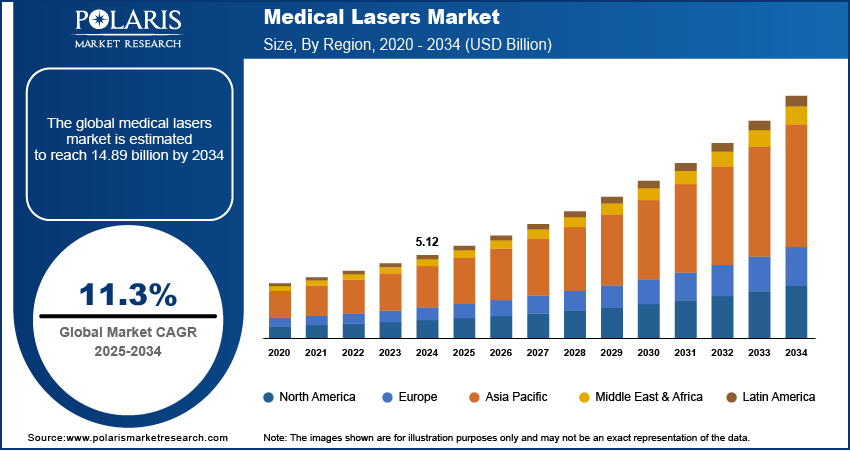

The global medical laser systems market is estimated around USD 4.30 Billion in 2025,?with consistent growth anticipated during 2026–2034. Growth is supported by rising adoption of minimally invasive medical procedures, increasing demand for aesthetic and dermatology treatments, and expanding applications of laser technologies in ophthalmology and surgical interventions. The market is projected to grow at a CAGR of 10.7% during the forecast period.

Market Statistics

Key Takeaways

- North America accounted for the largest regional share of around 41.2% in 2025, driven by advanced healthcare infrastructure, high adoption of technologically advanced devices, and increasing demand for laser-based treatments.

- By Application, Dermatology & Aesthetic segment accounted for the largest share of approximately 36.8% in 2025, supported by rising demand for non-invasive cosmetic procedures and skin rejuvenation treatments.

- By Product Type, Diode Laser segment is projected to grow at a CAGR of 7.9%, driven by compact design, lower operational costs, and high reliability across dermatology, dentistry, and minor surgical procedures.

- By End Use, Cosmetic Clinics segment is projected to grow at a CAGR of 8.3%, driven by rising demand for aesthetic medicine and increasing outpatient procedure volumes.

Industry Dynamics

- Growing demand for minimally invasive and non-invasive treatments is driving the adoption of laser-assisted treatments in dermatology, ophthalmology, and surgery.

- Ongoing technological developments with femtosecond laser systems and AI-assisted laser systems improve accuracy and efficacy of treatments.

- High investment costs of laser systems are a major factor hindering the adoption of laser systems in healthcare facilities.

- Development of AI-based laser systems and robotic surgical systems creates growth opportunities for the global medical laser systems market.

What is included in the medical laser systems market?

The Medical Laser Systems Market refers to the structured development, manufacturing, and commercial deployment of laser-based medical equipment used for therapeutic, surgical, and diagnostic procedures. A medical laser system is considered a capital medical device, which has the capability to produce controlled laser energy for interaction with targeted tissues, thereby providing cutting, ablation, coagulation, or photothermal treatments in medical settings. These medical laser systems are widely used in the medical industry, particularly in hospitals, clinics, and ambulatory surgical centers, where the use of precise energy treatments helps in achieving accurate results.

The market for medical laser systems includes surgical lasers, dermatological and aesthetic lasers, ophthalmic lasers, dental lasers, and urology/lithotripsy lasers. These medical laser systems utilize various laser technologies, such as diode, CO2, Nd:YAG, Alexandrite, and erbium, which allow precise targeting of the tissues with minimal damage. These systems are designed and developed with primary objective of providing reliable systems with stable energy and safety features, which enable the physicians to carry out precise treatments with minimal recovery time.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Medical laser systems market consists of capital laser equipment, integrated optical control systems, and clinical system software to control the equipment. Accessories such as lasers, fibers, probes, cooling gels, or eye protection are not included in the market value, except in situations where they are included in the purchase contract for the systems.

Drivers & Opportunities

Increasing demand for minimally invasive and non-invasive procedures: Growing demand for minimally invasive surgery coupled with preference for faster recovery and lower risk of procedures is driving the market. According to the American Society of Plastic Surgeons 2023 report, minimally invasive procedures grew by 7% year over year, reflecting higher patient adoption of cost-effective aesthetic treatments. This is also enhancing the cosmetic laser treatment market and increasing the demand for dermatology laser treatment. In addition, the advancement of technology, such as the introduction of femtosecond laser technology, is also increasing the precision and thereby boosting the medical laser systems market growth.

Rising prevalence of chronic diseases and vision disorders: Increasing chronic conditions and vision problems among patients is creating demand for the laser surgery treatment. The World Health Organization has estimated that chronic conditions may contribute to 86% of the estimated 90 million deaths projected for 2050. This rise in chronic conditions is propelling the need for medical laser systems used for cataract surgery and other medical procedures.

Restraints & Challenges

High initial equipment cost and maintenance requirements: High initial equipment cost is one of the major restraining factors for medical laser devices. Medical laser systems pricing analysis shows significant variation based on power output, imaging integration, and automation features. Regulatory barriers related to medical laser devices and laser safety regulations in the healthcare sector further increases the certification and compliance costs.

Opportunity

Development of AI-assisted laser systems: Integration of artificial intelligence is creating new business opportunities in the medical laser systems market. For instance, in October 2025, Monteris Medical and Symphony Robotics formed a strategic partnership to develop an artificial intelligence-based micro-robotic laser ablation system in the brain that combines robotics, artificial intelligence, and real-time MRI. This partnership is a step forward in advancing artificial intelligence-assisted laser systems to allow precise targeting and navigation in minimally invasive neurosurgical procedures. Integration of artificial intelligence in laser systems is beneficial as it adjust parameters automatically according to patient and treatment needs.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the medical laser systems market by product type, application, end users to help readers identify the fastest expanding and most attractive demand segments.

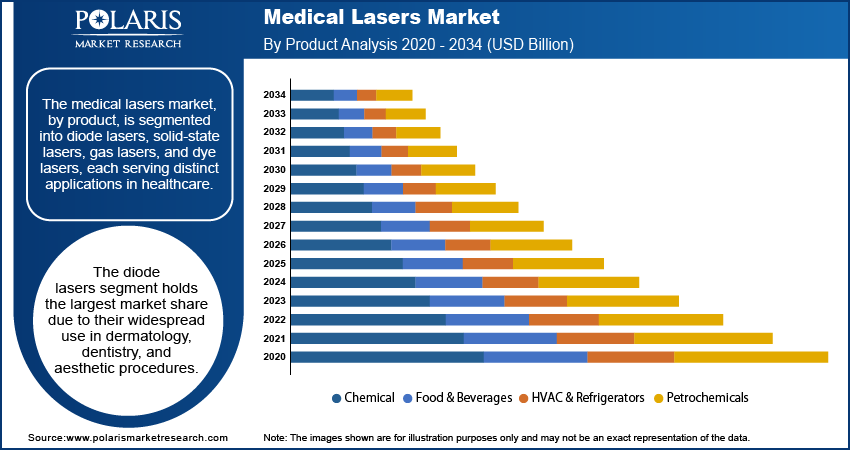

By Product Type

-

Diode Laser Systems

Diode laser systems account for the largest share of the diode laser systems market size due to broad clinical use across dentistry, dermatology, and minor surgical procedures. Its compactness, low operating cost, and reliability make it an ideal candidate for widespread adoption. The dental laser equipment segment is largely dependent on diode laser systems for soft tissue work and periodontal treatments.

-

Solid-State Laser Systems

The solid-state medical laser systems market represents the fastest-growing product segment. Nd:YAG medical laser systems are widely used in minimally invasive procedures due to deeper tissue penetration and high precision. Growth is particularly strong in ophthalmology laser devices market applications such as posterior capsulotomy and retinal photocoagulation.

By Application

-

Dermatology

Dermatology accounts for the largest share of the dermatology laser systems market size. Demand is driven by the expanding aesthetic laser devices market, including treatments for skin resurfacing, pigmentation correction, and hair removal. The laser skin resurfacing market continues to grow due to increasing consumer demand for cosmetic procedures.

-

Ophthalmology

The ophthalmology laser devices market is the fastest-growing application segment. Technological developments like femtosecond laser ophthalmology systems enable precise vision correction procedures. The demand for LASIK laser systems is fueled by an increase in demand from across the globe and wider accessibility of advanced vision correction technologies.

By End Users

-

Hospitals

Hospitals dominate held the largest market share in medical laser system. Multi-specialty hospitals use laser systems in dermatology, ophthalmology, and surgical departments.

-

Cosmetic Clinics

Cosmetic clinics accounted for the largest market share in 2025, propelled by the growing popularity of aesthetic medicine and non-invasive cosmetic treatments, laser treatment center. Dermatology and aesthetic clinics are showing increasing interest in acquiring technologically advanced laser equipment.

Source: Polaris Market Research Analysis

Regional Analysis

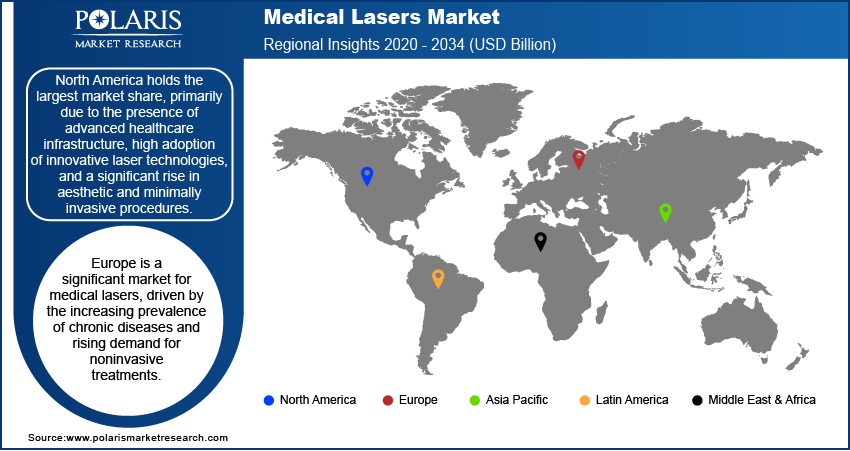

North America Medical Laser Systems Market Assessment

North America medical laser systems market held dominant position in the regional market, fueled by growing number of surgeries, established reimbursement practices, and rising trend of adopting AI-assisted surgical solutions. Hospitals and clinics are showing interest in acquiring laser-based solutions to perform urology, dermatology, and ophthalmology surgeries. In December 2025, Medtronic announced US FDA clearance of its Hugo robotic-assisted surgery system, which is indicated for a range of minimally invasive urologic surgeries, such as prostatectomy and nephrectomy. This development reinforced activity within AI-integrated surgical ecosystems and expanded procedural capabilities across advanced operating rooms.

Asia Pacific Medical Laser Systems Market Insight

Asia Pacific medical laser systems market is projected to grow at a fastest pace during the forecast period, propelled by the increasing healthcare infrastructure across China, Japan, Korea, and India. The growth of private hospitals and aesthetic treatment facilities is boosting demand for dermatology, ophthalmology, and minimally invasive surgical laser systems. In addition, rapid urbanization and increasing disposable incomes are further fueling cosmetic procedures. In India, private equity investment has reached to USD 572 million in the healthcare sector through 33 deals in Q2 CY25. Such investment trends are increasing the need for medical laser systems in India.

Europe Medical Laser Systems Market Overview

Europe was the second largest market in medical laser systems propelled by the rising development of high-standard infrastructure in the medical industry in Germany, France, and the UK. The medical industry has been utilizing high-tech laser systems in hospitals and clinics, particularly in ophthalmology, oncology, and dermatology procedures. Strict regulatory environment in the region is impacting the quality and safety of the products. The medical laser industry in Germany has been one of the significant contributors to the market, considering the high manufacturing capabilities in the country.

Latin America & Middle East Medical Laser Systems Market Assessment

The Latin America medical laser market and the Middle East medical laser systems market progressed through expanding medical tourism and modernization of specialty healthcare facilities. Cosmetic dermatology clinics and surgical centers in Brazil, Mexico, UAE, and Saudi Arabia are increasingly using advanced medical laser systems to attract international patients. The increasing investments in the healthcare sector and demand for minimally invasive procedures have contributed to the adoption of medical laser systems in emerging markets for medical laser systems.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The competitive scenario for medical laser systems is driven by innovation in medical lasers, precision in medical procedures, and increasing applications of medical lasers in dermatology, ophthalmology, dentistry, and surgery. The medical laser system market is highly competitive, with players developing advanced medical lasers for improved safety, precision, and ease of use for minimally invasive procedures. Strategic partnerships with hospitals, dermatology clinics, and ambulatory surgical centers are crucial in boosting the adoption of medical lasers in healthcare services.

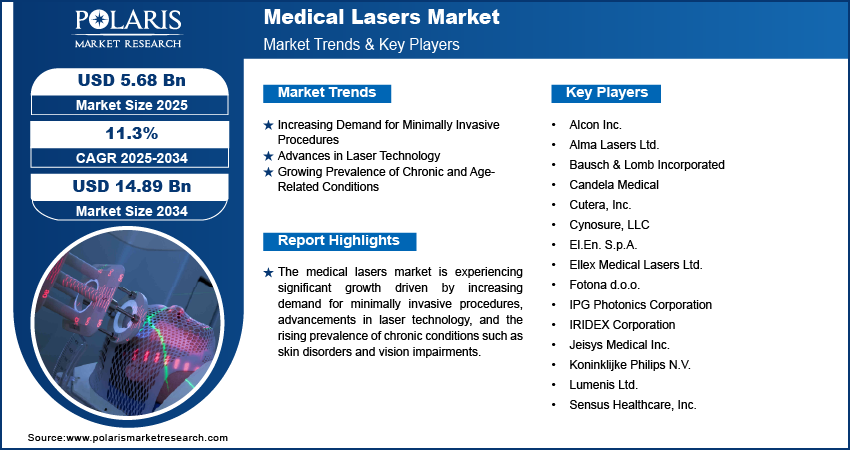

Leading companies in the medical laser systems market include Alcon Inc., Alma Lasers Ltd., Bausch Health Companies Inc., Biolase, Inc., Boston Scientific Corporation, Candela Medical, Inc., Carl Zeiss Meditec AG, Cutera, Inc., Cynosure, LLC (Hologic, Inc.), El.En. S.p.A., Fotona d.o.o., IPG Photonics Corporation, Koninklijke Philips N.V., Lumenis Be Ltd., and Lutronic Corporation.

Key Players

- Alcon Inc.

- Alma Lasers Ltd.

- Bausch Health Companies Inc.

- Biolase, Inc.

- Boston Scientific Corporation

- Candela Medical, Inc.

- Carl Zeiss Meditec AG

- Cutera, Inc.

- Cynosure, LLC (Hologic, Inc.)

- El.En. S.p.A.

- Fotona d.o.o.

- IPG Photonics Corporation

- Koninklijke Philips N.V.

- Lumenis Be Ltd.

- Lutronic Corporation

Pricing, Investment Trends & Strategic Opportunities

-

Medical Laser Systems Pricing Analysis

Pricing of various medical laser systems is based on applications, technology, and system capability. Dermatology and aesthetic laser systems are usually in the middle range of pricing, whereas surgical and ophthalmology laser systems are in a higher range of pricing. The cost of laser systems also covers accessories and treatment handpieces, and various software packages. Procurement decisions often favor multi-application platforms that improve clinical utilization and treatment flexibility.

-

Total Cost of Ownership (TCO) Considerations

The ROI medical laser equipment calculation extends beyond purchase price. Total Cost of Ownership includes maintenance contracts, calibration, consumables, and operator training. Laser systems with higher treatment capacity and upgrade potential offer higher returns with minimal downtime.

-

Investment & Expansion Opportunities

The rising rate of minimally invasive treatments is fueling investments in laser technologies. Venture capital investors are showing keen interest in next-generation laser technologies in medical devices. Emerging markets offer expansion opportunities for companies with private clinic and hospital investments in advanced technologies. An effective market entry strategy for medical laser systems includes partnerships with distributors and support services for facilitating adoption.

Industry Developments

- March 2026: Monteris Medical reported results from a new study showing that its NeuroBlate laser ablation system may enhance the effectiveness of immunotherapy in patients with recurrent high-grade brain tumors.

- September 2025: The Technology Innovation Institute (TII) unveiled its 2 µm high-power fiber laser platform for precision and next-generation medical devices.

- February 2024: BIOLASE launched the Waterlase iPlus Premier Edition, a next-generation all-tissue laser system designed to expand the use of lasers across dental procedures.

Medical laser systems Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021-2034)

- Diode Laser Systems

- Solid-State Laser Systems

- Gas Laser Systems (CO₂ & Excimer)

- Dye & Emerging Fiber Lasers

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Dermatology

- Ophthalmology

- Urology & Gynecology

By End Users Outlook (Revenue, USD Billion, 2021-2034)

- Hospitals

- Ambulatory surgical centers

- Cosmetic clinics

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Medical laser systems Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 4.30 Billion |

| Market Size in 2026 | USD 4.76 Billion |

| Revenue Forecast by 2034 | USD 10.72 Billion |

| CAGR | 10.7% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Medical Laser Systems Market FAQ's

• The global market size was valued at USD 4.30 Billion in 2025 and is projected to grow to USD 10.72 Billion by 2034.

• North America dominates due to high healthcare expenditure, strong adoption of advanced surgical technologies, and well-established hospital infrastructure.

• Major applications include dermatology treatments, ophthalmic surgeries, dental procedures, urology treatments, and minimally invasive surgical procedures.

• Key companies include Alcon Inc., Alma Lasers Ltd., Bausch Health Companies Inc., Biolase Inc., Boston Scientific Corporation, Candela Medical Inc., Carl Zeiss Meditec AG, Cutera Inc., Cynosure LLC, El.En. S.p.A., Fotona d.o.o., IPG Photonics Corporation, Koninklijke Philips N.V., Lumenis Be Ltd., and Lutronic Corporation.

• The factors propelling growth include rising demand for minimally invasive procedures, increasing aesthetic treatments, and technological advancements in laser-based medical equipment.

Download Sample Report of Medical Laser Systems Market

Please fill out the form to request a customized copy of the research report.