Minimally Invasive Surgery Market Trends, Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Minimally Invasive Surgery Market Summary

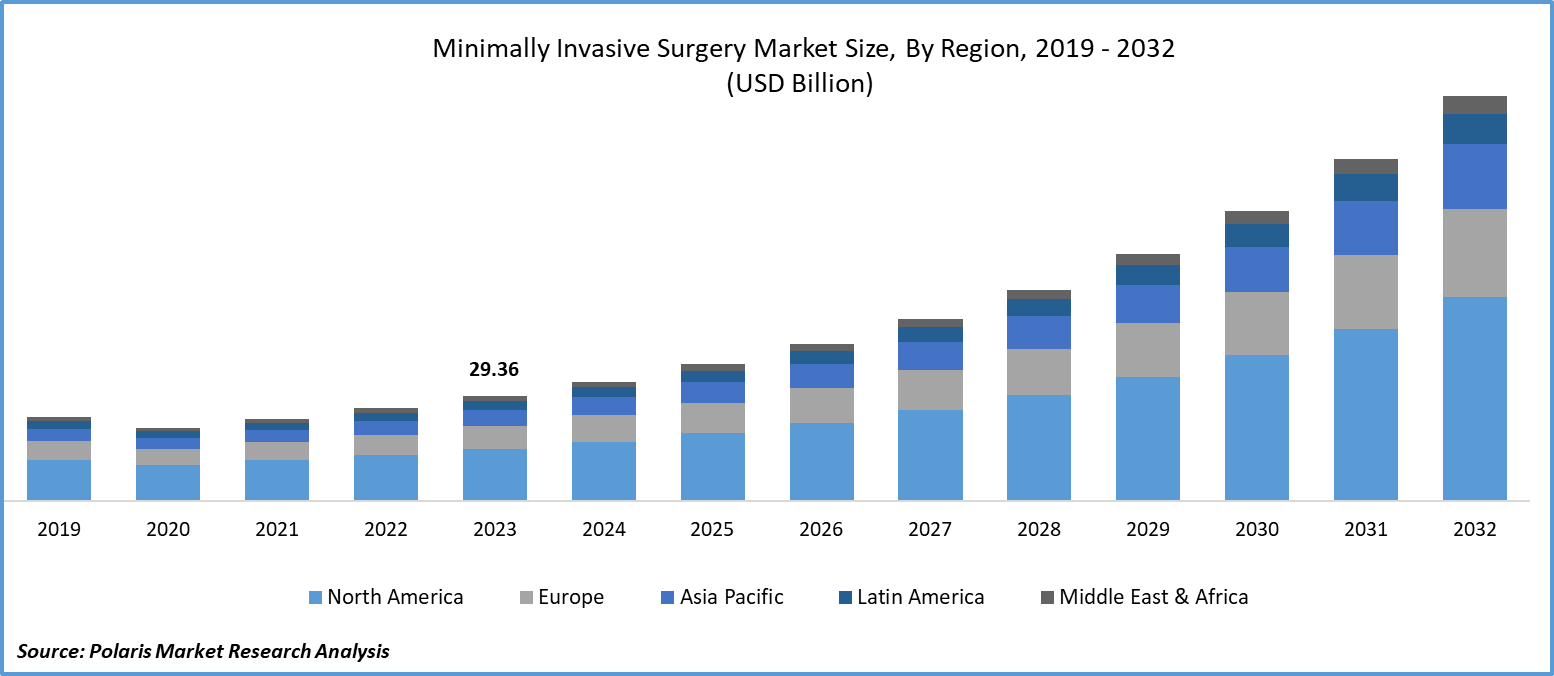

The global minimally invasive surgery market size was valued at USD 522.51 billion in 2025. The market is projected to account for a CAGR of 7.8% between 2026 and 2034. The irreversible shift away from open surgical procedures across all major clinical specialties is contributing to the market growth.

Market Statistics

Key Takeaways

- North America accounted for the largest market share of 39.2% in 2025. The surge in demand for MIS technology is attributed to the increasing cases of chronic ailments in the region.

- Asia Pacific is projected to register the highest CAGR of 8.5% during the forecast period. An aging population and rising healthcare expenditures contribute to the region’s rapid growth.

- The surgical devices segment led the market with a 48.6% revenue share in 2025. Surgical tools are fundamental components that play a vital role in surgeries.

- The neurological surgery segment is expected to account for the fastest growth rate of 8.9%. Growth is driven by advancements in imaging and surgical technologies.

- The hospital, clinics & ablation centers segment led the market with a 62.4% revenue share in 2025. Increased operating room capacity and favorable reimbursement policies have contributed to the segment’s leading market share.

Industry Dynamics

- The rising prevalence of orthopedic disorders has resulted in an increase in minimally invasive surgeries.

- Growing insurance coverage and the rise of AI-integrated surgical platforms is contributing to the market expansion.

- Expansion of ambulatory surgery centers presents several market opportunities.

- The expensive nature of robotic systems may present minimally invasive surgery market challenges.

To Understand More About this Research: Download Sample Report

Minimally invasive surgery (MIS) uses small devices, cameras, and lights to reduce the number and size of cuts during a procedure. Minimally invasive surgeries are safer than traditional procedures. This is because they involve fewer complications, shorter recovery time, less bleeding, and improved results. These aspects make minimal-invasive procedures increasingly popular among both surgeons and patients worldwide. Minimally invasive procedures are performed on patients undergoing orthopedic, vascular, neurological, and cardiothoracic operations.

For instance, in January 2024, Arthrex introduced TheNanoExperience.com, a new patient-oriented resource that showcases the science and advantages of Nano arthroscopy. This innovative orthopedic procedure is minimally invasive and has the potential to facilitate a swift return to activity with reduced pain.

The minimally invasive surgery market is experiencing a technology-driven shift in 2025-2026, with AI in minimally invasive surgery and robotic-assisted surgery market as key drivers of its development. AI-driven imaging, computer-assisted navigation, and robots such as the da Vinci 5 robot by Intuitive Surgical, the Hugo RAS robot by Medtronic, and the Versius system by CMR Surgical have been introduced to broaden the applicability of minimally invasive surgery. About 85% of eligible surgeries in developed healthcare systems are now performed using minimally invasive techniques. The move represents a clear trend away from conventional open surgeries, as technological advances have enhanced accuracy while minimizing patient downtime.

The expansion of the global market for minimally invasive surgical procedures can be attributed to several factors. Some of these include the increasing popularity of minimally invasive surgeries and higher investments by government and private organizations in setting up medical establishments. Technological advancements have also played an important role in this regard. The widespread presence of many long-term diseases, such as renal disorders, cardiovascular diseases, respiratory problems, and digestive disorders, has been a driving force behind market growth. Non-communicable diseases (NCDs) accounted for 43 million fatalities in 2021, as per the statistics released by the WHO. Cardiovascular diseases accounted for over 19 million deaths in 2021. It is followed by cancers (10 million) and chronic respiratory diseases (4 million). Diabetes led to over 2 million deaths in 2021. 73% all the NCD deaths are in low- and middle-income nations.

The growing number of elderly patients drives the minimally invasive surgery market growth, as they are more likely to suffer from chronic conditions. The rise in surgical cases also boosts demand. The development of robotic assistance and awareness regarding the benefits of minimally invasive surgeries are some of the factors that aid the market development. However, the high cost of procedures may present market challenges in the coming years.

Minimally Invasive Surgery Market Dynamics

Growing Number of Orthopedic Conditions

The rising prevalence of orthopedic disorders is one of the major minimally invasive surgery market drivers. According to the WHO, over 1.71 billion people globally live with musculoskeletal disorders. The rising global aging population has resulted in an increased number of people suffering from orthopedic diseases like osteoarthritis and bone fractures. This development has led to an increase in the need for orthopedic operations. Moreover, advances in minimally invasive surgery technology have made these operations even more effective and efficient. Patients are preferring minimally invasive operations to open surgery as the former results in faster recovery and fewer risks during the operation.

Rising Insurance Coverage

Laparoscopic treatment methods are less invasive and more economical than conventional methods. This affects hospital admission and pre- and post-operation costs. People undergoing procedures covered under the laparoscopic surgery market recover faster, lose less blood, and experience fewer postoperative complications. Furthermore, in certain nations, health insurance companies have begun covering these minimally invasive procedures. This is because physicians believe these operations will enable hospitals to reduce expenses, making them preferable to conventional surgical methods.

Rise of AI-Integrated Surgical Platforms

AI in healthcare is rapidly emerging as one of the most important factors driving the minimally invasive surgeries industry, shifting from innovation to practical application. Nowadays, such technology is widely used by surgeons to plan their operations, interpret imaging data during surgery, and even provide real-time guidance during surgery. For example, in December 2025, Medtronic announced that its Hugo robotic-assisted surgery system had been cleared by the FDA to conduct urological surgeries. This robot offers a flexible platform for use in the U.S.

Similarly, J&J MedTech advanced its OTTAVA platform based on early patient cases performed during gastric bypass surgery in 2025. Also, the MONARCH Platform for Urology from J&J MedTech, employing AI-simulated virtual operating room planning, is slated to be commercially available in the U.S. in 2026. The AI in minimally invasive surgery trends are helping minimize the learning curve for surgeons, thereby increasing the availability of complex minimally invasive surgeries. Consequently, the uptake of robotic-assisted minimally invasive surgery is rapidly increasing even in emerging economies, driving the industry's development.

Outpatient Shift and Growth of Ambulatory Surgical Centers

The trend of surgical procedures being moved from hospital settings to ambulatory surgical centers (ASCs) is quickly becoming one of the significant factors for growth in the minimally invasive surgery market. ASCs have many advantages in terms of costs, where procedures are generally cheaper by 45%–60% than surgeries done in hospitals. Patient satisfaction is also usually higher due to the reduced waiting time and better patient care.

MIS Market Restraints

Expensive Nature of Robotic Systems

Robotic-assisted surgeries tend to be more expensive compared to other procedures, thereby leading to a situation where some people either delay seeking treatment or avoid treatment altogether due to the costs involved. Additionally, aside from the general high costs of robotic surgery, there is the extra cost of maintenance, estimated at USD 125,000 per year. Budgets for many hospitals in Europe have declined, with the expectation of further such reductions in the coming years. Due to such budget limitations, there is an increasing need for measures to control costs across several areas of hospital operations.

Risk of Complications

The risk of complications is also one of the minimally invasive surgery market challenges. Although minimally invasive surgery offers many benefits, the risk of problems remains, but not as high as with conventional surgical procedures. Minimally invasive surgeries result in faster recovery times with minimal complications. However, concerns about patient safety, including the risk of organ damage, bleeding, or infections during minimally invasive procedures, may deter health care professionals from using these approaches.

MIS Regulatory Landscape Complexity and Surgeon Training Requirements

Approvals for MIS devices, especially those involving AI and automation, have become more stringent. In the U.S., for example, the FDA has tightened the standards for SaMDs and AI-driven tools. It mandates robust clinical evidence before granting approval. As such, companies have to spend longer periods in research and development, in addition to increased costs. In Europe, the transition to the EU Medical Device Regulation (MDR) has increased the certification timeline by 12 to 24 months, compared to the previous regime.

In addition to regulatory matters, another difficulty concerns the MIS training market. Surgeons must be trained through simulation before being allowed to work with robotic systems. This adds to the costs incurred by health care organizations. It also slows implementation processes, especially in lower- and middle-income countries where training infrastructure is still developing.

AI & Robotics Convergence in Minimally Invasive Surgery Market

The convergence of AI and robotic technology is transforming minimally invasive surgery. The initial surgeon-controlled systems have now evolved into a more advanced, integrated platform.

Current platforms include AI imaging, machine learning algorithms for outcomes prediction, and partial forms of surgical procedure automation. By using these technologies, surgeons can make more informed choices, ensure procedural uniformity, and begin automating specific surgical tasks.

Existing Application of AI in Minimally Invasive Surgery (2025-2026)

AI technology is currently employed at different phases of the minimally invasive surgery market. Pre-surgery planning software utilizes machine learning algorithms based on large databases of images to develop surgical maps for each patient that help to perform operations according to a more accurate route.

During surgery, computer vision technology incorporated into laparoscopic cameras detects the anatomical structures of interest and warns of potential risk zones that could lead to adverse consequences. In addition, prediction tools are used in hospital systems to predict risk associated with some patients. It helps in efficient planning for anesthesia, staffing, and resources.

Platform Development Milestones (2025-2026):

- Da Vinci 5 (2025): Manufactured by Intuitive Surgical, it has a state-of-the-art haptic feedback system along with AI-driven navigation in difficult procedures. In addition to this, it facilitates better data capture for surgical analyses.

- Hugo RAS: This platform by Medtronic demonstrated 98.5% effectiveness during trials. It was filed with the FDA in April 2025. The platform received FDA clearance on December 3, 2025. The first commercial surgery in the U.S. was performed in February 2026 at the Cleveland Clinic.

- OTTAVA Platform: Produced by Johnson & Johnson MedTech, the platform conducted its initial clinical procedures in April 2025. Following these initial procedures (which included a gastric bypass), the company submitted OTTAVA for FDA De Novo authorization in January 2026.

- Versius System: This system from CMR Surgical has been expanding into Latin America and Southeast Asia for hospitals that prefer a more compact and affordable robotic system.

- SSI Mantra 3: This surgical robot from India accomplished a breakthrough by conducting robotic cardiac surgery in the Americas. It is aiming for FDA approval by 2026.

- Toumai Robotic Surgery System: This multi-arm robotic surgery system with 3D visualization was launched in India by Kokilaben Dhirubhai Ambani Hospital in 2025 and includes a tremor-reduction feature.

- Swan EndoSurgical: This is a joint venture between Olympus Corporation and Revival Healthcare Capital. It was formed in July 2025 to advance endoluminal robotic technologies.

These trends indicate how AI and robotics are working together to improve surgical accuracy and expand access to more advanced procedures.

The minimally invasive medical robots market, which forms an important part of the overall MIS market, is experiencing rapid growth. The market size was estimated to be around USD 58.20 billion in 2025 and is expected to grow at a CAGR of 13.58%. Besides the current use of robotic technology, there is significant investment in next-generation systems. These new systems have incorporated aspects such as artificial intelligence, haptic feedback, and automation while being more economical. Previous robotic technologies often required an investment of USD 1.5 million to USD 2.5 million, thus restricting their use to major hospitals. However, the emergence of affordable solutions has opened up the entire market to ambulatory surgery centers and hospitals in developing nations.

MIS vs. Open Surgery: Clinical Outcomes

Peer-reviewed research increasingly supports the laparoscopic surgery benefits and better results achievable with minimally invasive methods. Here is a summary comparison based on data reported in studies conducted up to 2024-2025:

| Clinical Metric | Minimally Invasive Surgery | Traditional Open Surgery |

| Average Hospital Stay | 1–3 days | 5–7 days |

| Blood Loss (laparoscopic cholecystectomy) | ~50–100 ml | ~200–400 ml |

| Return to Normal Activity | 1–2 weeks | 4–6 weeks |

| Surgical Site Infection Rate | ~1%–2% | ~3%–8% |

| 30-Day Readmission Rate | Lower by ~20%–30% vs. open | Baseline |

| Postoperative Pain Score (VAS) | Significantly reduced | Higher |

| Cosmetic Outcome | Minimal scarring | Visible scar |

| Cost per Episode (US, hospital-based) | Lower by 15%–40% in ASC settings | Higher |

It is important to understand that not all patients and medical cases would benefit from the minimally invasive technique. The patient's complexity, preexisting illnesses, and the need for specific surgery will be important in deciding on the application of MIS. Another very important element in success is the professional competency of the medical staff involved in the procedure. No matter what technology is used in surgery, surgeons' expertise will influence invasive surgery clinical outcomes. Healthcare institutions should also conduct a careful analysis before introducing MIS programs. Issues like financial benefits, technological infrastructure, and medical competency should be taken into account.

Reimbursement and Regulatory Landscape

The reimbursement of minimally invasive surgeries varies from country to country and significantly affects the adoption rate and market size of this surgical technique in particular regions.

| Region/Country | Reimbursement Status | Key Developments (2024–2026) |

| United States | CMS provides coverage for most standard MIS techniques; robotic MIS covered by increasing numbers of CPT codes | New Category III CPT code for robotic lymphovenous bypass effective from January 1, 2026 |

| Germany (GKV) | Most MIS procedures reimbursed through the DRG scheme; increase in robotic surgery covered | EU MDR implementation adding certification difficulty |

| United Kingdom (NHS) | Recommendations from NICE on coverage; robotic surgery authorized for particular indications | NHS Long Term Plan promotes MIS development in community surgical centers |

| Japan | MHLW provides reimbursement for robotic surgery in certain operations; list expanded since 2020 | Government heavily funds surgical robotics research & development |

| India | Private insurance coverage for MIS is increasing; limited coverage by national health plan | Increased medical tourism for MIS; evolving device regulation through CDSCO |

| China | NHSA coverage for laparoscopy and robot-assisted surgery growing | Creating their own robot systems (companies based in Tianjin) |

Most MIS devices in the U.S. obtain approval through the FDA 510(k) clearance pathway, whereas advanced devices must go through more stringent approval processes. Newer FDA guidelines for AI-assisted surgical devices provide greater clarity but require more substantial evidence. The MIS market regulatory landscape in Europe is complex due to the recently implemented EU Medical Device Regulation (MDR). With certification bodies having limited capabilities, new device approval can be slow, thereby making it costlier for smaller device manufacturers.

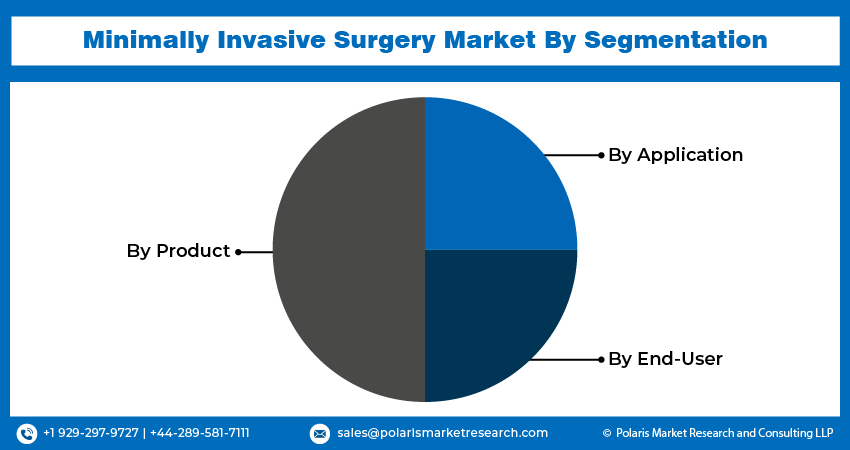

Minimally Invasive Surgery Market Segmentation

By Product Insights

The surgical devices segment led the market with a 48.6% revenue share in 2025. Surgical instruments for MIS are classified into handheld instruments, laparoscopy devices, guidance devices, and inflation systems. Such tools are fundamental components that play a vital role in improving surgery. The invention of medical equipment such as advanced laparoscopic tools has facilitated the development of MIS and improved surgical procedures by adding accuracy and flexibility. Advanced laparoscopic tools can be used to carry out complicated surgical procedures accurately. The high surgical robotics market share can also be attributed to technological innovations that have been brought about by the major players. The innovations often feature healthcare mobile robotics technology, artificial intelligence, and imaging that help surgeons conduct surgery with ease.

It is projected that the fastest-growing sub-segment within the product category will be the medical robotics industry through 2034 due to the widespread adoption of robot-assisted surgery technology. The global market for minimally invasive medical robots alone was valued at approximately USD 58.20 billion in 2025. This highlights the significant investment being made in robotic surgery infrastructure worldwide.

By Application Insights

The neurological surgery segment is expected to account for the fastest growth rate of 8.9% during the forecast period. Growth is due to advancements in imaging and surgical technologies that facilitate more accurate operations. There is an emphasis on minimizing risks, reducing complications, and achieving a fast recovery time, which are among the major benefits of MIS. Moreover, the trend towards patient-centric and value-driven health care encourages the use of neurological minimally invasive surgery market solutions.

Urological surgery is a rapidly developing category, where robotic-assisted surgery for prostate cancer is currently considered the most appropriate solution for patients who have prostate cancer in many advanced healthcare markets. The use of robots in the urological surgery MIS market makes the procedure easier to perform in difficult-to-reach areas and helps achieve better results than traditional surgery.

Gynecological surgery remains the largest segment in terms of revenue, accounting for approximately 33% of the MIS market in 2025. Gynecological surgery minimally invasive market demand is driven by a large number of operations, such as hysterectomies, myomectomies, and endometriosis treatments, conducted worldwide.

By End-User Insights

The hospital, clinics & ablation centers segment led the MIS end-user segmentation category with a 62.4% revenue share in 2025. The factors that have led to this are increased operating room capacity, favorable reimbursement policies, and the availability of high-quality equipment. In addition, hospitals can perform numerous types of operations; hence, they are the preferred place for surgery among people, particularly in developing nations. For instance, according to February 2026 data by the America Hospital Association, there are 6,100 hospitals in the U.S.

Despite the hospital sector's continued dominance as the top revenue generator among end users, ASCs are emerging as the fastest-growing segment in the minimally invasive surgery industry, according to projections through 2034. The volume of procedures in ASCs has been increasing significantly in developed nations such as the United States, Australia, and Germany, driven by cost advantages, favorable reimbursement practices, and a preference for outpatient procedures. This trend is supported by advances in the development of portable robotic devices at lower price points, which can be used in ASCs. The Versius robot by CMR Surgical and Mako Smart Robotics by Stryker are examples of such devices that have contributed to this trend.

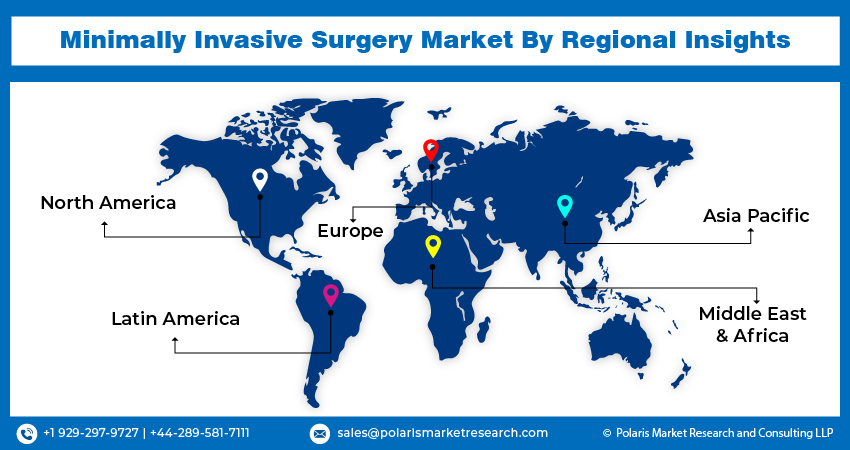

Minimally Invasive Surgery Market Regional Insights

North America

The North America minimally invasive surgery market accounted for the largest market share of 39.2% 2025 and is expected to maintain its dominance over the anticipated period. The surge in demand for minimally invasive surgery (MIS) technology is attributed to the increasing cases of chronic ailments in North America. Another development is occurring in sectors such as neurosurgery, whereby surgical processes that were conducted using open surgical methods have become less invasive through endoscopy. MIS systems' popularity is expected to rise since they require smaller cuts, shorter recovery periods, and reduce the cost of treatments. Moreover, continuous innovation on the part of leading firms in the U.S. is helping fuel the growth of this market. Enhanced healthcare infrastructure, increased adoption of technology, and heightened awareness about alternatives for treatment are some other factors driving market development.

Asia Pacific

The Asia Pacific minimally invasive surgery market is projected to register the highest CAGR of 8.5% during the forecast period. The primary factors driving the growth of the minimally invasive surgery (MIS) industry include the aging population, rising healthcare expenditures, and the increased spending on healthcare facilities. The patients themselves are opting for the MIS approach due to the associated shorter stay in hospitals, reduced postoperative pain, and quicker recovery process than with conventional surgery methods. Continuous developments in surgical procedures and technology continue to foster adoption. In the Asia Pacific region, the market will be fueled by an increasing number of regional companies offering minimally invasive surgery (MIS) systems.

The largest growth potential in the Asia-Pacific region lies in the China MIS market, where increased reimbursement by the National Healthcare Security Administration (NHSA) for laparoscopy and robotic surgery procedures is playing an important role. Additionally, local companies are becoming increasingly competitive due to their lower-priced offerings compared to expensive systems such as the da Vinci Surgical System from Intuitive Surgical.

The India minimally invasive surgery market presents itself as a dual opportunity as well. The country experiences growth in its local MIS market through private hospitals and medical tourism. At the same time, India emerges as an important manufacturing base for surgical robots. In January 2025, the SSI Mantra system demonstrated its potential for conducting telesurgeries over long distances. Apart from that, in October 2024, Intuitive Surgical partnered with KIMS Hospitals to introduce 25 robotic surgery programs across Maharashtra, Karnataka, Andhra Pradesh, and Telangana. The initiative targeted tier-2 and tier-3 city access.

The Europe minimally invasive surgery market is witnessing steady growth. It is driven by aging populations, higher surgical rates, and robust government healthcare spending. The introduction of the new regulation called the EU Medical Devices Regulation (MDR) may present some challenges for manufacturers in the short term. However, it will result in better product quality and safety. Germany, France, and the UK are the countries contributing substantially to the market. These countries together contribute to 60% of the market revenue.

The Middle East & Africa and Latin America are now becoming regions with high potential. The expansion moves, such as CMR Surgical's Versius rollout in 2025, demonstrate that there is significant opportunity to tap into. In addition, other initiatives in the healthcare sector, such as Vision 2030 in Saudi Arabia, create favorable conditions for MIS development.

MIS Competitive Landscape

The minimally invasive surgery market is fragmented and extremely competitive. In addition, all the major companies have been investing heavily in research and development in order to establish a foothold in the market. There have been a number of strategies employed by companies in this market in order to gain more share. These include partnerships, product enhancements, and collaborations, amongst others.

The robotic surgery competitive landscape is characterized by a two-tier structure. Established global firms lead the minimally invasive surgery market share, especially with their robotics and imaging technologies. Other regional and specialty players have started gaining prominence, offering affordable solutions driven by artificial intelligence. Intuitive Surgical remains the leader in the installed base due to its da Vinci Surgical System. However, other players, such as Medtronic, Johnson & Johnson MedTech, and CMR Surgical, present competition to Intuitive Surgical market share with their Hugo RAS, OTTAVA system, MONARCH Platform for Urology, and Versius system, respectively.

One of the competitive areas for 2025-2026 is the production of smaller, cheaper robots specifically intended for use in ambulatory surgical centers. Given that the costs of such robots have dropped to under USD 500,000, they can help bring minimally invasive procedures to more patients.

Johnson & Johnson MedTech is one of the key participants in the minimally invasive surgery industry, providing an extensive line of surgical tools, robotics, and other digital technology solutions. The company strives to innovate and collaborate to improve surgical accuracy and improve patient outcomes.

Medtronic plc is another leading provider of minimally invasive surgical equipment that covers several fields of medicine. The company pays close attention to the development of highly advanced systems and to expanding its presence worldwide, thereby promoting the use of minimally invasive surgical procedures.

List of Key Companies

- Abbott Laboratories

- Arthrex

- Asenus Surgical

- Becton, Dickinson & Company

- Boston Scientific Corporation

- Eximis Surgical

- Ge Healthcare

- Johnson & Johnson Medtech

- Medtronic Plc

- Nuvasive

- Orthofix Holdings,Inc

- Smith & Nephew

- Stryker Corporation

- Virtual Ports

- Zimmer Biomet Holdings

Industry Developments

- July 2025: Intuitive received FDA clearance for its advanced bipolar electrosurgical instrument, Vessel Sealer Curved. The electrosurgical instrument is fully wristed and compatible with da Vinci multiport systems. It is capable of sealing, cutting, grasping, dissecting tissue, and transecting lymphatic vessels.

- May 2025: Intuitive Surgical revealed a next-generation enhancement to its da Vinci robotic platform featuring improved tactile feedback and AI-driven navigation for complex thoracic and urologic surgeries.

- March 2025: CMR Surgical broadened the worldwide deployment of its Versius robotic system across Latin America and Southeast Asia to address rising demand for compact, affordable MIS solutions in hospitals.

- January 2025: Boston Scientific Corporation signed a definitive agreement to acquire Bolt Medical, Inc. The company revealed the acquisition will involve adding laser IVL technology to its MIS cardiovascular portfolio.

Report Coverage

The Minimally Invasive Surgery market report emphasizes key regions across the globe to provide a better understanding of the product to users. Also, the report provides market insights into recent developments and trends, and analyzes the technologies gaining traction worldwide. Furthermore, the report provides in-depth qualitative analysis of the various paradigm shifts associated with the transformation of these solutions. The report provides a detailed analysis of the market, focusing on key aspects such as competitive analysis, product, application, end-user, and their future growth opportunities.

The 2025 edition of this report features improved coverage of critical themes that are impacting the minimally invasive surgery market. These themes include the emergence of AI and robotics in the clinical environment, country-specific reimbursement analyses of the top minimally invasive surgery markets, and new data on the clinical outcomes of minimally invasive surgery compared to conventional open surgeries. Moreover, the new edition also provides improved competitive intelligence information relating to new platforms, regulatory trends, and partnerships made during 2025-2026.

Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Electrosurgical Devices

- Electrocautery Devices

- Electrosurgical generators & accessories

- Imaging & Visualization Systems

- X-Ray imaging

- Ultrasound

- CT imaging

- MRI imaging

- Visualization Systems

- Surgical Devices

- Laparoscopy Devices

- Trocar and Cannula

- RASP (Robotic- Assisted Simple Prostatectomy)

- Laparoscope

- Graspers and Dissectors

- Handheld Instruments

- Probes

- Laser fiber devices

- Tubular Retractor

- Dilator

- Suturing Instruments

- Inflation Systems

- Balloon Inflation Systems

- Balloon Catheters

- Guiding Devices

- Guiding Catheters

- Guidewires

- Laparoscopy Devices

- Medical Robotics

- Robotic softwares & Services

- Robotic Systems

- Robotic Instruments

- Endoscopy Devices

- Diagnostic endoscopes

- Flexible endoscopes

- Rigid endoscopes

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Neurological Surgery

- Cardio-Thoracic Surgery

- Dental Surgery

- Vascular Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Oncology Surgery

- ENT & Respiratory Surgery

- Cosmetic Surgery

- Gastrointestinal & Abdominal Surgery

- Others

By End-User Outlook (Revenue, USD Billion, 2021–2034)

- Ambulatory Surgical Centers

- Orthopedic, Emergency & Trauma Centers

- Hospitals, Clinics & Ablation centers

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Minimally Invasive Surgery Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 522.51 billion |

| Market Size in 2026 | USD 562.63 billion |

| Revenue Forecast by 2034 | USD 1,029.64 billion |

| CAGR | 7.8% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Minimally Invasive Surgery Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market was valued at USD 522.51 billion in 2025. It is projected to reach USD 1,029.64 billion by 2034.

The market is projected to account for a CAGR of 7.8% during 2026 to 2034.

North America led the market in 2025. This is due to its healthcare infrastructure and favorable reimbursement policies.

Key players include Intuitive Surgical (da Vinci platform), Medtronic plc (Hugo RAS), Johnson & Johnson MedTech (OTTAVA, MONARCH), Stryker Corporation, Boston Scientific, CMR Surgical (Versius), Smith & Nephew, Zimmer Biomet, Becton Dickinson, and Abbott Laboratories, among others.

The market is primarily driven by rising prevalence of chronic diseases requiring surgical intervention and growing global aging population.

Key challenges include high upfront capital costs for robotic systems and annual maintenance costs.

Artificial intelligence is being used for preoperative planning and intraoperative guidance. The technology also assists with outcome prediction.

Download Sample Report of Minimally Invasive Surgery Market

Please fill out the form to request a customized copy of the research report.