Personal Health Record Software Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

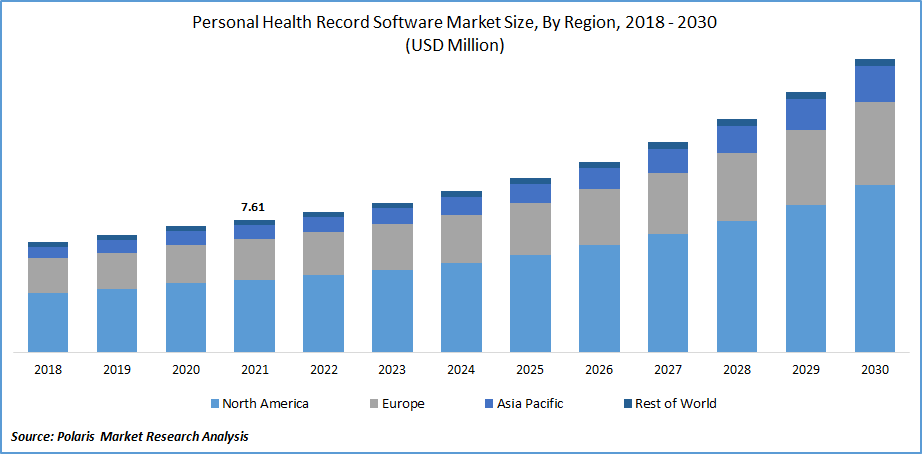

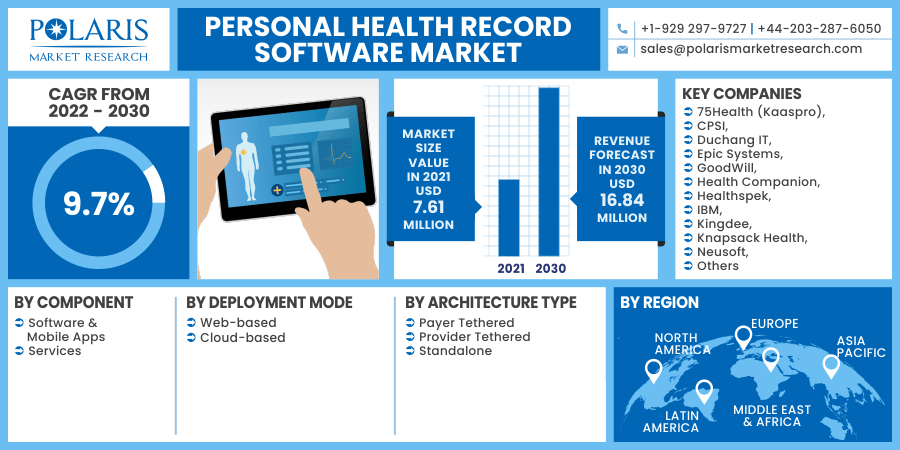

The global personal health record software market was valued at USD 7.61 million in 2021 and is expected to grow at a CAGR of 9.7% during the forecast period. The demand for the product is rising due to the growing demand for cloud-based software for dealing with individual data is accelerating the market demand globally.

Know more about this report: Download Sample Report

Know more about this report: Download Sample Report

Moreover, rising acceptance for the evolving technologies, along with the growing responsiveness for the medical information storage and management solutions, also contribute to the personal health record software market demand.

The widespread COVID-19 brings a positive impact on the global industry. The pandemic imposed medical sector to allocate personal medical data in a set-up that is easily accessible and secured for the consumers. These electronic medical records present various efficient tools for data and medical management.

Thereby, the growing acceptance of emerging technologies for catering to increasing customer demand contributes to the industry growth. Besides, personal medical record software also provides government and medical organizations for collecting and analyzing the personal data of COVID-19 patients. Thus, the rising initiatives for the penetration of digital platforms for pandemic management may increase the market demand for personal medical record software globally. Hence, these factors create lucrative growth in the global personal health record software market in the near future, owing to the continued adoption of digital platforms in the medical industry.

Know more about this report: Download Sample Report

Industry Dynamics

Growth Drivers

The growing awareness about medical information storage and management among urban patients is primarily attributed to the personal fitness record software industry growth. In some past years, various patient information was managed by the medical professionals, and, generally, the personal information was stored in storage rooms, which eradicate medical practitioners from allocating medical data.

Thereby, medical groups are forced to share patient medical records in an efficient setup in the modern era. Furthermore, product launches and various business strategies by the major industry competitors are accelerating the personal health record software market demand across the globe.

For instance, in Feb 2019, Fujitsu declared the launch of its new Fujitsu Healthcare Solution Healthcare Personal Service Platform. This platform can collect and integrate a patient's personal medical data record. Likewise, in March 2020, Knapsack Health introduced the company's new free PHR (Personal Health Record) software for individuals, families, and caretakers. Hence, these various growth factors may gain significant prominence in the personal health record software market that fosters the industry demand.

Report Segmentation

The market is primarily segmented on the basis of component, deployment mode, architectural type, and region.

| By Component | By Deployment Mode | By Architecture Type | By Region |

|

|

|

|

Know more about this report: Download Sample Report

Insight by Deployment Mode

The web-based deployment mode segment is the leading segment in terms of revenue generation in the year 2020. The increasing penetration of online apps and evolving digitization are the major driving factor for the segment growth. Development in innovative and up-to-date technologies facilitates consumers to apps with the help of Uniform Resource Locators (URLs). Moreover, a simple exchange of crucial information between multiple clinicians and patients is connected with web-based PHR software, further contributing to the segment demand.

The cloud-based deployment mode segment will likely exhibit the fastest CAGR in the forecasting period. Growing demand for cost-effective IT infrastructure among enterprises and access to various devices from anywhere may fuel the segment growth. The growing responsiveness for e-health by population and rising concern regarding the privacy and security of data is also acting as a catalyzing factor for the industry growth. Cloud server suppliers generally provide a third-party module thereby; medical data can be robustly stored while maintaining the privacy of consumer personal and medical information.

Insight by Architecture Type

The standalone segment is accounted with the largest revenue share in the global industry and is expected to rise fastest over the foreseen years. The standalone system is entirely patient-controlled, and professionals can only inspect information only when their patients give them access. The major advantage of using a standalone PHR is its perceived privacy management and conviction, contributing to segment growth. In addition, patient data management is the exclusive factor that is linked with standalone PHRs, which, in turn, further accelerates the segment demand.

The provider-tethered segment is likely to grow at the highest growth rate in the global industry. Provider-tethered PHRs are associated with the medical plan information system or medical organization's electronic health record (EHR) system. The emergence of technologically developed medical services along with rising government schemes for promoting the adoption of medical IT is fueling the segment growth.

Geographic Overview

Geographically, North America is the largest revenue contributor in 2021 and is expected to dominate the global industry over the forecast period. The growing requirements for following regulatory guidelines & limiting the rising medical costs, as well as increasing government initiatives for eHealth, are attributed to the industry demand.

In addition, the increasing inclination towards developing a sound sustainable medical system by non-government organizations also leads to industry growth across the regional market. Furthermore, growing investment in medical R&D activities and increasing population also boost the segment demand. Therefore, these factors accelerate the demand for personal medical record software across North America.

Moreover, the rest of the world is projected to grow at the highest CAGR across the globe in the upcoming years. The increasing demand for remote patient monitoring solutions, along with the growing number of the aging population, is fueling the market's demand. Also, rising collaborations and initiatives by leading market players for rapid technological advancements across the medical sector lead to market development. Moreover, growing incidences of long-term chronic conditions as well as minimum medical data management cost also boost the market growth in the regional market over the upcoming years.

Competitive Insights

Some of the major players operating in the global market include 75Health (Kaaspro), CPSI, Duchang IT, Epic Systems, GoodWill, Health Companion, Healthspek, IBM, Kingdee, Knapsack Health, Neusoft, NoMoreClipboard, PA SUN, Patient Ally, PCCW Solution, PKU Healthcare IT CO., Ltd, Practice Fusion, Inc., Records For Living, Inc., SoftClinic Software, Validic, Wining, and Zapbuild.

Personal Health Record Software Market Report Scope

| Report Attributes | Details |

| Market size value in 2021 | USD 7.61 million |

| Revenue forecast in 2030 | USD 16.84 million |

| CAGR | 9.7% from 2022 - 2030 |

| Base year | 2021 |

| Historical data | 2018 - 2020 |

| Forecast period | 2022 - 2030 |

| Quantitative units | Revenue in USD million/billion and CAGR from 2022 to 2030 |

| Segments covered | By Component, By Deployment Mode, By Architectural Type, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Companies | 75Health (Kaaspro), CPSI, Duchang IT, Epic Systems, GoodWill, Health Companion, Healthspek, IBM, Kingdee, Knapsack Health, Neusoft, NoMoreClipboard, PA SUN, Patient Ally, PCCW Solution, PKU Healthcare IT CO., Ltd, Practice Fusion, Inc., Records For Living, Inc., SoftClinic Software, Validic, Wining, and Zapbuild. |

Download Sample Report of Personal Health Record Software Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

Please fill out the form to request a customized copy of the research report.