Prostate Health Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

REPORT DETAILS

REPORT DETAILS

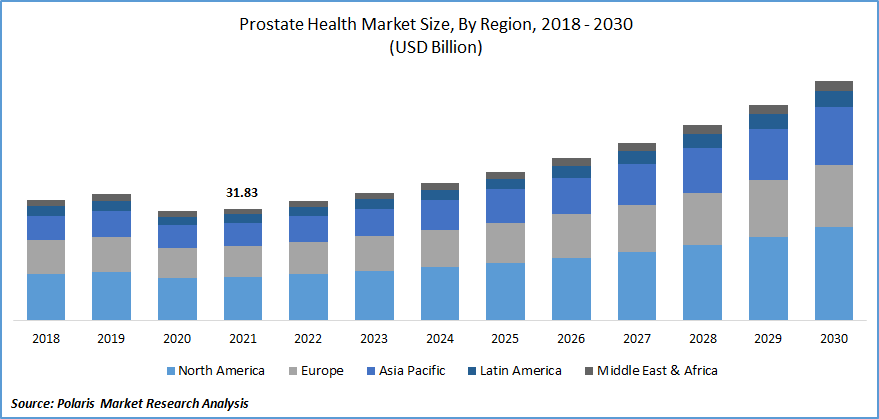

The global prostate health market was valued at USD 31.83 billion in 2021 and is expected to grow at a CAGR of 9.1% during the forecast period. Increasing innovations and FDA approvals by major players, emerging pipeline drugs, collaboration for commercializing drugs, and emerging therapies for cancer are boosting the prostate health market growth during the forecast period.

Know more about this report: Download Sample Report

Know more about this report: Download Sample Report

The various major players such as HALO diagnostics, Avenda Health, Novartis AG, and SonaCare Medical, among others, focus on treating cancer with innovation. The various players are developing treatment devices with technologically advanced features. The FDA approvals by the government are to create opportunities for the prostate health market growth over the forecast period.

For instance, in August 2021, HALO Diagnostics has expanded the availability of a radiation-free, minimally invasive, and image-guided treatment that targets and destroys cancer cells. TULSA-PRO is a technique performed in the magnetic resonance imaging (MRI) suite by Profound Medical Corp (Profound). It uses a combination of real-time MRI and robotically controlled transurethral ultrasound technology to locate and eradicate cancer cells using ablation. HALO Dx expands the number of personalized services it can provide to patients with cancer by introducing TULSA-PRO.

Further, in January 2021, Myovant partnered with Pfizer to introduce its drug Orgovyx (relugolix). In June 2021, Novartis announced that the FDA had approved 177Lu-PSMA-617, experimental device therapy to treat metastatic castration-resistant prostate cancer (mCRPC). Breakthrough Therapy is given to drugs studied for critical illnesses and shows early clinical evidence of significant improvement over current therapy. Thus, the FDA approvals for the treatment of cancer are boosting the prostate health market growth.

However, the side effects of the medicines and therapies for BPH and prostate health are restraining the prostate health market growth during the forecast period. While both medicines and surgery can treat BPH, both have severe adverse effects. Alpha-blockers, 5-ARIs, and other medication groups are routinely used to treat BPH. Dizziness, postural hypotension, and allergies are all common side effects of alpha-blockers. Dizziness and postural hypotension are especially concerning in the elderly since they might result in serious illnesses such as accidents and consequent injuries.

Know more about this report: Download Sample Report

Know more about this report: Download Sample Report

Industry Dynamics

Growth Drivers

The rising prevalence of benign prostatic hyperplasia, rising overweight, rise in prevalence of cancer, an increased number of prostatitis are all driving industry growth. Obesity and BPH are strongly intertwined. As per the WHO, In 2020, 39 million children under the age of five were overweight and obese. In 2016, nearly 340 million children and youth aged 5 to 19 were overweight or obese. Obesity causes various factors, including increased sympathetic nerve activity, abdominal pressure, an inflammatory reaction, and oxidative stress, all of which enhance BPH development. In the Asia Pacific, Australia has the highest prevalence of cancer. This is augmenting the market for prostate health market growth.

Furthermore, the most frequent type of cancer among males is cancer. According to the American Cancer Society's estimations for prostate cancer in 2021, around 248,530 new cases and 34,130 deaths originated in the United States in 2020 due to cancer. It is a relatively rare disease in developing countries, but its incidence and death have increased, offering market prospects. One of the variables that can be attributed to the rising instances in Asia-Pacific is the effect of western culture and lifestyle.

Report Segmentation

The market is primarily segmented based on disease indication, modality, treatment, and region.

| By Disease Indication | By Modality | By Treatment | By Region |

|

|

|

|

Know more about this report: Download Sample Report

Insight by Disease Indication

Prostate cancer segment is anticipated to garner the largest revenue share in the global market. Hormone therapy is generally an effective first-line treatment approach for cancer. Cancer vaccines, radiopharmaceutical agents, subsequent hormone therapies, or chemotherapies are alternatives for treatment after hormonal treatments. Cancerous cells acquire resistance to these medicines within a few months. Therefore immunotherapies are predicted to be widely used for cancer therapy over the forecast period.

Geographic Overview

In terms of geography, North America had the highest share in 2021. The high prevalence of BPH, coupled with treatment innovations, is expected to drive the region forward. Furthermore, advantageous reimbursement rules, a solid healthcare infrastructure, research funding, and product introductions have propelled this market's expansion.

Moreover, Asia Pacific witnessed a high CAGR in the global market in 2021. Emerging economies (such as China, India, Brazil, and Mexico) will likely offer major growth prospects to market participants in the following years. Factors such as the presence of a strong target patient group, rising healthcare spending, increased physician awareness, and substantial increases in the geriatric population are projected to drive demand for prostate health solutions in these nations.

For instance, According to the World Bank, in 2018, around 6.67% of the GD was healthcare expenditure in East Asia & Pacific region. In Japan, healthcare expenditure was 10.95%, China 5.35%, Australia 9.28%, South Korea 7.56%, Maldives 9.41%, and Myanmar 4.8% of the GDP. The Asia Pacific region has a rapidly rising population with benign prostatic hyperplasia.

Competitive Insight

Some of the major players operating in the global market include Abbott Laboratories, Amgen Inc., Astellas Pharma Inc., AstraZeneca PLC, Bayer AG, Bristol-Myers Squibb Co., Eli Lilly and Company, Endo Pharmaceuticals Inc., Ferring Pharmaceuticals Inc., GlaxoSmithKline PLC, Johnson & Johnson, Merck & Co., Inc., Pfizer Inc., and Siemens Healthcare AG.

Prostate Health Market Report Scope

| Report Attributes | Details |

| Market size value in 2021 | USD 31.83 billion |

| Revenue forecast in 2030 | USD 68.0 billion |

| CAGR | 9.1% from 2022 - 2030 |

| Base year | 2021 |

| Historical data | 2018 - 2020 |

| Forecast period | 2022 - 2030 |

| Quantitative units | Revenue in USD million and CAGR from 2022 to 2030 |

| Segments covered | By Disease Indication, By Modality, By Treatment, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Companies | Abbott Laboratories, Amgen Inc., Astellas Pharma Inc., AstraZeneca PLC, Bayer AG, Bristol-Myers Squibb Co., Eli Lilly and Company, Endo Pharmaceuticals Inc., Ferring Pharmaceuticals Inc., GlaxoSmithKline PLC, Johnson & Johnson, Merck & Co., Inc., Pfizer Inc., and Siemens Healthcare AG. |

Download Sample Report of Prostate Health Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

Please fill out the form to request a customized copy of the research report.