Radiotheranostics Market Demand, Industry Trends, 2026-2034

REPORT DETAILS

Radiotheranostics Market Summary

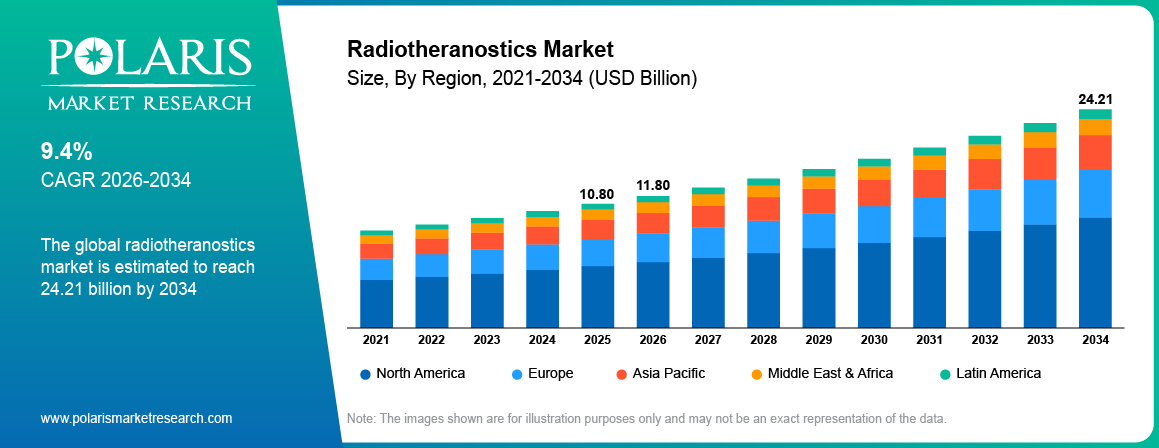

The global radiotheranostics market was valued at USD 10.80 billion in 2025 and is projected to reach USD 24.21 billion by 2034, registering a CAGR of 9.4% during the forecast period. Market growth is attributed to FDA approvals for radioligand therapy, increasing use of Lutetium-177 drugs for treating prostate cancer and neuroendocrine cancers, and investments into the production of radiopharmaceuticals.

Market Statistics

Radiotheranostics Market Key Takeaways 2025

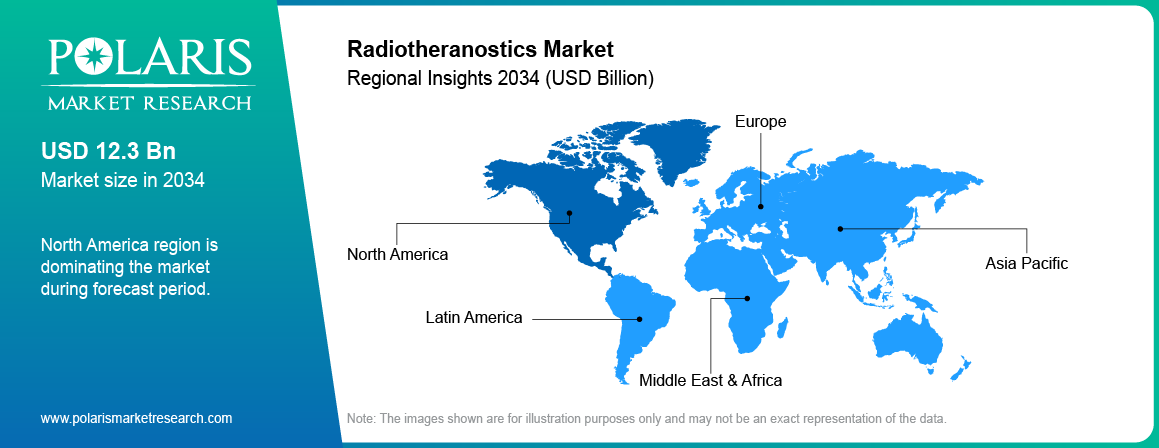

- In 2025, North America held the largest radiotheranostics market share of 37.70%, driven by approved radioligand therapies, robust nuclear medicine infrastructure, and substantial investments in oncology.

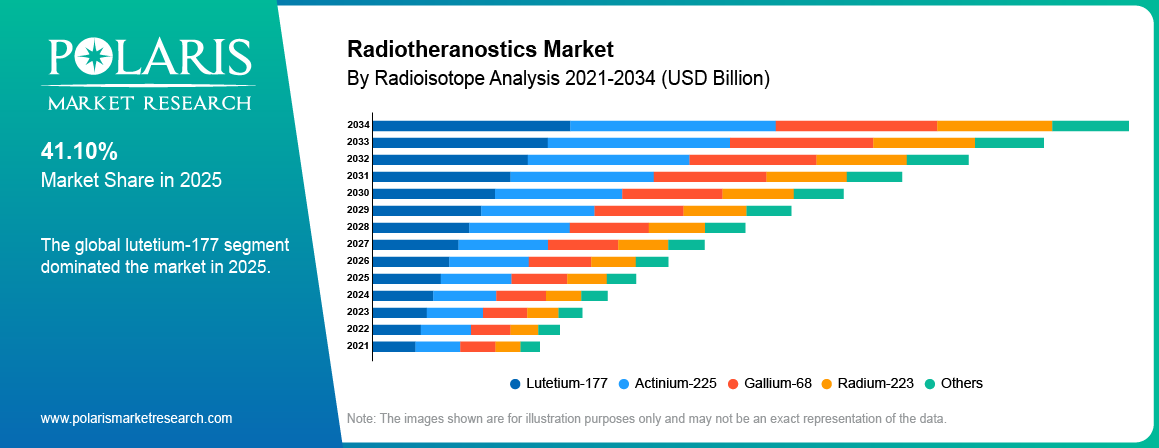

- Lutetium-177 held the dominating radioisotope share at 41.10% in 2025, owing to its widespread use in approved radioligand therapies.

- Prostate cancer was the leading application segment in 2025 with a market share of 37.10%, due to increasing adoption of PSMA targeting therapies.

- The hospitals emerged as the largest end-user segment with a share of 34.10% in 2025, owing to their capabilities in nuclear medicine and radioligand therapy.

- The targeted alpha therapy based on actinium-225 is expected to show the highest growth rate in the coming years, due to its rising clinical development pipeline.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observation

What is Radiotheranostics?

Radiotheranostics refers to precision oncology technology that employs diagnostic imaging and radiotherapy based on the same or highly similar molecular targets. First, doctors perform diagnostic imaging in order to detect tumors with the presence of a certain biomarker. Afterwards, this molecular target is used to deliver a radioisotope to the tumor.

This is an integrated method of selecting patients, treatment planning, dosimetry, and treatment monitoring in a single treatment process. Unlike the traditional techniques such as radiation and chemotherapy, radiotheranostics directly deliver radiation to cancer cells without affecting the healthy cells. The increasing demand for targeted cancer treatment methods and approval of radioligands are among the factors contributing to the growth of the market.

Source: Polaris Market Research Analysis

Radiotheranostics Market Driver Impact Analysis

The radiotheranostics market is projected to grow at a CAGR of 9.4% through 2034, supported by rising approvals for radioligand therapies, expanding radiopharmaceutical production, and increasing adoption of theranostic approaches for prostate cancer, neuroendocrine tumors, and other solid tumors. The table below outlines the key growth drivers and their estimated contribution across major geographies.

| Market Driver | Est. CAGR Impact | Geographic Relevance | Impact Timeline |

| FDA and EMA approvals expanding radioligand therapy indications | +2.8% | North America, Europe | Short to medium term |

| Scaling of Lutetium-177 and Actinium-225 production capacity | +2.3% | Global | Medium term (2–4 years) |

| Growing clinical adoption of PSMA-targeted theranostic pairs | +2.0% | North America, Europe, Asia Pacific | Short to medium term |

| Expansion of targeted alpha therapy clinical pipelines | +1.7% | US, Europe | Medium to long term |

| Government investment in nuclear medicine infrastructure | +1.4% | Global | Long term |

| Increasing integration of dosimetry and AI-guided treatment planning | +0.9% | North America, Europe, Japan | Medium term |

* Indicative estimates based on market context and analyst judgment. Figures reflect relative driver weight, not additive CAGR contributions. Source: Polaris Market Research Analysis.

Radiotheranostics Market Industry Dynamics

- Expanding commercial availability of approved radioligand therapies is driving rapid growth in hospital nuclear medicine department infrastructure and specialist oncology referral networks.

- Growing radioisotope production investment from both government-supported and commercial suppliers is addressing supply chain constraints that previously limited market scaling.

- Isotope supply chain reliability and the short physical half-lives of therapeutic radioisotopes create logistical complexity that continues to challenge broad geographic market penetration.

- Pharma and specialty radiopharmacy partnerships are accelerating the commercialization of next-generation radioligand therapies targeting novel tumor antigens across breast, lung, and kidney cancers.

Radiotheranostics Market Drivers, Restraints and Opportunities

How Is the Commercial Success of Approved Radioligand Therapies Driving Growth in the Radiotheranostics Market?

The commercial success of Pluvicto for metastatic castration-resistant prostate cancer and Lutathera for neuroendocrine tumors has strengthened the adoption of radiotheranostics in oncology. In May 2026, Novartis received MHRA authorization in the UK for an expanded indication of Pluvicto (lutetium [¹⁷⁷Lu] vipivotide tetraxetan) for eligible patients with PSMA-positive metastatic castration-resistant prostate cancer (mCRPC). These approvals have demonstrated the therapeutic potential of radioligand therapy and boosting pharmaceutical industry players to invest more into the development of the next generation treatment strategies against various types of cancer.

How Is the Expansion of Radioisotope Production Reshaping the Radiotheranostics Market?

The increasing production of Lutetium-177 and Actinium-225 isotopes is critical to ensure the rising need for radiotheranostic treatment strategies. Government organizations and private enterprises have been increasing their investments into the construction of isotope production facilities to increase the availability and become less dependent on a limited number of facilities. For example, in June 2026, Telix Pharmaceuticals concluded an agreement for the long-term supply of Actinium-225 from the Australian Nuclear Science and Technology Organisation (ANSTO)(Source: www.iaea.org).The agreement strengthens isotope availability for the company's targeted alpha therapy pipeline.

What Challenges Threaten Radiotheranostics Market Expansion? Supply Chain Complexity and Logistics

The short decay of radioisotopes makes their production, distribution, and delivery quite challenging. The special nature of handling along with nuclear medicine departments adds another layer of difficulty to the process. The lack of facilities that handle the radiopharmaceuticals close to the treatment centers is another limitation that prevents more widespread use of this modality. Regulations on production, quality control, and distribution add additional cost to the process.

What Opportunities Exist in the Radiotheranostics Market? Targeted Alpha Therapy and Next-Generation Indications

Targeted alpha therapy based on Actinium-225 represents a major growth opportunity for the radiotheranostics market. Alpha emitting radioisotopes provide high-intensity radioactivity exposure to cancer cells with minimal harm to the surrounding normal tissue. In May 2026, The Oak Ridge National Laboratory (ORNL) started a novel project aimed at enhancing the production and study of alpha emitting radioisotopes for TAT(Source: www.ornl.gov).This project solidifies the provision of medical isotopes and development of advanced radiopharmaceuticals. Several clinical programs are evaluating Actinium-225 therapies for prostate cancer, blood cancers, and other solid tumors.

Source: Polaris Market Research Analysis

Segment and Regional Leaders at a Glance

According to Polaris Market Research, North America leads the market while Asia Pacific the fastest-growing region.

- Dominant Region: North America

- Fastest-Growing Region: Asia Pacific

- Largest Radioisotope Segment: Lutetium-177

- Largest Application Segment: Prostate Cancer

- Largest End User Segment: Hospitals

Radiotheranostics Market Segmentation Analysis

The report provides a comprehensive analysis of the radiotheranostics market by radioisotope, application, and end user to identify key revenue-generating and high-growth segments.

Radiotheranostics Market by Radioisotope

What is the Largest Radioisotope Segment in the Radiotheranostics Market?

Lutetium-177 dominated the radiotheranostics market by radioisotope in 2025, accounting for 41.10% of radioisotope segment revenue. Its dominant position reflects the commercial success of Lutathera and Pluvicto, both of which use Lutetium-177 as the therapeutic radioisotope, establishing a large installed patient base and a well-developed radiopharmacy dispensing infrastructure.

Which Radioisotope Segment is Growing Fastest in the Radiotheranostics Market?

Actinium-225 is projected to grow at the fastest CAGR during the forecast period, driven by its emerging clinical profile as a targeted alpha emitter with high tumor cell-killing potency. A growing number of clinical trials are investigating Actinium-225-labeled PSMA-targeting agents in prostate cancer and other solid tumor indications, with several programs approaching pivotal study readiness.

Radiotheranostics Market by Application

Which Application Segment Leads the Radiotheranostics Market?

Prostate cancer dominated the radiotheranostics market by application in 2025, representing 37.10% of application segment revenue. The commercial approval and growing adoption of PSMA-targeted radioligand therapy for metastatic castration-resistant prostate cancer has established prostate cancer as the largest therapeutic application of radiotheranostics.

Which Application Segment is Growing Fastest in the Radiotheranostics Market?

The neuroendocrine tumors segment is projected to grow at the fastest CAGR during the forecast period, supported by increasing awareness of somatostatin receptor-targeted theranostics, expansion of PRRT treatment center accreditation, and a growing clinical evidence base supporting earlier use of Lutathera in well-differentiated neuroendocrine tumors.

Radiotheranostics Market by End User

Which End User Leads the Radiotheranostics Market?

Hospitals dominated the radiotheranostics market by end user in 2025, accounting for 34.10% of end-user segment revenue. Hospitals represent the primary administration setting for approved radioligand therapies, given their ability to house certified nuclear medicine departments, maintain radiation safety compliance programs, and manage the specialist oncology and nephrology monitoring requirements associated with radioligand therapy administration.

Which End User Segment is Growing Fastest in the Radiotheranostics Market?

Cancer centers are projected to grow at the fastest CAGR during the forecast period, as dedicated oncology facilities invest in nuclear medicine infrastructure to meet growing patient demand for radioligand therapies. The move to administer radioligand therapy in specialized cancer facilities is made possible by the provision of radiopharmacy distribution services, radiation safety procedures, and presence of oncology experts needed to manage patients effectively.

Segment Summary Table

| Segment | Category | 2025 Status | Forecast CAGR | Key Driver |

| Lutetium-177 | Radioisotope | Largest share, 41.10% | High | Commercial approval of Pluvicto and Lutathera |

| Actinium-225 | Radioisotope | Fastest growing | High | Targeted alpha therapy pipeline expansion |

| Prostate Cancer | Application | Largest share, 37.10% | High | PSMA-targeted radioligand therapy adoption |

| Neuroendocrine Tumors | Application | Fastest growing | High | PRRT expansion and diagnostic imaging uptake |

| Hospitals | End User | Largest share, 34.10% | High | Nuclear medicine department infrastructure |

| Cancer Centers | End User | Fastest growing | High | Dedicated oncology radioligand therapy programs |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Radiotheranostics Market Regional Analysis

North America Radiotheranostics Market Size and Share

North America dominated the radiotheranostics market in 2025 with a 37.70% revenue share, supported by FDA approvals for Pluvicto and Lutathera, a well-developed nuclear medicine department network, and high oncology care expenditure. The approval by The U.S. FDA of Pluvicto (lutetium Lu 177 vipivotide tetraxetan) in March 2025 was for the treatment of metastatic castration-resistant prostate cancer (mCRPC) that is positive for prostrate-specific membrane antigen (PSMA)(Source: www.fda.gov). This approval enables the drug to be administered at an earlier stage of treatment.

US Radiotheranostics Market

The US has the largest market share in the radiotheranostics market within North America, due to the commercialization of Pluvicto and Lutathera after the FDA approval. Increasing investments in radiopharmacy facilities domestically is further fueling market growth. In April 2025, Novartis invested around USD 23 billion into its expansion of manufacturing and radiopharmacy facilities in the US to increase production and distribution of radiopharmaceuticals driven by increasing demand for precision oncology therapies.

Canada Radiotheranostics Market

Canada represents a developing market for radiotheranostics with approvals of radioligand therapy from Health Canada and with a national framework for nuclear medicine that helps in the production of radioisotopes and developing clinical programs. The skills for the production of isotopes, gained with the help of AECL and TRIUMF, making Canada a strategically important supplier of radioisotopes in North America.

Europe Radiotheranostics Market Analysis

Europe has a prominent position in the radiotheranostics market globally due to the EMA approval of Lutathera and Pluvicto and established reputation of nuclear medicine studies. In April 2025, Gustave Roussy received permission to carry out phase I clinical studies of nuclear medicine, adding new opportunities for the assessment of radiopharmaceutical treatment at the early stage. This event facilitates nuclear medicine studies in Europe and helps create novel targeted cancer medicines.

Germany Radiotheranostics Market

Germany is one of the leaders in the European radiotheranostics market owing to the well-developed nuclear medicine infrastructure and established PET and SPECT imaging systems. Moreover, Germany has major players in the pharmaceutical industry such as Bayer AG that commercializes the radiopharmaceutical drug Xofigo for bone metastasis therapy. Furthermore, reimbursement of radioligand therapies in Germany’s compulsory health insurance system further boosts the market growth in the country.

UK Radiotheranostics Market

The UK market expansion is driven by the incorporation of approved radioligand therapies in the NHS, increasing investments in research, and rising treatment capacity for radioligand therapies within NHS Trusts. Pluvicto and Lutathera have experienced better access in NHS patients owing to MHRA approvals and NHS commissioning. In support of this trend, NIHR has invested around USD 7.3 million in May 2026 in the field of digital health research in the UK, boosting innovation and adoption of advanced healthcare technologies across the country(Source: www.nationalhealthexecutive.com)

Asia Pacific Radiotheranostics Market Growth Rate and Forecast

Asia Pacific is projected to experience highest CAGR during the forecast period, fueled by increasing approvals for radioligand therapies in Japan, Australia, South Korea, and China, coupled with rising investments in nuclear medicine infrastructure. Australia, Japan, and South Korea are the most developed markets in Asia Pacific in terms of adoption of radioligand therapies, whereas China is considered to have the most potential market due to its large oncology patient base and rising investment in domestic radiopharmaceuticals.

Japan Radiotheranostics Market

There is growth potential in the radiotheranostics market in Japan due to its state-of-the-art nuclear medicine industry, regulatory changes made by the Pharmaceuticals and Medical Devices Agency (PMDA), and growing partnerships between universities and pharmaceutical companies. For example, in February 2026, Alpha Tau Medical received Japanese marketing approval for Alpha DaRT to treat unresectable locally advanced or locally recurrent head and neck cancer. The approval expands regulatory access to radioligand therapy in Japan.

Australia Radiotheranostics Market

Australia is one of the leading radiotheranostics markets in Asia Pacific. Growth has been facilitated due to the existence of TGA approval, vibrant nuclear medicine research ecosystem, and ANSTO’s ability to produce radioisotopes in Australia. In February 2025, IGNITE Synergy Grant was rolled out in Australia, which provided USD 3.2 million to foster the development of new generation nuclear medicine for prostate cancer(Source: www.anzsnm.org.au).The country is also strengthening its role as a regional hub for radiopharmaceutical development and isotope supply.

Latin America Radiotheranostics Market

The Latin America radiotheranostics market is expected to grow at a moderate pace during the forecast period. Brazil and Mexico remain the key markets, supported by rising oncology investments, increasing radiopharmaceutical approvals, and expanding nuclear medicine infrastructure. For example, in February 2026, Brazil and India signed a partnership agreement to facilitate the development of locally-made oncology biosimilars like nivolumab and pertuzumab through technology transfer and manufacture(Source: www.pearceip.law).The partnership entails an investment of up to USD 140 million during the first year in order to boost the manufacturing capability of oncology products in Brazil.

Middle East & Africa Radiotheranostics Market

Middle East & Africa radiotheranostics market is gradually developing driven by the investment in healthcare in Saudi Arabia, the United Arab Emirates, and Israel. Israel still dominates the region propelled by its extensive research in oncology and nuclear medicine. Investments in cancer care facilities in the GCC nations have also been increasing the demand for radioligand therapies.

Source: Polaris Market Research Analysis

Regulatory Heatmap

| Country | Policy Environment | Key Regulations | Market Implication | Trend |

| US | Favorable | FDA NDA approvals for Pluvicto, Lutathera, and Xofigo; NRC and Agreement State radioactive material licensing | Strong commercial infrastructure; active new indication review pipeline | Expanding |

| European Union | Favorable | EMA centralized marketing authorization; EURATOM radiation protection directives; national nuclear medicine reimbursement | Established clinical adoption; evolving reimbursement expansion across member states | Expanding |

| UK | Favorable | MHRA approval alignment with EMA; NHS commissioning frameworks; Environment Agency radioactive materials regulation | NHS integration driving gradual access expansion; favorable regulatory stance | Expanding |

| Germany | Favorable | BFARM/EMA marketing authorization; GKV-SV reimbursement; Radiation Protection Act (StrlSchG) | Strong academic-clinical adoption; national reimbursement supports patient access | Expanding |

| Japan | Favorable | PMDA approval pathway; national health insurance coverage; Radioisotopes Act | Established nuclear medicine infrastructure; growing RLT commercialization | Expanding |

| Australia | Favorable | TGA therapeutic goods approval; PBS reimbursement; ARPANSA radiation safety | Regional isotope production hub; active RLT clinical programs | Expanding |

| China | Neutral | NMPA radiopharmaceutical regulations; national nuclear medicine development program | Large patient opportunity; domestic production investment and regulatory pathway development | Developing |

| India | Developing | CDSCO radiopharmaceutical regulations; AERB radiation safety; BARC isotope programs | Large oncology patient base; infrastructure investment required for clinical scaling | Developing |

Source: Polaris Market Research Analysis

Radiotheranostics Market Competitive Landscape and Key Players

The radiotheranostics market across the globe is characterized by moderate level of concentration in the competition, where the rivalry exists in terms of approved radioligand therapy commercialization, radioisotope production and sourcing, operation of radiopharmacy dispensing network, and development of clinical stage programs. The main elements of competitive landscape comprise approved portfolio size, supply chain security for radioisotopes, reach of radiopharmacy dispensing network, clinical stage pipeline, and manufacturing reliability and regulatory compliance.

The competitive scenario is getting transformed due to the involvement of major pharmaceutical companies into the expansion of radioligand therapy pipeline, acquisitions of radiopharmaceutical companies and radioisotope manufacturers, and the establishment of partnership in supply chain to ensure future supply of limited radioisotopes. Large pharmaceutical firms compete with the established radiopharmaceutical companies.

Competitive Positioning Table

| Company | Est. Market Position | Primary Focus | Geographic Focus | In Report |

| Novartis | Top 3 | Approved RLT portfolio: Pluvicto and Lutathera; pipeline expansion | Global | Yes |

| Bayer AG | Top 3 | Xofigo Ra-223 commercial; PSMA-targeted pipeline programs | Global | Yes |

| Lantheus Holdings | Top 5 | Radiodiagnostic imaging agents and PSMA theranostic pipeline | North America, Global | Yes |

| Telix Pharmaceuticals | Top 5 | PSMA-targeted diagnostic and therapeutic radiopharmaceuticals | Global | Yes |

| Curium | Top 5 | Radiopharmaceutical manufacturing and distribution network | Europe, North America | Yes |

| ITM Isotope Technologies Munich | Top 10 | Lutetium-177 and Actinium-225 production and RLT development | Europe, Global | Yes |

| Eli Lilly | Top 10 | Targeted alpha therapy pipeline including Ac-225 PSMA programs | Global | Yes |

Source: Polaris Market Research Analysis

Radiotheranostics Market Technology and Innovation Landscape 2025–2026

The radiotheranostics market is advancing through innovation in targeted alpha therapy radioisotope production, automated radiopharmacy dispensing systems, AI-guided dosimetry and treatment planning, novel targeting vector chemistry, and theranostic pairing strategies for emerging tumor antigens.

| Technology | Adoption Stage | Key Development | Market Impact |

| Lutetium-177 Non-Carrier-Added Production | Mainstream adoption | Expanded no-carrier-added Lu-177 reactor production capacity | Supports high specific activity requirements for clinical applications |

| Actinium-225 Targeted Alpha Therapy | Early commercial deployment | New production routes including linear accelerator-based Ac-225 generation | Expands isotope supply for growing alpha therapy clinical pipeline |

| Automated Radiopharmacy Dispensing | Growing deployment | Robotic dispensing systems reducing radiation exposure and improving dose accuracy | Supports scaling of radioligand therapy administration across sites |

| AI-Guided Dosimetry and Treatment Planning | Early commercial deployment | Machine learning integration into absorbed dose calculation workflows | Improves precision of radioligand therapy dose selection |

| Novel Targeting Vectors (FAP, HER2, SSTR) | Growing deployment | Expansion of clinical programs using fibroblast activation protein and HER2 targeting | Broadens addressable tumor indications beyond PSMA and SSTR |

| Theranostic Pairing with PET Imaging | Mainstream adoption | Ga-68 and F-18 diagnostic agents paired with Lu-177 and Ac-225 therapeutics | Enables patient selection and treatment monitoring integration |

Source: Polaris Market Research Analysis

Near-term market development will be primarily driven by expanded PSMA-targeted radioligand therapy adoption and the advancement of Actinium-225-based clinical programs toward regulatory submission. Novel targeting vector programs including FAP and HER2 represent medium-term pipeline contributions that are expected to broaden the addressable indication scope of the radiotheranostics market during the latter part of the forecast period.

Who Buys Radiotheranostics Market Research and Why?

The radiotheranostics market report helps stakeholders identify commercial growth opportunities, evaluate competitive positioning, assess technology and supply chain dynamics, and develop evidence-based strategies for investment, partnership decisions, and market entry across the global oncology radiopharmaceutical landscape.

| Buyer / Investor Type | Primary Use Case | Key Insight Sought | Decision Horizon |

| Pharmaceutical Companies | Pipeline investment and commercial strategy | Indication opportunity and competitive benchmarking | 3–7 years |

| Radioisotope Producers | Capacity planning and partnership development | Demand forecasting by isotope type and region | 5–10 years |

| Hospital and Cancer Center Administrators | Nuclear medicine program development | Infrastructure requirements and patient demand | 2–5 years |

| Venture Capital and Private Equity | Investment evaluation in radiotheranostic biotechs | Platform differentiation and clinical pipeline value | 3–7 years |

| Government and Regulatory Agencies | Nuclear medicine policy and isotope security programs | Market structure and supply chain resilience | 5–10 years |

Source: Polaris Market Research Analysis

What are the Barriers to Entering the Radiotheranostics Market?

-

Radioisotope Supply Access: Securing reliable, long-term access to therapeutic radioisotopes, particularly Actinium-225, requires partnerships with a limited number of specialized production facilities or significant capital investment in isotope production infrastructure.

-

Radiopharmaceutical Manufacturing Compliance: Radioligand therapy manufacturing requires GMP compliance, radiation safety infrastructure, and specialized quality control capabilities that represent significant capital and operational investment.

-

Regulatory Pathway Complexity: Radioligand therapy approval requires clinical evidence of both the targeting agent's safety and efficacy and the radiopharmaceutical product's manufacturing quality, extending the development timeline.

-

Specialized Clinical Administration Infrastructure: Establishing certified nuclear medicine departments with radiation safety compliance programs and specialized oncology monitoring capabilities requires substantial institutional investment.

-

Reimbursement Landscape Navigation: Securing national reimbursement for novel radioligand therapies requires health technology assessment submissions and payer engagement that add time and cost to market access.

-

Intellectual Property and Targeting Vector Licensing: Many established targeting vectors and chelator chemistry platforms are subject to patent protection, creating licensing requirements for new entrants developing competing programs.

Radiotheranostics Market Premium Insights and Forward Outlook

Actinium-225 Supply Chain Development as a Strategic Market Imperative

The commercial scaling of Actinium-225 production represents the most strategically critical supply chain development challenge for the radiotheranostics market through the forecast period. Current global Actinium-225 production capacity is constrained by the limited number of facilities capable of producing the isotope in quantities sufficient for large-scale clinical trials and commercial supply. Investments in uranium-233 decay supply chains, linear accelerator-based production, and thorium-229 generator systems are all being pursued by governments and commercial producers to address this bottleneck, and the company or consortium that achieves scalable, reliable Actinium-225 production first will hold a durable competitive advantage across the targeted alpha therapy market.

Indication Expansion Beyond Prostate Cancer and NETs

The commercial validation of PSMA-targeted and SSTR-targeted radioligand therapies in prostate cancer and neuroendocrine tumors is catalyzing investment in radiotheranostic approaches for a broader set of solid tumor indications. Fibroblast activation protein-targeted programs, HER2-targeted radioligand therapies, and carbonic anhydrase IX-targeted approaches are all in active clinical development, representing a significant pipeline of potential new commercial entrants that could expand the total addressable market substantially through the latter part of the forecast period.

Cost Benchmarking Table

| Product / Service Type | Est. Price Range (USD) | Key Cost Driver | Complexity Tier |

| Lu-177 PSMA Radioligand Therapy (per cycle) | USD 42,000–USD 50,000 per cycle | Isotope, manufacturing, and dispensing cost | High |

| Lu-177 DOTATATE (Lutathera, per cycle) | USD 35,000–USD 45,000 per cycle | Production and radiopharmacy dispensing | High |

| Ra-223 Therapy (Xofigo, per injection) | USD 10,000–USD 13,000 per injection | Isotope production and specialty distribution | Standard-High |

| Ga-68 PSMA PET Imaging Agent (per dose) | USD 1,500–USD 3,500 per dose | Cyclotron or generator production cost | Standard |

| Actinium-225 RLT (investigational) | USD 80,000–USD 150,000+ per cycle | Constrained isotope supply and high production cost | Enterprise |

| Radiopharmacy Dispensing Infrastructure | USD 2,000,000–USD 10,000,000+ | Facility setup and compliance program costs | Enterprise |

Source: Polaris Market Research Analysis

Key Players

- Novartis AG

- Bayer AG

- Lantheus Holdings Inc.

- Telix Pharmaceuticals Limited

- Curium Pharma

- ITM Isotope Technologies Munich SE

- Eli Lilly and Company

- Bristol Myers Squibb Company

- AstraZeneca plc

- Fusion Pharmaceuticals Inc.

- Point Biopharma Global Inc.

- RadioMedix Inc.

- RayzeBio Inc.

Radiotheranostics Market Industry Developments

- April 2026: Actinium Pharmaceuticals launched a pan-tumor development strategy to advance Actinium-225–based targeted radiotherapies across multiple solid tumor indications. The strategy expands the use of radiotheranostics through clinical utilization of targeted alpha-emitting treatments in precision oncology(source: ir.actiniumpharma.com).

- October 2025: SpectronRx initiated large-scale manufacturing of high-purity Actinium-225 (Ac-225) to fortify the availability of radioisotopes in the global cancer-targeted therapeutic landscape. The milestone supports the expansion of radiotheranostics by enabling broader development and commercialization of next-generation targeted alpha therapies(source: www.urotoday.com)

Radiotheranostics Market Segmentation

By Radioisotope Outlook (Revenue, USD Billion, 2021–2034)

- Lutetium-177

- Actinium-225

- Gallium-68

- Radium-223

- Others

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Prostate Cancer

- Neuroendocrine Tumors

- Other Solid Tumors

- Hematologic Malignancies

- Others

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Hospitals

- Cancer Centers

- Imaging Centers

- Specialty Clinics

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

Radiotheranostics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 10.80 Billion |

| Market Size in 2026 | USD 11.80 Billion |

| Revenue Forecast by 2034 | USD 24.21 Billion |

| CAGR | 9.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered | By Radioisotope | By Application | By End User |

| Regional Scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Competitive Landscape | Industry Trend Analysis (2025); Company Profiles including overview, financial information, product benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization available as per requirements with respect to countries, regions, and segmentation. |

FAQ's

• The global radiotheranostics market was valued at USD 10.80 billion in 2025 and is projected to reach USD 24.21 billion by 2034.

• The market is projected to grow at a CAGR of 9.4% during the forecast period from 2026 to 2034.

• North America was the dominant region in the global radiotheranostics market in 2025 and captured around 37.70% of the global revenue share owing to FDA approved radioligand therapies and strong nuclear medicine facility infrastructure.

• Lutetium-177 was the leading radioisotope segment in 2025 with 41.10% revenue share owing to successful commercialization of Pluvicto and Lutathera.

• Actinium-225 is projected to grow at the fastest CAGR during the forecast period, driven by a growing pipeline of targeted alpha therapy clinical programs across multiple tumor indications.

• Participants include Novartis AG, Bayer AG, Lantheus Holdings, Telix Pharmaceuticals, Curium, ITM Isotope Technologies Munich, and Eli Lilly, among many others.

• Primary drivers are increasing FDA and EMA approvals of radioligand therapies, rising capacity for Lutetium-177 and Actinium-225 production, growing use of PSMA-based therapies, and robust pipeline of targeted alpha therapies.

• Neuroendocrine tumors is projected to grow at the fastest application segment CAGR, supported by expanding PRRT treatment center accreditation and growing diagnostic imaging uptake for patient selection.

Download Sample Report of Radiotheranostics Market

Please fill out the form to request a customized copy of the research report.