Viral Vector And Plasmid DNA Manufacturing Market Research Report - Forecast to 2026-2034

REPORT DETAILS

REPORT DETAILS

Viral Vector And Plasmid DNA Manufacturing Market Summary

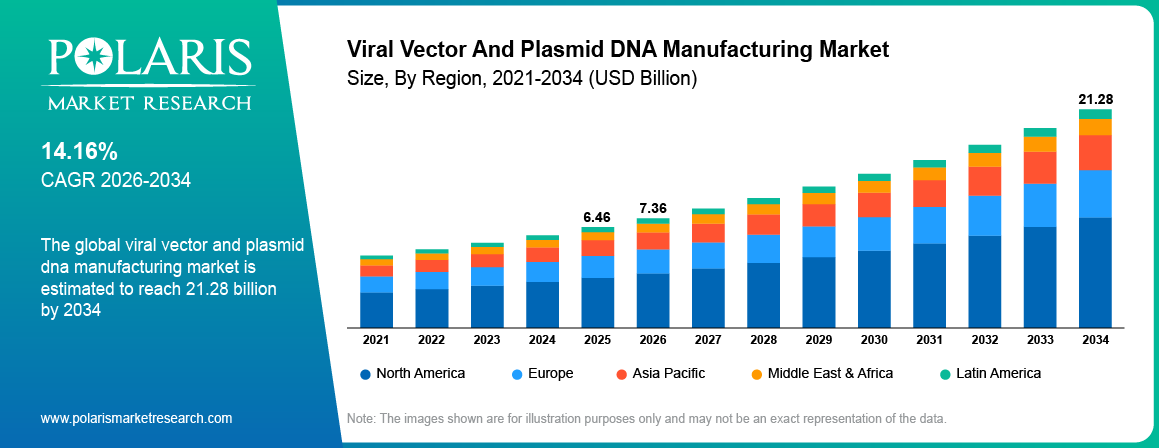

The global market for viral vectors and plasmid DNA manufacturing was estimated to be worth USD 6.46 billion in 2025 and expected to hit USD 21.28 billion by 2034, growing at a CAGR of 14.16%. The growth of this market can be attributed to increasing demand for gene therapy, precision medicine, and regenerative medicine. Additionally, increasing investments and organoids commercialization contribute to the growth of this market. Europe held the largest market share in 2025 owing to strong manufacturing infrastructure for biopharmaceuticals.

Market Statistics

Viral Vector And Plasmid DNA Manufacturing Market Key Takeaways 2025

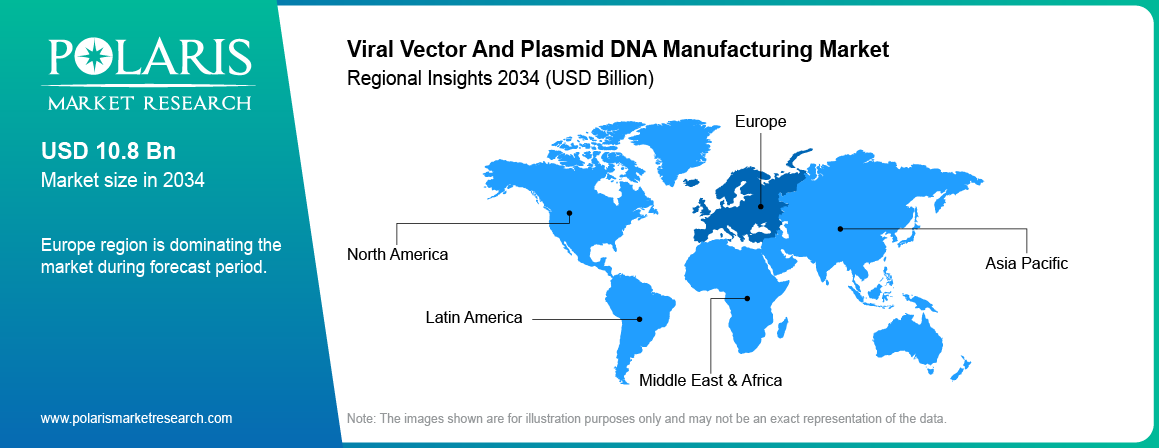

- Europe dominated the market with 42.0% share in 2025 owing to strong manufacturing capabilities and supportive regulations.

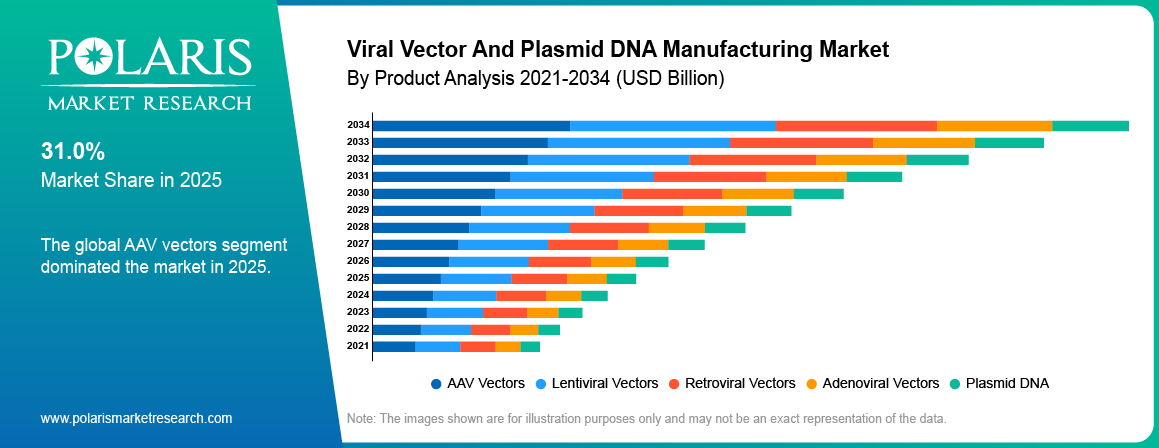

- AAV vectors accounted for the largest product segment accounting for 31.0% in 2025.

- Gene therapy companies represented the largest end-user segment with 37.0% share in 2025.

- Asia Pacific is projected to grow at the fastest CAGR of 16.70% during the forecast period.

- Precision medicine and regenerative therapies are increasing manufacturing demand.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observation

What is Viral Vector And Plasmid DNA Manufacturing?

Viral vector and plasmid DNA manufacturing refers to the production of biological products used in gene therapy, cell therapy, and vaccines. Such biological products facilitate the delivery of genetic material into the target cells and assist in advanced drug discovery.

The supply chain consists of raw material suppliers, producers, contract development and manufacturing organizations, testing service providers, distributors, and end-users. The process of production consists of upstream manufacturing, purification, quality testing, and fill-finish. The final products are delivered to the pharmaceutical and biotechnology firms.

Market growth is supported by increasing clinical trials, expanding commercial manufacturing, and rising investment in advanced therapies. Companies are also improving production technologies to increase manufacturing efficiency. These developments continue to create long-term market opportunities.

Source: Polaris Market Research Analysis

Viral Vector And Plasmid DNA Manufacturing Market Industry Dynamics

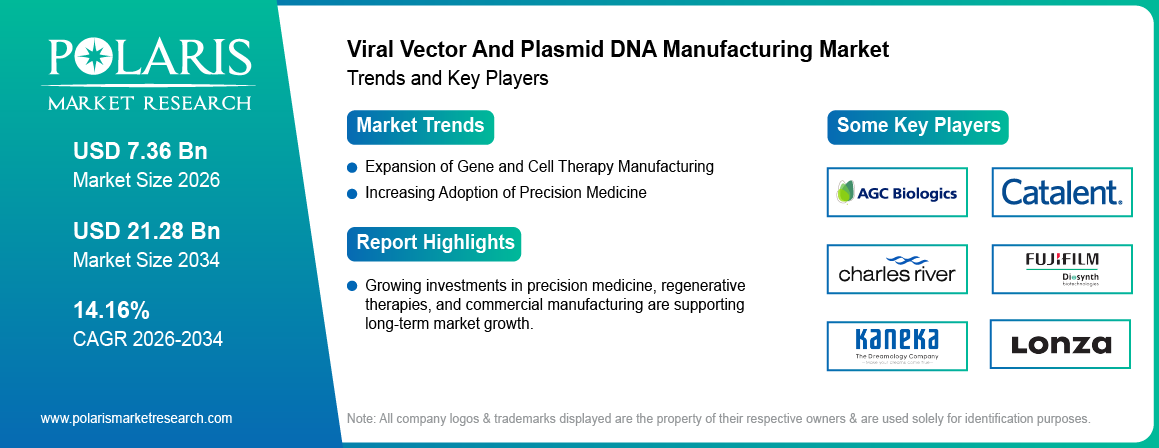

- Rising investments in gene and cell therapy manufacturing are driving market growth.

- Manufacturing technology improvements are increasing production efficiency.

- High manufacturing costs remain a major industry challenge.

- Expansion of regenerative medicine is creating new growth opportunities.

Market Size and Growth Analysis 2026-2034

Market growth is driven by increasing commercialization of gene and cell therapies. Pharmaceutical companies are expanding manufacturing capacity to meet rising clinical and commercial demand. Improvements in production technologies are also supporting market expansion.

Precision medicine and regenerative medicine investments are contributing to an increase in the production process all over the world. Firms have been concentrating on automation, increasing capacity, and collaboration. These initiatives are expected to support steady market growth during the forecast period.

| Market Driver | Est. CAGR Impact | Geographic Relevance | Impact Timeline |

| Precision medicine adoption | +2.3% | Global | Medium to long term |

| Gene therapy manufacturing expansion | +2.0% | US, Europe, Asia Pacific | Medium term |

| Regenerative medicine growth | +1.7% | Global | Long term |

| CDMO partnerships | +1.3% | North America, Europe | Short to medium term |

| Manufacturing technology improvements | +1.0% | Global | Medium term |

* Indicative estimates based on market context and analyst judgment. Figures reflect relative driver weight, not additive CAGR contributions. Source: Polaris Market Research Analysis.

Manufacturing companies are expanding commercial production to meet growing customer demand. Buyers are giving greater importance to production quality, regulatory compliance, and supply reliability. This trend is encouraging continuous investment across the market.

Viral Vector And Plasmid DNA Manufacturing Market Drivers, Restraints and Opportunities

How are Rising Investments in Gene and Cell Therapy Manufacturing Driving Market Growth?

Rising investments in gene and cell therapy manufacturing are increasing demand for viral vectors and plasmid DNA. In May 2026, Cell and Gene Therapy Catapult made investments in Lir Therapeutics, which aims at developing its AAV capsid design platform using AI technology(Source: catapult.org).The manufacture of viral vectors is becoming increasingly efficient due to commercial facilities being developed by pharma and biotech companies owing to an increasing number of therapies. An increasing number of clinical trials and approvals are adding to this demand for manufacture.

How are Manufacturing Technology Improvements Increasing Production Efficiency?

Advancements in manufacturing technologies are making the process of generating viral vectors and plasmid DNA efficient. Automated systems, single-use bioprocessing systems, and sophisticated purification methods are being used by firms to generate better products and scalability. The new technologies are increasing efficiency in terms of time and costs involved. It is facilitating commercial manufacture of the products.

What Challenges Restrict Viral Vector and Plasmid DNA Manufacturing Market Growth?

High manufacturing cost is still hampering commercialization. High costs are associated with the manufacturing process due to special facilities, professionals, and stringent quality control measures. These factors remain key challenges for market participants.

How is the Expansion of Regenerative Medicine Creating Market Opportunities?

Expansion of regenerative medicine is creating significant growth opportunities for the viral vector and plasmid DNA manufacturing market. The increase in cell and gene therapy treatments is leading to an increase in demand for scalable methods of manufacture. For example, CIRM allocated USD 44 Billion to support regenerative medicine research and manufacturing(Source: cirma.ca.org). This helps to expand cell and gene therapy production infrastructure and supporting growth in viral vector and plasmid DNA manufacturing. Rising investments in tissue engineering and organoid research are further increasing production requirements. These trends are expected to support long-term market growth.

Source: Polaris Market Research Analysis

Segment and Regional Leaders at a Glance

According to Polaris Market Research, Europe leads the market while Asia Pacific is the fastest-growing region.

- Dominant Region: Europe

- Fastest Growing Region: Asia Pacific

- Largest Product Segment: AAV Vectors

- Largest End User Segment: Gene Therapy Companies

Segmentation Analysis

The report provides a comprehensive analysis of the viral vector and plasmid DNA manufacturing market by product, workflow, and end user to identify major revenue-generating and high-growth segments.

Viral Vector and Plasmid DNA Manufacturing Market by Product

Which Product Dominated the Market in 2025?

The AAV vectors segment dominated the market with 31.0% share in 2025 owing to its wide use in commercial gene therapy manufacturing. In June 2026, SK pharmteco launched the SKyvec high-yield viral vector platform to improve scalable AAV and lentiviral vector manufacturing and support greater plasmid DNA demand(Source: skpharmteco.com).The segment benefits from increasing regulatory approvals and clinical adoption. Growing investments in gene therapy programs continue to support segment growth.

Which Product is Growing Fastest in the Market?

The lentiviral vectors segment is projected to grow at the fastest CAGR of 14.4% during the forecast period. Increasing use in CAR-T cell therapy and stem cell research is driving demand. Growing clinical development activities are supporting segment expansion.

Viral Vector and Plasmid DNA Manufacturing Market by Workflow

Which Workflow Dominated the Market in 2025?

The upstream processing segment dominated the market with 42.0% share in 2025 due to increasing commercial production of viral vectors and plasmid DNA. Companies are investing in advanced bioreactor technologies to improve production efficiency. These investments continue to strengthen segment growth.

Which Workflow is Growing Fastest in the Market?

The downstream purification segment is projected to grow at the fastest CAGR of 15.0% during the forecast period. Rising demand for high-purity biological products is increasing investment in purification technologies. Continuous process improvements are supporting market growth.

Viral Vector and Plasmid DNA Manufacturing Market by End User

Which End User Dominated the Market in 2025?

Gene therapy companies dominated the market with 37.0% share in 2025 owing to the rapid expansion of commercial gene therapy programs. Increasing product approvals are driving manufacturing demand. Growing investment in advanced therapeutics is supporting segment growth.

Which End User is Growing Fastest in the Market?

CDMOs are projected to grow at the fastest CAGR of 15.0% during the forecast period. Pharmaceutical companies are also beginning to outsource manufacture in order to make processes more scalable and faster. This trend is creating strong growth opportunities for service providers.

Segment Summary Table

| Segment | Category | 2025 Status | Forecast CAGR | Key Driver |

| AAV Vectors | Product | Largest Share | Moderate | Commercial gene therapy adoption |

| Lentiviral Vectors | Product | Fastest Growing | High | CAR-T therapy development |

| Upstream Processing | Workflow | Largest Share | Moderate | Manufacturing expansion |

| Downstream Purification | Workflow | Fastest Growing | High | Higher product purity requirements |

| Gene Therapy Companies | End User | Largest Share | Moderate | Commercial manufacturing demand |

| CDMOs | End User | Fastest Growing | High | Manufacturing outsourcing |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

Europe Viral Vector and Plasmid DNA Manufacturing Market Size and Share

Europe dominated the market with 42.0% share in 2025 owing to favorable regulations and well-established biopharmaceutical manufacturing facilities. In March 2026, New England Biolabs and Touchlight have partnered to introduce the EnClose Cell-free dbDNA Synthesis Kit, making viral vector manufacture faster through a scalable solution compared to traditional plasmid DNA manufacture(Source: neb.com).Germany, the UK, Switzerland, and France remain key manufacturing hubs. Rising investment in advanced therapy medicinal products is supporting regional market growth.

Asia Pacific Viral Vector and Plasmid DNA Manufacturing Market Growth and Forecast

Asia Pacific is projected to grow at the fastest CAGR of 16.7% during the forecast period due to increasing biotechnology investments. China, Japan, South Korea, India, and Singapore are expanding manufacturing capacity for advanced biologics. In June 2026, Zhongmu Healthcare gene therapy trial for retinitis pigmentosa was undertaken, leading to an increased need for the manufacture of GMP-grade AAV vectors and plasmid DNA for the clinical stage. Government backing and increased outsourcing activities are propelling regional growth.

North America Viral Vector and Plasmid DNA Manufacturing Market Size and Share

In 2025, North America occupied a considerable market share of 24.0% owing to its advanced biotechnology sector as well as robust manufacturing infrastructure. The US dominated the regional market as a result of increased investment in the production and research of gene therapies. In May 2026, ProBio and Curocell moved their CAR-T therapy called CRC01 into commercial manufacturing after obtaining BLA approval, thus creating increasing demand for lentiviral vector manufacturing and plasmid DNA manufacturing in GMP grades.

Latin America Viral Vector and Plasmid DNA Manufacturing Market Size and Share

Latin America is witnessing steady growth at a CAGR of 13.1% due to increasing healthcare investments and improving biotechnology infrastructure. Brazil, Mexico, and Argentina are expanding research activities across advanced therapies. Growing pharmaceutical investments continue to support market expansion.

Middle East & Africa Viral Vector and Plasmid DNA Manufacturing Market Size and Share

The Middle East and Africa market is growing steadily at a CAGR of 12.9% due to increasing healthcare modernization and biotechnology investments. Saudi Arabia, the UAE, Israel, and South Africa are increasing capacities in the pharmaceuticals manufacturing industry. In June 2026, Genetix Biotherapeutics and SPIMACO entered into a collaboration to bring to market and manufacture LYFGENIA and ZYNTEGLO gene therapies in Saudi Arabia and other regions in the Middle East. There are government policies that are creating market growth opportunities.

Regulatory Heatmap

| Region/Country | Policy Environment | Key Regulations | Market Implication | Trend |

| US | Favorable | Official program or regulatory framework in Source Log | Supports procurement and validation | Expanding |

| Canada | Neutral | Federal and provincial procurement rules | Requires local buyer qualification | Developing |

| Germany | Favorable | EU framework plus national programs | Supports regulated adoption | Expanding |

| UK | Neutral | UK standards and procurement framework | Creates entry requirements | Stable |

| China | Favorable | Industrial policy and localization rules | Supports scale but raises localization risk | Expanding |

| Japan | Favorable | Technology and healthcare/industrial policy | Supports premium applications | Stable |

| India | Developing | Sector programs and procurement rules | Creates long-term volume upside | Developing |

| Australia | Neutral | Standards and pilot funding frameworks | Supports selective deployments | Developing |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Competitive Landscape and Key Players

The market has moderate fragmentation owing to the existence of international producers and specialized CDMOs. Competitive advantage is established on the basis of manufacturing capabilities, quality, regulation, and efficiency. There is ongoing investment in facility development, partnership building, and technology adoption among the companies operating in this market.

Players involved in the market are Thermo Fisher Scientific Inc., Lonza Group, Merck KGaA, Catalent Inc., Sartorius AG, FUJIFILM Diosynth Biotechnologies, Charles River Laboratories, Oxford Biomedica plc, AGC Biologics, and WuXi Advanced Therapies. Players are developing their manufacturing capacity, bioprocessing technologies, and strategic alliances to cater to the rising demand for gene and cell therapy drugs.

Competitive Positioning Table

| Company | Est. Market Position | Primary Strength | Geographic Focus | In Report |

| Thermo Fisher Scientific | Top 5 | Global manufacturing network | Global | Yes |

| Lonza | Top 5 | CDMO expertise | North America, Europe | Yes |

| Catalent | Top 10 | Viral vector manufacturing | Global | Yes |

| Charles River Laboratories | Regional Leader | Bioprocessing services | US, Europe | Yes |

| Oxford Biomedica | Niche Leader | Lentiviral vector platform | Europe | Yes |

| Sartorius | Top 10 | Bioprocess solutions | Global | Yes |

| WuXi Advanced Therapies | Top 10 | Cell and gene therapy manufacturing | Global | Yes |

* Estimated market positioning based on revenue scale, geographic reach, and service breadth. Not ranked by precise market share percentage. Source: Polaris Market Research Analysis.

Technology and Innovation Landscape

The market is witnessing continuous improvements in manufacturing technologies and production efficiency. The adoption of automation and process digitalization will enhance product quality. Growth in commercial manufacturing platforms will drive large-scale production.

| Technology | Adoption Stage | Key Development | Market Impact |

| Automation | Growing Deployment | Automated production systems | Improves manufacturing efficiency |

| Digital Analytics | Early Commercial | Process monitoring | Enhances quality control |

| Quality Management Systems | Mainstream | Digital documentation | Supports regulatory compliance |

| Single-use Manufacturing | Growing Deployment | Flexible production platforms | Reduces production time |

| Commercial Scale Manufacturing | Early Commercial | Capacity expansion | Improves product availability |

Source: Polaris Market Research Analysis

Buyer Use Cases and Market Entry Barriers

This report is useful for analyzing market opportunities, production trends, and competitive positioning. It also helps with investment decisions and regional expansion plans. The buyers are able to detect high growth segments and make future demand predictions.

| Buyer / Investor Type | Primary Use Case | Key Insight Sought | Decision Horizon |

| Biotechnology Companies | Manufacturing expansion | Production capacity | 2–5 Years |

| Pharmaceutical Companies | Supplier selection | Manufacturing capability | 1–3 Years |

| CDMOs | Capacity planning | Outsourcing demand | 2–5 Years |

| Investors | Opportunity assessment | Market growth | 3–7 Years |

| Government Organizations | Policy planning | Industry development | 3–7 Years |

Source: Polaris Market Research Analysis

What are the Barriers to Entering the Market?

- High capital investment for manufacturing facilities.

- Strict regulatory and quality requirements.

- Complex production and validation processes.

- Limited availability of skilled professionals.

- Long development and commercialization timelines.

- Need for advanced manufacturing technologies.

Premium Insights and Forward Outlook

Demand for viral vectors and plasmid DNA is expected to increase with the expansion of precision medicine and regenerative therapies. Companies are investing in larger manufacturing facilities and advanced production technologies. Growing organoid commercialization is expected to create additional business opportunities.

Cost Benchmarking Table

| Product | Est. Price Range | Key Cost Driver | Complexity Tier |

| AAV Vectors | USD 60,000–300,000 | Manufacturing process | High |

| Lentiviral Vectors | USD 80,000–450,000 | Technology integration | High |

| Plasmid DNA | USD 30,000–180,000 | Purification process | Medium |

| Manufacturing Services | USD 150,000–900,000 | Production scale | High |

Source: Polaris Market Research Analysis

Key Players

- AGC Biologics

- Catalent Inc.

- Charles River Laboratories

- FUJIFILM Diosynth Biotechnologies

- Kaneka Corporation

- Lonza Group

- Merck KGaA

- Oxford Biomedica

- Sartorius AG

- Thermo Fisher Scientific Inc.

- VGXI Inc.

- WuXi Advanced Therapies

Industry Developments

- January 2025: Asimov and AGC Biologics partnered to streamline and reduce the cost of viral vector manufacturing through a single-plasmid production platform(Source: asimov.com).

- May 2025: 3PBIOVIAN introduced new technology platforms to accelerate and enhance the efficiency of viral vector manufacturing(source: 3pbiovian.com)

Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- AAV Vectors

- Lentiviral Vectors

- Retroviral Vectors

- Adenoviral Vectors

- Plasmid DNA

By Workflow Outlook (Revenue, USD Billion, 2021–2034)

- Upstream Processing

- Downstream Purification

- Fill-Finish and Testing

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Gene Therapy Companies

- CDMOs

- Academic & Research Institutes

- Pharmaceutical Companies

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 6.46 Billion |

| Market Size in 2026 | USD 7.36 Billion |

| Revenue Forecast by 2034 | USD 21.28 Billion |

| CAGR | 14.16% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

• The global viral vector and plasmid DNA manufacturing market was valued at USD 6.46 billion in 2025 and is projected to witness steady growth during the forecast period.

• The global market is forecast to reach USD 21.28 billion by 2034 at a CAGR of 14.16% during 2026-2034.

• Europe was the leader in the market accounting for 42.0% share in 2025 owing to developed biopharmaceutical manufacturing facilities in Europe as well as favorable regulations.

• AAV vectors held the dominating market share of 31.0% in 2025 due to its wide application in gene therapy manufacturing.

• Major companies include Thermo Fisher Scientific Inc., Lonza Group, Merck KGaA, Catalent Inc., Sartorius AG, Oxford Biomedica plc, Charles River Laboratories, FUJIFILM Diosynth Biotechnologies, AGC Biologics, and WuXi Advanced Therapies.

• Growing demand for gene therapies, precision medicine, regenerative medicine, and organoid commercialization is driving market growth.

• In 2025, gene therapy companies accounted for the largest market share of 37.0% due to increasing commercialization of advanced therapies.

Download Sample Report of Viral Vector And Plasmid DNA Manufacturing Market

Please fill out the form to request a customized copy of the research report.