Revenue Cycle Management Market Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Revenue Cycle Management Market Summary

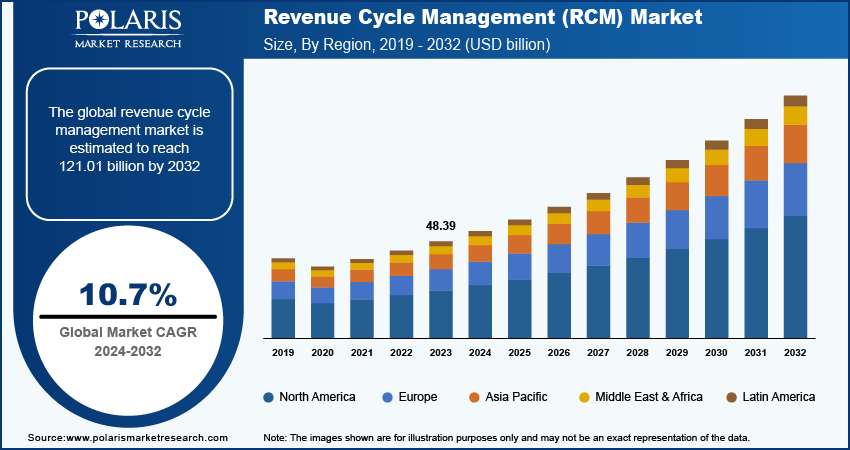

The global revenue cycle management market was valued at USD 85.2 billion in 2025 and is expected to register a CAGR of 11.53% from 2026 to 2034. This expansion is attributed to rising demand for efficient healthcare billing systems and automation in medical administration. The market’s momentum is fueled by rising claims and denial management complexities, increasing focus on medical billing automation, and the growing demand for revenue integrity across hospital chains, physicians, and diagnostic networks. Emerging revenue models and the complexity of payer rules have created the need for integrated RCM platforms from hospitals and physicians.

Market Statistics

Key Takeaways

- North America led the market with 40.0% revenue in 2025, owing to extensive healthcare infrastructure and technology adoption.

- The Asia Pacific revenue cycle management market is expected to register a CAGR of 14.6% during the forecast period. Rapid economic development and increasing healthcare expenditures are driving market growth in the region.

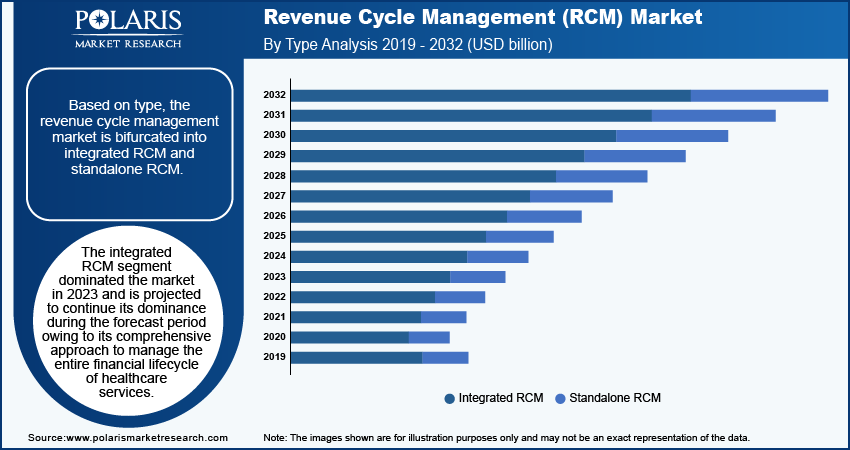

- The integrated RCM segment had the largest market share accounting for 65.0% in 2025. This is because of the holistic management offered for the entire financial life cycle of healthcare services.

- Medical coding and billing held a 21.0% market share in 2025. This is primarily due to its essential role in facilitating accurate claims submission and reimbursement.

- The electronic health record (EHR) segment is projected to register the highest CAGR of 12.5% during the forecast period. Its ability to improve overall healthcare process efficiency by integrating patient records will drive the growth rate.

When readers assess the revenue cycle management software market, they tend to focus on features that help healthcare providers avoid losing revenue. In particular, there is a strong interest in modules that facilitate denial prevention, automatically verify patient eligibility before services are delivered, and speed up patient collections. Together, these capabilities improve cash flow. They also reduce billing errors and administrative rework. All of this makes revenue operations more efficient and predictable.

Industry Dynamics

- The rising number of clinics and hospitals across the world drives the industry growth.

- Growing investments by governments in developing healthcare infrastructure propel the RCM market expansion.

- High costs associated with revenue cycle management hinder market development.

- Rising reliance on prior authorization processes and growing scrutiny from payers has resulted in increased demand for automation tools. This shift is opening up various growth opportunities for RCM vendors over the forecast period.

AI Impact on Revenue Cycle Management (RCM) Market

- Artificial intelligence (AI) technology translates clinical notes into billing codes. It leads to reduced risk of human errors and speeds up claims processing.

- AI provides forecasts on the claim denials, which improves resolution rates and reduces revenue loss.

- AI in revenue cycle management tools verifies insurance coverage instantly. It helps improve patient experience and minimize delays.

- AI streamlines the entire billing cycle. This saves time and reduces administrative burden.

What is Revenue Cycle Management (RCM)?

Revenue Cycle Management (RCM) is the financial process in healthcare organizations. RCM is used to track patient care episodes from appointment scheduling and registration to final payment collection. It integrates administrative and clinical functions, including insurance verification, coding, billing, claims submission, payment posting, and collections. RCM helps ensure accurate and timely reimbursement.

Real-world applications of AI in revenue cycle management include high-volume and rule-based functions. These are coding assistance, medical documentation assistance to improve clinical documentation, denial analytics, and follow-ups on claim status. However, to be successful, audit-ready processes have to be implemented. Healthcare organizations increasingly seek applications of AI that provide explainable results, rule-driven processes, and human oversight to avoid disputes over denied claims and to understand how results were attained.

Revenue cycle management (RCM) begins when a patient makes an appointment and ends when the account balance is resolved through contractual adjustments, insurance payments, write-offs, or patient payments. Healthcare organizations use RCM to manage the clinical functions associated with claims processing and revenue generation. RCM aims to increase accurate revenue through various processes by identifying and improving deficiencies.

Source: Polaris Market Research Analysis

From an operational standpoint, revenue cycle management is typically divided into three stages: front-end activities such as patient access and eligibility checks, mid-cycle processes including coding, charge capture, and documentation, and back-end functions covering claims submission, denial management, payment posting, and collections. RCM systems help organizations improve key performance metrics such as clean claim rates, days in accounts receivable, and cost-to-collect by reducing manual rework and limiting revenue leakage throughout the entire workflow.

The growing digitization of healthcare is driving the revenue cycle management market. The complexity of billing and claims processes increases as healthcare organizations adopt electronic health records (EHRs), telemedicine platforms, patient portals, billing automation, and other digital tools. A report from the OECD indicates that nearly 93% of the primary care practices in the 24 member nations of the OECD utilized electronic medical records in 2021. Handling the large volume of data generated by such platforms requires efficient RCM solutions.

Data silos within healthcare organizations are rising. This has led to increased demand for revenue cycle management solutions. Accessing information is harder when patient and financial data are in separate systems. The data separation also makes maintaining consistency across workflows difficult. RCM platforms solve this by consolidating data from billing, coding, and claims into a single view. Fragmented systems also increase the chances of claim denials. This is because gaps in eligibility, authorization, and documentation are more difficult to identify at an early stage. As a result, modern RCM platforms are built around unified workflows. These platforms connect eligibility verification with authorization tracking, coding edits, and claim scrubbing. This integrated approach prevents denials. It also reduces rework across the revenue cycle.

The market for revenue cycle management is driven by the rising number of hospitals and clinics across the globe. According to published data from the WHO, there were 165,000 hospitals worldwide in 2021. The presence of a large number of hospitals and medical institutions is often associated with an increased number of administrative tasks such as billing, coding, and collection processes. RCM systems make administrative tasks easier by efficiently performing them with technology. This increases the adoption of RCM systems in a large number of hospitals and clinics. Growth in provider networks also increases complexity in payer contracting and reimbursement rules. This makes claims and denial management capabilities like appeals workflows and underpayment recovery more important for sustaining margins.

Revenue Cycle Management (RCM) Stages and Functions

| RCM Stage | Function |

| Medical Coding | Converts clinical procedures, diagnoses, and treatments into standardized medical codes. It enables accurate billing and insurance claims processing. |

| Billing | Generates patient bills and payer invoices based on coded healthcare services and prepares charges for submission. |

| Claims Submission | Sends insurance claims to payers for reimbursement, verifies claim accuracy, and ensures compliance with payer requirements. |

| Payment Processing | Posts insurer and patient payments, manages denials or underpayments, and follows up on outstanding balances for complete revenue collection. |

Source: Polaris Market Research Analysis

Revenue Cycle Management Market – Opportunity and Drivers

Rising Patient Financial Responsibility and Denial Prevention Automation

Deductibles and out-of-pocket costs are rising. So, providers are placing greater emphasis on patient financial engagement tools that offer clearer upfront cost estimates and flexible payment options. Preference is also being given to tools that lower bad-debt risk. Meanwhile, increasingly complex payer rules and prior authorization requirements are driving demand for automation to prevent denials and accelerate reimbursement. All of these factors make it one of the most immediate growth opportunities for the revenue cycle management software and RCM services landscape.

Growing Spending by Governments on Healthcare Infrastructure

Government investments include funding for medical technologies and advanced diagnostic equipment. Upgrades such as these add new codes, services, and procedures. There is a subsequent need for well-developed RCM solutions to address all changes and ensure timely claims processing. According to the Institute for Health Metrics and Evaluation, 62% of global health spending in 2021 was paid for by governments. Government investments also accelerate digitization mandates and interoperability programs. These, in turn, raise demand for integrated RCM platforms able to adapt quickly to changes in coding and reimbursement while keeping financial workflows audit-ready.

Source: Polaris Market Research Analysis

Segment Insights

Revenue Cycle Management Breakdown – by Type Insights

Based on type, the revenue cycle management market is bifurcated into integrated RCM and standalone RCM. The integrated RCM segment had the largest share accounting for 65.0% in 2025 and is expected to remain the same throughout the forecast period, driven by its end-to-end approach to managing the financial lifecycle of services delivered in the healthcare sector. Integrated RCM systems seamlessly integrate clinical and administrative tasks. They make billing, coding, claims, and patient collections more efficient. Real-time integration and analysis of data are also facilitated in such systems, thus ensuring compliance with regulatory requirements. Integrated platforms are also preferred because they reduce handoffs between point solutions, provide better visibility into analytics across the revenue cycle workflow, and enable edits that improve billing accuracy and claim automation.

Revenue Cycle Management Breakdown – by Function Insights

In terms of function, the revenue cycle management market is segmented into claims and denial management, medical coding and billing, electronic health records (EHR), clinical documentation improvement (CDI), insurance, and others. Medical coding and billing held 21.0% market share in 2025 due to its importance in correctly submitting and processing payments. Medical coding and billing systems are a very crucial part of coding healthcare services and submitting them to insurance companies for claim payments. Complexity in medical coding, along with precise and timely medical billing, has created a significant need for efficient tools, such as medical coding and billing systems, that are less prone to errors and better at maximizing payments. These systems play a major role in combating denial payments, improving payments, and thereby claiming a prominent market share in 2025.

Claim and denial management remains an important focus area for providers as they seek to minimize denials by improving eligibility verification, authorization verification, coding edit reviews, and fast-track appeals processes. RCM solutions that integrate denial analytics with operational tools such as work queues, root cause analysis, and current payer rules are increasingly recognized as a revenue protection solution rather than claims submission tools.

The electronic health record (EHR) segment is projected to grow rapidly with a CAGR of 12.5% over the forecast period. This is attributed to the ability to improve overall healthcare process efficiency by integrating patient records. EHRs ensure easy access to and sharing of medical records among various healthcare practitioners. EHRs make it easy to coordinate patient care and minimize administrative tasks. The need for access to patient data to make clinical decisions drives the growth of EHRs. When deeply integrated with RCM, EHRs enhance the quality of charge capture and documentation.

Source: Polaris Market Research Analysis

Regional Insights

By region, the study provides the revenue cycle management market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America revenue cycle management market accounted for the largest market share capturing 40.0% in 2025, with the U.S being the leading country in the regional market. The overall healthcare infrastructure in the U.S., with high technology adoption, played a vital role in its leading share. Healthcare organizations across the country are increasingly adopting advanced tools like RCM to optimize financial operations, claims processing, and billing efficiency. Moreover, high healthcare spending and advancements played a vital role in establishing a leading share in this market. According to statistics released by the California Health Care Foundation, $4.3 trillion, over $12,500 per individual, was spent by the U.S. on healthcare in 2021. The region’s mature payer ecosystem and strong adoption of revenue cycle outsourcing and automation initiatives further support demand for advanced RCM solutions.

The Asia Pacific revenue cycle management market is expected to register a CAGR of 14.6% during the forecast period. The regional market growth is driven by rapid economic development and increasing healthcare expenditures. The market is also benefiting from expanding healthcare infrastructure in countries such as India and China. The push toward digital transformation and improvements in healthcare access have led to the use of advanced solutions that enhance billing accuracy and operational efficiency. Moreover, Asia Pacific has a large and steadily growing population, along with a rising burden of chronic diseases. These factors are increasing the need for scalable financial management tools such as revenue cycle management solutions. The region accounts for around 60% of the global population, representing more than 4.3 billion people, which places significant pressure on healthcare systems. As patient volumes grow, providers require RCM platforms that can scale easily and handle the financial and operational complexities of a rapidly expanding patient base. Furthermore, modernization of claims processing and increased focus on scalable hospital billing systems are accelerating the use of cloud-based revenue cycle management solutions across major APAC economies.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

Key market players are investing heavily in research and development to expand their offerings. This is expected to fuel the revenue cycle management market growth in the coming years. Market participants are also undertaking a variety of strategic activities. They include innovative launches, international collaborations, higher investments, and mergers and acquisitions to expand their global footprint. To expand and survive in a more competitive and rising market environment, the revenue cycle management industry must offer innovative solutions.

The competitive landscape can be broadly divided into four main vendor groups. The first includes platform and EHR-aligned providers that offer fully integrated, end-to-end RCM solutions. The second group consists of specialized RCM software vendors focused on coding, denial management, and analytics. The third category covers RCM services and BPO providers that support outsourced revenue cycle operations. The fourth includes claims infrastructure and clearinghouse-adjacent solutions that enable eligibility checks and claim routing.

This classification helps buyers compare vendors based on the depth of integration, the level of services provided, and the maturity of automation capabilities.

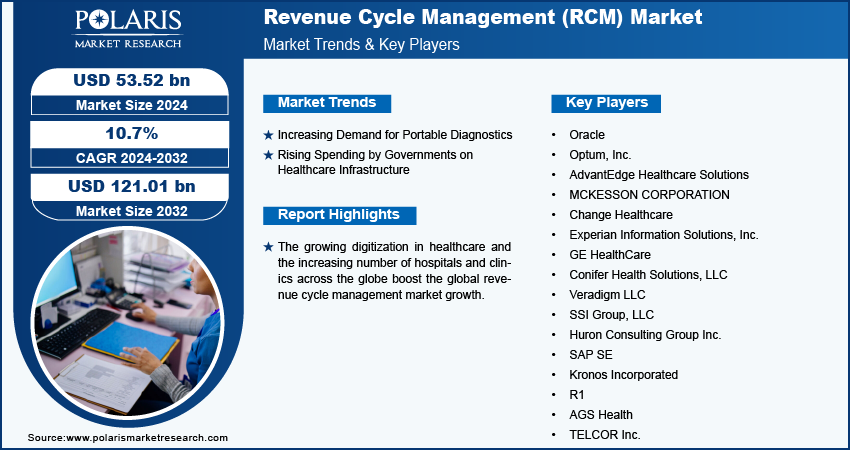

The revenue cycle management market is fragmented, with the presence of numerous global and regional market players. Major players in the market are Oracle; Optum, Inc.; AdvantEdge Healthcare Solutions; MCKESSON CORPORATION; Change Healthcare; Experian Information Solutions, Inc.; GE HealthCare; Conifer Health Solutions, LLC; Veradigm LLC; SSI Group, LLC; Huron Consulting Group Inc.; SAP SE; Kronos Incorporated; R1; AGS Health; and TELCOR Inc.

Oracle, founded in 1977, is a global technology company known for its database software and enterprise solutions. In healthcare, Oracle provides revenue cycle management platforms that help organizations simplify financial processes, improve revenue, and make the patient experience smoother. In July 2024, Odyssey House, a mental health and substance abuse treatment provider in Utah, started using Oracle Health to improve patient care and manage revenue more effectively.

McKesson Corporation, established in 1833 and headquartered in New York City, is a major healthcare services and IT provider. The company offers comprehensive RCM solutions. Its solutions are created to improve financial outcomes while supporting better patient experiences. McKesson’s RCM platforms are based on a clinically integrated approach. They link clinical and operational data to simplify workflows and support more efficient care delivery.

List of Key Companies

- AdvantEdge Healthcare Solutions

- AGS Health

- Change Healthcare

- Conifer Health Solutions, LLC

- Experian Information Solutions, Inc.

- GE HealthCare

- Huron Consulting Group Inc.

- Kronos Incorporated

- MCKESSON CORPORATION

- Optum, Inc.

- Oracle

- R1

- SAP SE

- SSI Group, LLC

- TELCOR Inc.

- Veradigm LLC

Revenue Cycle Management Industry Developments

Recent trends indicate a growing level of consolidation, AI adoption, and the rise of end-to-end platforms amongst revenue cycle management firms. These factors indicate the overall market trend of revenue cycle automation and integration.

February 2026: Firstsource Solutions Limited announced a strategic partnership with Prosper AI. It emphasizes scaling AI-driven voice workflows across healthcare revenue cycle management (RCM). Firstsource will deploy AI-powered voice agents and agentic capabilities across critical patient-facing and administrative processes. It will help healthcare providers enhance patient access, financial performance, and regulatory compliance. (Source: firstsource.com)

May 2025: New Mountain Capital merged three of its portfolio companies to launch an AI-enabled revenue cycle management (RCM) platform. The merged companies include Access Healthcare, SmarterDx, and Thoughtful.ai. (Source: newmountaincapital.com)

Future of Revenue Cycle Management (RCM) Market

As per our study on RCM, the market is expected to grow rapidly in the coming years. AI-driven automation improves coding accuracy, reduces claim denials, and speeds up reimbursement cycles. Adoption of such technologies is projected to offer lucrative opportunities in the coming years. Cloud-based RCM platforms are gaining popularity. This is due to their scalability, lower infrastructure costs, and real-time access to financial data. Growing demand for interoperability is also driving integration between RCM systems and electronic health records (EHRs). It enables smoother data exchange and better workflow efficiency. Further, predictive analytics and patient-centric payment solutions would enhance financial performance and patient satisfaction across healthcare organizations.

Revenue Cycle Management Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Integrated RCM

- Standalone RCM

By Function Outlook (Revenue, USD Billion, 2021–2034)

- Claims and Denial Management

- Medical Coding and Billing

- Electronic Health Record (EHR)

- Clinical Documentation Improvement (CDI)

- Insurance

- Others

By Deployment Outlook (Revenue, USD Billion, 2021–2034)

- Web-Based

- On-Premise

- Cloud-Based

By Component Outlook (Revenue, USD Billion, 2021–2034)

- Software

- Services

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Hospitals

- General Physicians

- Labs

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Revenue Cycle Management Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 85.2 billion |

| Market Size in 2026 | USD 94.9 billion |

| Revenue Forecast by 2034 | USD 227.5 billion |

| CAGR | 11.53% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Revenue Cycle Management Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global revenue cycle management market size stood at USD 85.2 billion in 2025 and is projected to grow to USD 227.5 billion by 2034.

The global market is projected to register a CAGR of 11.53% during the forecast period.

North America accounted for the largest share of the global market in 2024

Oracle; Optum, Inc.; AdvantEdge Healthcare Solutions; MCKESSON CORPORATION; Change Healthcare; Experian Information Solutions, Inc.; GE HealthCare; Conifer Health Solutions, LLC; Veradigm LLC; SSI Group, LLC; Huron Consulting Group Inc.; SAP SE; Kronos Incorporated; R1; AGS Health; and TELCOR Inc. are among the key players in the market.

The electronic health record (EHR) segment is projected for significant growth in the global market during the forecast period.

The integrated RCM segment dominated the market in 2025.

Integrated RCM is typically part of a unified electronic health record (EHR) system. Standalone RCM is a separate system that needs to integrate with various other healthcare software applications.

The most important modules in RCM software focus on automation, integration, and analytics. The include patient access, intelligent claim scrubbing & submission, denial management & appeals, and analytics & reporting.

Revenue cycle management reduces denials and underpayments by catching errors before claims are submitted and automating processes to minimize human error.

Healthcare providers should consider outsourcing RCM when facing declining revenue, high denial rates, or staffing shortages.

Download Sample Report of revenue cycle management market

Please fill out the form to request a customized copy of the research report.