U.S. Silent Generator Market Demand, Growth Opportunity, 2025-2034

REPORT DETAILS

U.S. Silent Generator Market Summary

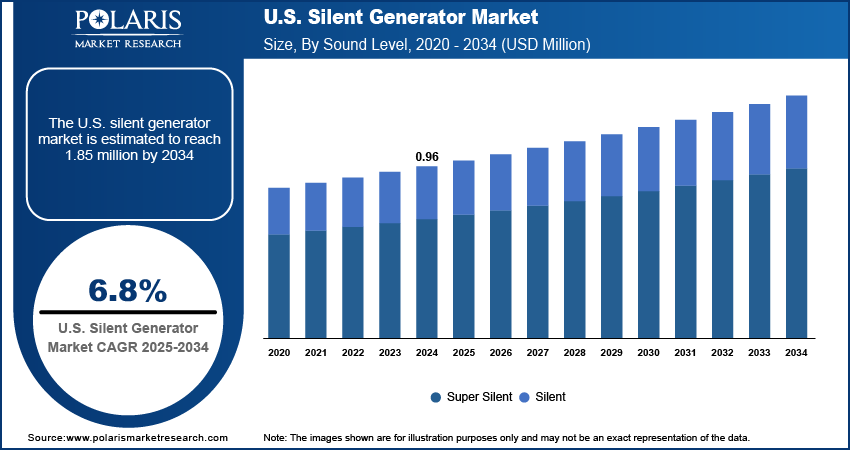

The U.S. silent generator market size was valued at USD 0.96 million in 2024 and is anticipated to register a CAGR of 6.8% from 2025 to 2034. The silent generator demand in the U.S. is mainly driven by the growing need for reliable backup power due to frequent power outages. These outages are often caused by aging power grids and extreme weather conditions. The demand is also boosted by stricter rules on noise pollution, especially in city areas.

Market Statistics

Key Takeaways

- By sound level, the silent segment held the largest share in 2024. These are the generators with noise levels between 60 to 70 decibels.

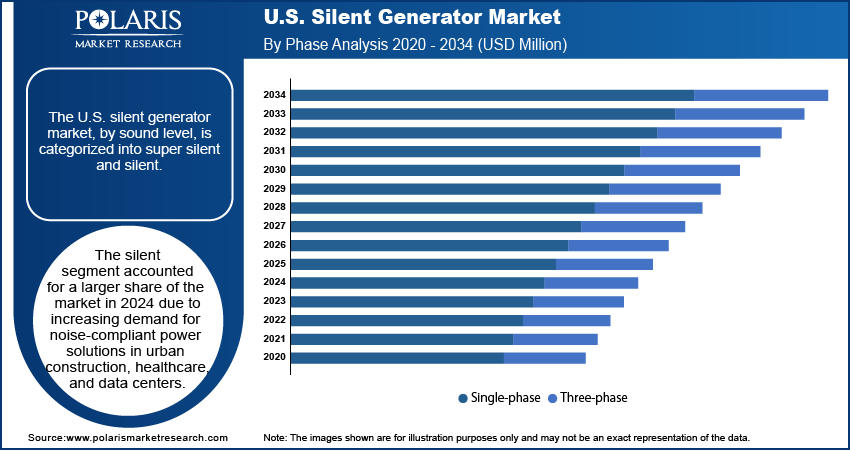

- In terms of phase, the single-phase segment dominated in 2024, due to its high demand in residential and small-scale commercial settings.

- Based on type, the stationary segment held the largest share in 2024. These generators are used in high-power applications that require continuous, reliable backup.

- By fuel type, the diesel segment held the largest share in 2024. The dominance is attributed to its use in heavy-duty commercial and industrial applications.

- Based on end use, the commercial segment dominated in 2024, as offices, retail stores, and hotels need a reliable and quiet power supply.

Industry Dynamics

- The rising frequency of power outages from aging electrical grids and extreme weather events is a major growth driver. This drives a need for dependable backup power solutions across residential and commercial sectors to ensure continuous operation and energy security.

- Stricter rules on noise pollution, especially in urban areas, are driving the adoption of silent power sources. This has made generators with low decibel levels a preferred choice for hospitals, hotels, and residential buildings where a quiet atmosphere is important.

- Growth in infrastructure and construction projects, along with increased mining activities in remote locations, is boosting demand. These sites often lack access to a main power grid and rely on portable, reliable power sources to run their equipment without causing a noise disturbance.

A silent generator is a power-generating unit specifically designed to operate with very little noise. These units have special soundproof covers and features that reduce sound coming from their engine and exhaust systems. They are an ideal fit for places where noise is a concern, such as residential areas, hospitals, and outdoor events.

One of the drivers for the market growth is the increasing popularity of outdoor and recreational activities. This includes things such as tailgating, camping, and outdoor concerts. People who enjoy these activities need a reliable power source for their equipment, but they also want to keep the area quiet for a better experience. Portable silent generators are a good fit for this need.

Another driver is the rise of the film and entertainment industry. These industries need power for their cameras, lights, and sound equipment. However, they need a power source that does not interfere with sound recordings. Thus, thermoelectric generators and silent generators have become necessary equipment for many film and television sets.

Source: Polaris Market Research Analysis

Drivers and Trends

Power Grid Vulnerability and Extreme Weather: The rise in the number of power failures in the U.S. contributes to the silent generator market growth. The power grid in the U.S. is in a dilapidated state and incapable of sustaining the growth in power demand. Most of the aged power grid infrastructure is also more sensitive to adverse weather conditions. This increases the risk of blackouts for the public and businesses. Thus, there is also an increase in the need for parked power solutions to support the uninterrupted operations of essential services and the seamless flow of daily activities.

The U.S. Census Bureau's 2023 American Housing Survey found that 1 in 4 U.S. households reported experiencing at least one complete power outage in the previous year. Of these, 70% said at least one outage lasted for six hours or more. The high rate and long duration of these outages highlight the need for backup power. This trend shows how vital silent generators are becoming for those seeking to keep their homes and businesses running during an emergency.

Increase in Construction and Infrastructure Development: The U.S. silent generator market is strongly influenced by the steady increase in construction and infrastructure development. Government initiatives like the Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA) inject substantial federal funding into modernizing infrastructure, clean energy projects, and utility networks, fostering demand for reliable, quiet power backup solutions essential for construction sites and urban expansion. Growth in residential, commercial, and nonresidential construction segments, including healthcare facilities and data centers, further boosts the need for silent generators that minimize noise pollution and comply with stricter environmental regulations.

Additionally, the rise of smart buildings and sustainability-driven design elevates demand for energy-efficient, low-emission generators supporting uninterrupted power in sensitive environments. Urbanization trends, especially in growth corridors like the Southern U.S., sustain infrastructure investments, making silent generators crucial for continuous operation during grid outages. Market growth is also underpinned by advancements in construction technology and a focus on resilient, environmentally responsible urban development, positioning silent generators as vital to supporting expanding construction activities throughout the country in 2025 and beyond.

According to the U.S. Census Bureau's "Monthly Construction Spending" report from November 2023, total construction spending was estimated at an annual rate of $2,050.1 billion, which was a 6.2% increase from the same period in 2022. This growth in construction spending points to more projects needing on-site power solutions. The increase in construction activity, particularly in areas where noise levels are a concern, boosts the demand for silent generators across the U.S.

Source: Polaris Market Research Analysis

Segmental Insights

Sound Level Analysis

Based on sound level, the segmentation includes super silent and silent. The silent segment held a larger share in 2024. These generators are designed to operate in a business and industrial setting that works silently for a range of 60 to 70 decibels. There is a perfect balance between performance, power, and noise reduction, so they are a good choice for places such as construction, industrial buildings, and large public events. Silent generators are ideal for a wide range of power ratings as well, and are good for both small and larger businesses.

The super silent segment is anticipated to register a higher growth rate during the forecast period. These are the most silent generators, working on lower than 60 decibels. The generators are highly in demand for areas such as homes, hospitals, hotels, and schools that require minimal noise. Urban cities seeking to reduce noise pollution further are a major driver of their rapid growth. The awareness of noise control and its benefits is growing steadily, and so the demand for super silent generators is growing fast.

Phase Analysis

Based on phase, the segmentation includes single-phase and three-phase. The single-phase segment held a larger share in 2024. This is mostly because of the convenience that single-phase units provide for residential and small commercial uses. These units are meant to operate the appliances, tools, and electronics that function on single-phase electricity. Homeowners, small business owners, and event planners are the most frequent customers. They require a portable and reliable backup generator and use it for everyday operations or during electricity outages. These customers prefer single-phase generators over three-phase generators because of their simpler design and lower price.

The three-phase generators segment is anticipated to register a higher growth rate during the forecast period. This is due to the increasing number of industrial and large-scale commercial projects that require more powerful equipment. Three-phase generators are crucial for heavy-duty operations that are power-intensive in data centers, manufacturing plants, hospitals, and large construction sites. These sites provide three-phase power to efficiently operate large machines and other equipment. The development of more industries and backbone infrastructure will subsequently increase the need for high-power silent generators.

Type Analysis

Based on type, the segmentation includes portable and stationary. The stationary segment held the largest share in 2024. For functions that require sustained high power, such as hospitals, data centers, manufacturing facilities, and powerhouses, these generators work best because they are permanently installed. Their popularity stems from the expectation of a quiet, reliable, and continuous power supply during critical functions, while avoiding unsightly noise. It is common for stationary units to connect to a building’s central power supply and seamlessly switch to backup power during a blackout.

The portable segment is anticipated to register a higher growth rate during the forecast period. In addition to serving as backup power for residential houses, portable silent generators are also useful for recreational activities such as camping and tailgating. They can also be utilized as a supplied power for small-scale outdoor events, construction sites, and other professional functions. The portable units are becoming more popular as many small businesses and homeowners seek adaptable and affordable power solutions to counter rising levels of power outages. People living in remote areas and off-grid locations value these generators as they offer convenient and quiet power.

Source: Polaris Market Research Analysis

Fuel Type Analysis

Based on fuel type, the segmentation includes diesel, natural gas, and others. The diesel segment held the largest share in 2024. This is a result of the high power and efficiency outputs associated with diesel generators, making them a staple within the residential, commercial, and industrial markets. Since diesel generators can provide generators with energy for long periods of time, they are widely used in critical places such as data centers, manufacturing factories, and hospitals. Their ability to work in strenuous conditions provides longevity in both standby and continuous power.

The natural gas segment is anticipated to register the highest growth during the forecast period. This is a result of the increased focus on reducing emissions as well as the clean and renewable energy shift. Compared to diesel, natural gas burns cleaner and emits fewer pollutants, making it favorable in areas with poor air quality and in urban cities where these emissions are regulated. Natural gas, too, can be considered more practical, since it can be delivered without the need for on-site fuel storage equipment.

Key Players and Competitive Insights

The competition in the U.S. silent generators market comprises several important market participants along a value chain whose focus is a blend of product development, resourceful output, and niche demand servicing. For example, Generac Power Systems, Cummins Inc., and Caterpillar Inc. manufacture and sell a spectrum of equipment for domestic and industrial purposes. Honda and Kohler, conversely, focus on smaller portable generators for consumer and leisure applications. Competition in the market is based on product differentiation, pricing, customer after-sales service, and responsiveness to demand for more ecological and less noisy equipment. In addition, the development of hybrid and synthetic natural gas-powered equipment is a focus of the market participants.

A few prominent companies in the industry include Generac Holdings Inc., Cummins Inc., Caterpillar Inc., Kohler Co., Atlas Copco AB, Briggs & Stratton Corporation, Doosan Portable Power, Multiquip Inc., Wacker Neuson SE, and Yanmar Holdings Co., Ltd.

Key Players

- Atlas Copco AB

- Briggs & Stratton Corporation

- Caterpillar Inc.

- Cummins Inc.

- Doosan Portable Power

- Generac Holdings Inc.

- Honda Power Equipment

- Kohler Co.

- Multiquip Inc.

- Wacker Neuson SE

- Yanmar Holdings Co., Ltd.

Industry Developments

August 2025: Caterpillar and Joule announced an agreement to power Joule's data center in North Carolina.

U.S. Silent Generator Market Segmentation

By Sound Level Outlook (Revenue – USD Million, 2020–2034)

- Super Silent

- Silent

By Phase Outlook (Revenue – USD Million, 2020–2034)

- Single-Phase

- Three-Phase

By Type Outlook (Revenue – USD Million, 2020–2034)

- Portable

- Stationary

By Fuel Type Outlook (Revenue – USD Million, 2020–2034)

- Diesel

- Natural Gas

- Others

By End Use Outlook (Revenue – USD Million, 2020–2034)

- Residential

- Commercial

- Industrial

U.S. Silent Generator Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 0.96 million |

| Market Size in 2025 | USD 1.03 million |

| Revenue Forecast by 2034 | USD 1.85 million |

| CAGR | 6.8% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

U.S. Silent Generator Market FAQ's

The market size was valued at USD 0.96 million in 2024 and is projected to grow to USD 1.85 million by 2034.

The market is projected to register a CAGR of 6.8% during the forecast period.

A few key players in the market include Generac Holdings Inc., Cummins Inc., Caterpillar Inc., Kohler Co., Atlas Copco AB, Briggs & Stratton Corporation, Doosan Portable Power, Multiquip Inc., Wacker Neuson SE, and Yanmar Holdings Co., Ltd.

The silent segment accounted for a larger share of the market in 2024.

The single-phase segment is expected to witness a faster growth during the forecast period.

Download Sample Report of U.S. Silent Generator Market

Please fill out the form to request a customized copy of the research report.