Rutile Market Regional and Global Analysis with Growth Factors, 2026-2034

REPORT DETAILS

REPORT DETAILS

Rutile Market Overview

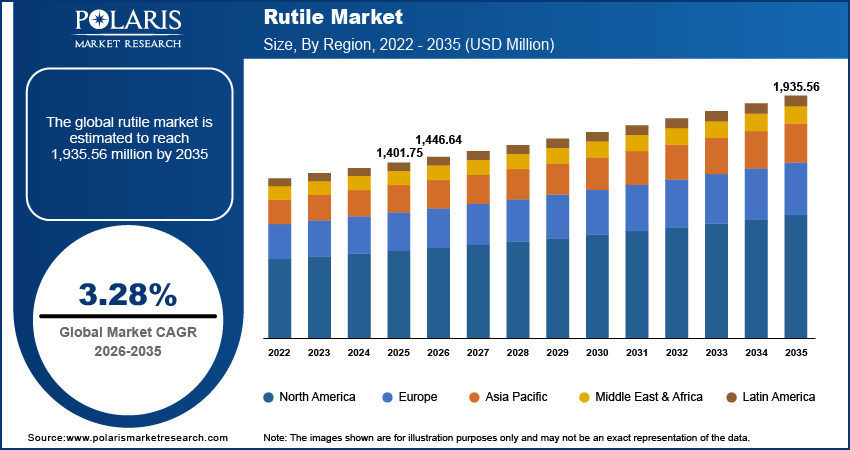

The global rutile market is estimated around USD 1.40 billion in 2025, with consistent growth anticipated during 2026–2034 at a CAGR of 3.28%. Due to the sustained increase in demand for TiO 2 pigments, welding consumable and high-end ceramics & electronics, the market is projected to grow at a moderate mid-single-digit CAGR during the forecast period.

Market Statistics

Key Takeaways

- The?Asia Pacific dominated the market in 2025 with 55.0% share, due to the burgeoning industrial demand from construction, automotive, packaging, and general manufacturing

- North America is?anticipated to witness the highest growth at a CAGR of 3.8%. This is due to the adoption of TiO? based products in advanced coatings, engineered polymer, welding applications, and specialty ceramics

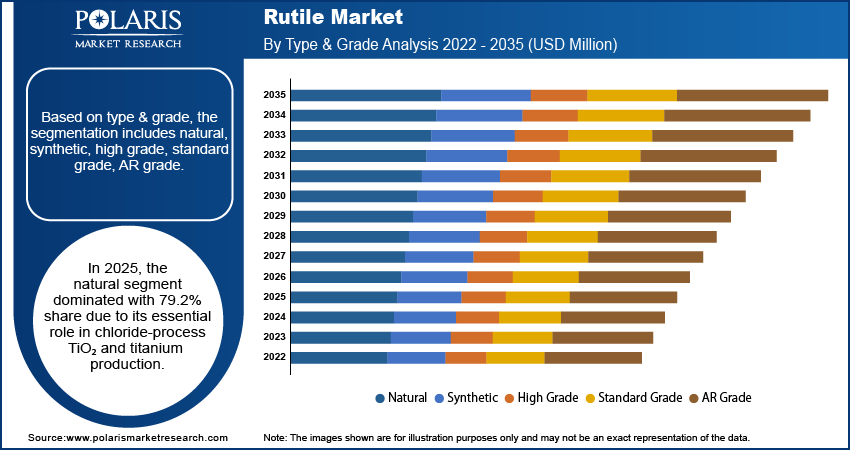

- The natural segment held the largest share of the market in 2025, with 79.2% of revenues due to their high titanium dioxide content and low levels of impurities.

- Ultra-high purity rutile accounted for 25.0% share in 2025, as it is vital for applications where material defects cannot be tolerated, serving as a base material in semiconductor substrates, precision optics, and next generation catalytic systems

- Paints & coatings segment dominated the market with 45.0% share in 2025. This application holds the major part of the rutile pigment market with majority of the?global production being consumed by it.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Future Demand Scenarios

- Base scenario: demand increases with output from construction, automotive and industrial sectors, as well as small improvements from high-purity applications.

- Upside scenario: more rapid penetration of chloride-route TiO2 in developing countries and further investments in high-end applications such as photocatalysis and semiconductor-grade rutile.

- Conservative scenario: downturn in construction and industrial activity, and deferral of new TiO₂ capacity.

Industry Dynamics

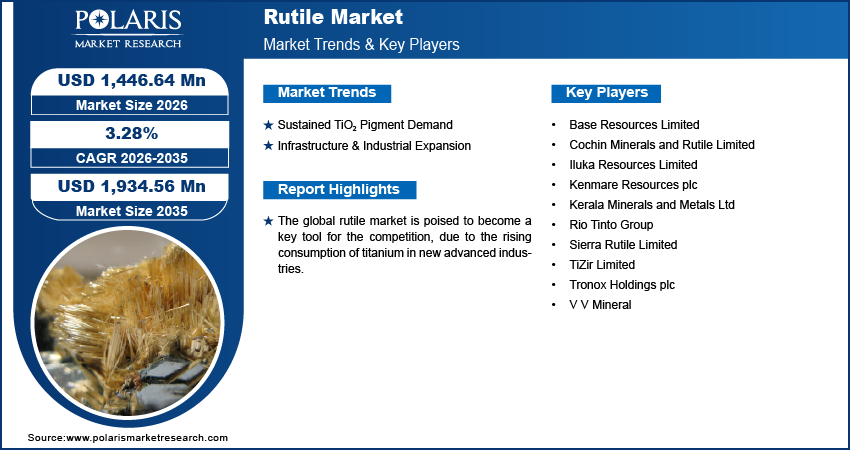

- Sustained TiO₂ pigment demand drives the market growth

- Infrastructure & industrial expansion boost the adoption of rutile

- Advanced ceramics, electronics & optics create opportunity to expand

- Environmental regulations and ESG pressures create challenges

What is Rutile and Why It Matters

Rutile is a natural TiO₂ of the highest quality. It is the indispensable raw material for the production of high-purity titanium metal and sparkling white pigments. Its high quality and low level of impurities make it the essential cost-effective raw material for a successful chloride process plant. Demand is driven by paints, plastics, aerospace and welding rods. Lock in this essential mineral to maintain quality, consistency, and a strong competitive position in the high-performance promise market growth.

Natural vs Synthetic Rutile – Key Differences

- The rutile industry is also a mining industry, as rutile is mined and separated from heavy minerals sand along with ilmenite and zircon from beach and inland deposits. This material is separated commercially as a co-product with ilmenite and zircon by physical separation techniques. Its major benefit is that it is naturally formed and, in many cases, exceptionally high titanium dioxide with low levels of impurities is delivered from the earth. This pattern of naturally occurring characteristics makes it the best choice as a feedstock for the most challenging applications, such as titanium metal and specialty chloride-process pigments. Thus, market fundamentals are tied into a handful of global mineral sands mining projects for produceable levels of zircon, titanium, and rare earth concentrates to supply the majority of off-take demand. For example, in 2023, global mine production of zirconium mineral concentrates rose to 1.6 Billion tons. Therefore, the supply chain is characterized as a finite, geographically concentrated one that is prone to disruptions triggered by the operational and political stability of critical producing regions.

- The synthetic rutile market is a fabricated market, developed to compensate the supply gap of its natural form. It involves the chemical processing of relatively low-grade ilmenite ore in a series of processes, such as the Becher or Benelite processes. These treatments enable the user to extract iron and other impurities, thereby increasing the titania content, under artificial conditions, to levels applicable to many industrial purposes. This segment of the market acts as an essential protector in the global titanium feedstock supply, delivering a scalable and tunable solution for the industry. Manufacturers are able to tailor their processes to the quality requirements, which adds flexibility for the users downstream. Furthermore, the viability of the synthetic rutile market would therefore be directly related to the cost effectiveness of these upgrading processes. Therefore, the price of the ilmenite ore that is based on the technological efficiency of these upgrading processes and the costs of sourcing further drives their growth.

Growing Strategic Importance in the Titanium Value Chain

In the titanium supply chain, the capture of high-purity rutile is a routine procurement activity and a strategic focus. This change is a reflection of the industry's overall trend towards more utilization of facilities, less waste and tighter environmental compliance. The best chloride-route titanium dioxide plants and the best titanium metal furnaces have been optimized to run at peak efficiency with certain, high quality feed materials. Suppose routinely reliable access to rutile that meets very high standards of purity and particle size is no longer simply a matter of supply security; it is now directly dependent on production cost, product quality, and environmental impact. As a result, the demand profile is becoming more complex and uneven, and the evaluation criteria are no longer based on quantity but on the precise technical attributes of the source, such as environmental, social, and governance (ESG) credentials. The consistent producer’s performance, trusted to deliver on both quality and responsibility, has become a powerful differentiator that protects customers from both technical and reputational risks.

Key Rutile Grades & Primary End-Uses

| Rutile / TiO₂ grade (indicative) | Product type (natural / synthetic / pigment) | Typical TiO₂ content range | Primary end-uses |

| Natural rutile concentrate | Natural rutile mineral concentrate | ~95–100% TiO₂ (natural TiO₂) | - Feedstock for TiO₂ pigment via chloride process (with other high-TiO₂ feedstocks). - Feedstock for titanium metal (via TiCl₄ and Kroll/Hunter processes). - Component of welding-rod coatings (as rutile mineral). |

| Synthetic rutile, 90–91% TiO₂ | Synthetic rutile | 90–90.5% TiO₂ (minimum, typical Indian SRP output). | - High-TiO₂ feedstock for chloride-route TiO₂ pigment plants. - Feedstock for TiCl₄ and titanium sponge/metal production. - Flux component in welding electrode coatings and special abrasives. |

| Synthetic rutile, 92–93% TiO₂ | Synthetic rutile | 92–93% TiO₂ (KMML synthetic rutile specification). | - Captive feedstock for rutile-grade TiO₂ pigment (chloride route). - Feedstock for titanium tetrachloride and sponge. |

| Synthetic rutile, 95% TiO₂ | Synthetic rutile (upgraded ilmenite) | ~95% TiO₂ (upgraded ilmenite / synthetic rutile). | - Export / merchant feedstock for TiO₂ pigment production (mainly chloride process). - Feedstock for TiCl₄ and titanium metal where high TiO₂ is required. |

| Synthetic rutile, 96.5% TiO₂ | High-grade synthetic rutile | ~96.5% TiO₂. | - High-grade feedstock for TiO₂ pigment plants (especially chloride route). - Feedstock for titanium metal and specialty applications requiring very high TiO₂. |

| Rutile-grade TiO₂ pigment (chloride process) | Finished pigment (rutile crystal form) | Commercial pigment-grade TiO₂ (surface-treated; produced to rutile crystal form). | - Outdoor and architectural paints and coatings (preferred over anatase due to better UV/weather resistance and lower reactivity with binders). - Plastics and rubber, including white plastics and films. - Paper, inks, roofing granules, ceramics, catalysts, textiles, floor coverings. |

The global rutile market is poised to become a key tool for the competition, due to the rising consumption of titanium in new advanced industries. New applications in additive manufacturing, aerospace alloys, and next generation electronics are putting unprecedented demand on high-purity titanium feedstock. Rutile's natural compatibility with the high efficiency chloride process makes it pivotal to cost and environmental performance. This report eliminates all the noise and delivers actionable intelligence on supply risk, the threat from synthetic rutile, and geopolitical dependence. Investors and strategist’s knowledge of the rutile supply chain is no longer optional. It is the source to securing margin and managing risk in the increasingly high-stakes advanced materials space.

Drivers & Opportunities

Sustained TiO₂ Pigment Demand

The expansion of rutile market size is witnessed on account of the increasing global demand for rutile-based feedstock for titanium dioxide pigments consumption. This reliance establishes a direct and strong correlation between the paints and coatings industry and rutile demand. The rising demand for highly long lasting and bright white pigments from worldwide growing construction activities, automotive production, and industrial maintenance is expected to boost market growth. Rutile TiO2 (chloride route) is the premium product in this sector and is produced by the efficient chloride process. According to a 2022 report from the Ministry of Mines, the production capacity for the TiO2 pigment production was estimated at 5.7 Billion tonnes per annum.

Furthermore, any increase in activities in the end-user sectors from new housing construction and infrastructure projects to the automotive original equipment and refinish markets means more demand for high-quality TiO2 production, which in turn requires a stable and dependable source of suitable rutile feedstock.

Infrastructure & Industrial Expansion

The demand for rutile is due to broad-based automotive and infrastructure development across a number of downstream products. Large scale construction, power generation, and opportunities in shipbuilding and heavy engineering also have an impact on the demand for welding electrodes. An April 2025 World Bank Group report, global infrastructure investment growth is forecasted to remain at 2.7% for 2025-26. Rutile is present in the coating of most electrodes and flux-cored wires used for welding and adds arc stability. This contributes to smooth slag formation and promotes a smooth, bright weld bead.

Hence, large-scale national infrastructure projects in emerging nations and maintenance plus growth in the industrial base of the developed world often lead to pronounced spikes in demand for rutile in welding applications. This industrial growth also creates need for specialized industrial coatings and refractory ceramics applied in high temperature environments, both of which employ rutile in a variety of applications.

Restraints & Challenges

Environmental Regulations and ESG Pressures

Stringent environmental regulations and ESG implications adversely affect the rutile market which restricts supply and raises cost of operation. It is more sensitive to tailings management, water use, land rehabilitation, community impact, and mineral sands mining on the environment. Stricter environmental standards and longer process of approval make capital requirements for green infrastructure more challenging and hold back greenfield projects and expansions at existing mine sites.

Business Impact:

- Profit: The income from energy is under margin pressure as the compliance costs and fines, if any, are passed to the producers and suppliers who may compensate for such cost by charging higher prices for feedstock.

- Supply: Regulatory barriers can result in supply bottlenecks, making the market tighter and more vulnerable to disruption.

- Pricing: Companies with weak ESG practices might suffer price discounts or lose contracts, and frontrunners might command price premiums.

Emerging Opportunities

Advanced Ceramics, Electronics & Optics

The exceptional advanced ceramics, optical lenses, and electronics properties of high purity rutile are opening up a wide range of new high-margin opportunities beyond conventional industrial applications. Rutile is employed in high-performance ceramic, electronic, and optical components, such as special purpose capacitors, optical lens coatings, and semiconductor substrates. The above applications of rutile indicate new specification driven premium demand.

Business Impact:

- Profit: These specialized segments have a higher margin per ton than pigment-grade food.

- Supply: Demand is increasing for ultra-high purity and defect-free material, which drives a separate supply chain evolved for it away from the bulk industrial feedstock.

- Pricing: Prices are disconnected from commodity TiO2 cycles and are rather derived from technical performance, resulting in stable, premium price levels for qualified producers.

Segmental Insights

This report provides granular coverage of the rutile market by type, grade, purity, particle size, application, and source, enabling readers to identify the fastest-growing and most profitable demand pockets.

By Type & Grade

-

-

Natural Rutile

-

The natural segment held the largest share of the market in 2025, valued at 79.2% of revenue. This is attributable to its indispensability as a key, high-quality raw material for the chloride-process titanium dioxide industry and the production of high-grade titanium metal. The natural product’s high titanium dioxide content and low levels of impurities provide both technical and economic benefits to the synthetic product for the most stringent applications. This established position in relatively critical, specification-driven supply chains means that a strain in its supply effects the largest volume/revenue share.

-

-

Synthetic Rutile

-

The synthetic segment is expected to witness the fastest growth at a CAGR of 3.6% during the forecast period. This is due to their scalable and strategic complement to limited natural supplies. Synthetic production based on plentiful ilmenite resources provides a stable, adjustable option, while high-quality titanium ore from conventional natural deposits is becoming shorter in supply and costly. Its growth is driven by continuous technological advancements in upgrading technologies that improve quality and cost of upgrading making it an attractive feedstock for applications in the rutile pigments industry.

- Grade Categories

-

High Grade:

-

The high-value, specialized end use markets include high-grade rutile for titanium metal and new applications in advanced electronics, and ultrafine rutile for high-grade coatings and catalysts, for which quality is a key factor in selection of material. For example, in the manufacturing of high-quality aerospace titanium metal, an alloy’s structural integrity and performance under extreme stress can only be assured by using very pure rutile with precisely controlled levels of trace elements.

-

-

Standard / General-Purpose Grade:

-

It is the essential base material for the rutile pigments market, and as the general-purpose rutile for welding electrodes in general construction and manufacturing worldwide, its consistent performance and its value for money are vital. For example, ordinary architectural paints and rutile for steel-welding electrodes are used in shipbuilding. Standard grade rutile offers an ideal combination of performance and economy, leading to very high demand volumes.

-

-

Low Grade / AR Grade:

-

It caters to the price-sensitive customers in which the minimum specification fulfilment is good enough. It finds application in lower performance ceramic and industrial coatings formulations, providing an option to the market of a lower cost feedstock. For example, in certain ceramic tile manufacturing, AR-grade rutile is incorporated as an opacifier in the glaze formulation when ultra-high brightness is not a critical focus for cost savings.

Type & Grade Segment Analysis

| Segment | Market Share Ranking | Fastest-Growing Indicator | Key Driver |

| Natural Rutile | High | No | Essential for chloride-process TiO₂ & titanium metal. |

| Synthetic Rutile | Medium | Yes | Scalable supply from ilmenite; tech improvements. |

| High Grade | Medium | Yes | Premium applications in metal, electronics, catalysts. |

| Standard Grade | High | No | Core pigment and welding electrode demand. |

| AR Grade | Low | No | Fills demand in cost-sensitive, low-spec markets. |

The report evaluates each grade by market size, share, growth rate, and indicative pricing differentials.

By Purity & Particle Size

-

Purity Levels:

- Ultra-high purity rutile:

This is the highest quality level in this market, characterized with titanium dioxide content >99.9% and ultra low trace elements. It is vital for applications where material defects cannot be tolerated, serving as a base material in semiconductor substrates, precision optics, and next generation catalytic systems.

-

- High purity rutile:

High purity rutile segment holds the largest market share valued at 25.0%, owing to its function as a premium and an industrial product. It is the essential raw material used in the production of high-grade rutile pigment market products. In automotive OEM coatings, the demand is for high durability and gloss. It is needed to manufacture high quality rutile for welding electrodes for use in critical pipeline and aerospace welding. This dual consistent demand from two high-value industries strengthens its position. For example, high gloss chip-resistant white paint for new cars can only be made using high purity rutile based TiO₂ to obtain the required brightness and durability.

-

- Medium & low purity:

This is for use in applications where “whiteness” and chemical purity are less important than functional performance and cost. It is used in industrial maintenance paints, some plastic masterbatches, and in the ceramic and refractory products of lower specifications, driven by the use of materials that falls short in some aspects of the requirements of the high end market.

-

Particle Size Segments:

- Ultrafine:

The high-performance coatings and specialized photocatalytic application for ultrafine rutile is designed to offer the highest surface area and efficiency in light-scattering, with a particle size in the sub-micron range. It is essential for high opacity in thin film coatings for electronics and automotive, and is the material of choice for next generation photocatalytic systems where reaction surface area is the key. Fueled by the ceaseless demand for smaller and better products in high-tech industries. s

-

- Fine & Medium:

This particle range constitute the major part of rutile pigments market. It is the perfect particle size to obtain the highest opacity and brightness in paints, plastics, and paper coatings. The demand is directly related to worldwide industrial output and consumer expenditure. Construction, automotive and packaging industry growth directly correlates to usage of the fine and medium pigments.

-

- Coarse:

Coarse rutile particles are tailored for use in applications where physical properties take precedence over pigment properties. This segment mainly used in rod coating with controlled particle size, since size influences the behavior of the flux and the stability of the arc. Fueled by global infrastructure spending and heavy industry activity. The demand for welding consumables is directly boosted by infrastructure projects, growth in energy pipeline systems, and shipbuilding and metal fabrication led by governments.

Purity & Particle Size Segment Analysis

| Segment | Market Share Ranking | Fastest-Growing Indicator | Key Driver |

| Ultra-High Purity | Low | Yes | Semiconductors, advanced optics, catalysis. |

| High Purity | High | No | Premium pigments, high-spec welding electrodes. |

| Medium & Low Purity | Medium | No | Industrial coatings, plastics, general ceramics. |

| Ultrafine Particle | Low | Yes | High-opacity coatings, photocatalytic systems. |

| Fine & Medium Particle | High | No | General rutile pigments market (paints, plastics, paper). |

| Coarse Particle | Medium | No | Rutile for welding electrodes, refractories. |

By Application

-

Paints & Coatings

This application holds the major part of the rutile pigment market with majority of the global production being consumed by it. The growth is attributed to the demand from construction, automotive OEM and industrial maintenance industries, as they rely on titanium dioxide for critical opacity, brightness and durability. For example, the bright and durable white finish on outside home siding is created using a rutile-based TiO₂ pigment.

-

Plastics & Paper

The consumption is driven by the influence of UV protection and bright white color in the consumer packing, automotive parts, and houseware. For example, white plastic food containers are formulated with rutile pigments to provide an opaque, clean look that shields contents from light-induced deterioration.

It serves as a coagulant and whitening agent in the manufacture of high-grade printing papers and specialty boards. The demand is related to high end packaging and publishing application, which requires higher whiteness and print fidelity. For example, rutile pigment is often added to the bright, smooth page of a luxury cosmetic box to enhance color reproduction and to give the box that sumptuous feel.

-

Welding Electrodes & Cutting Consumables

This sector is a consistent buyer of particular grades of rutile for welding electrodes. Demand is tied to infrastructure development globally, ship building, and pipeline projects, as rutile coated rods provide stable arc performance and a high-quality weld. For example, building a new natural gas pipeline takes rutile-coated welding electrodes by the ton to lay down strong, dependable seams.

-

Ceramics & Refractories

Applied to reinforce white color of ceramics glazes and enhance thermal stability in refractory coatings for kilns and furnaces. Its growth is tied to construction activity and industrial production. For example, rutile is used in the glaze to achieve the high gloss white surface of a ceramic sanitaryware product.

-

Electronics, Optics & Advanced Materials

This premium segment accounts for the majority of the demand for ultrafine rutile and high purity rutile. Growth is fueled by high-end applications in semiconductor substrates, optical coatings and photocatalytic systems, which require perfection in material properties.

Brief Example: A specialized optical lens for a semiconductor lithography machine may be coated with one based on high purity rutile for accuracy light handling.

Regional Analysis

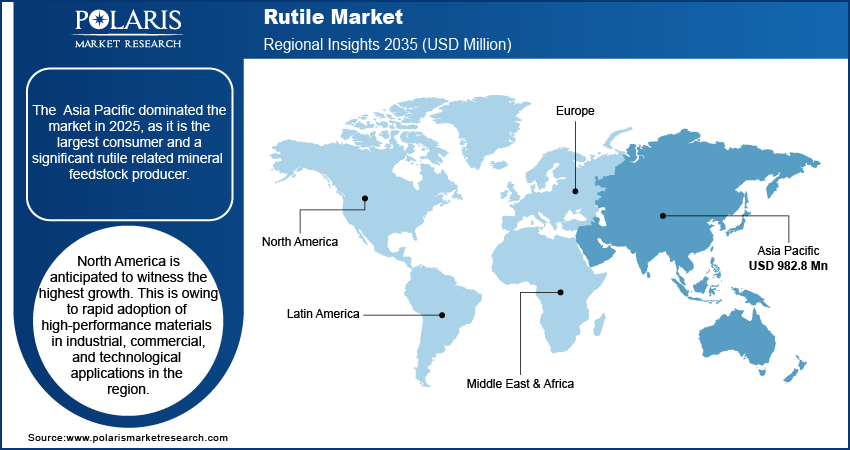

Asia Pacific Market Assessment

The Asia Pacific dominated the market with 55.0% share in 2025, as it is the largest consumer and a significant rutile related mineral feedstock producer. The region's burgeoning industrial demand from construction, automotive, packaging, and general manufacturing continues to be the major driver of titanium dioxide (TiO2) pigments, welding consumables, ceramics, and advanced materials. China as a domestic producer of TiO2 pigment builds up its internal supply chain rather than relying on imported feedstocks. Their demand is also driven by India and Southeast Asian countries with major infrastructure projects and expanded use of TiO2-based products in paints, plastics and coatings.

North America Rutile Market Insights

North America is anticipated to witness the highest growth at a CAGR of 3.8%. This is owing to rapid adoption of high-performance materials in industrial, commercial, and technological applications in the region. The adoption of TiO₂ based products in advanced coatings, engineered polymer, welding applications, and specialty ceramics is increasing in the region, supported by an established manufacturing system which emphasizes on quality, performance and sustainability. Increasing focus on material utilization and product innovation is driving the demand for higher grade of titanium feedstocks such as rutile.

Europe Rutile Market Overview

The Europe growth in the rutile market is attributed to its focus on regulatory compliance, product quality, and material sustainability for various end-use industries. The use of advanced TiO2 formulations and high-purity feedstocks to comply with ever-more stringent environmental and performance requirements is increasing in the region, particularly in the application fields of coatings, plastics and specialty chemicals production. This regulatory milieu spurs a persistent demand for rutile as an input material on account of its enhanced efficiency and reduced level of impurities, relative to other feed materials. Furthermore, rutile is utilized in high performance applications such as automotive coatings, engineered materials and high-performance ceramics, with these applications well established in Europe’s mature manufacturing base, where strength and reliability are key.

Heat Map Analysis

| Region | Demand Intensity | Production Strength | Industrial Consumption | Regulatory Influence | Growth Momentum |

| Asia Pacific | High | High | High | Medium | High |

| North America | Medium | Medium | High | High | Very High |

| Europe | Medium | Low–Medium | Medium–High | Very High | Medium |

Key Players & Competitive Analysis Report

The global rutile market is moderately consolidated with large, integrated mineral sand producers dominating. Competition is shaped by strategic shifting towards vertical integration and portfolio diversification in titanium feedstocks. Players such as Iluka Resources, Rio Tinto, and Tronox If these are well-endowed mining assets and they are a substantial proportion of premium natural rutile supply, the Also manufacture synthetic rutile and a number of coproducts including zicon. Competition in ESG and the supply of reliable, high-purity grades to chloride-process plants is also fierce. Regional experts like in West Africa's Sierra Rutile, serve particular regions, and there are a number of Indian producers. Strategic initiatives (including joint ventures) and capacity expansions in the resource-rich areas of Africa and Australia are focused on ensuring long-term supply of resource and to reduce the risks associated with supply in a highly regionalized production base.

Major companies operating in the rutile industry include Base Resources Limited, Cochin Minerals and Rutile Limited, Iluka Resources Limited, Kenmare Resources plc, Kerala Minerals and Metals Ltd, Rio Tinto Group, Sierra Rutile Limited, TiZir Limited, Tronox Holdings plc, and V V Mineral.

Key Players

- Base Resources Limited

- Cochin Minerals and Rutile Limited

- Iluka Resources Limited

- Kenmare Resources plc

- Kerala Minerals and Metals Ltd

- Rio Tinto Group

- Sierra Rutile Limited

- TiZir Limited

- Tronox Holdings plc

- V V Mineral

ESG & Technology Trends Shaping Future Demand

The technology seen in rutile market is expected to impact strongly on sustainable regulations. A pair of powerful macro trends are producing a wave of new demand and redefining competition.

Large Band Gap Semiconductor & Photocatalysis

In addition to conventional applications, high-purity rutile is increasingly used in advanced technology applications owing to its special electronic and optical characteristics. As a large band gap semiconductor, it currently is being investigated for use with next-generation sensors, UV photodetectors, and certain solar cell components. In photocatalysis rutile-based materials (nano) act as catalysts in light driven reactions with proven commercial applications in air/water purification systems and green hydrogen production. These applications advance rutile from a basic commodity to the specialty chemicals arena, whereby high-margin, technology-led demand could be created.

Mining and Community Impact Sustainability

ESG performance is a direct commercial differentiator. It downstream customers, in particular European and North American region, are increasingly requiring materials that have been sourced responsibly. Producers are making investments in dry-stack tailings management, water recycling and biodiversity plans to achieve a social license to operate. Good community relations and open reporting have become vital to winning project financing, permits and long-term offtake agreements with large TiO₂ producers. Being a leader on ESG gives producers pricing premiums and market access.

What to Watch Next

| Trend / Development | What to Monitor | Potential Market Impact |

| Commercial Scaling of Photocatalysis | Deployment of rutile-based reactors in industrial water/air purification. | Creation of a new, high-value demand segment for ultra-pure rutile. |

| ESG-Linked Financing | Growth of sustainability-linked loans & green bonds for mining projects. | Accelerated capital access for leaders; higher cost of capital for laggards. |

| Policy in Producing Nations | Changes to export or investment rules in Australia, Sierra Leone, Mozambique. | Increased supply chain volatility and potential for sudden trade flow disruptions. |

| Substitution & Process R&D | TiO₂ producer R&D into alternative feedstocks (e.g., upgraded ilmenite). | Long-term demand risk for standard-grade rutile if cost-effective alternatives emerge. |

| China's Chloride-Route Expansion | Pace of new chloride-process TiO₂ plant construction and feedstock sourcing. | Significant upside for premium rutile demand, tightening global supply. |

Industry Developments

- October 2025: Lion Rock Minerals secured USD 5.6 Billion in a share placement for its Minta project in Cameroon, with Tronox acquiring a 5% stake. The strategic partnership aims to advance drilling and resource definition at the rutile and monazite site. (Source: ecofinagency.com)

Rutile Market Segmentation

By Type & Grade Outlook (Revenue, USD Billion, 2021-2034)

- Type

- Natural

- Synthetic

- Grade

- High Grade

- Standard Grade

- AR Grade

By Purity & Particle Size Outlook (Revenue, USD Billion, 2021-2034)

- Purity Level

- Ultra-high purity rutile

- High purity rutil

- Medium & low purity

- Particle Size

- Ultrafine

- Fine & Medium

- Coarse

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Paints & Coatings

- Plastics

- Paper

- Welding Electrodes

- Ceramics/Refractories

- Electronics & Optics

By Source Outlook (Revenue, USD Billion, 2021-2034)

- Titanium Ore

- Ilmenite Ore

- Rutile Sand

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Rutile Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.40 Billion |

| Market Size in 2026 | USD 1.44 Billion |

| Revenue Forecast by 2034 | USD 1.87 Billion |

| CAGR | 3.28% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 1.40 billion in 2025 and is projected to grow to USD 1.87 billion by 2034.

The?Asia Pacific dominated the market in 2025 with 55.0% share, due to the burgeoning industrial demand from construction, automotive, packaging, and general manufacturing

Due to its high refractive index and strong opacity, rutile is mainly used for titanium metal production, pigment for paints, electrodes for welding, processing ceramics, optical instrument, and electronics.

A few of the key players in the market are Base Resources Limited, Cochin Minerals and Rutile Limited, Iluka Resources Limited, Kenmare Resources plc, Kerala Minerals and Metals Ltd, Rio Tinto Group, Sierra Rutile Limited, TiZir Limited, Tronox Holdings plc, and V V Mineral.

Key factors include sustained TiO pigment demand, infrastructure & industrial expansion, driven by paints, plastics, aerospace and welding rods, and rising consumption of titanium in new advanced industries.

Download Sample Report of Rutile Market

Please fill out the form to request a customized copy of the research report.