Simulators Market Insight & Growth Analysis, Global Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Simulators Market Summary

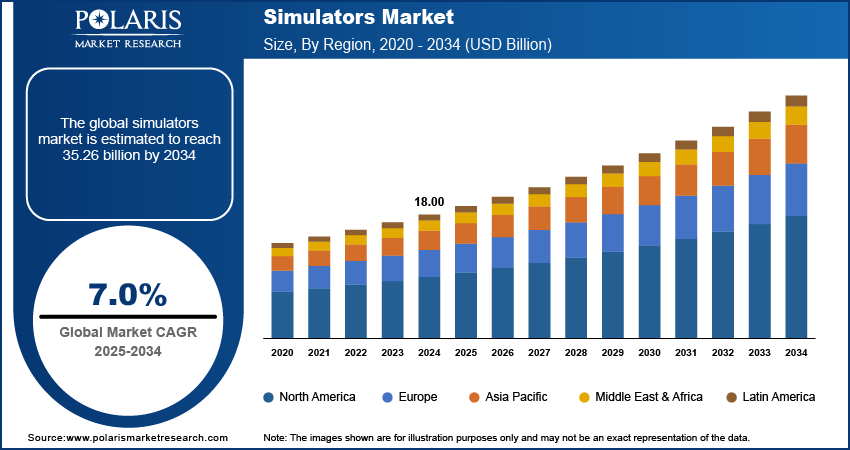

The global simulators market was valued at USD 19.23 billion in 2025, growing at a CAGR of 7.0% during the forecast period. The market growth is primarily driven by continuous advancements in technology and the presence of stringent environmental regulations across industries where risk mitigation is crucial.

Market Statistics

Key Takeaways

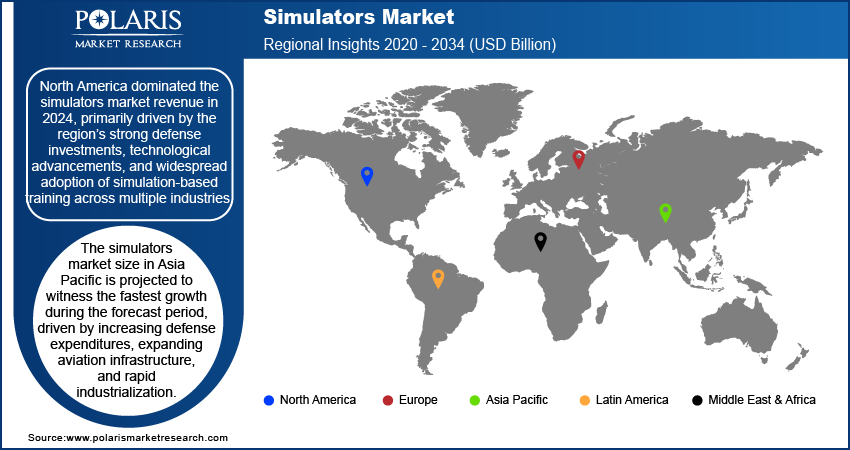

- North America dominated the global market with a 33.40% share in revenues in 2025. Advanced technology and high investment in the defense sectors lead to the market dominance of North America.

- The Asia Pacific region is expected to witness the highest CAGR of 7.60%. High industrialization rates and investment in defense expenditure support market growth.

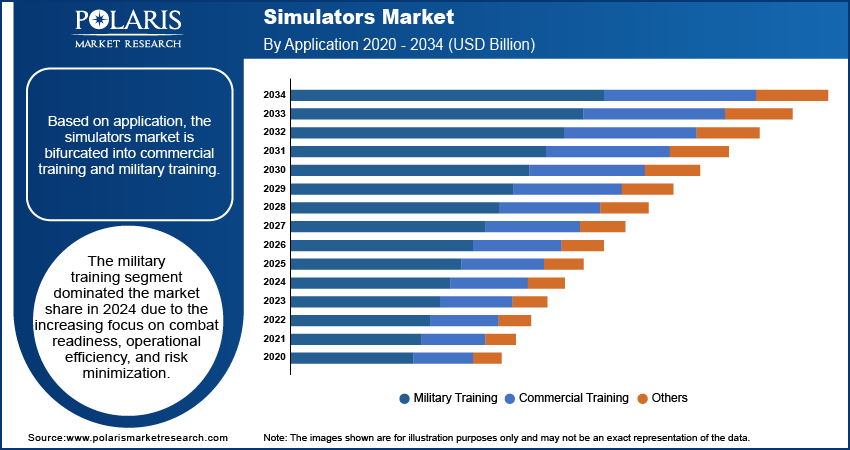

- Military training holds the largest market share of 50.10% in 2025. Higher emphasis on minimizing risks and improving efficiency supports the segment’s leading position.

- The maritime segment is expected to witness the highest growth rate of 7.90%. This is mainly due to increased usage of simulation technology in offshore and naval operations.

- Full flight simulators held a significant market share of 35.85% in 2025. This is due to high investments made in pilot training and an increase in air traffic.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The growing demand for realistic training solutions, which leverage advanced technologies to create highly accurate and immersive training environments, is fueling market expansion.

- Increased investments in advanced simulation centers globally to cater to the rising need for high-quality, accessible training facilities are boosting market development.

- Expanding applications of simulators beyond traditional sectors is expected to create several market opportunities.

- The high cost of gaming simulators may hinder market growth.

AI Impact on Simulators Market

- AI enhances simulators by embedding decision-making algorithms that mimic human reasoning. This allows trainees to practice in unpredictable, high-stress environments.

- AI identifies strengths, weaknesses, and error patterns by analyzing user performance data in real time.

- AI can autonomously generate new training scenarios instead of relying on pre-coded environments.

- AI-driven simulators provide safe environments to test autonomous vehicle systems, drones, and robotics before live deployment.

Simulators are advanced systems that replicate real-world environments to train individuals, test equipment, and improve operational efficiency across various industries. The simulators market growth is attributed to continuous technological advancements. Innovations such as AI-driven analytics, virtual reality (VR), and augmented reality (AR) are revolutionizing the realism and interactivity of simulations, making them more effective for training and analysis. In December 2024, EON Reality launched EON-XR 10.6, featuring a Knowledge Simulator and AI-driven tools to transform immersive learning content creation, practice, and assessment in AI-assisted VR/AR knowledge transfer for industry and education. The integration of high-fidelity graphics, haptic feedback, and cloud-based simulation platforms has further expanded their applicability in the aviation, healthcare, defense, and automotive sectors. These advancements improve training effectiveness and also reduce operational risks and costs, improving the overall simulators market demand.

The simulators market development is influenced by strict safety regulations across industries where precision and risk mitigation are critical. In February 2025, NISC highlighted its use of the open-source Network Simulator 3 (ns-3) for public safety research, releasing modules for ProSe, MCPTT, UAV energy models, and a visualization tool. Market players are signing collaborations with universities to improve simulation capabilities for mission-critical communications. In sectors such as aerospace, healthcare, and defense, regulatory bodies minimize rigid training and assessment procedures, making simulation-based training an essential compliance requirement. Simulators provide a controlled and repeatable environment for personnel to develop expertise while ensuring compliance with safety protocols without real-world consequences. This regulatory-driven demand reinforces the adoption of simulation technologies, positioning them as essential tools for improving skill development and operational safety across multiple industries.

Market Dynamics

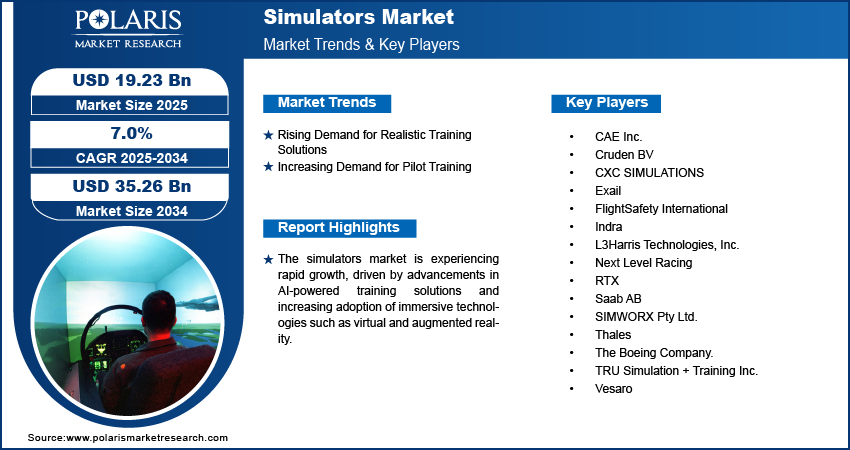

Rising Demand for Realistic Training Solutions

Traditional training methods often fall short in replicating real-world complexities, making high-fidelity simulation technology essential for improving decision-making and response times in critical environments. Advanced simulators leverage advanced technologies such as artificial intelligence, virtual reality, and real-time data processing to create highly immersive and accurate training environments as industries increasingly prioritize hands-on, experiential learning to enhance skill development and operational efficiency. This trend is further supported by strategic collaborations aimed at advancing simulation capabilities across industries. In February 2025, Zen Technologies Limited collaborated with TXT Group to develop advanced pilot training solutions, combining Zen’s simulation expertise with TXT’s aerospace software capabilities to deliver cost-effective, innovative aviation simulators for global markets. This enables professionals in the aviation, defense, healthcare, and automotive sectors to gain practical experience without exposure to real-world risks. Thus, as industries focus on enhancing workforce competency and operational preparedness, the demand for realistic training solutions continues to drive the simulators market growth.

Increasing Demand for Pilot Training

Airlines and defense organizations require advanced training solutions to ensure pilot proficiency and operational safety with expanding global air travel and fleet modernization initiatives. The growing demand for high-quality, accessible training facilities has led to significant investments in state-of-the-art simulation centers worldwide. In October 2023, Simaero announced the opening of a state-of-the-art Training Center in Delhi, featuring eight simulator bays with A320, B737 Max, and ATR 72-600 devices to meet the growing demand for pilot training in India. Simulators provide a cost-effective and risk-free environment for pilots to develop critical skills, practice emergency procedures, and adapt to complex flight scenarios without real-world consequences. The integration of high-fidelity graphics film, artificial intelligence, and real-time scenario modeling further improves the effectiveness of simulation-based training. As aviation regulations continue to emphasize stringent training standards, the adoption of flight simulators remains essential for maintaining safety, compliance, and operational efficiency. Therefore, the rising demand for pilot training boosts the simulators market development.

Flight vs Driving vs Medical vs Military Simulators

| Simulator | Primary Use | Important Characteristics | Industries | Advantage |

| Flight Simulator | Pilot training | Realism in cockpit, realistic flight dynamics, training for emergencies | Aeronautics, military | Training pilots safely without the risk of flying |

| Driving Simulator | Driver training | Environment like roads, various traffic situations, weather simulation | Vehicle manufacturers, logistics | Enhancing driving ability and lowering the risk of accidents |

| Medical Simulator | Surgical and medical procedures training | Human replica, surgery procedure simulation, patient responses simulation | Medicine, health care | Learning surgical procedures safely |

| Military Simulator | Training for combat operations and missions | Scenarios of war, weapons simulations, tactical training | Defense force, military | Tactical decision making and preparation for missions |

Segment Insights

Assessment by Application Outlook

The global simulators market segmentation, based on application, includes commercial training, military training, and others. The military training segment dominated the simulators market share in 2025 due to the increasing focus on combat readiness, operational efficiency, and risk minimization. Defense organizations worldwide are prioritizing advanced simulation-based training programs to improve personnel proficiency in complex and high-risk scenarios. Military simulators provide realistic battlefield environments, allowing soldiers, pilots, and naval officers to develop tactical skills without live combat exposure. The integration of artificial intelligence, virtual reality, and real-time scenario replication further improves training effectiveness while reducing costs associated with live exercises. Therefore, as defense agencies continue to invest in modernizing training infrastructure, the demand for high-fidelity military simulators remains a key driver of simulators market growth.

Evaluation by Platform Outlook

The global simulators market segmentation, based on platform, includes airborne, land, and maritime. The maritime segment is expected to witness the highest growth rate during the forecast period due to the rising adoption of simulation technologies for naval operations, commercial shipping, and offshore industries. There is a growing need for advanced training solutions to improve navigational skills, emergency response, and vessel operation efficiency with increasing global maritime trade and strict safety regulations. Maritime simulators provide a controlled environment for training ship crews, naval officers, and port operators, allowing them to handle real-world challenges such as adverse weather conditions and emergencies. The integration of high-fidelity simulation models, augmented reality, and AI-driven analytics is further driving the adoption of maritime simulators, resulting in the simulators market expansion.

Advanced Simulation Trends

Virtual and Augmented Reality Simulators: These simulators are capable of designing training environments that simulate real-life situations. They enhance the learning process and make training safer across sectors such as aviation, health care, and defense.

Use of Artificial Intelligence for Simulation: Artificial intelligence technology could be effectively used to increase the efficiency of simulator work. This is achieved through adaptive simulation design and real-time response, which depends on actions and decisions made by users.

Cloud Computing for Simulation: Cloud computing makes it possible to hold online training sessions without using any specific hardware for simulation program operation and also discussing results in real time.

Real-Time Analytics in Simulations: Real-time analytics monitor the performance of trainees and help identify errors immediately

Regional Analysis

By region, the report provides the simulators market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the simulators market share in 2025, primarily driven by the region’s strong defense investments, technological advancements, and widespread adoption of simulation-based training across multiple industries. The presence of key market players, along with continuous innovation in simulation technologies, has contributed to the region’s leadership in this sector. The defense sector remains a major contributor, with government agencies investing heavily in next-generation training systems to enhance military preparedness. These investments are exemplified by high-value contracts aimed at modernizing defense capabilities. In January 2025, Lockheed Martin received a USD 270 million contract with the US Air Force to integrate advanced TacIRST sensors into the F-22 Raptor, enhancing its infrared threat detection and countermeasure capabilities through the Infrared Defensive System (IRDS). Additionally, the commercial aviation, healthcare, and automotive industries in North America are increasingly leveraging simulators to improve operational efficiency and safety standards. This well-established ecosystem of technological innovation and industry-wide adoption has reinforced North America’s position as the leading revenue contributor in the global simulators market revenue.

The Asia Pacific simulators market is projected to witness the fastest growth during the forecast period, driven by increasing defense expenditures, expanding aviation infrastructure, and rapid industrialization. Governments of the region are actively investing in simulation-based training programs to enhance military capabilities and support the growing commercial aviation sector. In November 2024, The Indian Air Force launched a C-295 Full Motion Simulator at Air Force Station Agra in November 2024. This advanced facility enables realistic mission training and emergency scenario practice, reducing actual flight hours while supporting India's self-reliant aerospace manufacturing initiative through domestic C-295 production. Additionally, advancements in healthcare, automotive, and maritime industries are driving demand for high-fidelity simulators to improve workforce training and operational efficiency. The rise of smart city initiatives, technological innovation, and the integration of virtual reality and artificial intelligence further contribute to the region’s expanding adoption of simulation technologies. As Asia Pacific continues to prioritize digital transformation and industry modernization, the simulators market demand is expected to grow at an accelerated pace during the forecast period.

Key Players & Competitive Analysis Report

The competitive landscape comprises global leaders and regional players aiming to capture significant simulators market share through technological innovation, strategic collaborations, and regional expansion. Industry leaders such as CAE Inc., L3Harris Technologies, Thales Group, and others leverage strong R&D capabilities and extensive distribution networks to deliver advanced simulation systems across aviation, defense, healthcare, and industrial training applications. Simulators market trends indicate rising demand for high-fidelity training solutions, such as AI-driven simulators, virtual reality (VR)-based training modules, and cloud-based simulation platforms, reflecting advancements in immersive learning and operational readiness. The simulators market is projected to experience significant growth, fueled by increasing demand for cost-effective training, strict safety regulations, and advancements in AI and real-time analytics. Regional players focus on localized requirements by offering tailored and affordable simulation solutions, particularly in emerging markets. Simulators market competitive strategies include mergers and acquisitions, partnerships with defense and commercial training institutions, and the development of next-generation simulation technologies to meet the growing need for enhanced training efficiency and risk mitigation. These factors highlight the critical role of technological advancements, regulatory compliance, and regional investments in driving the expansion of the global simulators market. A few key major players are CAE Inc.; Cruden BV; CXC SIMULATIONS; Exail; FlightSafety International; Indra; L3Harris Technologies, Inc.; Next Level Racing; RTX; Saab AB; SIMWORX Pty Ltd.; Thales; The Boeing Company; TRU Simulation + Training Inc.; and Vesaro.

The Boeing Company, founded in 1916 by William E. Boeing, is an American multinational corporation specializing in aerospace. Headquartered in Arlington, Virginia, Boeing operates through three main divisions: Boeing Commercial Airplanes; Boeing Defense, Space & Security; and Boeing Global Services. The company designs and manufactures a wide range of products, such as commercial jetliners, military aircraft, rotorcraft, satellites, and defense systems, serving customers in over 150 countries. Boeing is recognized as the largest aerospace manufacturer and a leading defense contractor in the world. In addition to its manufacturing capabilities, Boeing invests heavily in simulation technology to enhance training and operational efficiency. The company offers advanced flight simulators that replicate real-world flying conditions for pilot training and aircraft testing. These simulators are integral to ensuring safety and proficiency among pilots and crew members, allowing for realistic practice without the risks associated with actual flight. Boeing's commitment to innovation and sustainability positions it at the forefront of the aerospace industry, continually adapting to meet emerging challenges and customer needs.

L3Harris Technologies, Inc. is an American aerospace and defense technology company formed through the merger of L3 Technologies and Harris Corporation in June 2019. The company specializes in a wide range of products and services, such as command and control systems, tactical radios, avionics, night vision equipment, and intelligence, surveillance, and reconnaissance (ISR) systems. L3Harris serves customers across government, defense, and commercial sectors in more than 100 countries with ∼USD 18 billion in annual revenue and around 48,000 employees. One of the key areas of expertise for L3Harris is its development of simulators and training devices designed for both military and commercial applications. These simulators play a crucial role in preparing personnel for real-world scenarios by providing realistic training environments. They encompass various domains, including aviation training systems, such as the Predator and Reaper Mission Aircrew Training System (PMATS), which has trained thousands of aircrew members annually. The company's commitment to innovation ensures that these simulators integrate advanced technologies to meet the evolving needs of its clients, thereby enhancing operational readiness and effectiveness in complex mission environments.

List of Key Companies

- CAE Inc.

- Cruden BV

- CXC SIMULATIONS

- Exail

- FlightSafety International

- Indra

- L3Harris Technologies, Inc.

- Next Level Racing

- RTX

- Saab AB

- SIMWORX Pty Ltd.

- Thales

- The Boeing Company.

- TRU Simulation + Training Inc.

- Vesaro

Simulators Industry Development

April 2026: CAE Simulation Training Private Limited (CSTPL), a joint venture between CAE and InterGlobe Enterprises, announced the opening of its fourth pilot training academy in India. This 44,000-square-foot facility has been opened in Mumbai to assist India's growing aviation industry. (source: prnewswire.com)

October 2025: Exail revealed the delivery of two EF-Truck driving simulators to the French Ministry of the Armed Forces for the Operational Energy Service (SEO). The company stated that these simulators will enable military drivers to prepare for complex and multi-domain scenarios. (source: exail.com)

Simulators Market Segmentation

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Commercial Training

- Military Training

- Others

By Solution Outlook (Revenue, USD Billion, 2021–2034)

- Products

- Services

By Platform Outlook (Revenue, USD Billion, 2021–2034)

- Airborne

- Land

- Maritime

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Full Flight Simulators

- Flight Training Devices

- Other

By Technique Outlook (Revenue, USD Billion, 2021–2034)

- Live

- Virtual & Constructive Simulation

- Synthetic Environment Simulation

- Gaming Simulation

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Simulators Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 19.23 billion |

| Market Size Value in 2026 | USD 20.57 billion |

| Revenue Forecast by 2034 | USD 35.26 billion |

| CAGR | 7.0% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global simulators market size was valued at USD 19.23 billion in 2025 and is projected to grow to USD 35.26 billion by 2034.

The global market is projected to register a CAGR of 7.0% during the forecast period.

North America dominated the market revenue share in 2025

A few of the key players in the market are CAE Inc.; Cruden BV; CXC SIMULATIONS; Exail; FlightSafety International; Indra; L3Harris Technologies, Inc.; Next Level Racing; RTX; Saab AB; SIMWORX Pty Ltd.; Thales; The Boeing Company; TRU Simulation + Training Inc.; and Vesaro.

The military training segment dominated the market share in 2025.

A simulator is a device that creates an environment or situation similar to reality to train, test, and analyze without putting oneself at risk in reality.

There are several types of simulators. These include flight simulators, driving simulators, medical simulators, military simulators, and industrial training simulators.

They are needed for training staff, testing machines, improving decision-making skills, and analyzing performance.

Download Sample Report of Simulators Market

Please fill out the form to request a customized copy of the research report.