Commercial Printing Market Share, Size, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

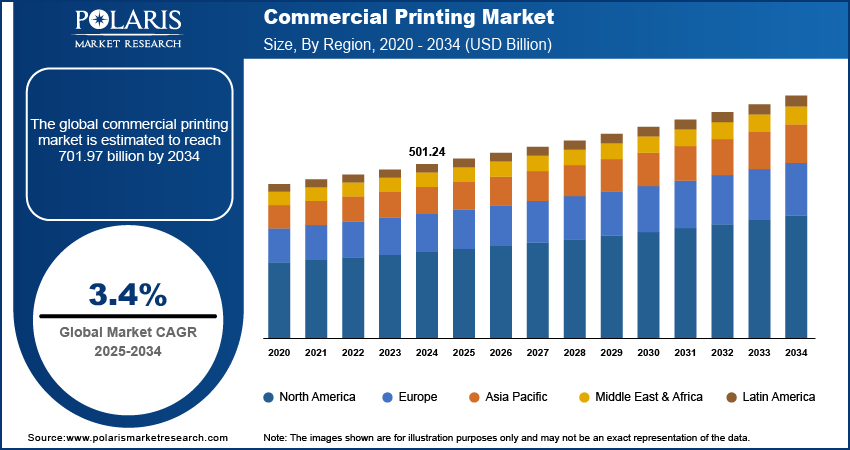

Commercial Printing Market Summary

The global commercial printing market was valued at USD 514.80 billion in 2025 and is expected to grow at a CAGR of 2.6% during the forecast period. The growth is driven by rising demand for commercial printing services as businesses and industries need more promotional materials, such as brochures and booklets.

Market Statistics

Key Takeaways

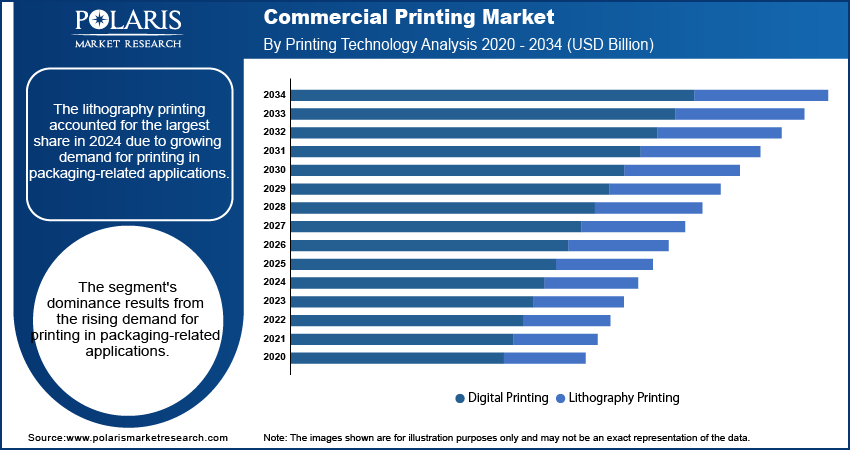

- Lithographic printing accounted for the largest share in 2025, driven by growing demand in packaging applications.

- The advertising segment is expected to grow significantly due to the legal requirement to print packaging on goods.

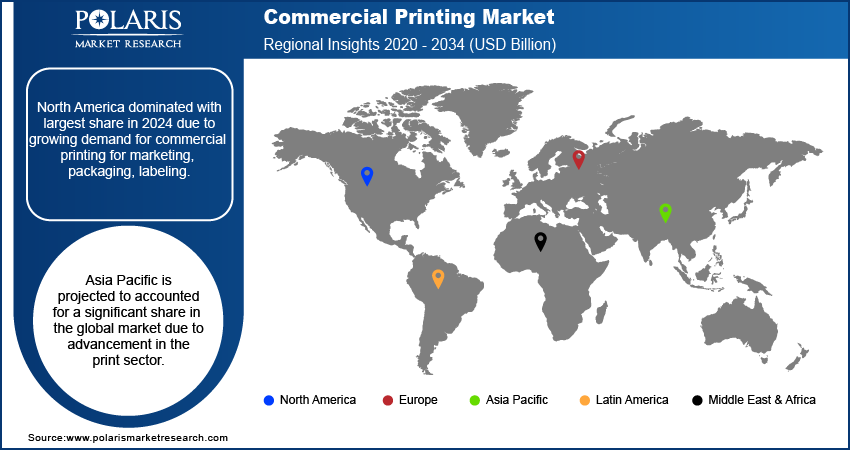

- North America dominated with the largest share in 2025 due to growing demand for commercial printing for marketing, packaging, and labeling.

- Asia Pacific is projected to account for a significant share of the global market, driven by advancements in the print sector.

The overview of the commercial printing industry mentioned above encompasses professional printing services in prepress, printing, and finishing. It also encompasses products such as marketing collateral, publications, labels, and packaging components. The market scope varies by source: some include packaging-related printing in commercial printing, while others treat it as a distinct market.

Industry Dynamics

- The growth of e-commerce is increasing demand for commercial printing and packaging labeling, thereby fueling further growth.

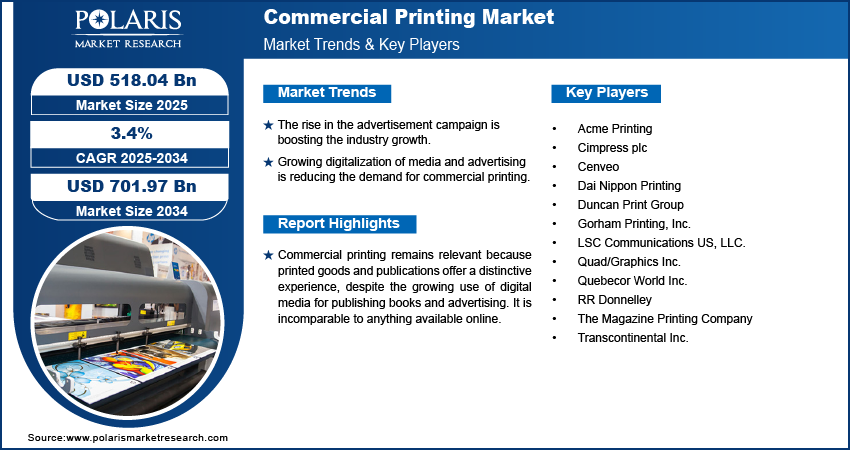

- The rise in the advertisement campaign is boosting the industry growth.

- Technological advancement is driving the growth.

- E-commerce growth supports packaging and labeling printing, while digitization reduces traditional publication volumes. On the other hand, print-on-demand, variable-data printing, and Web-to-Print solutions create new opportunities for growth.

- One major limiting factor in the printing industry is the rise of digital media, which reduces the need for printing.

Method Note:

This forecast uses 2025 as the base year, with R&D projections covering the 2026–2034 period. The commercial printing industry is driven by revenues from advertising, marketing, transactional, and digital print, as well as select packaging-related commercial print (such as labels and folding cartons) produced through commercial printing. The industry is not driven by industrial packaging, bulk corrugated packaging, or in-house business printing. Divergences in the magnitude of the market or the CAGR for publishers may be due to differences in the base year, the scope of the categories, or the length of the time frame.

Source: Polaris Market Research Analysis

The e-commerce industry is expanding globally as smartphone penetration and internet access grow in both urban and rural areas. According to the U.S. Census Bureau, retail e-commerce sales in the U.S. alone were USD 304.2 billion in the second quarter of 2025, an increase of 1.4% from the first quarter. This growth in e-commerce sales is driving demand for printing, packaging, and labelling, which, in turn, is fueling demand for commercial printing. Furthermore, expanding the quick commerce sector in countries such as India is fueling demand for creative packaging, which in turn drives commercial printing and industry growth.

The growing adoption of smartphones and omnichannel retailing is driving demand for e-commerce packaging printing. This includes labels, stickers, inserts, and unboxing materials. Consequently, the trends in commercial printing are becoming increasingly linked to packaging print demand, particularly in high-frequency delivery models such as quick commerce.

Commercial printing remains relevant because printed goods and publications offer a distinctive experience, despite the growing use of digital media for publishing books and advertising. It is incomparable to anything available online. Regular book and magazine readers prefer printed publications to online ones because physical books enhance the experience. Users also benefit from printed books, such as easier reading.

New practical aspect: In addition to publications, commercial printing also supports compliance and brand success. This involves packaging elements, point-of-sale materials, product manuals, catalogs, and direct mail. Personalized and variable data printing allows for targeted marketing and integrates print media with digital experiences via QR codes and trackable URLs.

Source: Polaris Market Research Analysis

Industry Dynamics

Growth Drivers

The demand for prints in the developing regions, such as Asia Pacific and Latin America, is rising. This rise in demand is driven by urbanization and rising literacy rates. This rise in urbanization and literacy is boosting demand for brochures, manuals, catalogs, and other commercial publications, which in turn is fueling demand for commercial printing. Moreover, the expansion of the urban infrastructure in developing countries such as India, Mexico, and Vietnam is boosting the number of showrooms and shopping malls. This rise in showrooms and shopping malls is further driving demand for catalogs and advertising boards. Consequently, boosting demand for commercial printing drives industry growth.

These drivers are accelerating investments in faster turnaround digital printing, scalable offset printing, and automated finishing. Printers are upgrading capacity to handle shorter lead times and higher volumes. This shift helps meet the growing demand for catalogs, signage, and packaging-related collateral across the Asia Pacific commercial printing market and Latin America.

What is the Impact of Artificial Intelligence (AI) and Automation on the Commercial Printing Market?

The adoption of AI and automation technologies is influencing the commercial printing market. It is positively impacting cost structure and product customization. There is a rapid shift from volume-based production toward personalization and data-driven operations. The market is moving toward smarter and more sustainable printing solutions. Companies adopting AI and automation are better positioned to gain emerging opportunities. The technologies streamline operations, enhance customization, and enhance overall productivity. The following table provides the benefits and challenges of AI and automation in the commercial printing process.

AI applications exist in traditional commercial offset presses. AI in prepress helps optimize layout and imposition. AI quality control press allows real-time defect detection. Press predictive maintenance reduces press downtime. Press job scheduling and print workflow automation improve press turnaround time. All these developments help deliver print-on-demand operations more quickly.

| Printing Segment | AI and Automation Impact | Benefits | Challenges |

| Packaging Printing |

| Faster production, consistent quality | Requirement for high initial investments in automated packaging lines |

| Labels and Stickers |

| Precise cutting, reduced errors | Complex integration with legacy label printing systems |

| Large-Format Printing |

| High-quality prints, optimized machine usage, reduced wastage | Requirement for skilled operators for advanced machinery |

| Textile Printing |

| Shorter lead times, reduced material waste, and customizable prints | High equipment cost, requirement for specialized maintenance |

| Advertising and Marketing |

| Personalized campaigns, faster content adaptation, improved customer engagement | Integration with digital marketing tools, data privacy compliance |

| Publishing |

| Faster production cycles, reduced labor dependency, reduced errors | Limited flexibility for artistic or niche printing |

| Print-on-Demand Services |

| Reduced inventory and waste, just-in-time production | Requirement for investments in software platforms and real-time monitoring |

Source: Polaris Market Research Analysis

Report Segmentation

By Substrate / Print Medium

The paper and paperboard segment dominated the commercial printing market due to their widespread use in brochures, catalogs, books, and packaging collateral. Plastics and films were showing steady growth driven by demand for labels, flexible packaging, and promotional materials. Textile printing is poised to be more widely utilized in signage and branded merchandise. Metals and other substrates were valuable substrates used in specialty and decorative printing applications. An expanding range of substrates encourages printers to adopt digital, offset, and flexographic printing technologies that support the production of a variety of materials.

By Service Type

The printing service category is the leading segment, powered by ongoing demand for large-format printing and shorter-run jobs. Design and prepress services continue to expand, reflecting growing demand for customized designs and quick setup for new jobs. Finishing and bindery services also become more relevant as companies emphasize high-quality appearance and longevity. Fulfillment and distribution services also rise, reflecting growing demand for e-commerce printing and the need for on-demand printing services. The inclusion of services in this category underscores a shift in commercial printing beyond mere production.

By Printing Technology

The lithography printing segment dominated the market. The segment's dominance stems from rising demand for printing in packaging applications. Lithography technology offers several benefits, such as consistent, high-quality images, which encourage greater adoption. Lithographic printing is perfect for high-volume static mailings, such as directories and product advertising. Flexographic technology is among the most popular.

Lithography (commonly referred to as offset printing) is the primary process for high-volume, high-quality printing of commercial and related packaging when economies of scale are favored. However, flexographic and gravure printing are also widely used for high-volume packaging jobs, such as labels and flexible packs, due to the processes' fast, efficient nature.

The digital printing segment is anticipated to record the fastest CAGR. Due to their cost-effectiveness and flexibility, inkjet and laser printing solutions have been quickly adopted by the paper and packaging printing industry. The category is also expected to be driven by the uptake of Internet of Things (IoT) and artificial intelligence (AI) technologies. Because digital printing offers lower prices for color printing and a better return on investment, it is frequently used in printing operations.

Digital inkjet printing is finding application in short-run packaging and labels, as well as in variable campaigns, whereas toner-based printing solutions cater to fast commercial print jobs. The printing technologies discussed are complemented by personnel and other variables that impact commercial printing industry trends.

Advertising Segment is Expected to Witness Significant Growth

The advertising segment is expected to grow significantly during the forecast period due to rising demand for attractive brand promotions. Companies worldwide are focusing on creative brand campaigns to attract younger audiences. This creative brand campaign is increasing the packaging and promotional board needs that align with the brand campaigns, driving demand for commercial printing in advertising applications. Moreover, advancements in digital printing are making advertisement printing more efficient and cost-effective. This cost-effectiveness is fueling the adoption, thereby driving the segment growth.

The regulatory aspect mostly drives demand for printing and labeling, whereas advertising follows experience marketing, point-of-sale printing, and retail activations. Digital printing capability upgrades are expanding campaign-driven commercials, hence influencing faster turnaround times through automation.

Source: Polaris Market Research Analysis

Regional Analysis

Demand in Asia Pacific is Expected to Witness Significant Growth

Asia Pacific is anticipated to develop at the highest CAGR over the forecast period. Advancements in the print sector, notably digital technologies, are driving regional expansion, particularly in China and India. Due to these advancements' high-speed capabilities, conventional printers have been supplanted by high-tech commercial printers. Along with supporting the target market, the region's e-commerce boom and the organization of the retail sector offer tremendous opportunities for packaging expansion, further driving demand for commercial printing.

The growth of the Asia Pacific commercial printing market is rapidly linked to quick commerce packaging cycles, Local SKU proliferation, and greater acceptance of web-to-print solutions to better manage order, proof, and fulfillment processes, especially for small and large retailers.

In 2024, North America dominated the market share. The rising demand for commercial printing for marketing, packaging, labeling, and advertising is fueling a regional boom. Additionally, it is projected that the presence of essential firms in the area, like Quad/Graphics Inc., Acme Printing, Cenevo, and RR Donnelley, will further spur the industry's expansion. Furthermore, the presence of major e-commerce players such as Amazon, Walmart, and eBay is fueling demand for creative packaging, thereby boosting commercial printing in the region.

Buyers in North America are increasingly likely to compare commercial printing suppliers based on their capabilities in workflow automation, sustainability, and turnaround. These needs have triggered demands for an upgraded press fleet.

Source: Polaris Market Research Analysis

Competitive Insight

The competitive environment is characterized by large firms that can service an entire country and invest in automation, while others are specialists in packaging, labels, or high-end finishing, which explains why different commercial printing firms cater to different markets.

Some of the major players operating in the global market include Quad/Graphics Inc., Acme Printing, Cenveo, RR Donnelley, Transcontinental Inc., LSC Communications US, LLC., Gorham Printing, Inc., Dai Nippon Printing, The Magazine Printing Company, Cimpress plc, Quebecor World Inc., and Duncan Print Group.

Recent Developments

- December 2025: Page Bros Group announced the acquisition of BDH Tullford, also known as BD&H, a specialist in printed point-of-sale displays and signage. The deal merges BD&H’s retail graphics expertise with Page Bros’ commercial print and fulfillment services, strengthening its ability to deliver branded POS, wide-format printing, and signage solutions.

- June 2025: RRD also announced a multi-million-dollar digital investment in its Austell, GA facility, including an HP Indigo 120K Digital Press, a PageWide Advantage 2200 system, and its very first fully robotic handling line. This newest round of investment will accelerate the automation of the digital press and robotic handling, enabling RRD to better meet high-volume variable print-on-demand throughput while reducing unit costs.

- April 2025: TOPPAN Holdings completed its buyout of Sonoco's thermoformed and flexible packaging division, expanding its reach through 22 plants and 4,500 employees. This is not an isolated instance in mergers and acquisitions among commercial printing companies aimed at bolstering equipment for sustainable packaging in the Americas.

Commercial Printing Market Segmentation

By Printing Technology

- Digital Printing

- Lithography Printing

By Application

- Packaging

- Advertising

- Publication

By Substrate/Print Medium

- Paper & Paperboard

- Plastics/Films

- Textiles

- Metal

- Others

By Service Type

- Design/Prepress

- Printing

- Finishing/Bindery

- Fulfillment/Distribution

By Regional Outlook (Revenue-USD Billion, 2021–2034)

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Commercial Printing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 514.80 Billion |

| Market Size in 2026 | USD 526.79 Billion |

| Revenue Forecast by 2034 | USD 649.14 Billion |

| CAGR | 2.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Commercial Printing Market FAQ's

The global commercial printing market was valued at USD 514.80 billion in 2025 and is projected to reach USD 649.14 billion by 2034, growing at a CAGR of 2.6% during the forecast period.

Lithography (offset) printing dominates the market due to its efficiency in high-volume and packaging-related applications, while digital printing is the fastest-growing segment, driven by demand for short runs, personalization, and print-on-demand services.

Key growth drivers include expansion of e-commerce, rising demand for packaging and labeling, growth in advertising and promotional campaigns, and increased adoption of digital, AI-enabled, and web-to-print technologies.

North America held the largest market share in 2025, supported by strong demand for marketing, packaging, and labeling, as well as the presence of major printing companies. Asia Pacific is expected to witness the fastest growth due to e-commerce expansion, quick commerce, and digital print adoption.

Major applications include packaging, advertising, and publication printing, such as books, magazines, newspapers, promotional materials, catalogs, and direct mail, with packaging-related commercial print representing a significant share of overall demand.

Download Sample Report of Commercial Printing Market

Please fill out the form to request a customized copy of the research report.