E-learning Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

E-learning Market Summery

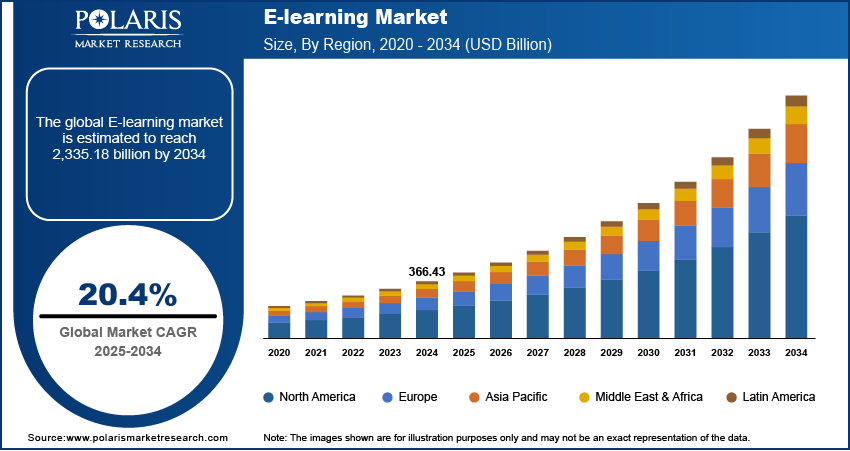

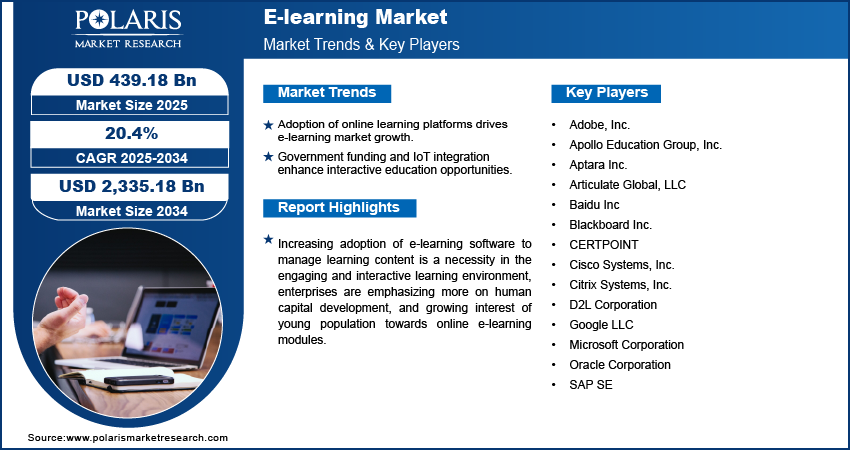

The global e-learning market size was valued at USD 439.92 billion in 2025 and is expected to grow at a CAGR of 20.4% during the forecast period, 2026 to 2034.

Market Statistics

Key Takeaways

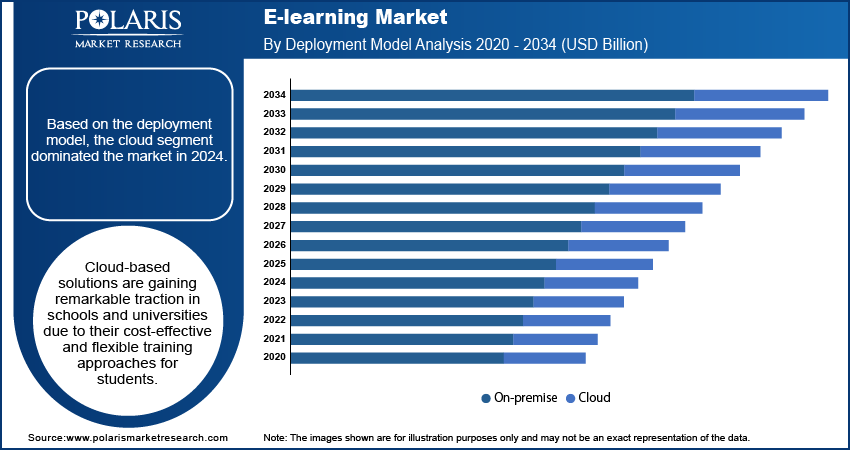

- In 2025, the cloud-based e-learning segment held the largest market share. This is due to the scalability, reduced infrastructure costs, and increased flexibility being provided to the users by cloud-based e-learning solutions.

- The higher education e-learning market is anticipated to see substantial growth. The demand for higher education e-learning is driven by the increasing need for specialized courses in the higher education sector.

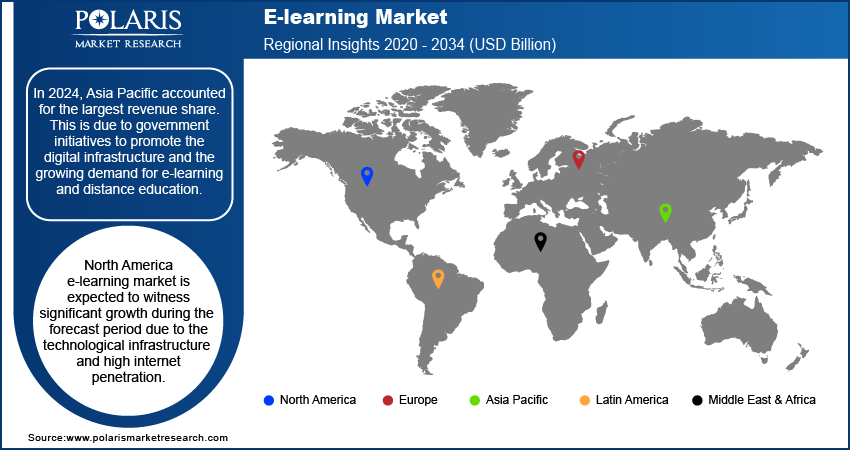

- The Asia Pacific e-learning market accounted for the largest share of revenue in 2025. This is fueled by the implementation of digital education and the growing use of online education for the K-12 level.

- The North America e-learning market is driven by well-developed infrastructure and AI-powered learning platforms in the enterprise training space.

The global e-learning market represents one of the rapidly growing sectors in the online education space. E-learning platforms, learning management systems, virtual classrooms, and corporate training platforms are the various categories covered by the global e-learning sector. Adoption is rising across schools, businesses, and government organizations as they seek flexible learning models that are easy to scale and more cost-effective.

The increasing use of cloud-based e-learning solutions, coupled with the availability of the internet and the use of smartphone technologies, has led to a significant expansion of online learning. Apart from the education sector, the use of corporate e-learning market solutions is also gaining acceptance among corporations that are focusing on employee development.

Industry Dynamics

- The rise in adoption of online learning platforms by educational centers for advanced teaching methods is driving the e-learning market.

- Apart from adoption at the academic level, enterprises have increasingly adopted e-learning platforms to enhance worker efficiency, reduce training costs, and embrace flexible working patterns.

- The integration of generative AI, augmented reality, and virtual reality offers opportunities for increasing user engagement on adaptive learning platforms.

- Digital fatigue and low learner engagement pose market challenges. Limited human interaction may lower learning outcomes.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

AI Impact on E-Learning Market

- AI assesses each student's performance and learning styles to automate the creation of personalized lessons and recommend personalized content.

- It automates the grading process, provides instant feedback on homework and assignments, and deploys chatbots to answer students' questions.

- Many AI tools are expected to create personalized, interactive learning materials and cultivate simulations of real-world scenarios for practice, increasing the pool of educational resources.

- AI is expected to provide early alerts and assessments for educators to identify students at risk of disengagement and falling behind.

- Artificial Intelligence technology is changing the face of the online learning industry by analyzing learning behavior patterns and, based on that, offering learning solutions.

- Organizations have begun using AI-enabled learning management systems that align with organizational goals. Educational institutions are using AI-powered tools to improve engagement and implement a results-oriented learning process.

Increasing adoption of e-learning software to manage learning content is a necessity in an engaging and interactive learning environment. Enterprises are emphasizing more on human capital development, and the growing interest of the young population in online e-learning modules. AI and machine learning have grown tremendously in e-learning services, enabling customized content tailored to each student's requirements. Furthermore, the introduction of technologies such as VR and AR has created realistic, active-training environments, improving skill acquisition. The technological innovation, with the shift toward flexible and remote work environments, is also a contributing factor in the adoption of e-learning platforms in corporate and academic settings.

Industry Dynamics

Growth Drivers

The adoption of online learning solutions and platforms is being deployed throughout educational institutions to assess the effectiveness of advanced learning methodologies, thereby contributing significantly to the growth of the e-learning market. Furthermore, the surging focus on childhood education and the growing public-private funding for K-12 education are further driving industry growth during the forecast period.

Additionally, increasing government initiatives in smart education and learning will create high growth prospects for the industry globally. IoT devices are being used to facilitate e-learning and education. This has made information exchange simple, exciting, and interactive, thereby gaining wide acceptance in the industry. This, in turn, is expected to accelerate the growth of the e-learning market worldwide.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Segmental Insights

The e-learning market segmentation provides insight into how providers, deployment models, course structures, and end user requirements influence adoption patterns across regions and industries.

Deployment Model Analysis

Based on the e-learning market by deployment model insights, the cloud segment dominated the market in 2025. Cloud-based solutions are gaining remarkable traction in schools and universities due to their cost-effective and flexible training approaches for students. The integration of cloud technology into digital learning enables students to access information anytime, anywhere. The cloud computing-based e-learning technology further enables educational institutions to build a virtual environment for learners and educators. Thus, cloud computing technology is majorly implemented in the education sector, contributing majorly to the segment’s leading market position.

Course Analysis

The primary and secondary education segment dominated the global industry due to increased use of digital learning methods in primary schools and the significant presence of online K-12 education providers worldwide. Further, digital tools, such as smartphones, have become exciting learning tools for improving educational quality and e-learning in distance education. Also, the use of digital media enhances course delivery flexibility, enabling learners to access online learning platforms and retrieve course resources. Thus, the emergence of a digital learning solution for primary and secondary education to engage in online training courses, which in turn expands the industry growth during the forecast timeframe.

The higher education segment is projected to witness significant growth in the industry due to the rise in the adoption of advanced learning methodologies effective for the education sector, driven by their various benefits, such as offering low-cost, specialized course learning. According to IBM statistics, e-learning can increase productivity by about 50% when using online learning software. Therefore, these factors are expected to drive global market growth.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Regional Analysis

North America E-Learning Market Assessment

The North America e-learning market is expected to witness significant growth during the forecast period due to the technological infrastructure and high internet penetration, which provide advancements in digital platforms. The region's high number of leading edtech companies and universities has boosted innovation with immersive and AI technologies. Moreover, investment in employee training to adopt online learning solutions boosts the demand. As compared with other regions, North America’s expansion is primarily fueled by an established digital infrastructure base, private investment, and early adoption of advanced learning technologies. Favorable policies that promote digital education and upskilling contribute to North America emerging as a distinct region rather than an emerging market.

Asia Pacific E-Learning Market Insights

Asia-Pacific accounted for the largest revenue share in the global E-learning market in 2025. This is due to government initiatives to promote the digital infrastructure and the growing demand for e-learning and distance education. The policy indicates that online education is developing to a noticeable extent. Furthermore, the rapid rise in the number of smart device users and the large presence of online and K-12 private education providers are directly impacting the higher market growth in emerging Asian countries, such as China, India, Malaysia, and others. The Asia-Pacific market accounts for a significant share of the global market over the foreseeable period, owing to the growing public-private funding for K-12 education. Unlike North America, the main driver of the Asia Pacific market has been scale, driven by the large number of students, government-sponsored digital education initiatives, and advances in internet and mobile infrastructure. Government-sponsored public funding programs and collaboration with private education technology firms help bridge the rural-urban divide in online education.

Europe E-Learning Market Assessment

Europe has also experienced substantial growth in the global e-learning market due to its established education systems, which have led to widespread adoption of e-learning. Government support, as well as investment by private organizations in educational and vocational initiatives, is enabling people to benefit from digital education, thereby driving market growth during the forecast period.

The e-learning industry in Europe is developing in a way not seen in Asia Pacific or North America, as government policy initiatives mainly drive developments here. The EU-level digital education frameworks, national lifelong learning strategies, and worker reskilling are key factors in the adoption of e-learning in the region. Moreover, the region's broadband availability and public funding support steady growth in the e-learning industry.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Key Players and Competitive Insights

The e-learning industry is fragmented, with the presence of several players. These include platform firms, learning content and course developers, and technology firms specializing in enterprise learning solutions. Participants in this industry span the value chain, from LMS platforms and learning content solutions to large learning platforms, analytics, and cloud-based solutions. The industry's dynamics are influenced by factors such as platform scalability, learning content quality, and interoperability with other system solutions.

Platforms and Learning Management Solution Providers

The platform vendors are the core of an e-learning ecosystem, offering learning management systems, virtual classroom facilities, assessment tools, and learner engagement solutions. Ease of use, scalability, data insights, and seamless integration with large enterprise IT systems are the focus areas for these vendors. Some leading companies for this offering include Blackboard Inc., D2L Corporation, Articulate Global, LLC, and CERTPOINT. Such platforms have been widely used in universities, institutes providing professional training, and corporate learning environments.

Content Development and Learning Services Providers

Content-based providers primarily engage in the development of content and courses as well as the provision of related services. These providers cover tailored course development, compliance courses, and skills-based learning programs for both organizations and learning institutions. Major market players such as Apollo Education Group, Inc., and Aptara Inc. provide content development and managed learning services to increase learner engagement.

Enterprise and Technology Platform Providers

The leading tech firms help the e-learning industry by offering cloud services, collaboration platforms, analytics, and AI-enabled learning platforms. The solutions offered by these tech firms can be integrated into a larger enterprise system to support training and remote education. The major technology providers in the market for e-learning solutions are Microsoft Corporation, Google LLC, Oracle Corporation, SAP SE, Cisco Systems, Inc., Citrix Systems, Inc., Adobe, Inc., and Baidu, Inc. The firms are seen as market leaders in the tech space owing to their powerful cloud platforms, AI-enabled personalization, security, and easy integration with enterprise solutions.

Competitive Positioning Overview

The e-learning industry competition is driven mostly by innovation in platforms, agility in content, and seamless enterprise system integration. Platform vendors are innovating to engage learners better and ensure smoother content delivery, whereas content vendors are innovating to ensure customization and high-quality learning. The key players in the enterprise technology space are distinguished for their scalable platforms, use of AI, and comprehensive e-learning ecosystems. The layered enterprise ecosystem implies a fragmented e-learning industry, with collaborations and ecosystem strategies very crucial for the growth of the e-learning sector.

Some of the major players operating in the global market include:

- Adobe, Inc.

- Apollo Education Group, Inc.

- Aptara Inc.,

- Articulate Global, LLC

- Baidu Inc

- Blackboard Inc.

- CERTPOINT

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- D2L Corporation

- Google LLC

- Microsoft Corporation

- Oracle Corporation

- SAP SE

Industry Developments

- April 2025: The Punjab and Haryana High Court passed a significant judgment that all academic credentials earned via distance learning from deemed universities, private institutions, and government universities are valid and will be given due recognition. Nevertheless, the recognition depends on verification and approval from the concerned government department or the University Grants Commission (UGC).

- July 2024: The online skill development platform, AMHSSC, joined forces with Bluesign Technologies AG of Switzerland to introduce a brand new e-learning program called “Foundation to Apparel Sustainability.” The initiative is designed to enhance sustainable practices in the apparel sector in India and will focus on areas of sustainable fashion, the circular economy, and advanced recycling methods.

E-learning Market Segmentation

By Provider Outlook (Revenue, USD Billion, 2021–2034)

- Content Provider

- Service Provider

By Deployment Model Outlook (Revenue, USD Billion, 2021–2034)

- On-premise

- Cloud

By Course Outlook (Revenue, USD Billion, 2021–2034)

- Primary and Secondary Education

- Higher Education

- Online Certification and Professional Course

- Test Preparation

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Academic

- Corporate

- Government

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

E-Learning Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 439.92 billion |

| Market Size in 2026 | USD 528.57 billion |

| Revenue Forecast by 2034 | USD 2,340.73 billion |

| CAGR | 20.4% |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | E-learning Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global e-learning market is expected to reach USD 2,340.73 billion by 2034, accounting for a CAGR of 20.4% between 2026 and 2034.

The cloud-based deployment model currently leads the market due to its cost efficiency, flexibility, and ease of access to the system.

AI and machine learning technologies support content customization to the needs of each individual learner, thereby enhancing the learning experience through learning pathways and facilitating the analysis of learning outcomes.

Asia Pacific dominated the e-learning market in 2025, driven by rising smartphone adoption, government smart education initiatives, expanding internet access, and the need for accessible education solutions in developing countries.

It helps reduce the cost of training and sessions, provides flexibility in scheduling, and ensures that training and learning content are delivered consistently to employees.

• The higher education segment is projected to witness significant growth during the forecast period.

Download Sample Report of e learning market

Please fill out the form to request a customized copy of the research report.