Flexible Packaging Market Share, Business Trends, Strategies, 2026-2034

REPORT DETAILS

Flexible Packaging Market Summary

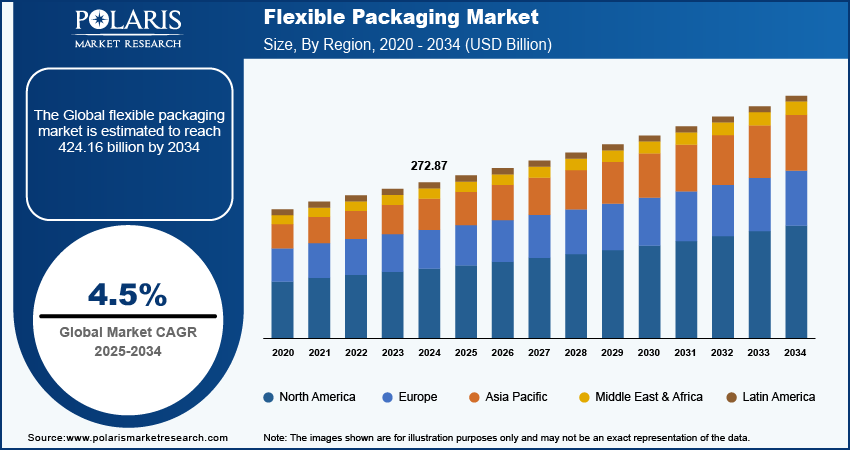

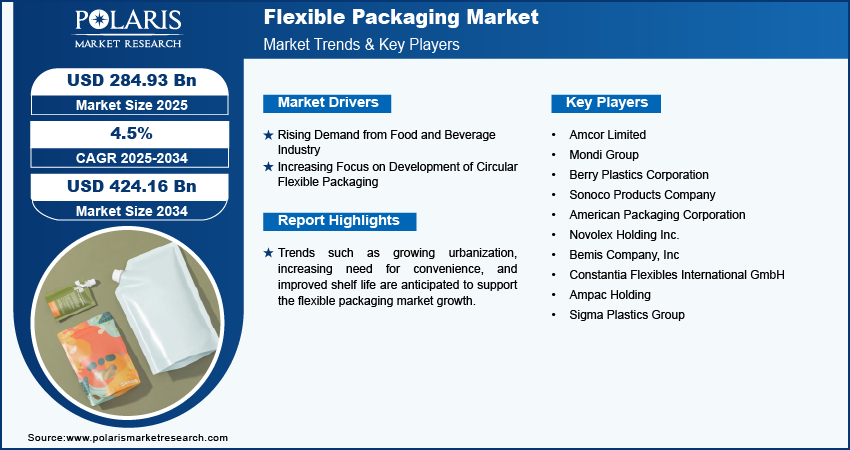

The global flexible packaging market size was valued at USD 284.93 billion in 2025, exhibiting a CAGR of 4.50% from 2026 to 2034. The increased demand from the food and beverage sector, emphasis on sustainability, urbanization, and the trend towards eco-friendly, circular packaging are all contributing to the growth of the market.

Market Statistics

Key Takeaways

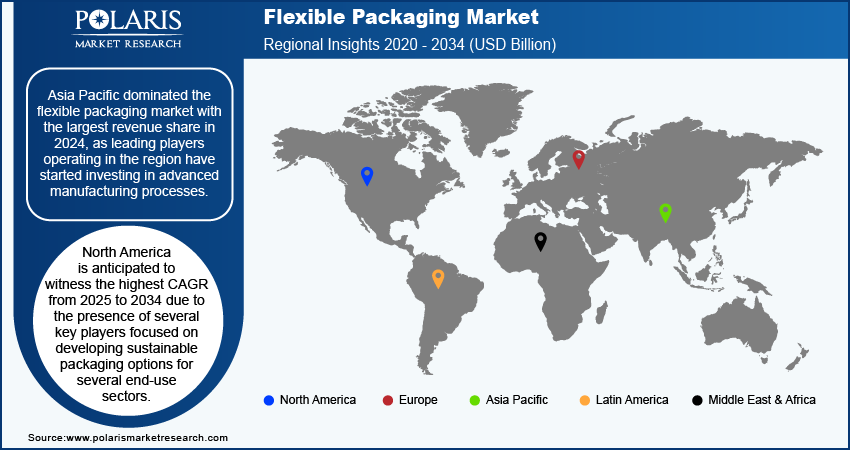

- Asia Pacific held the largest market share of 45.8% in 2025. This is due to increased purchasing power, expanding retail reach, and investment in high-tech production to cater to diverse consumer needs.

- The flexible packaging market in China is expected to record a growth rate of 6.35% CAGR during the forecast period due to increasing demand from end-use industries.

- From 2026 to 2034, North America is expected to experience a growth rate of 2.78% CAGR, driven by the adoption of green packaging and government support for traceability.

- In 2025, the pouches category dominated with a 39% revenue share because of their convenience, affordability, and multifaceted nature as a cost-effective substitute for conventional packaging.

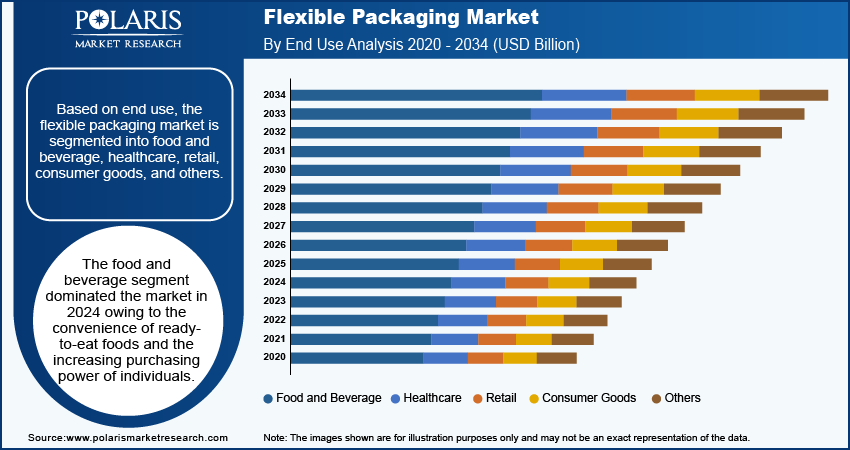

- In 2025, the food and beverage category dominated the market with a 59.6% share because of the convenience of ready-to-eat meals and increased consumer purchasing power.

Industry Dynamics

- The increasing demand for smaller and user-friendly packaging has prompted manufacturers to develop more eco-friendly packaging options, driving market growth.

- The increasing trend toward flexible packaging in the food and beverage segment, driven by hectic lifestyles and the demand for cost-efficient and convenient solutions, is fueling market growth.

- The increasing emphasis on principles of the circular economy, such as recycling and resource efficiency, is powering the growing worth of the market.

- One of the major constraints in the flexible packaging market is the complexity of recycling intricate materials, as well as the environmental impact of non-recyclable packaging elements.

Source: Polaris Market Research Analysis

What is Flexible Packaging?

Flexible packaging refers to non-rigid packaging materials used for packaging and protecting products. According to the flexible packaging association, it is any package or any part of a package whose shape can be readily changed. Flexible packaging is extremely customizable and can be tailored according to the requirements. Additionally, the packaging offers consumer convenience, is easy to transport and store, enhances shelf appeal, and produces fewer emissions. Bags, pouches, tubes, cardboard, and shrink film are a few common examples of flexible packaging.

The flexible packaging market growth is driven by factors such as improved economic conditions, demographic and socio-economic changes, and environmental concerns. Trends such as growing urbanization, increasing need for convenience, and improved shelf life are anticipated to support the market growth. Additionally, the rising demand for consumer-friendly packaging and the downsizing of packaging has encouraged packaging producers to develop more sustainable solutions, further supporting the market expansion.

The rising focus on sustainability and the growing need for eco-friendly packaging are other factors contributing to the rising flexible packaging market value. Increased demand for packaged foods, growth of the pharmaceutical industry, the transition from conventional packaging solutions to modern alternatives, and rising demand from emerging economies are expected to create lucrative flexible packaging market opportunities during the forecast period.

Market Drivers

Rising Demand from Food & Beverage Industry

In the twenty-first century, packaging has become more efficient, sustainable, and cost-effective. Owing to busy schedules, modern consumers are increasingly opting for packaged meals served in flexible and convenient packaging. As a result, more food businesses are looking to use flexible packaging in their products. Packaging companies are responding to this shift by engaging in strategic developments such as mergers and acquisitions and joint ventures that enable them to provide cost-effective, innovative packaging solutions. Therefore, the growing demand for flexible packaging in the food & beverage industry boosts the flexible packaging market growth.

Increasing Focus on Development of Circular Flexible Packaging

Flexible packaging aligns well with the principles of circular economy, as it is more resource-efficient compared to traditional packaging. Also, it emits fewer greenhouse gases while offering several benefits, including durability, versatility, and space efficiency. As the emphasis on the circular economy continues to rise globally, several governments and companies are undertaking initiatives to recycle packaging waste and promote resource optimization. A notable example of such initiatives is CEFLEX (Circular Economy for Flexible Packaging), a collaboration of over 180 European organizations, companies, and associations representing the entire value chain of flexible packaging. CEFLEX aims to make all flexible packing circular in Europe by 2025. Thus, the rising focus on the development of circular flexible packaging contributes to the increasing flexible packaging market value.

Material Mix & Shift Trends (Technical Insight)

| Company | Key material shifts in flexible packaging | Technical / investment benchmarks | Strategic implications for material mix |

| Amcor | Transition from multi‑material laminates (e.g., PET/aluminum) to recycle‑ready mono‑PE and mono‑PP structures (AmPrima) and recycle‑ready high‑barrier retort pouches (AmLite HeatFlex). | AmLite HeatFlex recycle‑ready retort structure launched as an industry‑first recyclable retort pouch; by FY23, 89% of Amcor’s flexible portfolio had a recycle‑ready design solution, and 90% of total portfolio by revenue was designed to be recyclable, reusable or compostable. | Marks a structural shift from mixed-plastic laminates to mono-material PE/PP films and retort pouches that fit existing polyolefin recycling streams while preserving barrier and heat‑resistance performance. |

| Amcor | Expansion of paper‑based performance structures (AmFiber Performance Paper) and integration of chemically recycled feedstocks into flexible packaging. | AmFiber performance paper launched across all major regions (EU, Asia, Americas); Amcor reports almost 30% year‑on‑year increase in recycled material purchased for its products and highlights chemical recycling as a route to virgin‑grade polymers from flexible waste. | Increases share of fiber‑based flexible and hybrid structures while preparing for future material loops where chemically recycled polymers replace part of virgin plastic in high‑performance films. |

| Huhtamaki | Launch of three “breakthrough” mono‑material flexible packaging solutions designed for recycling and using less material than conventional multi‑layer laminates. | Company invested in blown film and advanced coating technologies across sites to scale these mono‑material structures; defines sustainable packaging as recyclable, compostable or reusable, positioning new mono‑material flexibles within its blueloop circular portfolio. | Replaces complex plastic laminate combinations with PE‑ or PP‑based mono‑material films and coatings, simplifying sorting and recycling while maintaining protection for food and consumer goods. |

| Mondi | Development of aluminium‑free, paper‑based flexible packs for applications like Unilever’s Colman’s meal mixes, replacing previously unrecyclable multi‑material laminates. | Case study shows transition from plastic/foil laminate sachets to recyclable paper packaging; Mondi notes strong consumer response to “100% recyclable” messaging and positions paper flexibles as a core growth area for premium pet food and food products. | Drives a shift from foil and multi‑layer plastic films to barrier paper solutions where product requirements allow, increasing paper share in the flexible material mix. |

| Smurfit Kappa (including flexible paper structures) | Promotion of mono‑material corrugated and paper‑based structures that replace plastic cushions, bags and laminates, including flexible corrugated solutions for e‑commerce and bottle protection. | Reports highlight fit‑for‑purpose, 100% recyclable mono‑material designs that substitute bubble wrap and polystyrene with flexible corrugated elements, supported partly through green‑bond financed projects. | Although focused on paper rather than films, this reflects a macro shift from plastic flexible components (void fill, sleeves) to recyclable paper‑based flexibles and hybrids in secondary and tertiary packaging. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Segment Insights

Market Insights by Type

The flexible packaging market segmentation, based on type, includes bags, pouches, wraps, and others. The pouches segment accounted for the largest revenue share in 2025. Pouches are small, single-use bags commonly made from plastic films, aluminum-deposited films, or vapor-deposited films. They are easy to use and available in a diverse range of sizes and formats. Also, pouches are heat-sealable and usually considered a cost-effective alternative to containers made of cardboard, glass, and metal. Thus, the convenience and affordability of pouches make them a highly popular option across various sectors.

Market Insights by End-Use

The flexible packaging market, based on end-use, is segmented into food and beverage, healthcare, retail, consumer goods, and others. The food and beverage segment dominated the market in 2025 owing to the convenience of ready-to-eat foods and the increasing purchasing power of individuals. Flexible packaging is favored in the food and beverage sector as it can extend shelf life and offer convenience to consumers. Products such as snacks, beverages, and frozen foods use flexible packaging in the form of pouches and wrappers to reduce waste and increase transportability.

Source: Polaris Market Research Analysis

Flexible Packaging Market Material Type Comparison

| Material | Key Properties | Advantages | Major Applications |

| Plastic | Lightweight, durable, flexible, strong moisture and oxygen barrier, easy heat sealing | Cost-effective, versatile, high product protection, suitable for multilayer packaging | Food packaging, pharmaceuticals, personal care, and household products |

| Paper | Recyclable, biodegradable, printable, good stiffness, and eco-friendly appearance | Sustainable option, strong branding appeal, consumer preference for green packaging | Bakery products, dry foods, retail bags, and personal care packaging |

| Foil | Excellent barrier against light, oxygen, moisture, and contamination, with high temperature resistance | Extended shelf life, superior product protection, ideal for sensitive products | Coffee packs, dairy products, medicines, retort packaging, confectionery |

Source: Polaris Market Research Analysis

Market Outlook by Regional Insights

Asia Pacific dominated the largest flexible packaging market share in 2025. The region’s growing purchasing power has enabled consumers to purchase products from a sizable number of retail facilities, boosting the demand for flexible packaging solutions. Also, leading players operating in the region have started investing in advanced manufacturing processes to ensure product integrity and cater to diverse consumer needs.

The flexible packaging market in China has witnessed a rapid increase in demand from end-use industries such as cosmetics, food & beverages, pharmaceuticals, and household care. Besides, the implementation of stringent government regulations aimed at reducing packaging waste is anticipated to support the market growth in the country.

North America is anticipated to register the highest CAGR from 2026 to 2034. The region has the presence of several leading players focused on developing sustainable packaging options for several end-use sectors. Government initiatives aimed at increasing the traceability of packaging circulating in North America are driving businesses to use flexible packaging solutions.

Source: Polaris Market Research Analysis

Key Players & Competitive Insights

The flexible packaging market is characterized by fragmentation. It has the presence of several small and medium-sized companies. The leading market players are making significant investments in R&D to extend their product lines. Also, they are undertaking several strategic initiatives, such as mergers and acquisitions and partnerships, to expand their global reach. To expand and survive in a more competitive environment, the flexible packaging market must offer cost-effective items.

In recent years, the flexible packaging market has witnessed several technological and innovation breakthroughs, with key players seeking to provide advanced solutions that help meet sustainability goals. A few leading players in the market are Amcor Limited; Mondi Group; Berry Plastics Corporation; Sonoco Products Company; American Packaging Corporation; Novolex Holding Inc.; Bemis Company, Inc; Constantia Flexibles International GmbH; Ampac Holding; and Sigma Plastics Group.

List of Key Players

- Amcor Limited

- Mondi Group

- Berry Plastics Corporation

- Sonoco Products Company

- American Packaging Corporation

- Novolex Holding Inc.

- Bemis Company, Inc

- Constantia Flexibles International GmbH

- Ampac Holding

- Sigma Plastics Group

Flexible Packaging Industry Developments

September 2025: Mondi partnered with Ekornes, a leading Nordic furniture manufacturer, to replace traditional plastic packaging with its paper-based CompressWrap solution for mattresses. This recyclable, fiber-based packaging ensures durability during compression and makes unwrapping easier for consumers, supporting sustainability and circular economy goals. (Source: mondigroup.com)

July 2025: Amcor and Mediacor launched a recycle-ready, mono-material 2-liter refill pouch for Nana cleaning products, compatible with recycling across multiple European countries. The new packaging reduces plastic use by up to 80% and lowers the carbon footprint by 64% compared to conventional PET bottles. (Source: amcor.com)

April 2025: Amcor announced an USD 8.4 billion acquisition of Berry Global, strengthening its North American healthcare presence and expanding its sustainable flexible packaging portfolio. (Source: amcor.com)

Future of Flexible Packaging Market

The flexible packaging market is expected to witness strong growth. The expansion is driven by the increasing demand for sustainable and lightweight packaging solutions across industries. Rising adoption of recyclable, compostable, and bio-based materials supports the transition toward environmentally responsible packaging systems. Circular economy initiatives and stricter regulations on plastic waste are encouraging manufacturers to invest in mono-material structures and advanced recycling technologies. Emerging markets in Asia-Pacific, Latin America, and Africa are creating opportunities due to expanding retail sectors and rising packaged food consumption. Continuous innovation in high-barrier recyclable packaging and smart packaging solutions will strengthen long-term market expansion

Flexible Packaging Market Segmentation

By Type Outlook

- Bags

- Pouches

- Wraps

- Others

By Material Outlook

- Paper

- Plastic

- Flexible Foam

- Aluminum Foil

- Bioplastics

- Others

By End-Use Outlook

- Food and Beverage

- Healthcare

- Retail

- Consumer Goods

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Flexible Packaging Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 284.93 billion |

| Market Size Value in 2026 | USD 297.58 billion |

| Revenue Forecast by 2034 | USD 424.16 billion |

| CAGR | 4.50% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The flexible packaging market value reached 284.93 billion in 2025 and is projected to grow to 297.58 billion by 2034.

The market is projected to record a CAGR of 4.50% from 2026 to 2034.

Asia Pacific accounted for the largest flexible packaging market share.

A few key players in the market are Amcor Limited; Mondi Group; Berry Plastics Corporation; Sonoco Products Company; American Packaging Corporation; Novolex Holding Inc.; Bemis Company, Inc; Constantia Flexibles International GmbH; Ampac Holding; and Sigma Plastics Group.

The pouches segment accounted for the largest market share in 2025.

The food and beverage segment dominated the market in 2025.

Download Sample Report of Flexible Packaging Market

Please fill out the form to request a customized copy of the research report.