Float Glass Machinery Market Trends, Industry Analysis, 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

Market Overview

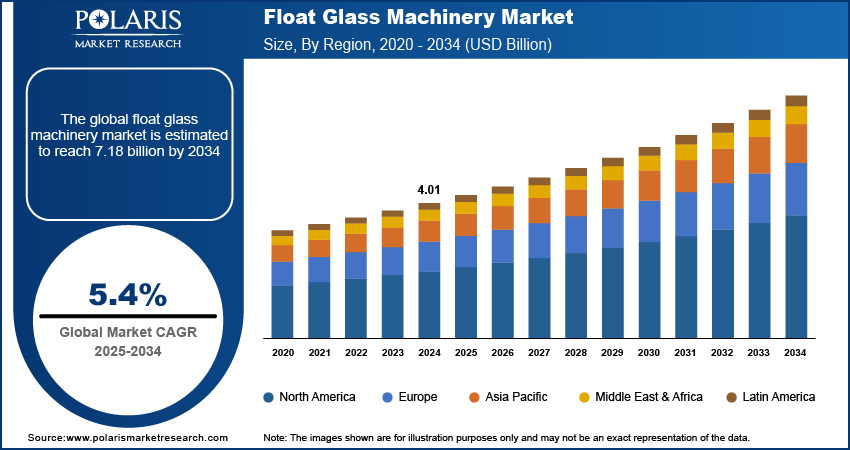

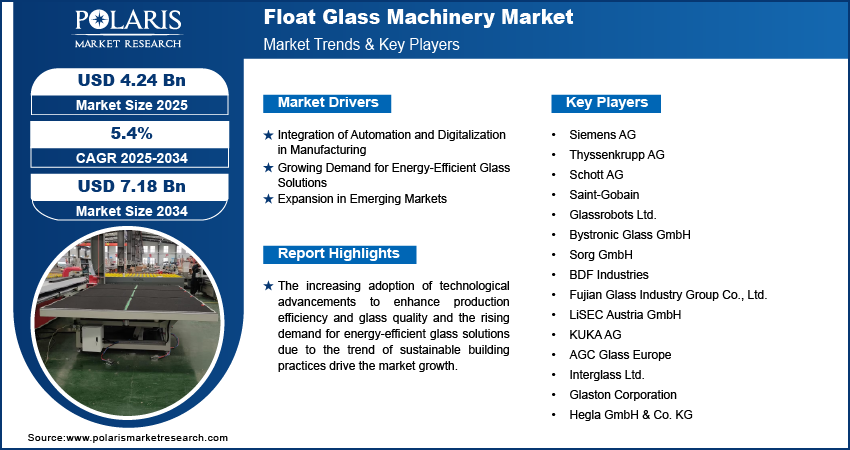

The global float glass machinery market size was valued at USD 4.01 billion in 2024. The market is projected to grow from USD 4.24 billion in 2025 to USD 7.18 billion by 2034, exhibiting a CAGR of 5.4% during 2025–2034.

The global float glass machinery market is growing owing to the increasing demand for high-quality flat glasses in various sectors, including construction and automotive, and the expansion of the construction industry, particularly in emerging markets.

The increasing adoption of technological advancements to enhance production efficiency and glass quality and the rising demand for energy-efficient glass solutions due to the trend of sustainable building practices drive the market growth. Emerging trends, such as the integration of automation and digitalization in float glass manufacturing processes, are expected to shape the market in the coming years, improving productivity and reducing operational costs.

To Understand More About this Research: Download Sample Report

Market Driver Analysis

Integration of Automation and Digitalization in Manufacturing

Modern float glass production lines incorporate sophisticated automation technologies to streamline operations, enhance precision, and reduce human error. Automated systems handle complex processes such as temperature control, glass cutting, and quality inspection with minimal manual intervention. Additionally, digitalization facilitates real-time monitoring and data analytics, enabling manufacturers to optimize production processes, predict maintenance needs, and improve overall efficiency. This shift toward high-tech solutions boosts productivity and aligns with the industry’s growing emphasis on cost reduction and quality assurance.

Growing Demand for Energy-Efficient Glass Solutions

Increasing awareness of environmental sustainability and the push for greener building practices propel the demand for energy-efficient glass solutions. Float glass manufacturers are responding by developing technologies that produce glass with superior thermal insulation properties, thus reducing energy consumption in buildings. This trend is driven by stringent regulations and standards aimed at minimizing carbon footprints and improving energy efficiency in construction. As a result, float glass machinery is evolving to support the production of advanced glass types that meet these new energy efficiency standards.

Expansion in Emerging Markets

The expansion of the construction and real estate sectors in emerging markets is a significant trend shaping the float glass machinery market. Countries in Asia Pacific, Latin America, and parts of Africa are experiencing rapid urbanization and infrastructure development, which drives the demand for float glasses. These regions are investing heavily in residential, commercial, and industrial construction projects, thereby creating a substantial requirement for high-quality float glasses. This expansion prompts manufacturers to tailor their machinery offerings to meet the specific needs and regulatory requirements of these emerging markets, such as adapting to local materials and climatic conditions.

Market Segment Insights

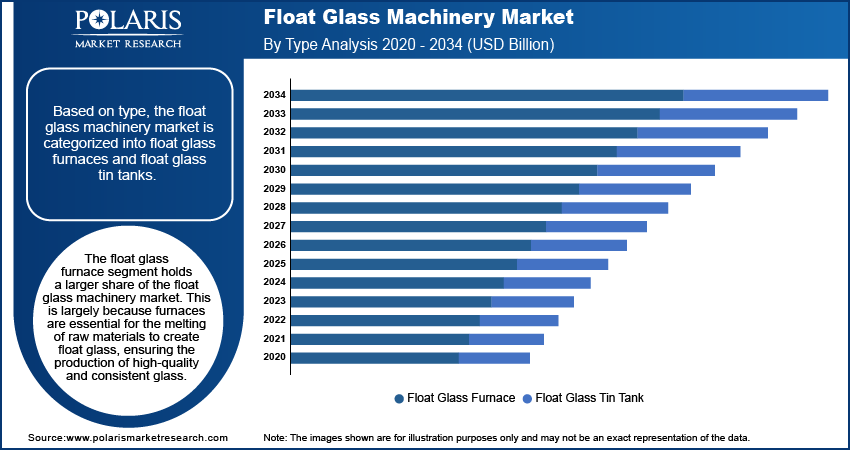

Float Glass Machinery Market Assessment by Type Insights

Based on type, the float glass machinery market is categorized into float glass furnaces and float glass tin tanks. The float glass furnace segment holds a larger share of the float glass machinery market. This is largely because furnaces are essential for the melting of raw materials to create float glass, ensuring the production of high-quality and consistent glass. The importance of furnaces in the manufacturing process solidifies their leading position, as they are pivotal in achieving the desired glass characteristics necessary for construction and automotive applications.

The float glass tin tank segment is emerging as the highest-growing category owing to Innovations in tin tank technology, including improved heat management and enhanced durability. Tin tanks play a crucial role in the cooling and solidifying phase of float glass production, and advancements in this area are contributing to increased efficiency and reduced production costs. This rising demand reflects the industry's focus on optimizing production processes and improving glass quality, positioning the float glass tin tank segment as a rapidly expanding segment in the market.

Float Glass Machinery Market Evaluation by Application Insights

The construction segment, in terms of application dominates the float glass machinery market due to the extensive use of float glass in facades, windows, and interior partitions, driven by ongoing construction projects and a growing emphasis on energy-efficient building materials. The high demand for aesthetically pleasing and functional glass in residential and commercial buildings underscores the leading position of the construction segment.

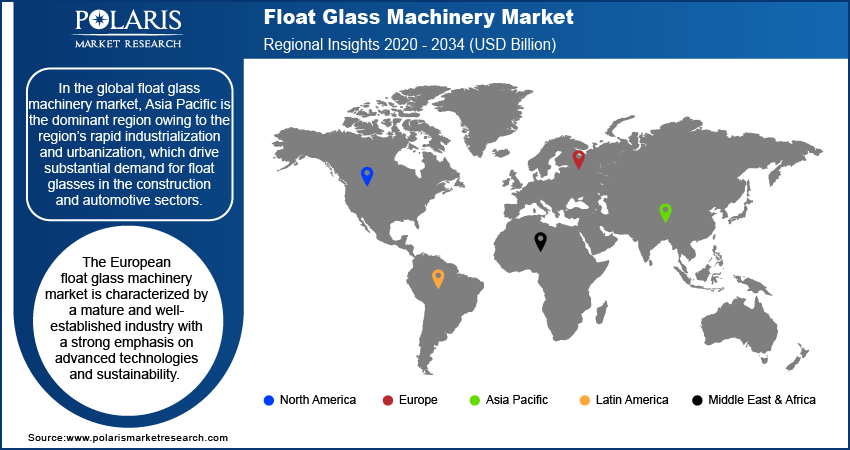

Market Regional Insights

By region, the study provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In the global float glass machinery market, Asia Pacific is the dominant region owing to the region’s rapid industrialization and urbanization, which drive substantial demand for float glasses in the construction and automotive sectors. Countries such as China and India are major contributors, with extensive infrastructure projects and a burgeoning automotive industry boosting market activity. Additionally, the region benefits from a growing focus on energy-efficient and sustainable building practices, further propelling its leading position. The combination of large-scale construction developments, increased vehicle production, and technological advancements in float glass machinery contributes to the Asia Pacific's dominance in the market.

The European float glass machinery market is characterized by a mature and well-established industry with a strong emphasis on advanced technologies and sustainability. European countries are known for their stringent regulations regarding energy efficiency and environmental impact, driving demand for high-quality float glass solutions that meet these standards. The region’s focus on renovation and refurbishment projects in residential and commercial buildings, combined with innovations in glass technology for automotive and architectural applications, supports steady market growth. Major players in Europe are also increasingly investing in research and development to stay competitive and meet the evolving needs of the market.

Key Players and Competitive Insights

Siemens AG, Thyssenkrupp AG, Schott AG, Saint-Gobain, and Glassrobots Ltd are among the key players in the float glass machinery market. Other significant contributors are Bystronic Glass GmbH; Sorg GmbH; BDF Industries; Fujian Glass Industry Group Co., Ltd.; and LiSEC Austria GmbH. Additionally, companies such as KUKA AG, AGC Glass Europe, Interglass Ltd., Glaston Corporation, and Hegla GmbH & Co. KG play important roles in the market. These companies are recognized for their advanced technologies and extensive expertise in float glass production machinery.

Saint-Gobain is a major player in the float glass machinery market, renowned for its advanced glass manufacturing technologies and commitment to sustainability. The company offers a diverse range of high-quality float glass solutions for construction and automotive applications. Saint-Gobain’s focus on innovation and efficiency helps it maintain a strong market presence.

Schott AG is another major player known for its cutting-edge glass technology and extensive float glass product portfolio. Serving various sectors, including architecture and electronics, the company is recognized for its precision and technological advancements in float glass manufacturing.

Key Companies

- Thyssenkrupp AG

- Schott AG

- Saint-Gobain

- Glassrobots Ltd.

- Bystronic Glass GmbH

- Sorg GmbH

- BDF Industries

- Fuyao Glass Industry Group Co., Ltd.

- LiSEC Austria GmbH

- KUKA AG

- AGC Glass

- Interglass Ltd.

- Glaston Corporation

- Hegla GmbH & Co. KG

Market Recent Development

February 2024, AGC and Saint-Gobain partnered to design a pilot flat glass line targeting significant CO₂ emission reductions. The refurbished line in Barevka, Czech Republic, aims to be 50% electrified and 50% fired by a combination of oxygen and gas, contributing to both companies' carbon neutrality goals

June 2023, Saint-Gobain Glass launched the production of India's first low-carbon glass, achieving an approximately 40% reduction in carbon footprint compared to existing products. This was accomplished through the use of recycled content and renewable energy sources.

April 2024, Vitro's 2024 Environmental Product Declarations (EPDs) for flat and processed glass indicate its architectural glass products contain just 1,240 kilograms of CO₂ equivalent, which is 13% lower than the industry standard.

November 2022, the float glass industry is transitioning from natural gas to green hydrogen and renewable energy in order to achieve carbon neutrality. Companies like Saint-Gobain and NSG Group are exploring hybrid technologies and hydrogen-based fuels to cut emissions and promote sustainability.

November 2021, Beibut Atamkulov, Minister of Industry and Infrastructure Development of the Republic of Kazakhstan, announced to open a new float glass production plant in the Kyzylorda region of the country in 2022. The plant will have a production capacity of 197.1 thousand tonnes per year and is expected to cover 98 percent of the demand for float glass in the domestic market.

Market Segmentation

By Type Outlook (Revenue – USD Billion, 2020–2034)

- Float Glass Furnace

- Float Glass Tin Tank

By Application Outlook (Revenue – USD Billion, 2020–2034)

- Construction

- Automotive Industry

- Others

By Regional Outlook (Revenue – USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size Value in 2024 | USD 4.01 billion |

| Market Size Value in 2025 | USD 4.24 billion |

| Revenue Forecast in 2034 | USD 7.18 billion |

| CAGR | 5.4% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global float glass machinery market size was valued at USD 4.01 billion in 2024 and is projected to grow to USD 7.18 billion by 2034.

The global market is projected to register a CAGR of 5.4% during 2025–2034

Asia Pacific accounted for the largest global market share.

Major companies such as Siemens AG, Thyssenkrupp AG, Schott AG, Saint-Gobain, and Glassrobots Ltd are operating in the float glass machinery market. Other significant contributors are Bystronic Glass GmbH; Sorg GmbH; BDF Industries; Fujian Glass Industry Group Co., Ltd.; and LiSEC Austria GmbH. Additionally, companies such as KUKA AG, AGC Glass Europe, Interglass Ltd., Glaston Corporation, and Hegla GmbH & Co. KG play important roles in the market.

The float glass furnace segment dominated the market in 2024.

The construction segment accounted for the largest share of the global float glass machinery market.

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research & Consulting, Inc. uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

1. Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

2. Data Collection

We gather information from both public and verified sources:

3. Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

| Region | Segment | VolumeUnits | Avg PriceUSD | RevenueUSD Mn | Share % |

|---|---|---|---|---|---|

| North America | Product A | 250 | 2.5 | 500 | 15% |

| Product A | XX | XX | XX | XX | |

| Product A | XX | XX | XX | XX | |

| Consistent methodology applied across regions | |||||

4. Market Estimation

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Forecasting

Step 6:

At Polaris Market Research & Consulting, Inc., we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Validation & Triangulation

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Triangulation Framework

Estimates are cross-verified across three sources:

Company-level data

• Primary inputs from industry participants

• Secondary benchmarks and published data

Variance maintained within +5-10%

Adjustments applied to align estimates

Segment values validated against overall market structure

Data Consistency & Integrity

Segment totals validated to 100%

Regional estimates aligned with global market size

Historical trends compared against forecast outputs

Assumptions reviewed for cross-segment and regional alignment

Final Outputs

Deliverables

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements

Download Sample Report of Float Glass Machinery Market

Please fill out the form to request a customized copy of the research report.