Gastrointestinal Stent Market Size, Share, Growth Analysis Report, 2026-2034

REPORT DETAILS

Gastrointestinal Stent Market Summary

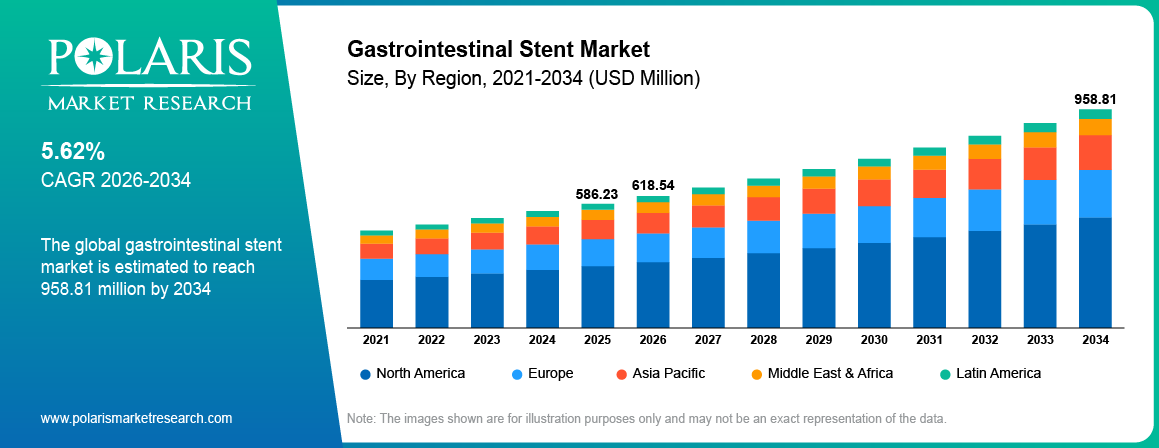

The global gastrointestinal stent market is estimated around USD 586.23 Million in 2025,with consistent growth anticipated during 2026–2034. Growth is driven by rising number of gastrointestinal cancer and shift towards minimally invasive procedure. The market is projected to grow at a CAGR of 5.62% during the forecast period.

Market Statistics

Key Takeaways

- North America gastrointestinal stent market dominated the global market in 2025, accounting for approximately 41.10% market share due to advanced healthcare infrastructure and high procedure volume.

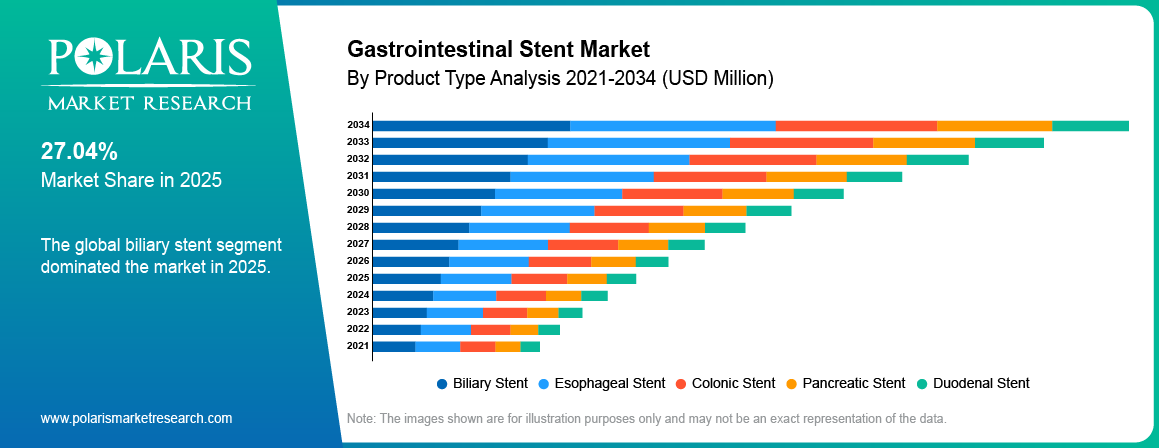

- Biliary stent dominated the market in 2025, holding approximately 38.65% market share due to rising incidence of biliary disorders.

- Pancreatic stents are expected to have the highest CAGR of approximately 13.80% during the forecast period due to increasing pancreatic disease cases and treatment adoption.

- In 2025, metal stent held the largest share in the global market, contributing approximately 42.25% market share due to durability and longer patency.

- Biliary disease segment dominated the market in 2025, accounting for approximately 36.90% market share due to growing prevalence of gallstones and bile duct obstructions.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Rising number of gastrointestinal cancer is increasing demand for gastrointestinal stents.

- Shift toward minimally invasive procedures is increasing demand for GI stents.

- High device costs are creating market challenges.

- Development of biodegradable stents are creating long-term growth opportunities.

What is the Gastrointestinal Stent Market?

Gastrointestinal (GI) stents are medical devices used to treat obstructions in the digestive tract, including the esophagus, stomach, intestines, and bile ducts. The purpose of these stents is to maintain the flow of blood by preventing the passage from narrowing or blocking, particularly in cases of cancer, stricture formation, and other GI disorders. The use of stents in GI disorders is common in hospitals and ambulatory surgery centers. The use of gastrointestinal stents is growing owing to the growing cases of gastrointestinal cancers.

The GI stents sector works under the regulatory structure of medical devices that aim at providing safety, efficacy, and procedural success. The demand for GI stents is rising owing to higher consciousness regarding early detection and improvements in endoscopic techniques. Medical practitioners are giving more preference to minimally invasive treatments and shorter recovery periods.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

There is a greater demand for gastrointestinal stents due to the rising number of digestive system diseases and the popularity of non-invasive techniques. The application of technologies such as self-expanding metal stents (SEMS) and degradable stents has led to improved results. Expansion of healthcare infrastructure and availability of skilled endoscopists are supporting market growth. These factors are driving the expansion of the global gastrointestinal stent market.

Drivers & Opportunities

Rising number of gastrointestinal (GI) cancer is increasing demand for gastrointestinal stents: Increase in gastrointestinal cancer cases has led to higher demand for obstruction management across hospitals and specialty care centers. Gastrointestinal stents are widely used to relieve blockages caused by cancers such as esophageal, colorectal, and pancreatic cancer. According to American Cancer Society (2025), the number of gastrointestinal (GI) cancer is projected to reach 9.06 million by 2050 globally, an increase of 85% compared to the number in 2022. Healthcare providers are reporting higher patient inflow requiring minimally invasive interventions for malignant obstructions. Medicals are increasingly adopting stent-based procedures to reduce surgical risks. This factor is supporting growth in the gastrointestinal stent market.

Shift toward minimally invasive procedures is increasing demand for GI stents: The growing preference for minimally invasive techniques results in the increased use of endoscopy treatment in different clinics. For instance, as per the National Library of Medicine, the adoption of minimally invasive surgical procedure rose from 51.2% in 2012 to 93.6% in 2024 among 1,142 colorectal cancer resections. Gastrointestinal stents are used to treat digestive tract obstructions without resorting to surgery. Minimally invasive surgeries are associated with reduced risks and shorter hospital stays. This trend encourages the development of the gastrointestinal stent market.

Restraints & Challenges

High device costs limit adoption of GI stents: GI stenting demands costly equipment, endoscopy equipment, and specialized medical knowledge. Cost considerations are posing difficulties for its adoption in budget-conscious regions. Coverage issues and large cost-sharing amounts are raising financial obstacles. This issue is hindering market growth within the GI stent industry.

Stent-related complications limit adoption of gastrointestinal stents: GI stenting poses risks that include stent migration, stent occlusion, stent perforation, and infection. Complications necessitate re-doing procedures and increase costs. Safety concerns and medical outcomes are causing some doctors to hesitate. This factor is limiting adoption in the GI stent industry.

Opportunity

Development of biodegradable stent is creating growth opportunities for the GI stent market: Biodegradable stents eliminate the need for removal procedures after treatment. They decrease potential issues and increase comfort. For example, in December 2025, University of Iowa Health Care was successful in performing the first clinical procedure involving the ARCHIMEDES FDA-approved biodegradable pancreatic stent in the US that will help offer less invasive treatment for the disease of pancreatitis and pancreatic cancer patients. Technological advancements in the materials used will be helping their adoption. This factor is creating growth opportunities in the gastrointestinal stent market.

Market expansion into emerging markets to provide opportunities for GI stents: There has been a growth in investment in healthcare as well as an establishment of specialty care centers in the developing nations. For example, the Indian government has committed USD 11.50 billion in the union budget of 2025-2026, which is an increase of 9.78% from the financial year 2025. Enhanced healthcare facilities and increased awareness of gastrointestinal conditions are boosting the demand for superior treatment options.

-stent-market-size-to-reach-usd-958.81-million-by-2034-.png)

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the gastrointestinal stent market by product type, material type, application, and end-use industry to help readers identify the fastest expanding and most attractive demand segments.

By Product Type

-

Biliary Stent

Biliary stent dominated the market in 2025, driven by the rising prevalence of biliary obstructions caused by conditions such as pancreatic cancer and gallstones. The rising adoption of minimally invasive endoscopy is aiding the demand. The healthcare sector is also emphasizing the development of advanced stents to ensure patency and minimize complications, which is expected to boost the segment's growth.

-

Pancreatic Stent

Pancreatic stents are expected to have the highest CAGR in the forecast period due to increasing cases of pancreatitis and pancreatic cancer. For instance, SEER reports suggest that the number of newly diagnosed cases of pancreatic cancer in the US for 2024 was 66,440, which accounted for 3.3% of all recently diagnosed cancer cases. Moreover, increasing use of endoscopic retrograde cholangiopancreatography (ERCP) procedures for pancreatic disease management is supporting segment expansion.

By Material Type

-

Metal Stent

In 2025, metal stent held the largest share in the global market, owing to their high longevity and better performance when compared to others. Metallic stents are used for the management of malignant obstructions in the gastrointestinal tract. The rising trend toward minimally invasive techniques for endoscopic procedures has contributed to the growing use of metallic stents.

-

Biodegradable Stent

Biodegradable stents segment is projected to grow at the fastest CAGR during the forecast period. This is due to the growing popularity of treatment systems that are convenient and innovative. Biodegradable stents break down naturally after performing their purpose in the body.

By Application

-

Biliary Disease

Biliary disease segment dominated the market in 2025, owing to the high incidence of diseases including bile duct obstruction and strictures, especially in elderly patients. GI stents are extensively used for the treatment of malignant and non-malignant cases of biliary obstruction. Increasing adoption of endoscopic procedures and rising incidence of pancreatic and liver-related disorders are supporting segment growth.

-

Colorectal Cancer

Colorectal cancer segment is projected to grow at the fastest CAGR during the forecast period, due to the rising global burden of colorectal malignancies and increasing preference for minimally invasive palliative treatments. Gastrointestinal stents are increasingly used to relieve obstruction and avoid emergency surgeries, especially in advanced-stage patients. Increasing awareness, screening programs, and development in stent technology are contributing to the fast expansion of this segment.

By End-Use Industry

-

Hospitals

Hospitals dominated the market in 2025, driven by the high volume of gastrointestinal procedures and availability of advanced endoscopic infrastructure. Hospitals provide treatment to serious cases of gastrointestinal diseases such as cancer that cause obstruction. Presence of skilled professionals, access to multidisciplinary care, and higher patient inflow are supporting segment growth.

-

Ambulatory Surgical Centers

Ambulatory surgical centers segment is projected to grow at the fastest CAGR during the forecast period, due to the increasing shift toward minimally invasive and outpatient procedures. These centers provide affordable procedures, shorter hospital stays, and faster recovery periods, thus becoming the preferred choice for the placement of GI stents. Rising healthcare cost pressures and growing preference for same-day procedures are accelerating segment expansion.

Source: Polaris Market Research Analysis

Regional Analysis

North America Market Assessment

North America gastrointestinal stent market dominated the global market in 2025, driven by high prevalence of colorectal cancer and strong awareness regarding minimally invasive treatment options. For example, based on the United States Cancer Statistics, the number of newly diagnosed patients with colorectal cancer was estimated to be 147,931 in 2022, while the mortality rate of colorectal cancer was 53,779 in 2023 in the US. The US holds the largest share of the market for GI stents in the North America region owing to well-established healthcare facilities along with high availability of advanced endoscopic techniques. The presence of key players and favorable reimbursement policies have improved access to therapy.

Asia Pacific Gastrointestinal Stent Market Insights

Asia Pacific gastrointestinal stent market is projected to grow at the fastest CAGR during the forecast period, driven by rising prevalence of gastrointestinal diseases. Countries such as India and China are seeing an increase in demand can be attributed to their developing healthcare infrastructure and increasing incidences of colorectal cancer. As stated by the National Library of Medicine in 2025, Asia was responsible for 50.2% of global colorectal cancers in 2022. In 2022, there were 966,400 new cases of which 462,300 cases had succumbed to the disease with a high mortality rate among young people accounting for 10%. Also, the rising government initiatives and expansion of endoscopic treatment facilities are supporting market growth.

Europe Gastrointestinal Stent Market Overview

Europe gastrointestinal stent market held the second-largest share, driven by advanced healthcare infrastructure and rising incidence of pancreatic cancers. For instance, in 2025, according to European Union, there was an increase in mortality rates associated with pancreatic cancer from 4.8% between 2013 and 2022 in Europe. Countries like Germany, France, and the UK are characterized by stable demand due to its developed healthcare facilities and availability of endoscopy. Growth in early diagnostic initiatives and introduction of novel stent technology are driving market growth.

LATAM & MEA Emerging Markets

Latin America and Middle East & Africa gastrointestinal stent market is growing steadily, supported by improvements in healthcare infrastructure and an increase in the number of gastrointestinal diseases and cancers. The emerging markets, including Brazil and South Africa, are penetrating higher in endoscopic procedures and specialized centers. Further, the rise in private healthcare establishments and the adoption of minimally invasive technology are contributing to market growth.

Source: Polaris Market Research Analysis

Competitive Landscape

Key Players & Competitive Strategies

The GI stents market exhibits moderate fragmentation, with global medical devices manufacturers and dedicated firms present in each product category. The competition depends on product quality, performance, and pricing. Companies within the market have been targeting innovation in stents and minimally invasive treatment options to bolster their presence in the market.

Some of the notable players in the market include Merit Medical Systems, Inc., ELLA-CS, s.r.o., Boston Scientific Corporation, Olympus Corporation, Cook Medical LLC, Medtronic plc, HOBBS MEDICAL, INC., Becton, Dickinson and Company, Taewoong Medical Co., Ltd., Micro-Tech (Nanjing) Co., Ltd., ENDO-FLEX GmbH, M.I.Tech Co., Ltd., and others.

Premium Insights

Comparison: Covered vs Uncovered Stents

| Parameter | Covered Stents | Uncovered Stents |

| Migration Risk | Higher | Lower |

| Tumor Ingrowth Prevention | High | Low |

| Flexibility | Moderate | High |

| Patency Duration | Longer | Shorter |

| Cost | High | Moderate |

| Complication Risk | Migration-related issues | Tumor ingrowth risk |

| Performance | Better obstruction control | Better anchoring |

| Application | Malignant strictures, palliative care | Biliary obstruction, long-term placement |

Source: Polaris Market Research Analysis

Technological Innovation

Technological advancements are reshaping the GI stent market, including:

- Increasing adoption of nitinol-based self-expandable metal stents (SEMS) due to superior flexibility, shape memory, and improved placement accuracy.

- Fast development of drug-eluting stents releasing medicines directly to the tumor location for controlling tumor growth and restenosis.

- Innovation of biodegradable gastrointestinal stents that require no removal process and are used for temporary therapy purposes.

- Innovation of anti-migration stents and hybrid stents for improving stability and ensuring lumen patency.

- Advances in technology used for coating stents to avoid infections, biofilms, and blockages caused by stents.

- Incorporation of AI-enabled and image-based insertion of stents into the body for improved outcomes.

Key Players

- Merit Medical Systems, Inc.

- ELLA-CS, s.r.o.

- Boston Scientific Corporation

- Olympus Corporation

- Cook Medical LLC

- Medtronic plc

- HOBBS MEDICAL, INC.

- Becton, Dickinson and Company

- Taewoong Medical Co., Ltd.

- Micro-Tech (Nanjing) Co., Ltd.

- ENDO-FLEX GmbH

- M.I.Tech Co., Ltd.

Industry Developments

- March 2026: Merit Medical Systems launched the Resilience Through-the-Scope (TTS) Esophageal Stent for the treatment of esophageal fistulas and strictures caused by malignant tumors. [source: www.globenewswire.com]

Gastrointestinal Stent Market Segmentation

By Product Type Outlook (Revenue, USD Million, 2021-2034)

- Biliary Stent

- Esophageal Stent

- Colonic Stent

- Pancreatic Stent

- Duodenal Stent

By Material Type Outlook (Revenue, USD Million, 2021-2034)

- Metal Stent

- Biodegradable Stent

- Plastic Stent

By Application Outlook (Revenue, USD Million, 2021-2034)

- Gastrointestinal Cancer

- Biliary Disease

- Colorectal Cancer

- Stomach Cancer

- Others

By End-Use Industry Outlook (Revenue, USD Million, 2021-2034)

- Hospitals

- Ambulatory Surgical Centers

- Others

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Gastrointestinal Stent Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 586.23 Million |

| Market Size in 2026 | USD 618.54 Million |

| Revenue Forecast by 2034 | USD 958.81 Million |

| CAGR | 5.62% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Gastrointestinal Stent Market FAQ's

The global market size was valued at USD 586.23 Million in 2025 and is projected to grow to USD 958.81 Million by 2034.

North America dominates the market driven by high prevalence of colorectal cancer and strong awareness regarding minimally invasive treatment options.

Major applications include gastrointestinal cancer, biliary disease, colorectal cancer, stomach cancer, and others.

A few of the key players in the market are Merit Medical Systems, Inc., ELLA-CS, s.r.o., Boston Scientific Corporation, Olympus Corporation, Cook Medical LLC, Medtronic plc, HOBBS MEDICAL, INC., Becton, Dickinson and Company, Taewoong Medical Co., Ltd., Micro-Tech (Nanjing) Co., Ltd., ENDO-FLEX GmbH, M.I.Tech Co., Ltd., and others.

Key drivers include rising number of gastrointestinal cancer and shift towards minimally invasive procedure.

Major demand comes from hospitals, and ambulatory surgical centers.

The market outlook remains strong due to development of biodegradable stents and expansion in emerging markets.

AI in GI stents enhances procedural precision through image-guided placement, and optimizes stent selection, by enabling predictive and real-time decision support.

Download Sample Report of Gastrointestinal Stent Market

Please fill out the form to request a customized copy of the research report.