Reports

Gene Therapy Market Opportunity, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Report Code:

PM1084

No. of Pages:

130

Format:

PDF

Published Date:

Base Year:

2025

Author:

Prajakta Bengale

Historical Data:

2021-2024

REPORT DETAILS

Report Code:

PM1084

Published Date:

No. of Pages:

130

Historical Data:

2021-2024

Format:

PDF

Author:

Prajakta Bengale

Base Year:

2025

ABOUT THIS REPORT

Gene Therapy Market Size, Share, Trends, Industry Analysis Report: By Therapeutic Area, Vector Type (Viral, Non-Viral), Approach, Route of Administration, and Region – Market Forecast 2026–2034

Gene Therapy Market Overview

Why Gene Therapy Is Reshaping Healthcare?

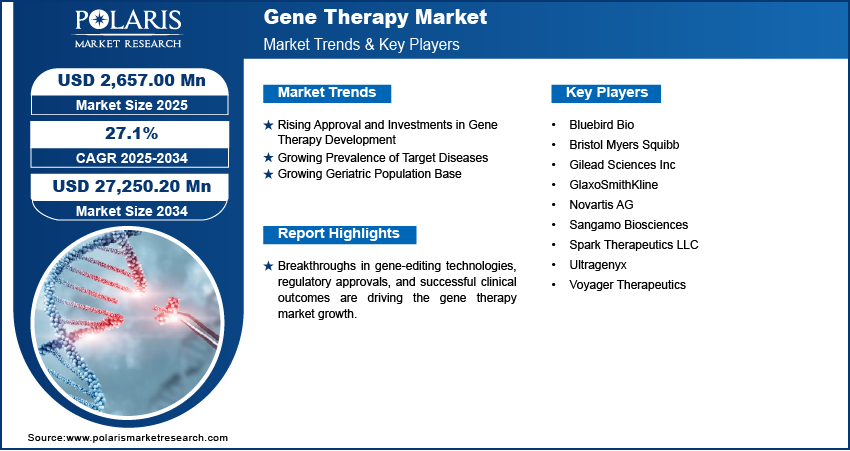

The global gene therapy market size was valued at USD 2.66 billion in 2025. The market is projected to grow from USD 3.29 billion in 2026 to USD 29.01 billion by 2034, exhibiting a CAGR of 27.1% during 2026-2035. Growing incidence of genetic diseases, advancements in emerging technologies such as gene delivery technology, increasing approvals for novel therapies, escalating investments in R&D, and expanding applications of personalized medicine are the major factors contributing to the growth of the industry.

Key Takeaways

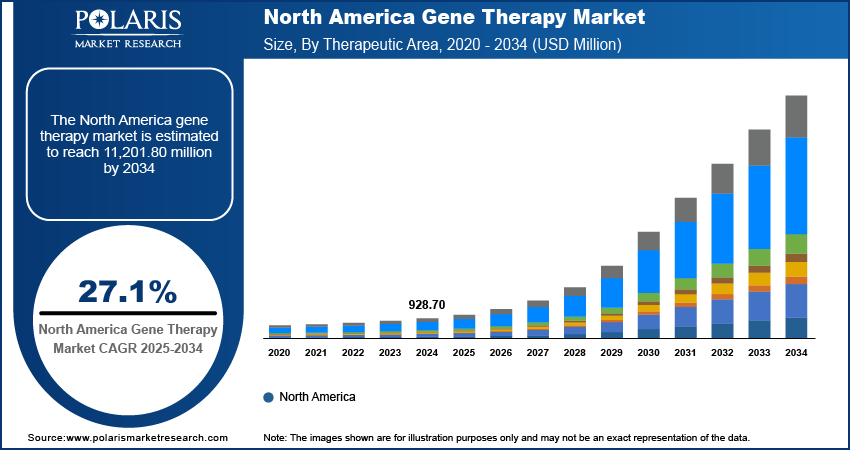

- North America led the market in 2025, supported by favorable regulatory policies, high R\&D funding, and a robust biopharmaceutical infrastructure that accelerates development and commercialization of advanced gene-based treatments.

- Europe ranked second in the market, fueled by comprehensive regulatory frameworks, sustained R\&D investment, and a rising number of therapy approvals enhancing treatment availability across the region.

- The hematological disorders segment is expected to grow at a CAGR of around 29.0%. Growth is driven by strong clinical success in treating conditions such as sickle cell disease and beta-thalassemia, along with increasing regulatory approvals and patient adoption.

- The oncological disorders segment captured approximately 38% of the market in 2025, driven by the global cancer burden and success of CAR-T cell therapies in treating hematologic cancers effectively.

- Viral vectors gene therapy are projected to grow at a 27.3% CAGR, owing to their strong cell-targeting ability, efficient gene delivery, and stable expression.

Market Statistics

- 2025 Market Size: USD 2.66 billion

- 2034 Projected Market Size: USD 29.01 billion

- CAGR (2026-2034): 27.1%

- North America: Largest market in 2025

Industry Dynamics

- The increasing incidence of genetic disorders and rare diseases, along with growing approvals of new oncology gene therapies, neurology gene therapies, hematology gene therapies is propelling the market growth.

- Growing clinical success of personalized treatments such as CAR-T (Kymirah and Yescarta) and Luxturna is increasing investor confidence and speeding up R&D activity, bringing gene therapy into the precision medicine spotlight.

- Substantial development costs and challenges in manufacturing and reimbursement continue to be significant barriers preventing greater access for patients and commercialization for manufacturers of gene therapy products worldwide.

- Advances in vector design, genome editing instruments and delivery systems are improving therapeutic efficiency and safety and contributing to the development of new methods and the wider clinical use-field.

What is Gene Therapy?

Gene therapy is a medical approach that modifies or replaces genes to treat diseases. It introduces genetic material into a patient’s cells. This is done using delivery systems such as viral or non-viral vectors. The goal is to correct faulty or missing genes. It helps restore normal cell function. In some cases, it can slow or stop disease progression. Gene therapy is used for genetic disorders, cancers, and certain chronic conditions. It targets the root reason of disease, which is different from treatments that only deal with symptoms.

Recent Technological Advancements in Gene Therapy

Major advances in vector design, production, and regulatory processes are accelerating commercial availability and enhancing therapeutic benefits in the market. Such improvements are enabling cost reduction, delivery accuracy and increase in potential patient population worldwide.

|

Recent Advances & Trends |

Recent Advances & Trends |

|

Improved rAAV vector design using AI-generated capsid libraries |

Enhances specificity and efficiency of gene delivery, enabling broader therapeutic applications. |

|

New scalable purification methods for full viral capsids (e.g., selective crystallization) |

Reduces production costs and improves yield, key for commercial scalability. |

|

Regulatory momentum & expanding clinical pipeline |

More approvals and advanced-stage programs drive broader adoption globally. |

To Understand More About this Research: Download Sample Report

Market Drivers, Challenges & Strategic Opportunities

Drivers

Regulatory momentum & increasing approvals

The market is primarily being driven by the positive regulatory momentum and rising number of approvals. The growing number of approved therapies to treat rare and debilitating diseases such as spinal muscular atrophy (SMA) and hemophilia helps build confidence in these therapies. This promotes further adoption in the clinic, draws new investment and inspires health care systems to pay for reimbursement. Accelerated approvals also contribute to the faster delivery of more transformative treatments to patients, further driving market growth and access on a global scale.

|

Year |

Number of FDA Gene Therapy Approvals |

Examples of Approved Therapies |

|

2023 |

8 |

Zynteglo, Luxturna |

|

2024 |

15 |

Skysona, Roctavian |

|

2025 |

20 |

ITVISMA, KEBILIDI |

Source: FDA

Growing burden of genetic and rare diseases

Increasing prevalence of genetic and rare diseases is the major factor propelling the market growth. Many patients experience diseases such as hemophilia, muscular dystrophy and many other rare metabolic diseases for which effective treatment options are minimal or non-existent. Improved genetic testing and earlier diagnosis are leading to identification of such disorders at an earlier stage, thereby driving the need for novel therapies. Gene therapy has the potential for long-term or even curative effects to help improve quality of life and mitigate the inherent long-term challenges of disease management.

Challenges

High cost per therapy and affordability barriers

Gene therapies are some of the expensive treatments worldwide, with costs commonly reaching the millions of dollars for a one-and-done dose. These high prices are the result of long research and development (R&D) cycles, custom manufacturing, small patient populations, and the possibility of one-time curative effects. But such pricing strategy poses major challenges to affordability for patients, insurers and health systems. Budgetary limitations, reimbursement negotiations, and restrictive coverage policies limit access and impede broader market penetration.

Manufacturing complexity and supply chain constraints

Production of gene therapies is a technologically advanced and strictly controlled process that requires scientific expertise, particularly in the case of producing viral vectors such as AAVs. Consistent with the load, purity and scalability is a major process challenge. High complexity quality standards, long lead times, and constrained production capacity on a global scale put additional stress on the supply chains. Any change in availability of materials or regulatory issues delay timelines and increase costs. These manufacturing and logistical hurdles slow commercialization efforts, making it difficult to meet rising market demand for high-quality, reliable gene therapy products.

Opportunities

Expanding into more common diseases

Improvements in vector design, safety, and delivery are enabling gene therapy to be considered for larger populations of patients. With the scale-up of manufacturing capabilities and treatment protocols, gene therapy has the potential to move beyond rare diseases and address more common genetic susceptibility and chronic diseases, representing an increased market opportunity and driving wider clinical adoption in mainstream healthcare.

Alternative payment models

Novel pricing strategies, including outcome-based contracts, an annuity-based payment plan over multiple years, and risk-sharing agreements among manufacturers and insurers, can help mitigate financial burden associated with high initial therapy costs. These arrangements provide payers with the opportunity to better align spending with the actual benefits to patients in real life situations, making them more affordable, opening up reimbursement routes and facilitating broader access to potentially life-changing gene therapies.

Segment Analysis

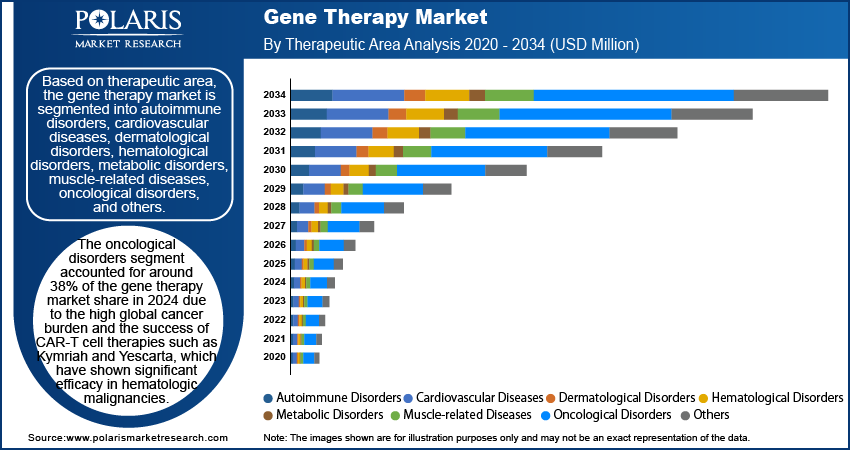

Gene Therapy Market Assessment by Therapeutic Area Outlook

Autoimmune Disorders: The autoimmune disorders segment is gaining considerable momentum because gene therapies seek to restore immune balance and avoid chronic tissue damage. They provide sustained symptom relief and less reliance on long-term immunosuppressive medication, which is likely to fuel broader clinical interest in many debilitating autoimmune diseases.

Cardiovascular Diseases: Cardiovascular indications are rapidly emerging among novel therapies aimed at stimulating heart muscle repair and regenerating blood vessels and involve the restoration of functional genes.

Dermatological Disorders: Skin disorder-focused gene therapy steadily advancing by repairing genetic skin abnormalities and enhancing wound healing in devastating disorders such as epidermolysis bullosa. Observable therapeutic outcomes and site-specific administration for a faster recovery time make skin regeneration as a research driver.

Hematological Disorders: Hematologic indications are progressing with an impressive pipeline of transformational cures for sickle cell disease and beta-thalassemia. Durable therapeutic responses, less need for transfusions, and approvals from regulatory bodies are continually boosting commercial adoption and payer acceptance.

Metabolic Disorders: The metabolic disorders segment is evolving as a focus segment on account of severe genetic enzyme deficiencies and lack of conventional treatment options. Gene therapy for a metabolic disease corrects underlying metabolic defect, with better long-term survival outcomes and improved disease management for these patients.

Muscle-Related Diseases: Neuromuscular and muscle-related products are developing rapidly with a number of potential therapies seeking to restore key structural proteins and slow muscle loss. The high unmet need in diseases such as Duchenne muscular dystrophy illustrates the need to continue advancing transformative gene based therapies.

Oncological Diseases: The oncology segment continues to account for the largest share of the overall market, and is best known for its use of gene modified immune cells that specifically target cancer cells. It represented ~38% of the gene therapy market in 2025 due to strong clinical achievement and investment support.

Others: Niche sections such as rare neurological, ophthalmic, and immune deficiencies are also gaining traction as innovations move into wider disease applications. Growing research, better diagnostics, and more treatment approvals are driving adoption in this niche but essential therapeutic areas.

Gene Therapy Market Evaluation by Vector Type Outlook

Viral Vectors: Viral vectors have dominated the market as a result of potent transduction efficiency and long-lasting gene expression. In general, AAV-based therapies are much more favored for in vivo gene therapy applications while retroviral/lentiviral vector demands for ex vivo modified cell therapies, such as those for hematologic and oncology indications, are increasing. However, the viral vectors manufacturing bottleneck continues to challenge large-scale production and supply.

Non-Viral Vectors: Non-viral vectors gene therapy are gaining traction due to the safe and scalable alternatives they provide without the risk of insertional mutagenesis. Such as lipid nanoparticles, polymer carrier and CRISPR-based delivery, are being developed to enhance targeted gene transfer for repeated dosing and expanded therapeutic access.

Gene Therapy Market Evaluation by Approach Outlook

Gene Augmentation: The gene therapy segment is witnessing growth during forecast period, as it addresses the underlying cause of a number of inherited disorders by introducing functional genes. Its durable one-time effect in hemophilia and retinal diseases is propelling clinical adoption and further investment in rare disease gene therapies market.

Oncolytic Viral Therapy: Oncolytic viral therapy is currently exerting strong momentum by preferentially killing tumor cells and inducing immune activation. The segment has witnessed a growing number of investors/funds and clinical trials attracted to the gene therapy for oncology-focus, benefitting from positive results in solid tumors as well as its use alongside standard of care.

Immunotherapy: Gene therapies based on cancer immunotherapy are also progressing rapidly with engineered immune cells providing targeted cancer destruction. The phenomenal success in hematologic cancers and solid tumors are establishing this segment as a major growth driver within the gene therapy space.

Other Approaches: Emerging gene therapy are gradually gaining traction with gene editing, RNA modulation and gene silencing platforms. Their flexibility to treat complex diseases without permanently modifying the DNA expands utility and drives innovation in numerous therapeutic areas.

Gene Therapy Types and Uses

|

Therapy Type |

Uses |

|

Gene Augmentation |

Used to replace missing or faulty genes in inherited disorders |

|

Oncolytic Viral Therapy |

Used to target and destroy cancer cells while activating immunity |

|

Immunotherapy |

Used to modify immune cells to recognize and attack cancer |

|

Gene Editing |

Used to correct specific genetic mutations at DNA level |

|

RNA-based Therapy |

Used to regulate or silence harmful gene expression |

Gene Therapy Market Regional Analysis

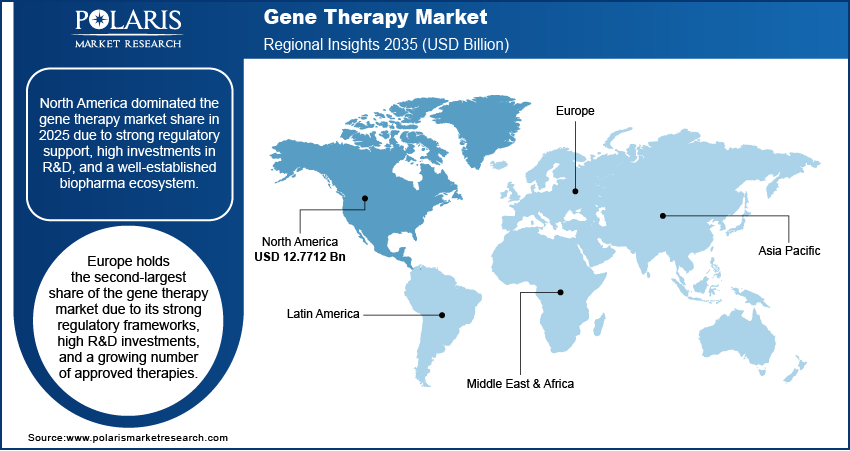

North America: North America gene therapy market is anticipated to be largest growing during forecast period. This is fueled by strong regulatory policies, high number of investments in R&D and the presence of a robust biopharma ecosystem. The FDA has also authorized a number of gene therapies, such as Luxturna for treating a rare form of inherited blindness and Zolgensma for spinal muscular atrophy. In 2023, the U.S represented more than 65% of global gene therapy clinical trials, backed by NIH and private funding in excess of USD 10 billion. The U.S gene therapy spending remains the highest globally, driven by extensive clinical research funding, advanced biotechnological infrastructure, and strong market demand.

Leading biotech hubs including Boston and San Francisco, and established players like Novartis, Bluebird Bio and Sarepta, are driving innovation in the market in North America. The region is further supported by sophisticated manufacturing facilities, reimbursement systems, and expanding patient access to gene therapies.

Europe: Europe is the second largest in terms of revenue contributor to the market due to its rigid regulatory scenarios, high research and development spending coupled with increasing number of therapies going approval. Several gene therapies including Skysona, Libmeldy and Roctavian have also been approved by the European Medicines Agency (EMA) which is further contributing towards market growth.

Countries like Germany, France and UK are at the forefront of clinical trials, underpinned by government-supported schemes such as Horizon Europe geared towards promoting advanced therapies.

In addition, the region has a well-established biopharma ecosystem, with orchard therapeutics and uniQure amongst the key players. Expansion of manufacturing capacity, coupled with rising adoption of value-based reimbursement models is another factor anticipated to reinforce Europe’s market position.

However, Europe pricing challenges remain a significant barrier, affecting patient access and reimbursement decisions, which could slow the overall market growth despite strong clinical and regulatory progress.

Asia Pacific: Asia Pacific is expected to grow significantly during the forecast period. This is due to rising incidence of chronic and genetic diseases, such as multiple cancers and rare diseases, is increasing the need for novel therapeutics. Top-tier nations including China, Japan, South Korea, and India possess enabling government initiatives, high biotechnology investment, and less strict regulatory procedures that facilitate clinical trials and product approval. Further, China's recent gene therapy approvals and Japan's evolving regulatory landscape, combined with supportive policies across Asia Pacific, are driving significant growth in the region's gene therapy market.

The region has the potential to be the key source of R&D, manufacturing and partnership in gene editing and cell therapy, with many global and local biotech companies on board. Market growth is driven by technological advancements in vector development, increasing number of clinical pipelines and patient population, although there are market challenges, including high costs and ethical issues, making Asia Pacific gene therapy market expansion.

Regional Heat Map Analysis – Gene Therapy Market

|

Region |

Market Attractiveness |

Key Highlights |

|

North America |

★★★★★ |

Dominant market; strong regulatory approvals; high therapy adoption; major biotech hubs |

|

Europe |

★★★★☆ |

Extensive clinical trials; strong reimbursement efforts; growing rare disease focus |

|

Asia Pacific |

★★★★☆ |

Increasing investments; expanding healthcare access; rapid clinical development in major economies |

Gene Therapy Market Key Players and Competitive Analysis Report

The competitive landscape of the market is marked by a blend of global leaders and regional players striving to capture market share through innovation, strategic partnerships, and geographic expansion. Major players such as Abeona Therapeutic; Novartis AG; Spark Therapeutics LLC; Gilead Sciences Inc.; Bristol Myers Squibb; Adverum Biotechnologies; Alnylam Pharmaceuticals; American Gene Technologies; Applied Genetic Technologies Corporation; Biogen; and Ultrageny dominate the market by leveraging their strong research and development (R&D) capabilities and vast distribution networks. These companies focus on product innovation to enhance efficiency, scalability, and reliability, addressing the growing demand for advanced automation solutions. Simultaneously, regional players are capitalizing on local market needs, providing customized and cost-effective ASRS solutions. Competitive strategies such as mergers, acquisitions, collaborations with tech firms, and expanding product portfolios are common approaches to enhance gene therapies market share and meet the diverse demands of industries. The robust late-stage pipeline, ongoing clinical trials, and strategic partnerships, along with the growth of contract development and manufacturing organizations (CDMOs), are further fueling expansion and innovation across the gene therapy market.

Companies Pipeline Analysis

|

Indication Area / Vector Type |

Preclinical |

Phase I |

Phase II |

Phase III |

Approved |

|

Hemophilia (AAV) |

BioMarin, Spark |

Pfizer, CSL Behring |

UniQure |

BioMarin, Pfizer |

BioMarin (Roctavian) |

|

Neuromuscular Disorders (AAV) |

Sarepta, Regenxbio |

Sarepta |

Sarepta, Audentes/AskBio |

Sarepta |

Novartis (Zolgensma) |

|

Inherited Retinal Diseases (AAV) |

MeiraGTx, 4DMT |

4DMT, AGTC |

Roche/Spark |

Roche/Spark |

Roche/Spark (Luxturna) |

List of Key Companies :

- Sangamo Biosciences

- Voyager Therapeutics

- Ultragenyx

- GlaxoSmithKline

- Gilead Sciences Inc

- Bristol Myers Squibb

- Novartis AG

- Spark Therapeutics LLC

- Bluebird Bio

Market Development

November 2025: Novartis' FDA approval of Itvisma, a one-time intrathecal gene therapy, treats SMA in children 2+, teens, and adults by replacing the SMN1 gene, improving motor function per Phase III STEER/STRENGTH studies. (Source: novartis.com

September 2024: Genprex, Inc. announced its intention to spin off a business to Develop gene therapy treatments for diabetes (type-1 and type-2 models). (Source: genprex.com

May 2025: Ensoma, Inc. received U.S. FDA clearance for its IND application for EN-374. It is an in vivo HSC-directed gene insertion therapy. It targets X-linked chronic granulomatous disease (X-CGD), a rare genetic disorder. Source: (ensoma.com)

April 2024, the President of India, Smt Droupadi Murmu, launched the first indigenous gene therapy for cancer in India at IIT Bombay. (Source: pib.gov.in)

Pricing Models, Reimbursement & Market Access Landscape

|

Region |

Pricing Range |

Reimbursement Landscape |

Market Access Factors |

|

North America (USA) |

USD 300,000 to over USD 4 million per treatment |

Medicare/Medicaid increasing coverage; outcome-based reimbursement models; amortized payments and risk-sharing emerging |

Advanced regulatory pathways; payer scrutiny; focus on affordability and long-term value |

|

Europe |

Approx. USD 583.50 to USD 2,334 billion (might varies by country) |

Adaptive EMA pathways; some outcome-based contracts; reimbursement inequalities across countries |

Decentralized manufacturing initiatives; EU Health Technology Assessment regulation shaping access |

|

Asia Pacific |

~ USD 24,100 to USD 60,250 million |

Limited coverage but improving; emerging value-based and outcomes-based models in Japan, South Korea, China |

Streamlined approvals; growing biotech investment; increasing local manufacturing capacity |

Future Outlook & Scenario Forecasts

From an analyst perspective, the market opportunities are characterized by rapid innovation and expanding therapeutic applications, driven by emerging technologies and personalized medicine. The market is anticipated to develop with enhanced regulatory guideline, increasing amount of collaboration/partnership from biotech company and healthcare provider.

Challenges to access and affordability may also drive the emergence of new pricing and reimbursement models that are based on long-term clinical outcomes. The industry is expected to place greater emphasis on scalable production to satisfy demand and ethical and safety concerns remain critical to the development process. In summary, forecast scenario in gene therapy has the potential to transform treatment approaches for rare and chronic diseases with wide-ranging effects on global healthcare systems.

Market Segmentation

By Type Therapeutic Area Outlook (Revenue, USD Billion, 2021–2034)

- Autoimmune Disorders

- Cardiovascular Diseases

- Dermatological Disorders

- Hematological Disorders

- Metabolic Disorders

- Muscle-related Diseases

- Oncological Disorders

- Others

By Vector Type Outlook (Revenue, USD Billion, 2021–2034)

- Viral

- Non-Viral

By Approach Outlook (Revenue, USD Billion, 2021–2034)

- Gene Augmentation

- Oncolytic Viral Therapy

- Immunotherapy

- Other Approaches

By Route of Administration Outlook (Revenue, USD Billion, 2021–2034)

- Intraarticular

- Intracerebellar

- Intradermal

- Intramuscular

- Intratumoral

- Intravenous

- Intravesical

- Intravitreal

- Subretinal

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future of Gene Therapy Market

The market is expected to expand with increasing approvals and stronger clinical pipelines. Advances in vector design and gene editing will improve safety and delivery efficiency. Expansion into common diseases will rise patient pool and demand. Manufacturing scale-up and cost reduction remain key focus areas. Growth will also be supported by partnerships, funding, and evolving reimbursement models.

Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2025 |

USD 2.66 billion |

|

Market Size Value in 2026 |

USD 3.29 billion |

|

Revenue Forecast by 2034 |

USD 29.01 billion |

|

CAGR |

27.1% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The gene therapy market recorded a revenue of USD 2.66 billion in 2025.

The market is expected to grow at a CAGR of 27.1% during the forecast period 2026-2034. The market is projected to reach a value of 29.01 by 2034.

Gene therapy targets the root cause of diseases. It can provide long term or one time treatment. It reduces dependence on ongoing medications.

There can be immune reactions and side effects. Delivery challenges and high costs are also concerns. Long term safety is still being studied.

Common types include gene augmentation, gene editing, and immunotherapy. Oncolytic viral therapy is also widely used.

Gene therapy is delivered using viral or non viral vectors. These systems support transfer genetic material into target cells.

It is used for genetic disorders, cancers, and rare diseases. Conditions like hemophilia, muscular dystrophy, and certain blood disorders are key areas of use.

Page last updated on: Apr-2023

Download Sample Report of Gene Therapy Market

Please fill out the form to request a customized copy of the research report.