Gene Delivery Technologies Market Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Gene Delivery Technologies Market Size and Growth Outlook

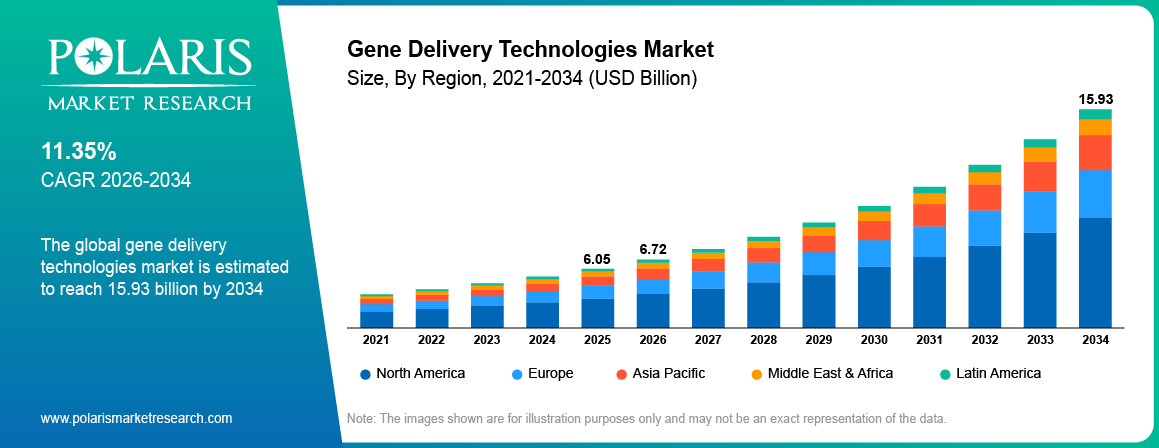

The gene delivery technologies market was valued at USD 6.05 billion in 2025. The market is projected to grow at a CAGR of 11.35% from 2026 to 2034. Rising demand for gene therapy and growing prevalence of genetic disorders and chronic diseases worldwide are driving the market growth.

Market Statistics

Gene Delivery Technologies Market Key Takeaways

- North America led with a 41.9% share in 2025. The high adoption of advanced viral and non-viral delivery systems contributes to the regional market dominance.

- Asia Pacific is projected to witness the fastest growth at a 13.2% CAGR. Rising patient population and awareness drive the regional market growth.

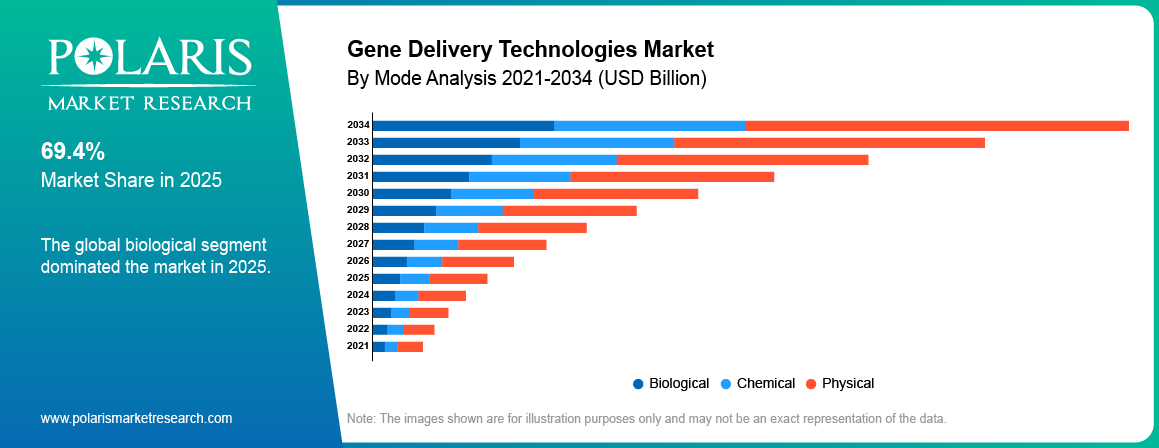

- The Biological segment dominated with a 69.4% share in 2025. The segment’s dominance is driven by high adoption of viral vector-based gene delivery systems.

- The In Vivo segment is projected to grow at a 13.8% CAGR. This is owing to the growing demand for direct gene delivery to patients.

- The Infectious Diseases segment led with a 36.7% share in 2025. The segment’s leading position is driven by the adoption of gene-based vaccines and therapies.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Gene Delivery Technologies Market Drivers, Opportunities and Challenges

- Rising demand for gene therapy for rare and chronic diseases is driving the adoption of advanced gene delivery solutions.

- Growing prevalence of genetic disorders worldwide is increasing awareness and use of targeted gene delivery technologies.

- High cost of gene therapy development and safety concerns related to viral vectors remain major market challenges.

- Innovations in non-viral vectors, CRISPR therapies, and AI-based delivery systems are opening new avenues for growth.

AI Impact on Vector Design, Formulation and Gene Delivery Manufacturing

- Artificial intelligence is enhancing the development of gene delivery technologies through bio-data analysis to pinpoint efficient delivery vectors and optimize the formulation design process.

- The use of machine learning algorithms helps identify the right delivery methods based on the prediction of gene transfer efficacy, accuracy, and safety profile.

- Artificial intelligence allows for faster research and manufacturing processes without compromising on the quality of the products produced.

- The technology is useful in clinical development due to patient selection and therapeutic outcome analysis.

Gene Delivery Technologies Market Definition and Scope

Gene delivery technologies provide the possibility of targeted delivery of therapeutic genes to cure genetic disorders and chronic illnesses. These technologies encompass viral and non-viral vectors, CRISPR systems, and RNA therapies, which are frequently combined with digital platforms and AI tools to maximize precision, efficiency, and personalized treatment outcomes.

Increasing demand for gene therapy driven by orphan and chronic conditions, as well as rising prevalence of genetic conditions worldwide, is pushing the adoption of next-generation gene delivery products. Patients and healthcare professionals are increasingly adopting such technologies to improve treatment outcomes and personalized care.

Source: Polaris Market Research Analysis

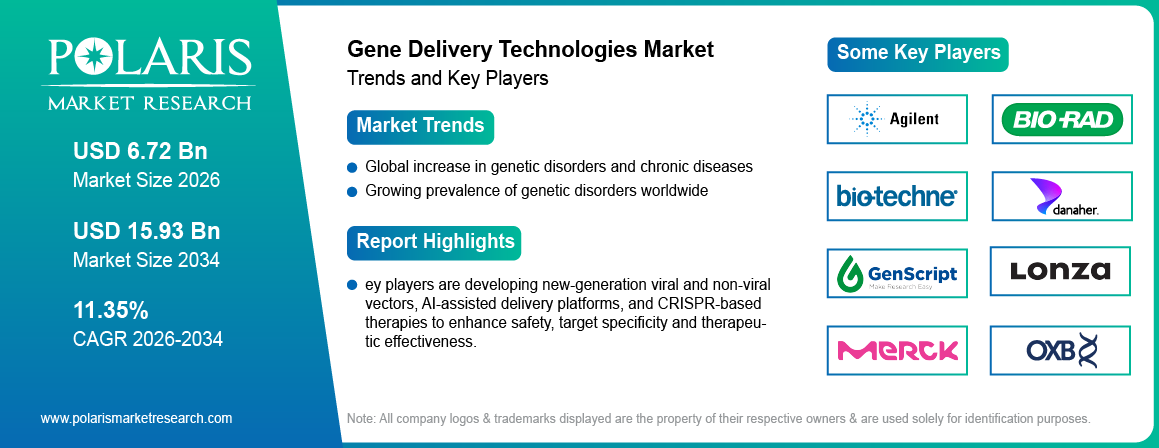

Key players are developing new-generation viral and non-viral vectors, AI-assisted delivery platforms, and CRISPR-based therapies to enhance safety, target specificity and therapeutic effectiveness. For instance, in August 2025, HORIBA and Fujifilm jointly developed a gene delivery system for improved productivity in gene therapy manufacturing for streamlining and up-scaling production of therapeutic genes. Increasing clinical trials, research collaborations with biotech firms and research institutes, and burgeoning market expansion are creating new markets for expansion.

How Do Gene Delivery Technologies Work?

Identification of Target – Researchers first decide which disease or condition necessitates treatment through genes.

Selection of Gene – The genes or DNA/RNA molecules are selected for transport into the target cells.

Selection of Delivery Method – A proper viral or non-viral vector is selected depending on the therapy and target site.

Delivery of the Gene – The gene is transported into the body cells by the selected method of delivery.

Cellular Uptake – The target cells take in the genetic material and start processing it.

Therapeutic Outcome – The delivered gene aids in restoration, replacement, or regulation of cellular functions in the treatment of the disease.

Viral vs. Non-Viral Gene Delivery Technologies: Efficiency, Safety and Capacity

| Feature | Viral Vector Delivery System | Non-viral Vector Delivery System |

| Delivery Efficiency | High | Moderate |

| Safety | Possibility of inducing an immune response | Low possibility of immune response |

| Mode of Delivery | Delivers using modified viruses | Delivers using lipids, nanoparticles, polymers, or physical methods |

| Capacity of Gene | Limited by size of the viral vector | Large capacity of gene to be delivered |

| Applications | Gene therapy, vaccines | Drug delivery, research, regenerative medicine |

Source: Polaris Market Research Analysis

Drivers & Opportunity

Global increase in genetic disorders and chronic diseases: Growing incidence of genetic disorders and chronic diseases is driving demand for novel gene delivery technologies. World Health Organization (WHO) in its latest report states that non-communicable diseases were responsible for 43 million deaths in 2021 and contributed 75% of total deaths worldwide, most of which were early deaths occurring in low- and middle-income countries. Patients increasingly turn to targeted therapies for illnesses such as cystic fibrosis, hemophilia, and muscular dystrophy. Physicians are embracing accurate and effective delivery systems to enhance outcomes. This trend is stimulating investment and speeding up adoption around the globe.

Growing prevalence of genetic disorders worldwide: The rising incidence of genetic disorders is driving the need for safe and efficient gene delivery systems. National Organization for Rare Disorders (NORD) states that approximately 25–30 million Americans, about 10% of the population, suffer from rare diseases that impact fewer than 200,000 people each. Growing awareness of hereditary diseases is driving healthcare systems toward personalized medicine. Non-viral and viral delivery systems are gaining more traction. The growing patient population is propelling the research for next-generation delivery technologies for wider applications.

Technological Advancements in Gene Delivery

There have been several technological advancements that are enhancing the effectiveness of gene delivery therapy systems. Efforts are being made to develop improved viral vector technology that is more specific and to lower the immune response against these viral vectors. Other methods of gene delivery, such as lipid nanoparticles and polymers, are gradually becoming more effective in delivering the gene into cells. There have been advancements in genome editing technology like CRISPR, and these are resulting in an increased use of gene delivery systems in genetic diseases. Improvements in automation and manufacturing are helping develop high-quality gene delivery systems.

Gene Delivery in Cell Therapy

Gene delivery technologies form a significant component of cell therapy since they deliver genetic material into the cells that are later infused back into the patients. Gene delivery is widely used to modify immune cells and allow them to be better at fighting diseases, including cancers. Scientists select either viral or non-viral gene delivery technologies depending on cell type and treatment. In addition, they continue to refine the delivery process to ensure its efficacy while not harming the functionality of cells. These developments are making cell therapies more effective, which is expected to increase the need for gene delivery technologies.

Gene Delivery Manufacturing Challenges

Manufacturing gene delivery systems is complex and requires specialized manufacturing facilities and rigorous quality control procedures. Manufacturing of viral vectors and other gene delivery systems has to be carried out with care to ensure high quality and consistency. Increased production levels may not be easy and require significant investment to be achieved. Companies are required to fulfill certain regulatory requirements on safety and quality before gene therapy products can be made available to the end users. Expensive manufacturing processes are among the challenges facing the sector. Improvements in manufacturing technologies are playing a part in overcoming these challenges.

Source: Polaris Market Research Analysis

Sustainable Gene Therapy Manufacturing

Sustainability is emerging as one of the key aspects of the manufacturing of gene delivery products. Companies have been optimizing their manufacturing processes to conserve energy, minimize wastage, and use raw material resources optimally. In addition to increasing efficiency, automation of manufacturing processes leads to resource savings because the errors associated with production are minimized. Scalable manufacturing systems have also been implemented in some firms to make manufacturing more efficient without impacting product quality.

Gene Delivery Technologies Market Segment Analysis

Mode Analysis

In terms of mode, the segment comprises of biological, chemical, and physical. The biological segment dominated the market in 2025, driven by high adoption of viral vector-based gene delivery systems. Moreover, increasing use in treating rare genetic disorders and chronic diseases is reinforcing market growth globally.

The chemical segment is expected to register the highest growth CAGR over the forecast period, owing to increasing innovations in non-viral chemical vectors. Further, better safety profiles and efficacy are boosting adoption in research and clinical applications.

Method Analysis

Based on method, the segmentation includes ex vivo, in vivo, and in vitro. The ex vivo segment led the market in 2025 owing to extensive application in the alteration of patient-derived cells prior to transplantation. Additionally, utility in personalized gene therapy is propelling continuous adoption in hospitals and research institutes.

In vivo segment witnessed the highest CAGR during the forecast period with the growing demand for direct gene delivery to patients. In addition, developments in viral and non-viral vectors are improving therapeutic outcomes globally.

Application Analysis

Based on application, the segmentation includes infectious diseases, oncology, ophthalmology, urology, diabetes, CNS, and others. The infectious diseases segment dominated the market in 2025, driven by the adoption of gene-based vaccines and therapies. Moreover, growing incidence of viral and bacterial infections is encouraging adoption of efficient gene delivery platforms.

The oncology segment is expected to grow at the highest CAGR during the forecast period, driven by growing use of gene therapy in the treatment of cancer. As per the WHO, the worldwide cancer incidence set to rise from 20 million in 2022 to over 35 million by the year 2050, with 9.7 million deaths and 53.5 million five-year or shorter survivors.

End User Analysis

Based on end user, the segmentation includes academic & research institutes, pharmaceutical & biotechnology companies, and other end users. Academic and research institutes dominated the market in 2025 due to extensive use of gene delivery technologies for laboratory and experimental studies. Moreover, funding for genetic research and collaborative programs is boosting segment adoption globally.

The pharmaceutical and biotechnology companies’ segment is projected to grow at the fastest CAGR during the forecast period, supported by increasing development of gene therapies and clinical trials. In addition, strategic partnerships are accelerating commercialization of advanced delivery platforms.

Source: Polaris Market Research Analysis

Regulatory Landscape of Gene Delivery Technologies

The use of gene delivery technology is subject to strict regulatory guidelines that must be met for its use within clinical settings. Regulatory bodies conduct a rigorous examination of the research studies, manufacturing procedures, and clinical trial findings to guarantee the safety and efficacy of the treatments. Companies are also expected to adhere to high-quality standards at every stage of drug development and production. With evolving gene therapies, the regulatory framework is constantly evolving to provide support to emerging gene delivery technologies. Clear approval processes are expected to drive the growth of the gene delivery technologies market.

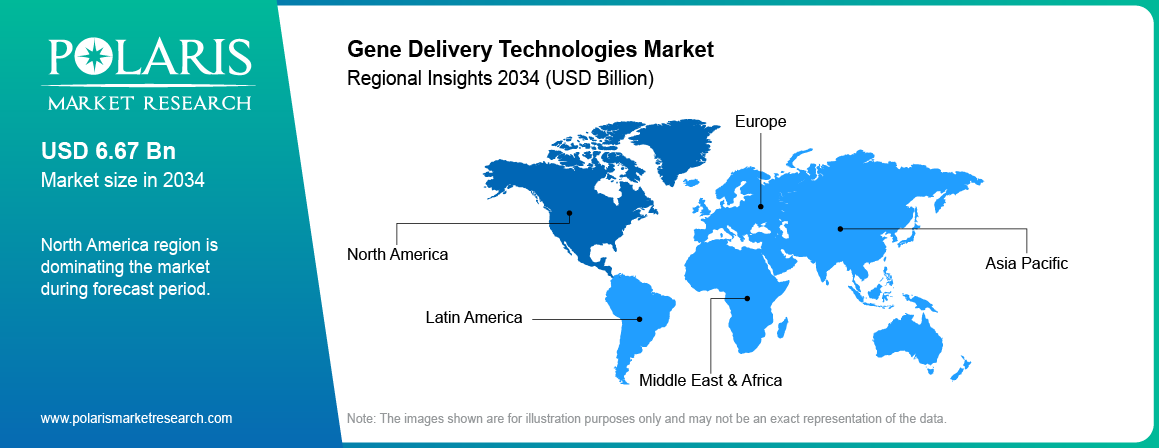

Regional Analysis

North America led the gene delivery technologies market due to high adoption of advanced viral and non-viral delivery systems. Moreover, well-established healthcare infrastructure and strong R&D investments are driving innovation. In addition, supportive government regulations for gene therapy are encouraging market expansion.

The U.S. Gene Delivery Technologies Market Insights

The U.S. dominated the gene delivery technologies industry due to increasing prevalence of genetic disorders and chronic diseases. According to the U.S. National health expenditure data, chronic diseases like heart disease, cancer, and diabetes are the main causes of death and disability in the U.S. and drive USD 4.9 trillion in yearly healthcare costs. Moreover, extensive clinical trial activity and biotechnology investments are promoting gene delivery technology adoption. In addition, favorable reimbursement policies are supporting widespread use in hospitals and research centers.

Europe Gene Delivery Technologies Market Insights

Europe holds the substantial share in the gene delivery technologies market owing to adoption of gene therapies for rare and chronic disorders. Moreover, strong pharmaceutical and biotechnology sectors are supporting technology integration. In addition, increasing clinical trials across major countries are expanding market opportunities.

Asia Pacific Gene Delivery Technologies Market Insights

Asia Pacific is the fastest growing market driven by rising awareness of gene therapies and growing patient population for genetic disorders. Nizam's Institute of Medical Sciences (NIMS) in Hyderabad, India witnessed a 418% increase in genetic disorder cases in the past decade, with 12,042 patients treated for rare genetic ailments in 2025, mainly because of increased awareness and diagnostic capabilities.

China Gene Delivery Technologies Market Insights

China is expanding owing to government programs favoring development in the field of gene therapy. In addition, rising rates of genetic disorders and huge patient population are driving demand. Additionally, partnerships between regional biotech companies and international players are strengthening market growth.

Source: Polaris Market Research Analysis

Future Outlook

The gene delivery technology market is expected to witness steady growth due to continuing developments in gene therapy, cell therapy, and personalized medicine. Improvements in technologies such as viral vectors, non-viral delivery technologies, and genome editing technologies have enhanced the efficacy and safety of therapies using genes. Clinical trial and approval activities will support the growth of the market. Investments in the biotechnology sector, along with manufacturing advances, is anticipated to solidify the market further. The growing adoption of personalized medicine will drive demand for gene delivery technologies.

Key Players & Competitive Analysis Report

The market for gene delivery technologies is moderately competitive, with players pushing viral and non-viral delivery platforms through AI implementation, CRISPR-based treatment, and digital tracking systems. Collaboration with research institutes, hospitals, and biotechnology firms also strengthens market reach, scalability, and adoption globally.

Key players in the market for gene delivery technologies are Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, Bio-Rad Laboratories, Inc., Agilent Technologies, Inc., Revvity, Inc., QIAGEN N.V., GenScript Biotech Corp., Takara Bio USA, Inc., Promega Corporation, Bio-Techne Corporation, Lonza Group AG, Oxford Biomedica PLC, Sartorius AG, and MaxCyte, Inc.

Key Players

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Bio-Techne Corporation

- Danaher Corporation

- GenScript Biotech Corp.

- Lonza Group AG

- MaxCyte, Inc.

- Merck KGaA

- Oxford Biomedica PLC

- Promega Corporation

- QIAGEN N.V.

- Revvity, Inc.

- Sartorius AG

- Takara Bio USA, Inc.

- Thermo Fisher Scientific Inc.

Industry Development

- May 2026: Dyno Therapeutics, Inc. introduced two new adeno-associated virus (AAV) gene delivery capsids for muscular delivery and central nervous system (CNS). The company also announced updated in vivo results for previously released capsids Dyno-yp2 (CNS) and Dyno-bn8 (muscle). Updates to its AI platform for genetic medicine market were also highlighted.(source: businesswire.com)

- April 2026: Dyno Therapeutics, Inc. announced a capsid license exercised by Astellas Pharma Inc. for skeletal muscle-targeted gene delivery. The company stated that the development marked Dyno’s second capsid licensed from its AI-powered sequence design platform. It positioned Dyno as the first firm to successfully license an AI-designed AAV capsid for both central nervous system and muscle gene therapies.(source: businesswire.com)

- August 2025: Merck KGaA partnered with Skyhawk Therapeutics in a deal worth up to USD 2 billion to advance RNA-targeting gene delivery technologies for neurological diseases.

- May 2025: GenScript launched a GMP-like mRNA manufacturing platform to accelerate early-stage drug development and gene delivery research.

- April 2025: Thermo Fisher Scientific launched its first U.S. cell and gene therapy collaboration center to advance process development and manufacturing for gene delivery and therapeutic applications.

Gene Delivery Technologies Market Segmentation

By Mode (Revenue, USD Billion, 2021–2034)

- Biological

- Adenovirus

- Retrovirus

- AAV

- Lentivirus

- Other Viruses

- Non-viral

- Chemical

- Physical

By Method (Revenue, USD Billion, 2021–2034)

- Ex vivo

- In vivo

- In vitro

By Application (Revenue, USD Billion, 2021–2034)

- Infectious Diseases

- Oncology

- Ophthalmology

- Urology

- Diabetes

- CNS

- Others

By End User (Revenue, USD Billion, 2021–2034)

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Other End Users

By Region (Revenue, USD Billion, 2021–2034)

- North America

- The U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

- Latin America

- Saudi Arabia

- UAE

- South Africa

- Israel

- Rest of South Africa

Gene Delivery Technologies Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 6.05 Billion |

| Market Size in 2026 | USD 6.72 Billion |

| Revenue Forecast by 2034 | USD 15.93 Billion |

| CAGR | 11.35% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021-2024 |

| Forecast Period | 2026-2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions and segmentation. |

Source: Polaris Market Research Analysis

Gene Delivery Technologies Market FAQs

The global market size was valued at USD 6.05 billion in 2025 and is projected to grow to USD 15.93 billion by 2034.

The global market is projected to register a CAGR of 11.35% during the forecast period.

North America dominated the gene delivery technologies market in 2025 due to high adoption of advanced gene therapy platforms and strong biotechnology infrastructure.

A few of the key players in the market are Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, Bio-Rad Laboratories, Inc., Agilent Technologies, Inc., Revvity, Inc., QIAGEN N.V., GenScript Biotech Corp., Takara Bio USA, Inc., Promega Corporation, Bio-Techne Corporation, Lonza Group AG, Oxford Biomedica PLC, Sartorius AG, and MaxCyte, Inc.

The biological segment was the market leader in 2025, led by widespread application of viral vectors in clinical gene therapy and ongoing investment in research on viral-based delivery.

The oncology segment is projected to grow fastest, supported by increasing clinical trials for cancer gene therapies and rising demand for targeted treatment solutions.

Gene delivery technologies are used to transfer DNA or RNA into the cells for both medical and research purposes. These technologies are very useful in the areas of gene therapy, cell therapy, vaccine development, and biomedical research.

The gene delivery systems that use viruses as delivery agents are known as viral gene delivery systems and are highly efficient in delivering genes to cells. Non-viral gene delivery systems use lipid-based nanoparticles or polymers as delivery agents.

Increasing demand for gene and cell therapies, investments in biotechnology research, and a growing number of clinical trials are the key factors driving market expansion.

Download Sample Report of Gene Delivery Technologies Market

Please fill out the form to request a customized copy of the research report.