Healthcare Command Centers Market Growth Drivers, Forecast, 2025-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Market Statistics

Overview

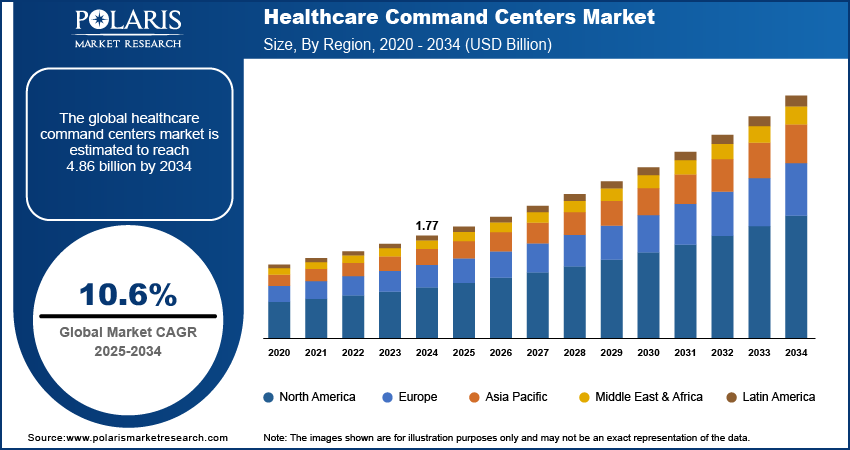

The healthcare command centers market was valued at USD 1.77 billion in 2024 growing at a CAGR of 10.6% from 2025-2034. Rising global healthcare spending along with government investments in smart healthcare & digital transformation is driving the industry.

Key Insights

- Hardware segment led in 2024 due to high adoption of real-time monitoring devices and centralized dashboards.

- Software segment is expected to grow fastest, driven by demand for AI-based analytics and integrated hospital management platforms.

- North America dominated in 2024 with strong presence of advanced healthcare command infrastructure.

- The U.S. led the region due to large-scale hospital modernization and adoption of digital command platforms.

- Asia Pacific is projected to grow fastest with expanding smart hospital projects and increasing digital health investments.

- China led APAC due to government-backed healthcare digitization and AI-driven hospital operations.

Industry Dynamics

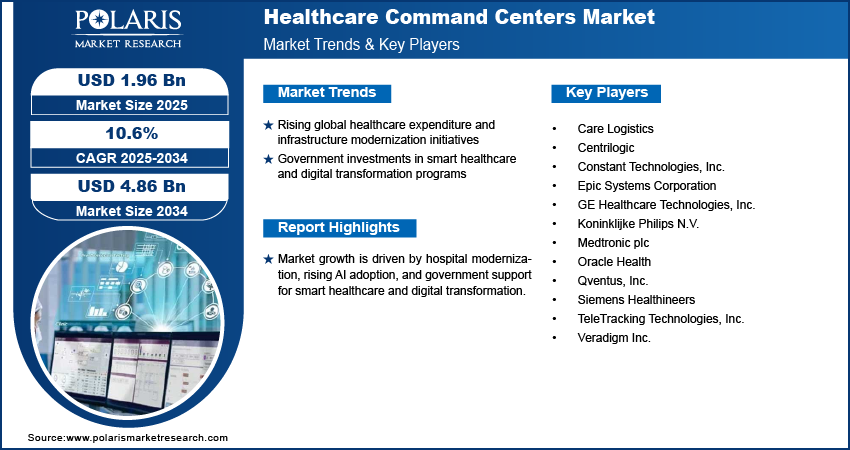

- Rising global healthcare expenditure and infrastructure modernization initiatives are driving adoption of healthcare command centers.

- Government investments in smart healthcare and digital transformation programs are increasing deployment of advanced command center platforms.

- High implementation costs and data privacy concerns remain key market challenges

- Predictive analytics, cloud integration, and digital twin technologies are opening new growth avenues.

Market Statistics

- 2024 Market Size: USD 1.77 Billion

- 2034 Projected Market Size: USD 4.86 Billion

- CAGR (2025-2034): 10.6%

- North America: Largest Market Share

Healthcare command centers are integrated platforms that monitor, coordinate, and streamline hospital operations, including patient flow, resource allocation, and clinical and non-clinical processes. Command centers are essential to provide operational effectiveness, patient safety, and decision-making and are shifting towards leveraging AI, predictive analytics, and cloud-based systems to derive real-time insights.

Growing worldwide healthcare expenditures, infrastructure replacement programs, and public spending on smart healthcare and digital business transformation projects are fueling the adoption of healthcare command centers. Hospital chains and healthcare networks are increasingly implementing such platforms to enhance patient throughput, optimize bed and staff utilization, and coordinate emergency and critical care operations. TeleTracking and Palantir partnered in January 2025 to enhance hospital command centers with AI-driven insights to manage real-time capacity, staffing, and patient flow.

Market leaders are offering advanced dashboards, predictive analytics platforms, and cloud platforms to meet emerging demands for operations. Growing hospital chains, increasing focus on patient-centric care and the expansion of digital health infrastructure in emerging economies are presenting new avenues for growth.

Drivers & Opportunity

Rising global healthcare expenditure and infrastructure modernization initiatives: Increasing healthcare spending is enabling hospitals to spend on facility upgrades and adopting new technologies. According to Eurostat, Germany led EU healthcare spending at USD 568 billion in 2022, followed by France (USD 364 billion), Italy (USD 204 billion), and Spain (USD 152 billion). Healthcare expenditure equaled 12.6% of GDP in Germany, 11.9% in France, and 11.2% in Austria. Modernization of the infrastructure is compelling healthcare command centers to optimize patient flow and resource utilization. Real-time analytics and monitoring solutions help in optimizing the workflows and enhancing the delivery of care.

Government investments in smart healthcare and digital transformation programs: Government investments in smart hospitals and digitalization are fueling command center deployments at a breakneck speed. It empowers AI, predictive analytics, and centralized monitoring solutions. For instance, Artisight raised an additional USD 40 million in July 2025 to bring its AI-driven smart hospital platform to 1,000 hospitals and enhance capabilities such as patient-fall prevention and ambient intelligence. Smart hospitals automate patient care, better utilize resources and respond faster to emergencies.

Segmental Insights

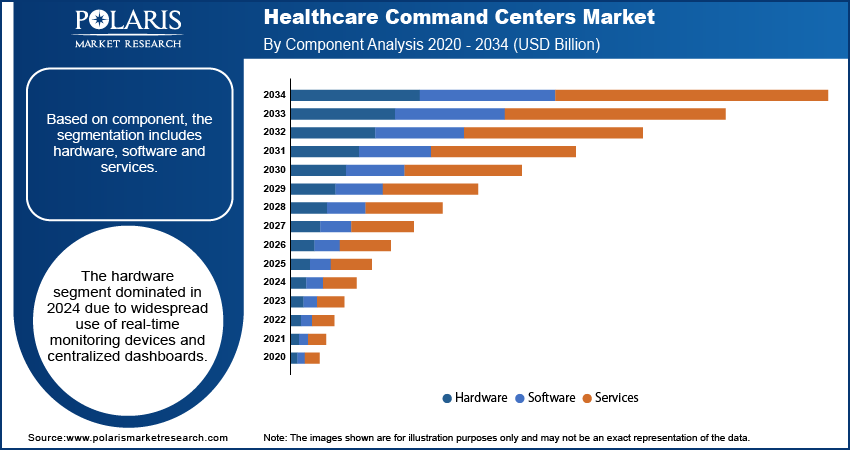

Component Analysis

Based on component, the segmentation includes hardware, software, and services. Hardware led the market during 2024 as there was increasing investment in cutting-edge hospital facilities and medical devices. Furthermore, increasing utilization of real-time monitoring solutions and centralized dashboards is generating incessant demand across healthcare centers globally.

The software segment is expected to grow at the highest CAGR during the forecast period with increasing deployment of AI-based analytics solutions. In addition, demand for predictive decision-making tools and cloud-based operational software is rising across hospitals and multi-hospital networks.

Deployment Mode Analysis

Based on deployment mode, the segmentation includes cloud-based, on-premise, and hybrid. The on-premises deployment segment dominated the market in 2024 as hospitals prefer secure, locally managed systems. Besides, stringent data privacy laws and heavy IT infrastructure investments support continued reliance on on-premises command center solutions.

The cloud-based deployment segment is anticipated to grow at the highest CAGR due to increasing adoption of elastic digital solutions and remote monitoring. Further, integration in the cloud enables multi-site hospital operations as well as predictive analytics deployment within networks.

Command Center Type Analysis

Based on command center type, the segmentation includes capacity & bed management/care progression centers, operations & resource orchestration centers, centralized clinical command centers, incident response/emergency operations centers, and security / facilities operations centers. The capacity and bed management / care progression centers segment dominated the market, driven by hospitals’ focus on optimizing patient flow and reducing overcrowding. In addition, real-time tracking of resources also improves operational effectiveness in critical and non-critical care units.

The operations and resource orchestration centers segment projected to grow at the highest rate due to greater demand for coordinated hospital functions. Moreover, AI-based scheduling and resource management tools enable efficient staffing, emergency readiness, and operations resilience.

Functional Modules Analysis

Based on functional modules, the segmentation includes AAV production, LV production, and other vectors. The real-time operational intelligence / dashboards module dominated the market, supported by hospitals’ requirement for comprehensive monitoring of clinical and administrative workflows. Moreover, instant visibility into key performance metrics aids proactive decision-making and operational efficiency.

The predictive forecasting and machine learning module expected to grow at the highest CAGR, driven by the necessity for proactive resource management and emergency planning. In addition, AI-based predictions optimize bed allocation, patient scheduling, and staff deployment across facilities.

End User Analysis

Based on end user, the segmentation includes pharmaceutical and biotechnology companies, contract development & manufacturing organizations (CDMOs) & CROs, and research and academic institutes. The large health systems / multi-hospital networks segment dominated the market due to extensive infrastructure and high patient volumes. Besides, command centers in centralized structure improve coordination, resource allocation, and interactive patient care across a number of hospital locations efficiently.

The tertiary / academic medical centers are expected to grow rapidly due to increasing utilization of advanced technologies and research-based operational needs. Additionally, these facilities focus on the application of Artificial Intelligence and predictive analytics for better patient care and workflow management.

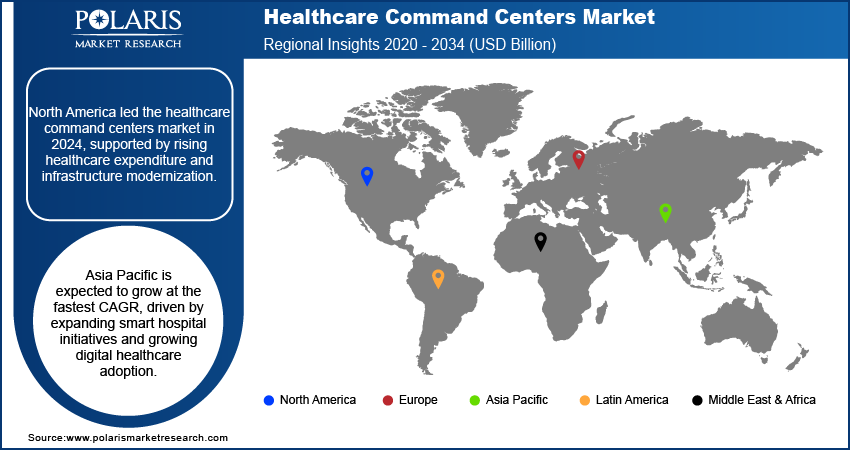

Regional Analysis

North America led the healthcare command center market due to rising investment in hospital infrastructure and the modernization of programs in the U.S. and Canada. The Canadian government is investing nearly USD 142 billion in 10 years, including USD 18 billion through funding agreements at the provincial and territorial levels, to increase access to health care, create a better workforce, and systematize the system with digital technology. Also, increasing adoption of AI-driven hospital operations platforms mandates command center deployment.

The U.S. Healthcare Command Centers Market Insights

The U.S. dominated the healthcare command centers industry fueled by large-scale hospital networks implementing real-time monitoring and predictive analytics solutions. Moreover, strict regulatory standards for patient safety and resource management encourage adoption of centralized command centers. In addition, extensive healthcare funding supports technology integration.

Europe Healthcare Command Centers Market Insights

Europe holds the substantial share in the healthcare command centers market propelled by the modernization of hospital systems and the adoption of AI-driven operational solutions in Germany, the UK, and France. Moreover, government-led healthcare digital transformation projects are increasing command center deployments. In addition, multi-hospital networks prioritize resource optimization to improve patient care.

Asia Pacific Healthcare Command Centers Market Insights

Asia Pacific is the fastest growing market owing to increasing healthcare digitization in China, India, and Japan. Moreover, growing government support for intelligent hospital initiatives drives adoption of command center solutions. For example, in December 2024, Sahyadri Hospitals launched Maharashtra's first AI-powered health command center, coupled with Dozee, to enhance patient safety via constant real-time monitoring and timely warning of health deterioration.

China Healthcare Command Centers Market Insights

China is expanding rapidly due to rapid hospital expansion and large-scale infrastructure development. In addition, domestic policies for digital healthcare and AI incorporation improve the operational effectiveness. Furthermore, rising patient volumes encourage hospitals to implement centralized command center solutions.

Key Players & Competitive Analysis Report

The healthcare command center market is relatively competitive, with companies developing cloud-integrated, AI-based, and predictive analytics solutions to enhance hospital operations. In addition to this, collaborations with hospital networks, technology vendors, and government agencies support scalability, adoption, and expansion in worldwide markets.

Key players in the market for healthcare command centers are GE Healthcare Technologies, Inc., Koninklijke Philips N.V., Siemens Healthineers, Oracle Health, TeleTracking Technologies, Inc., Epic Systems Corporation, Constant Technologies, Inc., Care Logistics, Centrilogic, Qventus, Inc., Medtronic plc, and Veradigm Inc.

Key Players

- Care Logistics

- Centrilogic

- Constant Technologies, Inc.

- Epic Systems Corporation

- GE Healthcare Technologies, Inc.

- Koninklijke Philips N.V.

- Medtronic plc

- Oracle Health

- Qventus, Inc.

- Siemens Healthineers

- TeleTracking Technologies, Inc.

- Veradigm Inc.

Industry Development

- October 2025: GE HealthCare partnered with two major U.S. medical systems to use AI in hospital command centers to improve patient flow, streamline operations, and reduce clinician burnout.

- October 2025: Clarium has added industry leaders to its team to advance AI-powered solutions for transforming the USD 250 billion U.S. healthcare supply chain.

Healthcare Command Centers Market Segmentation

By Component (Revenue, USD Billion, 2020–2034)

- Hardware

- Display Walls & Visualization Hardware

- Networking & Edge Appliances

- On-site Monitoring Stations / Consoles

- Software

- Real-time Dashboards & Visualization

- Predictive Analytics & Forecasting

- Scheduling & OR/Procedure Optimization

- Event / Alarm & Incident Management

- Integrations & Middleware

- Collaboration / Communication Workspace

- Services

- Implementation & Integration Services

- Managed Services / Virtual Command Center Operations

- Consulting

- Training & Continuous Optimization

- Data Science / Model Tuning

By Deployment Mode (Revenue, USD Billion, 2020–2034)

- Cloud-based

- On-premise

- Hybrid

By Command Center Type (Revenue, USD Billion, 2020–2034)

- Capacity & Bed Management / Care Progression Centers

- Operations & Resource Orchestration Centers

- Centralized Clinical Command Centers

- Incident Response / Emergency Operations Centers

- Security / Facilities Operations Centers

By Functional Modules (Revenue, USD Billion, 2020–2034)

- Data Aggregation & Interoperability

- Real-time Operational Intelligence / Dashboards

- Predictive Forecasting & Machine Learning

- Alerting, Escalation & Workflow Automation

- Simulation & Digital Twin

- Performance & KPI Reporting / BI

- RTLS / IoT Integration

By End User (Revenue, USD Billion, 2020–2034)

- Large Health Systems / Multi-hospital Networks

- Tertiary / Academic Medical Centers

- Community & Regional Hospitals

- Ambulatory Surgery Centers & Integrated Clinics

- Third-party Virtual Command Center Operators / Managed Service Providers

By Region (Revenue, USD Billion, 2020–2034)

- North America

- The U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

- Saudi Arabia

- UAE

- South Africa

- Israel

- Rest of South Africa

Healthcare Command Centers Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 1.77 Billion |

| Market Size in 2025 | USD 1.96 Billion |

| Revenue Forecast by 2034 | USD 4.86 Billion |

| CAGR | 10.6% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2025-2034 |

| Forecast Period | 2025-2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions and segmentation. |

FAQ's

The global market size was valued at USD 1.77 billion in 2024 and is projected to grow to USD 4.86 billion by 2034.

The global market is projected to register a CAGR of 10.6% during the forecast period.

North America dominated the healthcare command centers market in 2024 due to widespread AI adoption and hospital infrastructure modernization.

A few of the key players in the market are GE Healthcare Technologies, Inc., Koninklijke Philips N.V., Siemens Healthineers, Oracle Health, TeleTracking Technologies, Inc., Epic Systems Corporation, Constant Technologies, Inc., Care Logistics, Centrilogic, Qventus, Inc., Medtronic plc, and Veradigm Inc.

The hardware segment dominated in 2024 due to widespread deployment of real-time monitoring devices and centralized dashboards.

The tertiary / academic medical centers segment is projected to grow fastest due to rising adoption of predictive analytics and centralized command platforms.

Download Sample Report of Healthcare Command Centers Market

Please fill out the form to request a customized copy of the research report.