Laparoscopic Gynecological Procedures Market Size, Share & Industry Report, 2025-2034

REPORT DETAILS

Market Statistics

Overview

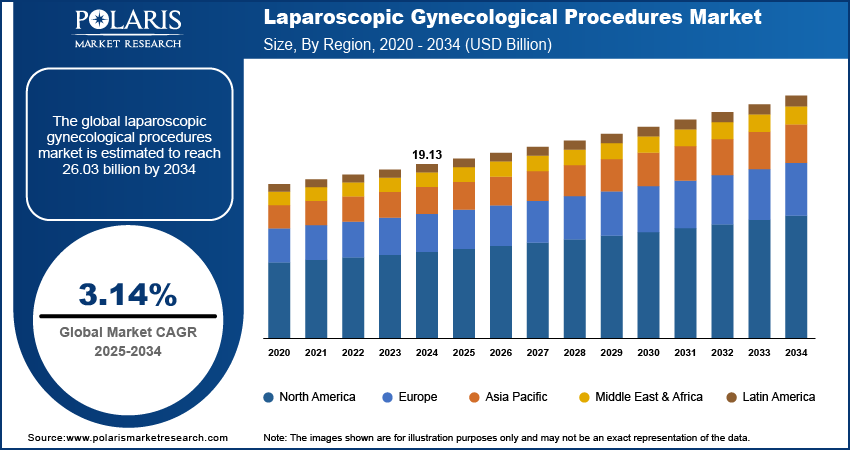

The laparoscopic gynecological procedures market was valued at USD 19.13 billion in 2024 growing at a CAGR of 3.14% from 2025-2034. Growing cases of gynecological disorders and delayed pregnancies are driving the demand for laparoscopic gynecological procedures.

Key Insights

- Laparoscopic hysterectomy led in 2024 due to high fibroid prevalence and growing adoption of minimally invasive surgery.

- Laparoscopic myomectomy is set to grow fastest with rising fibroid cases and better surgical technologies.

- North America dominated in 2024 with advanced healthcare infrastructure and high technology adoption.

- The U.S. led the region with specialized gynecology centers and strong robotic surgery adoption.

- Asia Pacific is projected to grow fastest with expanding hospital infrastructure and rising procedure awareness.

- India led APAC with growing healthcare investments and skilled laparoscopic surgeons.

Industry Dynamics

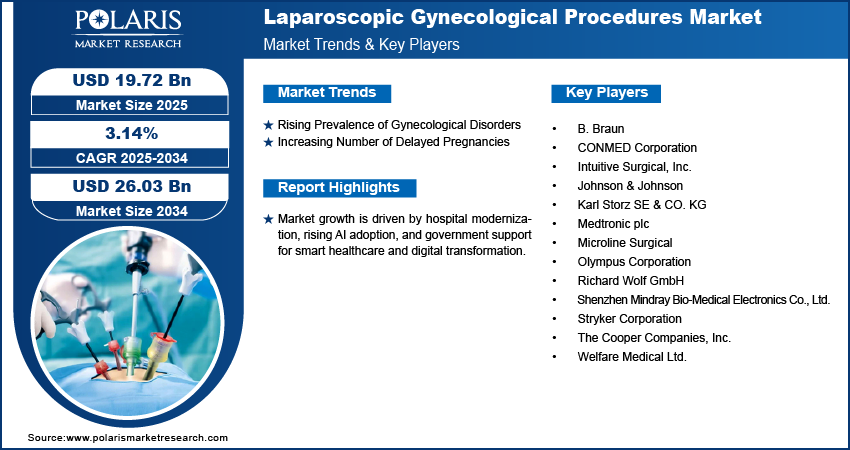

- Rising cases of gynecological disorders are driving procedure demand.

- Delayed pregnancies are increasing laparoscopic procedure volumes.

- High equipment costs are limiting adoption in developing regions.

- Robotic-assisted and minimally invasive technologies are creating opportunities for growth.

Market Statistics

- 2024 Market Size: USD 19.13 Billion

- 2034 Projected Market Size: USD 26.03 Billion

- CAGR (2025-2034): 3.14%

- North America: Largest Market Share

Laparoscopic gynecological procedures are minimally invasive surgeries for diagnosing and treating conditions such as endometriosis, ovarian cysts, and uterine fibroids. Laparoscopic gynecological procedures reduce recovery time, reduce post-operative complications, and improve surgical precision while making it preferred choice among patients and surgeons.

Source: Polaris Market Research Analysis

Rising incidence of gynecological diseases and increasing number of delayed pregnancies are driving demand for laparoscopic procedures. Advances in technology in surgical instruments, visualization systems and energy devices are also increasing adoption in hospitals and specialty clinics.

Unavailability of trained surgeons and high equipment costs are some of the major issues. However, increasing use of robotic-assisted technologies, single-incision techniques, and integration of digital imaging solutions is creating new avenues for growth in the market. For instance, in November 2023, Ethicon introduced an AI platform to enhance laparoscopic training and real-time skill development for gynecologic surgeons.

Drivers & Opportunity

Rising Prevalence of Gynecological Disorders: Rising prevalence of women's disorders such as endometriosis, uterine fibroids, and ovarian cysts is significantly driving the demand for minimally invasive surgery. Growing awareness of early detection and benefits of laparoscopic surgery over open surgery are driving market growth. Greater access to specialty gynecological care and specialty instruments are also continuously driving procedural volumes in clinics and hospitals.

Increasing Number of Delayed Pregnancies: The increasing trend of late pregnancies in women is causing a rise in age-related reproductive ailments like fibroids, infertility, and endometrial disorders. According to WHO, there are about 74 million women in low and middle-income countries who have an unintended pregnancy every year, which amounts to 25 million unsafe abortions and estimated 47,000 deaths during delivery. The trend is generating high demand for laparoscopic gynecological procedures with quick recovery and lower surgical risks.

Source: Polaris Market Research Analysis

Segmental Insights

Procedure Analysis

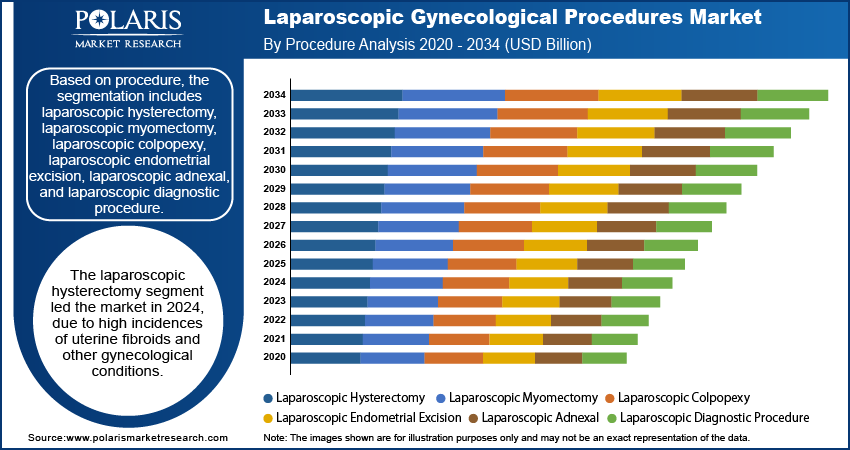

Based on procedure, the segmentation includes laparoscopic hysterectomy, laparoscopic myomectomy, laparoscopic colpopexy, laparoscopic endometrial excision, laparoscopic adnexal, and laparoscopic diagnostic procedure. The laparoscopic hysterectomy segment led the market in 2024, due to high incidences of uterine fibroids and other gynecological conditions. In addition, increasing education regarding minimally invasive procedures and enhanced surgical tools has facilitated greater adoption among hospitals and specialty clinics.

The laparoscopic myomectomy segment is anticipated to witness the highest growth CAGR during the forecast period due to an increasing incidence rate of fibroids among women in the reproductive age group. In addition, technological advancements and shorter recovery time are increasing adoption.

Surgical Tool Analysis

Based on surgical tool, the segmentation includes laparoscopes, trocars, electrosurgical devices, and handheld instruments. The laparoscopes segment dominated the market in 2024 as it plays a critical role in visualization in minimally invasive gynecological procedures. Furthermore, consistent improvements in image quality and ergonomic designs have maximized procedural efficiency as well as surgeon preference.

The electrosurgical devices segment is poised to register the maximum CAGR during the forecast period due to the growing application of energy-based instruments for delicate cutting and coagulation of tissue. In addition to this, technological innovations also remain the driving force in the market.

End User Analysis

Based on end user, the segmentation includes hospitals, clinics, and ambulatory surgery centers (ASCs). The hospitals segment dominated the market in 2024, driven by the presence of advanced surgery units and gynecology units. Moreover, hospitals ensure higher procedural volumes and quality post-operative care, resulting in growing adoption of laparoscopic procedures.

The ambulatory surgical centers (ASCs) are anticipated to grow at the highest CAGR during the forecast period due to increasing preference for outpatient surgery and economical surgical procedures. Additionally, increasing patient awareness is resulting in procedure adoption in ASCs.

Source: Polaris Market Research Analysis

Regional Analysis

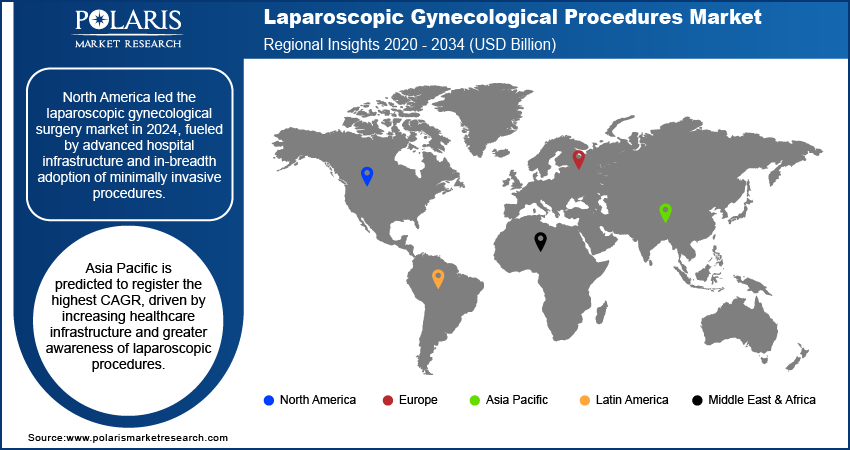

North America dominated the laparoscopic gynecological procedures market in 2024 due to the presence of advanced healthcare infrastructure and high adoption of minimally invasive surgeries. Also, growing women's awareness about gynecologic health continues to drive procedural demand. In addition, government initiatives promoting women health programs support widespread adoption.

The U.S. Laparoscopic Gynecological Procedures Market Insights

The U.S. dominated the laparoscopic gynecological procedures industry owing to high prevalence of gynecological disorders and well-established hospital networks. According to U.S. Centers for Disease Control and Prevention, roughly 13.3% of U.S. women aged 50+ have their fallopian tubes cut, 25.3% have their fallopian tubes tied, 14.9% have their fallopian tubes removed and 18.7% have both ovaries removed.

Europe Laparoscopic Gynecological Procedures Market Insights

Europe holds the substantial share in the laparoscopic gynecological procedures market due to high prevalence of gynecological conditions and well-established healthcare systems. Moreover, widespread availability of trained laparoscopic surgeons supports adoption. In addition, increasing patient preference for minimally invasive surgeries is enhancing procedural demand.

Asia Pacific Laparoscopic Gynecological Procedures Market Insights

Asia Pacific is the fastest growing market fueled by rising healthcare expenditure and expanding hospital infrastructure in emerging countries. Moreover, increasing awareness of minimally invasive procedures among women is supporting market adoption. In addition, government health initiatives are improving access to advanced gynecological care.

India Laparoscopic Gynecological Procedures Market Insights

India is experiencing strong market growth due to rising investments in specialty clinics and advanced hospitals. Invest India reports that India's healthcare sector is growing at a high pace, and home healthcare is set at USD 21.3 billion in 2027 while public health spending hit 2.5% of GDP in 2025. Additionally, increasing awareness among urban women about laparoscopic procedures is fueling procedural volumes.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

Laparoscopic gynecologic procedures market is moderately competitive, wherein companies develop advanced laparoscopic instruments, energy platforms, and robotic-assisted systems to improve surgical precision and patient outcomes. Beyond that, hospital and specialty clinic partnerships, as well as technology companies, enable adoption, training, and global market growth.

Key players in the market for laparoscopic gynecological procedures are Medtronic plc, Stryker Corporation, Karl Storz SE & CO. KG, Johnson & Johnson, Olympus Corporation, CONMED Corporation, B. Braun, The Cooper Companies, Inc., Richard Wolf GmbH, Microline Surgical, Welfare Medical Ltd., Intuitive Surgical, Inc., and Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

Key Players

- B. Braun

- CONMED Corporation

- Intuitive Surgical, Inc.

- Johnson & Johnson

- Karl Storz SE & CO. KG

- Medtronic plc

- Microline Surgical

- Olympus Corporation

- Richard Wolf GmbH

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Stryker Corporation

- The Cooper Companies, Inc.

- Welfare Medical Ltd.

Industry Development

- May 2025: B. Braun Thailand signed an MoU with TG-MET to advance laparoscopic surgery training, improve gynecologic skills, and promote international knowledge exchange through its Aesculap Academy.

- April 2024: Medtronic introduced AI-driven analysis and Live Stream technology in its Touch Surgery platform to improve laparoscopic and robotic-assisted surgery performance and training.

Laparoscopic Gynecological Procedures Market Segmentation

By Procedure (Revenue, USD Billion, 2020–2034)

- Laparoscopic Hysterectomy

- Laparoscopic Myomectomy

- Laparoscopic Colpopexy

- Laparoscopic Endometrial Excision

- Laparoscopic Adnexal

- Laparoscopic Diagnostic Procedure

By Surgical Tool (Revenue, USD Billion, 2020–2034)

- Laparoscopes

- Trocars

- Electrosurgical Devices

- Handheld Instruments

By End User (Revenue, USD Billion, 2020–2034)

- Hospitals

- Clinics

- Ambulatory Surgery Centers (ASCs)

By Region (Revenue, USD Billion, 2020–2034)

- North America

- The U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

- Latin America

- Saudi Arabia

- UAE

- South Africa

- Israel

- Rest of South Africa

Laparoscopic Gynecological Procedures Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 19.13 Billion |

| Market Size in 2025 | USD 19.72 Billion |

| Revenue Forecast by 2034 | USD 26.03 Billion |

| CAGR | 3.14% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2025-2034 |

| Forecast Period | 2025-2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 19.13 billion in 2024 and is projected to grow to USD 26.03 billion by 2034.

The global market is projected to register a CAGR of 3.14% during the forecast period.

North America dominated the laparoscopic gynecological procedures market in 2024 due to widespread AI adoption and hospital infrastructure modernization.

A few of the key players in the market are Medtronic plc, Stryker Corporation, Karl Storz SE & CO. KG, Johnson & Johnson, Olympus Corporation, CONMED Corporation, B. Braun, The Cooper Companies, Inc., Richard Wolf GmbH, Microline Surgical, Welfare Medical Ltd., Intuitive Surgical, Inc., and Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

Laparoscopic hysterectomy led the market in 2024 owing to the prevalence of uterine fibroids and widespread utilization of MIS procedures.

Ambulatory surgery centers (ASCs) is predicted to grow the most due to the rising demand for outpatient care and cost-effective laparoscopic alternatives.

Download Sample Report of Laparoscopic Gynecological Procedures Market

Please fill out the form to request a customized copy of the research report.