Infectious Respiratory Disease Diagnostics Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Infectious Respiratory Disease Diagnostics Market Summary

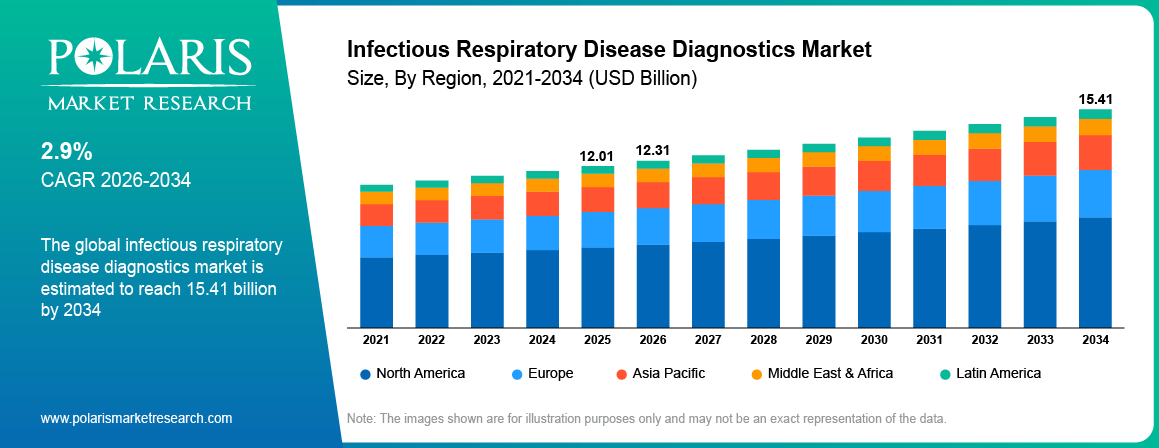

The global infectious respiratory disease diagnostics market is estimated around USD 12.01 billion in 2025,?with consistent growth anticipated during 2026–2034. Growth is driven by rising incidence of respiratory infections and increasing aging population. The market is projected to grow at a CAGR of 2.9% during the forecast period.

Market Statistics

Key Takeaways

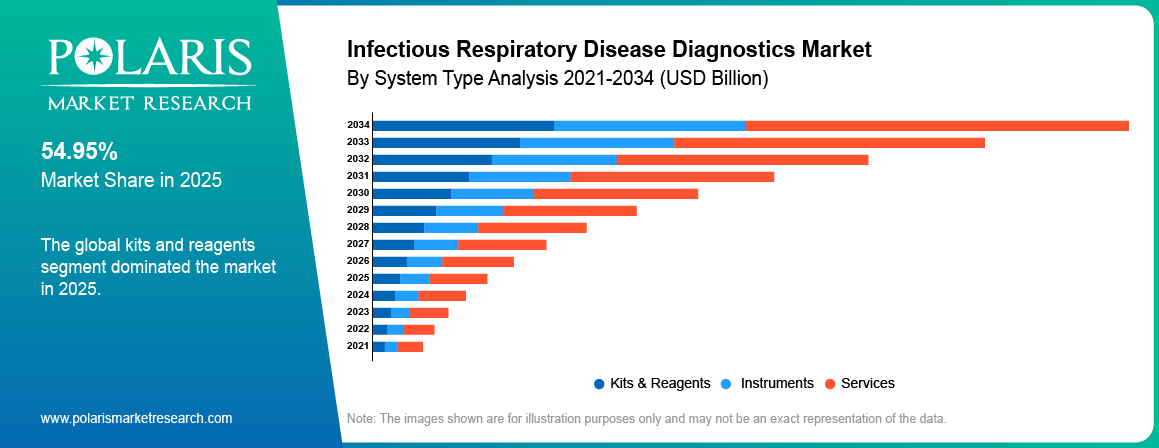

- Kits & reagents segment dominated the market in 2025 with 54.95% share, driven by high testing volume across laboratories and hospitals.

- The COVID-19 segment dominated the market with 29.9% revenue share in 2025 due to constant surveillance and occasional outbreaks.

- Home testing / POCT segment is projected to grow at the fastest CAGR of 3.1% during the forecast period, due to rising demand for convenient and rapid testing solutions

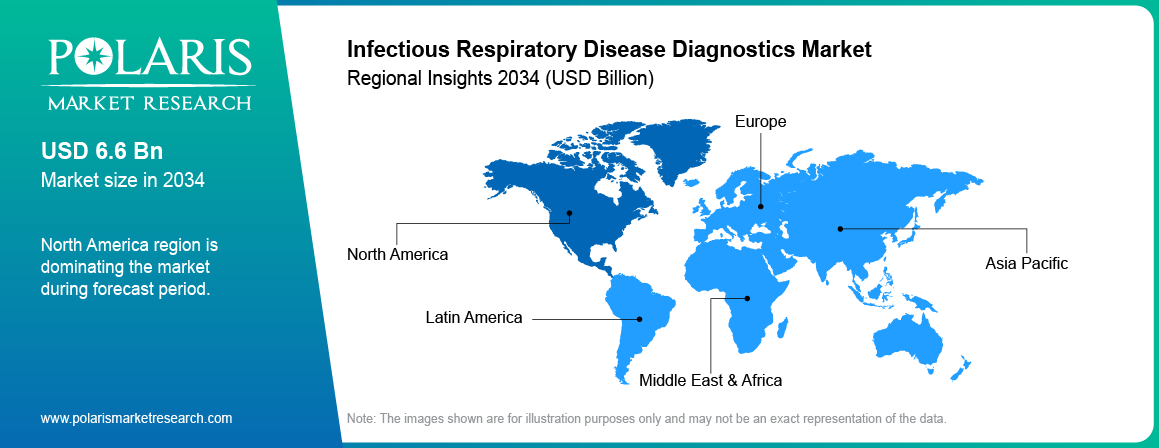

- North America dominated revenue with 43.72% revenue share due to strong healthcare infrastructure and high testing volumes.

- Asia Pacific infectious respiratory disease diagnostics market is projected to grow at the fastest CAGR of 3.5% during the forecast period, owing to rising population and increasing incidence of respiratory infections.

Industry Dynamics

- Rising incidence of respiratory infections is increasing demand for infectious respiratory disease diagnostics.

- Increasing aging population is driving higher diagnostic testing needs.

- High cost of molecular diagnostic tests is impacting adoption in cost-sensitive regions.

- Growing demand for home-based and self-testing kits is creating new growth opportunities.

What is the Infectious Respiratory Disease Diagnostics Market?

Infectious respiratory disease diagnostics involves the process of using various tests to detect any pathogens affecting the respiratory system, which includes bacteria and viruses. The diagnostics are vital for early diagnosis, monitoring the progress of diseases, and making treatment decisions. The tests are conducted in hospitals, diagnostic laboratories, and point-of-care facilities for diseases like influenza, COVID-19, and other respiratory infections. Rising incidence of respiratory infections is increasing demand for rapid and accurate diagnostic solutions.

Diagnostic technologies vary based on test type, speed, and application setting. PCR-based molecular diagnostic tests are highly sensitive and accurate. Antigen and rapid diagnostic tests offer fast screening in decentralized laboratories. Multiplex testing allows the identification of several pathogens within one test sample. Innovation in diagnostic platforms is helping to improve turnaround times and efficiency.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The increased need for diagnosis and management of outbreaks is contributing towards an increase in the adoption of more advanced respiratory diagnostic tools. There will be an increased investment by healthcare organizations in laboratory infrastructure and testing facilities. The increased need for pandemic preparedness and surveillance will fuel demand for advanced and rapid diagnostic technologies, which will boost the market.

Drivers & Opportunities

Rising Incidence of Respiratory Infections: The rising incidence rate of respiratory diseases is spurring the need for precise and effective diagnostic technologies. Health organizations have started adopting diagnostic solutions that enable quick identification and prevention of disease spread and ensure better treatment options for patients. For example, in April 2026, Salaera was introduced in order to improve breath diagnosis techniques and promote non-invasive testing of respiratory diseases and enhanced accuracy of monitoring clinical processes.[Source: www.azom.com]

Increasing Aging Population : The rising number of aging population increases the likelihood of developing respiratory disorders. Regular diagnosis is needed for managing the disease among elderly patients. According to WHO, the number of people above the age of 60 years will reach 1.4 billion in 2030 and 2.1 billion in 2050. The population of people over 80 years will be 426 million.[Source:www.who.int] This development is driving demand for the diagnostics of respiratory problems.

Restraints & Challenges

High Cost of Advanced Molecular Diagnostic Tests: The high costs associated with molecular diagnostics techniques is creating an issue in adopting the test technology in low-income countries. The healthcare institutions in such markets may have limited budgets to conduct mass diagnostics.

Opportunity

Growing Demand for Home-Based and Self-Testing Kits: Increasing consumer preferences for home and self-test kits have created new revenue streams for the market. Patients like to get their diagnostic tests done with maximum convenience and in minimum time without having to visit any healthcare facilities. In October 2025, ACON Laboratories launched a 4-in-1 Flowflex Plus home kit, .[Source: www.aconlabs.com]which has been approved by the FDA for testing RSV, influenza A/B, and COVID-19 in a single rapid test kit.Such trends are driving innovations in products and availability of diagnostic tests.

Source: Polaris Market Research Analysis

Technology & Testing Methods Analysis

Molecular Diagnostics vs Rapid Antigen Testing

Molecular diagnostics for respiratory infections, such as PCR respiratory diagnostics and nucleic acid amplification test (NAAT), have high sensitivity and precision when identifying pathogens. The laboratory opts for these diagnostics for confirmation and difficult samples. Fast antigen respiratory diagnostic tests allow rapid test results and facilitate mass testing. Purchasers choose PCR for precision, and antigen test kits for rapid testing and cost-effectiveness.

Multiplex Panels & Syndromic Testing

Multiplex respiratory diagnostics allow for the simultaneous detection of many different pathogens within one test. These panels are used by hospitals and diagnostics centers to distinguish between infections that display similar symptoms. Syndromic diagnostics help clinicians to make decisions faster. Multiplex respiratory diagnostics represent the choice for buyers as they require fewer tests.

Emerging Technologies

Some new diagnostic tools that have been developed include the use of artificial intelligence systems, biosensors, and digital diagnostics. The tools improve the accuracy of the interpretation of results and allow real-time monitoring. Biosensors are portable and are used for immediate diagnosis in remote locations.

Technology Comparison

| Technology | Accuracy | Speed | Cost | Scalability | Use Case |

| PCR / NAAT | High | Medium | High | Medium | Confirmatory diagnosis |

| Rapid Antigen | Medium | High | Low | High | Mass screening |

| Multiplex | High | Medium | High | Medium | Multi-pathogen detection |

| AI / Digital | High | High | Medium | High | Data analysis & automation |

| Biosensors | Medium-High | High | Medium | High | Portable testing |

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the infectious respiratory disease diagnostics market by product, disease type, and end user to help readers identify the fastest expanding and most attractive demand segments.

By Product

-

Kits & Reagents

Kits & reagents segment dominated the market in 2025, driven by high testing volume across laboratories and hospitals. Continuous demand for consumables in PCR and antigen testing is supporting segment growth. Rising frequency of diagnostic testing is increasing repeat purchases.

-

Instruments

Instruments segment is projected to grow at the fastest CAGR during the forecast period, due to increasing investment in advanced diagnostic infrastructure. Adoption of automated and high-throughput systems is improving laboratory efficiency. Expansion of molecular testing capabilities is accelerating segment demand.

By Disease Type

-

COVID-19

The COVID-19 segment dominated the market in 2025 due to constant surveillance and occasional outbreaks. The segment witnessed growth due to continuous testing needs in the healthcare and general environment segments. Screening programs organized by governments are ensuring steady test volume.

-

Influenza

Influenza segment is projected to grow at the fastest CAGR during the forecast period, due to rising seasonal infection rates and increased awareness for early diagnosis. World Health Organization reports about 1 billion seasonal influenza cases each year, including 3–5 million severe cases and up to 650,000 respiratory deaths.[Source: www.who.int] Increasing need for rapid and multiplex testing methods is contributing to the segment growth. Growth in preventive healthcare initiatives is boosting testing adoption rates.

By End User

-

Diagnostic Labs

The diagnostic lab segment dominated the market in 2025 due to high testing capacity and efficient laboratory infrastructure. They deal with large sample sizes and complicated molecular tests. Increasing outsourcing of diagnostic services is supporting segment growth.

-

Home Testing / POCT

Home testing / POCT segment is projected to grow at the fastest CAGR during the forecast period, due to rising demand for convenient and rapid testing solutions. Adoption of self-testing kits is increasing across urban populations. Growth in decentralized healthcare is accelerating segment demand.

Source: Polaris Market Research Analysis

Regional Analysis

North America Market Assessment

North America infectious respiratory disease diagnostics market dominated in 2025, due to advanced healthcare infrastructure and high adoption of molecular diagnostics. For instance, in February 2026, researchers from University of Maryland School of Medicine reported a new approach that improves early detection and monitoring of respiratory infections using advanced diagnostic methods.[Source:www.eurekalert.org] Strong presence of leading diagnostic companies is supporting continuous product innovation. High testing volumes across hospitals and laboratories are sustaining regional demand.

Asia Pacific Infectious Respiratory Disease Diagnostics Market Insights

Asia Pacific infectious respiratory disease diagnostics market is projected to grow at the fastest CAGR during the forecast period, owing to rising population and increasing incidence of respiratory infections. UNFPA states that the Asia Pacific older population will reach 1.3 billion by 2050, with women forming 53% of those aged 60+ and 60% of those above 80.[Source: asiapacific.unfpa.org] Therefore, aging population growth increases demand for infectious respiratory disease diagnostics due to higher infection risk among elderly groups. In addition, expanding healthcare infrastructure is improving diagnostic access coupled with government initiatives for disease surveillance are accelerating market growth.

Europe Infectious Respiratory Disease Diagnostics Market Overview

Europe infectious respiratory disease diagnostics market held the second-largest share, owing to strong public healthcare systems and established diagnostic networks. In December 2025, the European Commission allocated USD 1,036 million to support development of advanced diagnostic solutions aimed at addressing antimicrobial resistance.[Source: health.ec.europa.eu] Also, increasing focus on early disease detection is supporting testing demand. Adoption of multiplex and molecular diagnostics is expanding across the region.

Latin America Market Insights

The Latin American region is experiencing constant growth due to increased healthcare access and awareness regarding infectious diseases. Expansion of diagnostic laboratories is supporting testing capacity. Government programs for disease control are increasing demand for respiratory diagnostics.

Middle East & Africa Market Analysis

Middle East & Africa is experiencing gradual growth, driven by increasing investment in healthcare infrastructure. Rising burden of infectious diseases is supporting diagnostic demand. Adoption of point-of-care testing is improving access in remote areas.

Source: Polaris Market Research Analysis

Competitive Landscape & Strategic Insights

The respiratory infection diagnostic tests market are described as moderately fragmented, with international diagnostic firms, regional labs, and test kit providers dominating different testing areas. The competition is built around the quality of results, speed, costs, and technological compatibility. Companies in this market are working towards developing molecular tests, multiplexing, and point-of-care technologies.

Some of the notable players in the market include Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, Danaher Corporation, Siemens Healthineers, QIAGEN, bioMérieux, Becton Dickinson and Company, Hologic Inc., Cepheid, QuidelOrtho Corporation, Seegene Inc., and others.

Premium Insights & Future Outlook

Strategic Developments

- Decentralization of testing is shifting demand toward point-of-care and home diagnostics solutions

- Rising adoption of home-based testing is expanding access and improving early detection rates

- AI-driven diagnostics is improving accuracy and reducing turnaround time in clinical workflows

- Demand for multiplex and molecular testing is increasing across high-throughput laboratories

- Strategic focus is shifting toward scalable and cost-efficient respiratory diagnostic technologies

Future Outlook

- Respiratory diagnostics market future is expected to shift toward decentralized and digital testing models

- Growth in home diagnostics will increase consumer-driven testing adoption

- AI diagnostics market trends indicate higher integration of automation in result interpretation

- Future of infectious disease diagnostics will focus on rapid, portable, and multi-pathogen detection platforms

- Investment in advanced diagnostic infrastructure will support long-term market expansion

Key Players

- Abbott Laboratories

- Becton Dickinson and Company

- bioMérieux

- Cepheid

- Danaher Corporation

- Hologic Inc.

- QIAGEN

- QuidelOrtho Corporation

- Roche Diagnostics

- Seegene Inc.

- Siemens Healthineers

- Thermo Fisher Scientific

Industry Developments

- March 2026: Roche launched the cobas eplex RP3 panel, a CE-marked diagnostic test that detects up to 25 respiratory pathogens in a single sample, enabling rapid and accurate treatment decisions for respiratory infections. [source: roche.com]

- February 2026: Stanford researchers developed a nasal spray universal vaccine that delivers broad protection against multiple respiratory infections in preclinical studies. [source: med.stanford.edu]

Infectious Respiratory Disease Diagnostics Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021-2034)

- Kits & Reagents

- Instruments

- Services

By Disease Type Outlook (Revenue, USD Billion, 2021-2034)

- COVID-19

- Influenza

- Tuberculosis

- RSV

- Pneumonia

By End User Outlook (Revenue, USD Billion, 2021-2034)

- Hospitals

- Diagnostic Labs

- Home Testing / POCT

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Infectious Respiratory Disease Diagnostics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 12.01 Billion |

| Market Size in 2026 | USD 12.31 Billion |

| Revenue Forecast by 2034 | USD 15.41 Billion |

| CAGR | 2.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Infectious Respiratory Disease Diagnostics Market FAQ's

The global market size was valued at USD 12.01 Billion in 2025 and is projected to grow to USD 15.41 Billion by 2034.

North America dominates the market due to advanced healthcare infrastructure and high adoption of molecular diagnostics.

Major applications include hospitals, diagnostic laboratories, and home testing or point-of-care settings.

A few of the key players in the market are Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, Danaher Corporation, Siemens Healthineers, QIAGEN, bioMérieux, Becton Dickinson and Company, Hologic Inc., Cepheid, QuidelOrtho Corporation, Seegene Inc., and others.

Key drivers include rising incidence of respiratory infections, increasing aging population, and expansion of molecular testing technologies.

Major demand comes from diagnostic labs, hospitals, and home testing users.

The market outlook remains strong due to growth in home diagnostics, AI-driven testing, and decentralized healthcare models.

Download Sample Report of Infectious Respiratory Disease Diagnostics Market

Please fill out the form to request a customized copy of the research report.