Keytruda Market Size, Share, Global Analysis Report, 2026-2034

REPORT DETAILS

Keytruda Market Summary

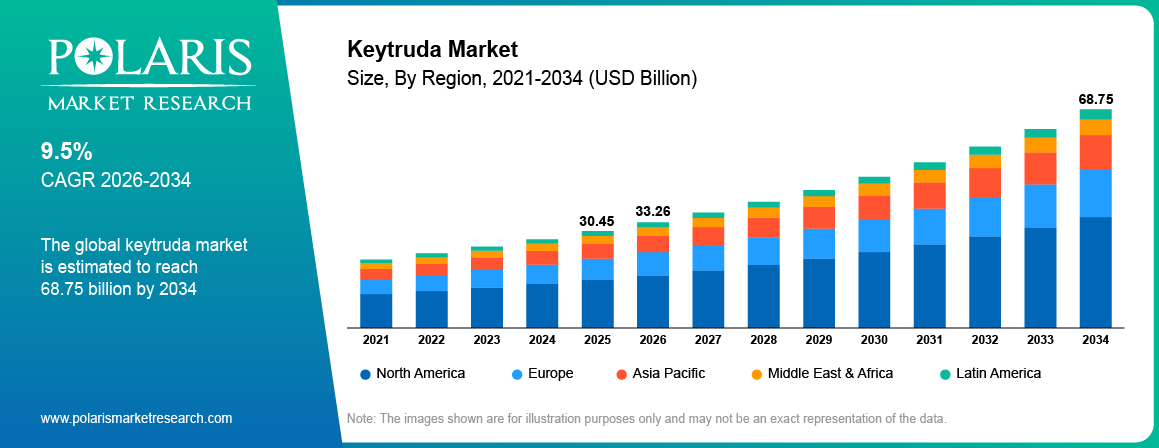

The global Keytruda market is estimated around USD 30.45 Billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by rising cancer incidence and expanding adoption of immunotherapy treatment across oncology care. The market is projected to grow at a CAGR of 9.5% during the forecast period.

Market Statistics

Key Takeaways

- North America accounted for the largest regional share of around 46.3% in 2025, driven by advanced oncology infrastructure, high immunotherapy adoption, and strong reimbursement support for cancer treatments.

-

By Indication, NSCLC segment accounted for the largest share of approximately 39.7% in 2025, supported by large patient population and widespread clinical adoption of Keytruda in lung cancer treatment.

-

By End Use, Hospitals & Oncology Centers segment accounted for the largest share of nearly 71.5% in 2025, driven by high treatment administration rates across specialized cancer care facilities.

Industry Dynamics

- Rising global cancer incidence supports expansion of immunotherapy treatment across the market.

- Clinical evidence demonstrating durable survival outcomes strengthens adoption of PD-1 inhibitor therapies in oncology protocols.

- High therapy cost creates treatment access limitations across price sensitive healthcare systems.

- Expansion of biomarker testing infrastructure supports long term opportunities across the market.

What is the Keytruda Market?

The Keytruda industry refers to the development, production, and commercialization of the Keytruda immunotherapy drug for the treatment of cancer. The ecosystem involves pharmaceutical firms, biotech research centers, clinical trial firms, and healthcare service providers. Hospitals, oncology clinics, and cancer treatment centers use this therapy to treat multiple types of cancer through immune system activation.

The industry focuses on the supply and distribution of Keytruda for indications such as melanoma, non-small cell lung cancer, head and neck cancer, and other advanced tumors. Pharmaceutical firms undertake clinical trials and approvals for the expansion of the treatment scope for various oncology segments. Healthcare providers administer the therapy through controlled medical settings as part of immunotherapy treatment protocols.

To Understand More About this Research: Download Sample Report

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The Keytruda industry differs from conventional chemotherapy drug markets. Traditional chemotherapy targets cancer cells directly through cytotoxic mechanisms. Keytruda is an immunotherapy drug that involves the inhibition of the immune system, thereby recognizing and targeting cancer cells. The treatment involves the use of precision medicine for the treatment of various types of cancer.

Drug Profile and Treatment Landscape

Mechanism of Action – PD-1 Pathway Inhibition

Keytruda acts as an immune checkpoint inhibitor targeting the PD-1 receptor on T-cells, restoring the immune response against the tumor cells. This action creates an opportunity for the expansion of the checkpoint inhibitor therapy market in the oncology treatment segments.

Approved Indications and Combination Regimens

Keytruda has received approvals for various cancer types, including melanoma, non-small cell lung cancer, head and neck cancer, and gastric cancer. The oncology treatment protocols are showing an increased trend of using combination therapy along with chemotherapy, targeted therapy, and other immunotherapy agents.

Biomarker Driven Demand (PD-L1, MSI-H/dMMR)

Precision oncology service adoption would lead to an increase in the use of biomarker tests in immunotherapy treatment selection. Keytruda treatment eligibility is determined by PD-L1 expression tests and MSI-H or dMMR biomarker tests. An increase in biomarker tests would lead to an expansion of the precision oncology market.

Drivers & Opportunities

Rising global cancer incidence: Increasing Global Cancer Cases: An increase in the incidence rate of various types of cancers, including lung cancer, melanoma, and head and neck cancers, is expected to drive the immunotherapy market. According to the WHO, the total cancer cases worldwide could increase to over 35 million by 2050, reflecting an increase of 77% from the 20 million cases documented in 2022. Hospitals are increasing the use of Keytruda in treating various types of cancers. This trend supports growth across the market.

Strong clinical outcomes of PD-1 inhibitors: Clinical studies report durable response rates and longer survival outcomes in several cancer indications. Oncologists increasingly integrate PD-1 inhibitor therapies into standard oncology treatment protocols. Expanding clinical evidence strengthens physician confidence in immunotherapy-based treatment strategies across the market.

Restraints & Challenges

High treatment cost: Immunotherapy drugs involve high treatment expenditure across oncology care. Multiple treatment cycles and hospital-based drug administration raise overall therapy cost. Budget limitations across public healthcare systems restrict broader treatment access. These factors create pricing pressure across the market.

Opportunity

Rising adoption of personalized medicine: Precision oncology approaches facilitate various cancer treatment strategies. For instance, in March 2026, Adela introduced tissue-free blood tests, as supported by a study published in NPJ Precision Oncology, which monitors response to immunotherapy in advanced solid tumors by detecting reductions in methylated ctDNA, which is associated with better outcomes. Also, biomarker tests, including PD-L1 expression, MSI-H, or dMMR tumor profiling, are used in selecting patients for immunotherapy. There is expansion of genomic testing infrastructure in hospitals. This development supports expansion across the Keytruda market.

To Understand More About this Research: Download Sample Report

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the market by indication, payer, and distribution channel to help readers identify the fastest expanding and most attractive demand segments.

By Indication

-

NSCLC

Non-small cell lung cancer held the largest market share in the year 2025. This is because the keytruda drug has high clinical adoption rates in the treatment of non-small cell lung cancer as first-line treatment and in combination. High patient population and treatment adoption rates in oncology centers ensure high revenue contribution from this indication.

-

Triple Negative Breast Cancer

The triple negative breast cancer segment is projected to grow at the fastest CAGR during the forecast period due to expanding approvals of immunotherapy-based treatment regimens. Rising clinical trials and broader treatment guidelines increase the use of checkpoint inhibitors in this cancer segment.

By Payer

-

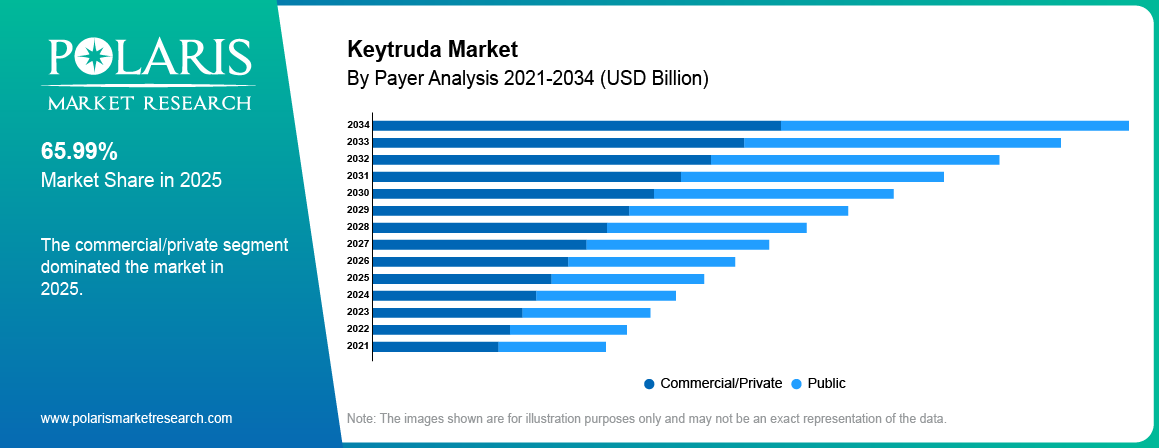

Commercial/Private

Commercial and private payers held the highest market share in the year 2025. This is because keytruda has high adoption rates in private health insurance plans. This ensures that patients have access to advanced treatment options in oncology through employer-based health plans.

-

Public

Public payers are expected to experience the highest CAGR during the forecast period. This is because government healthcare plans cover the population in various healthcare systems, including national cancer treatment plans.

By Distribution Channel

-

Hospital Pharmacy

Hospital pharmacy services had the highest market share in 2025, driven by the administration of immunotherapy drugs in treatment centers. Infusion based treatment protocols support hospital pharmacy dominance.

-

Specialty Pharmacy

The specialty pharmacy segment is projected to grow at the fastest CAGR during the forecast period due to increasing distribution of oncology biologics through specialized pharmaceutical supply networks and patient support programs.

To Understand More About this Research: Request Customization Source: Polaris Market Research Analysis

Regional Analysis

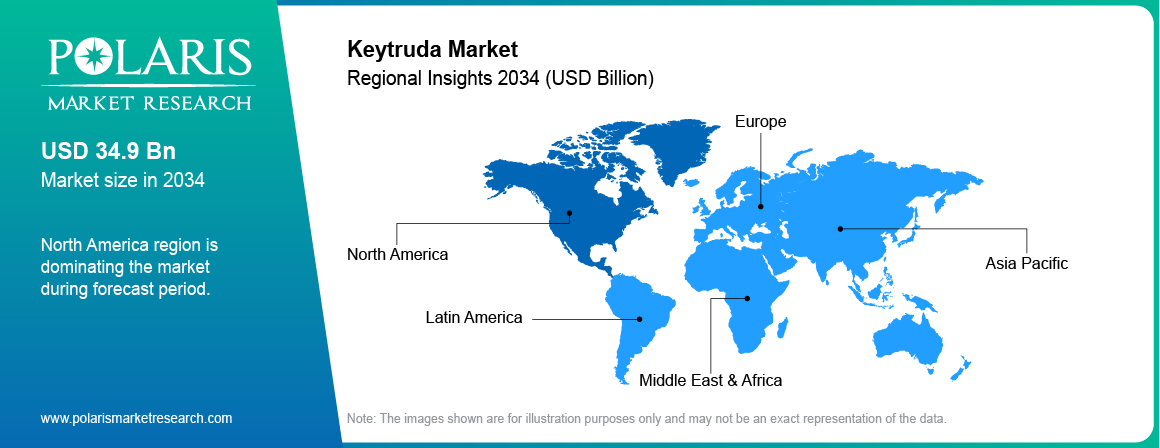

North America Market Assessment

North America Keytruda market dominated in 2025 driven by high cancer incidence and strong adoption of immunotherapy treatments across the U.S. and Canada. Hospitals and oncology centers widely use Keytruda across lung cancer, melanoma, and other tumor indications. The American Cancer Society reported around 2 million new cancer cases in the US in 2024. Strong oncology treatment infrastructure supports expansion of the US market.

Asia Pacific Keytruda Market Insights

Asia Pacific Keytruda market is projected to grow at the fastest CAGR during the forecast period due to expanding cancer burden and improving access to oncology treatment. The Lancet Oncology report shows that Southeast Asia recorded about 1.15 million new cancer cases in 2022, including 545,725 cases in men and 601,085 cases in women, while total cancer deaths reached 716,116. Also, countries such as China and India are expanding cancer hospitals, immunotherapy clinical trials, and oncology drug approvals.

Europe Keytruda Market Overview

Europe Keytruda market accounted for the second largest share driven by expanding immunotherapy adoption and strong oncology research infrastructure. Countries such as Germany, France, and the UK report high demand for checkpoint inhibitor therapies in lung cancer and melanoma treatment. The European Commission estimated the EU population reached about 450.6 million, and around 22% of the population was aged 65 years and above. Rising cancer incidence across aging populations supports expansion of the Europe market.

To Understand More About this Research: Request Customization

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The competitive landscape in the market shows that companies place a high priority on research in oncology treatments. Pharmaceutical companies invest in clinical studies that broaden the treatment indications of Keytruda. They partner with biotechnology companies, research organizations, and oncology treatment centers to innovate in the field of biomarker-guided immunotherapy.

Leading companies in the market are Merck & Co., Inc., Bristol-Myers Squibb Company, F. Hoffmann-La Roche AG, AstraZeneca plc, Pfizer Inc., Novartis AG, Sanofi S.A., Johnson & Johnson, GSK plc, Amgen Inc., Eli Lilly and Company, Regeneron Pharmaceuticals, Inc., and many more.

Keytruda Patent Expiry and Biosimilar Market Scenarios

| Scenario | Market Dynamics | Payer Behavior | Revenue Outlook |

| Base Scenario | Gradual entry of pembrolizumab biosimilars after loss of exclusivity for Keytruda. Branded therapy retains presence in major oncology indications. | Payers introduce partial biosimilar substitution across hospital formularies. | Moderate revenue decline across the keytruda market through 2034. |

| Aggressive Erosion Scenario | Multiple PD-1 inhibitor biosimilars enter the market with strong price competition. | Public and private payers favor biosimilar products in oncology procurement programs. | Faster revenue erosion across the keytruda market before 2034. |

| Resilient Combination Scenario | Expansion of combination immunotherapy regimens across cancer indications. | Payers retain coverage for branded therapy in combination treatment protocols. | Stable demand across the keytruda market through 2034. |

Source: Polaris Market Research Analysis

The oncology biologics market approaches a major patent transition period during the next decade. Biosimilar development programs for PD-1 inhibitors continue across global pharmaceutical pipelines. Expansion of biomarker driven treatment strategies and combination therapy protocols support sustained demand for branded immunotherapy products within the market through 2034.

Key Players

- Amgen Inc.

- AstraZeneca plc

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- F. Hoffmann-La Roche AG

- GSK plc

- Johnson & Johnson

- Novartis AG

- Pfizer Inc.

- Regeneron Pharmaceuticals, Inc.

- Sanofi S.A.

Industry Developments

- February 2026: PADCEV combined with KEYTRUDA reduces the risk of recurrence or death by nearly 50% in patients with high-risk muscle-invasive bladder cancer compared to chemotherapy alone.

- November 2025: The FDA approved KEYTRUDA (pembrolizumab) and KEYTRUDA QLEX (pembrolizumab and berahyaluronidase alfa-pmph), each combined with Padcev (enfortumab vedotin-ejfv), as perioperative treatment for cisplatin-ineligible adults with muscle-invasive bladder cancer.

Market Segmentation

By Indication Outlook (Revenue, USD Billion, 2021-2034)

- NSCLC

- Melanoma

- Renal Cell Carcinoma

- Urothelial Carcinoma

- Head & Neck Cancer

- MSI-H / dMMR Tumors

- Triple-Negative Breast Cancer

- Others

By Payer Outlook (Revenue, USD Billion, 2021-2034)

- Commercial/Private

- Public

By Distribution Channel Outlook (Revenue, USD Billion, 2021-2034)

- Hospital Pharmacy

- Specialty Pharmacy

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 30.45 Billion |

| Market Size in 2026 | USD 33.26 Billion |

| Revenue Forecast by 2034 | USD 68.75 Billion |

| CAGR | 9.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 30.45 Billion in 2025 and is projected to grow to USD 68.75 Billion by 2034.

North America dominates due to strong immunotherapy adoption and advanced oncology treatment infrastructure.

Major treatment indications include non-small cell lung cancer, melanoma, renal cell carcinoma, and head and neck cancer using Keytruda.

A few of the key players in the market are Merck & Co., Inc., Bristol-Myers Squibb Company, F. Hoffmann-La Roche AG, AstraZeneca plc, Pfizer Inc., Novartis AG, Sanofi S.A., Johnson & Johnson, GSK plc, Amgen Inc., Eli Lilly and Company, Regeneron Pharmaceuticals, Inc., and others.

Key factors include rising global cancer incidence and expansion of biomarker guided immunotherapy treatment.

Download Sample Report of Keytruda Market

Please fill out the form to request a customized copy of the research report.