Minimal Residual Disease Market Share, Size, Trends, Industry Analysis Report, 2025 - 2034

REPORT DETAILS

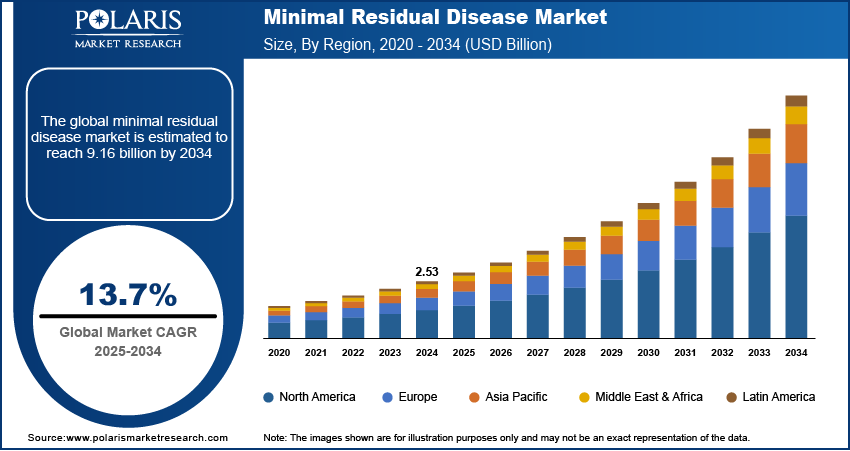

Minimal Residual Disease Market Summary

The global minimal residual disease market was valued at USD 2.53 billion in 2024 and is expected to grow at a CAGR of 13.7% during the forecast period.

Market Statistics

Key Takeaways

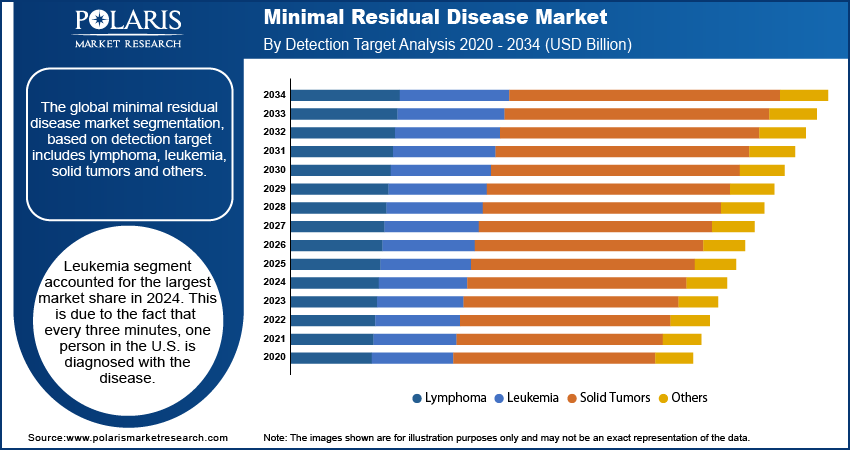

- Leukemia segment accounted for the largest market share in 2024. This is due to the fact that every three minutes, one person in the U.S. is diagnosed with the disease.

- Flow cytometry dominated the market in 2024. This is due to the excellent sensitivity and extensive applicability of MRD testing.

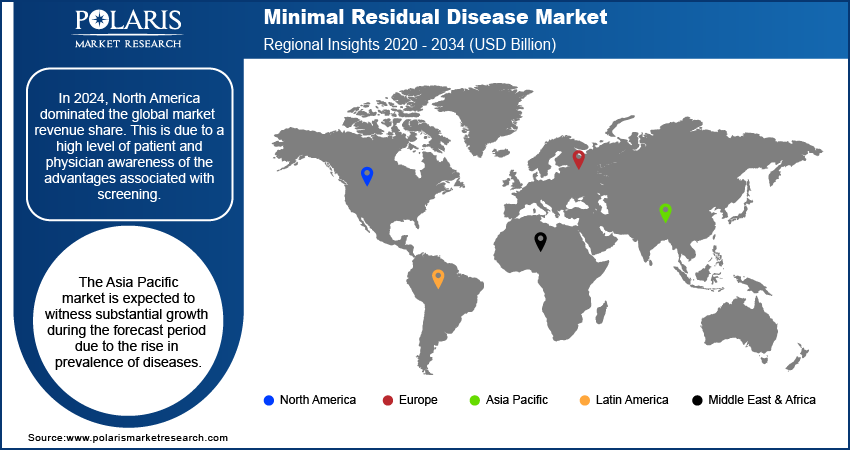

- In 2024, North America dominated the global market revenue share. This is due to a high level of patient and physician awareness of the advantages associated with screening.

- The Asia Pacific market is expected to witness substantial growth during the forecast period due to the rise in prevalence of diseases.

The increasing number of cancer patients and increased R&D spending are driving the expansion of the market. The growing use of next-generation sequencing (NGS) technology is another driving factor for this market. A further element in the market's growth is the technological developments in diagnostics and therapeutics through rising R&D expenditures.

Industry Dynamics

- The rise in cancer cases boosts the patient population, which requires long-term monitoring. This has created a larger and continuous need for MED testing for the management of the treatment and to detect relapse.

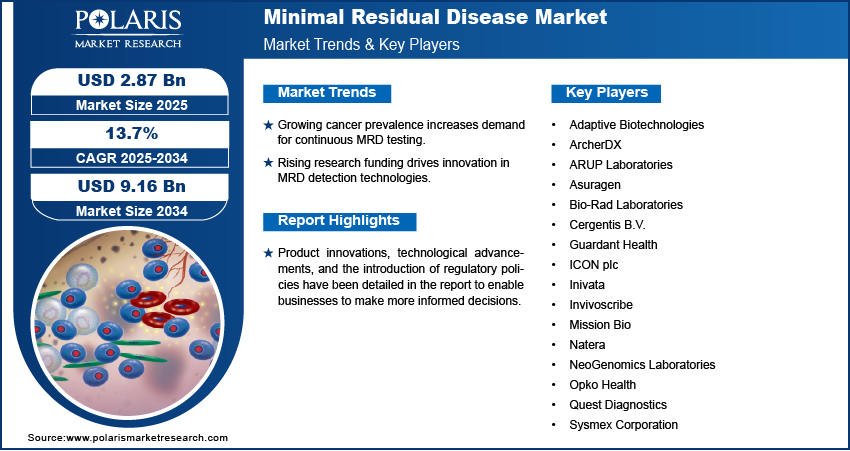

- Research funding initiatives expand the development and validation of new and more sensitive MRD detection technologies. These initiatives make advanced testing accessible and clinically adopted, supporting the market demand.

- Widespread adoption and integration into standard clinical practice, especially in cost-sensitive healthcare systems, is limited due to the high cost and complexity of MED tests.

- Its current use in blood cancers expand MRD testing into solid tumors, which is expected to increase the addressable patient population and create substantial opportunity for the market.

Product innovations, technological advancements, and the introduction of regulatory policies have been detailed in the report to enable businesses to make more informed decisions. Furthermore, the impact of the COVID-19 pandemic on the minimal residual disease market demand has been examined in the study. The report is a must-read for anyone looking to develop effective strategies and stay ahead of the curve.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Additionally, the development and use of NGS technologies, technological developments in cloud computing and data integration, and the availability of a technologically enhanced framework for healthcare research are all driving the market. Along with this, the expansion of genome mapping programs and the better regulatory & reimbursement environment for NGS-based diagnostic tests drive the minimal residual disease market growth throughout the projection period.

Global healthcare systems were impacted by the COVID-19 pandemic, which also caused many healthcare facilities to stop providing routine care, placing susceptible cancer patients at serious risk. Ever since the start of the COVID-19 pandemic, efforts have been made to increase the number of covid patients admitted and decrease the number of non-covid patients admitted, resulting in treatment delays.

Industry Dynamics

Growth Drivers

Global cancer occurrences have significantly increased and are expected to have a major impact on the market growth for treatments for minimal residual illness during the forecast period. It is projected that cancer patients who are undergoing cancer therapies favor the growth of the worldwide minimal residual illness market during the forecast period. A shift in the patient's focus toward minimal residual disease is anticipated due to the difficulties of PCR, FISH, & the flow cytometry to enumerate 1 in every 100,000 cells. Patients experience greater treatment accuracy as a result of the use of innovative technology. These factors might effect the overall market worldwide.

Source: Polaris Market Research Analysis

Report Segmentation

The market is primarily segmented based on detection target, test technique, End User and region.

| By Detection Target | By Test Technique | By End User | By Region |

|

|

|

|

Source: Polaris Market Research Analysis

Know more about this report: Download Sample Report

Segmental Analysis

Detection Target Analysis

In 2024, leukemia dominated the market owing to the fact that one person in the U.S. is diagnosed with leukemia every three minutes. For instance, according to the American Cancer Society, in 2022 there are around 60,650 new instances of leukemia, 24,000 people died from the disease and about 20,050 new cases of acute myeloid leukemia. Leukemia’s new cases were 14.1 per 100,000 men and women annually. The annual mortality rate was 6.0 per 100,000 men and women.

When the DNA of a single bone marrow cell is altered or mutated, leukemia develops because the cell is unable to mature and perform correctly. Leukemia cells frequently behave abnormally while interacting with white blood cells. According to studies, next-generation sequencing may reduce the prevalence of undiscovered minimal residual illnesses, enabling early care, which is essential for Acute Lymphocytic Leukemia patient survival.

Source: Polaris Market Research Analysis

Test Technique Analysis

Flow cytometry dominated the market in 2024 due to the excellent sensitivity and extensive applicability of MRD testing made possible by flow cytometry. The clinical care of individuals with acute leukemia places a growing emphasis on minimal residual disease testing. Among the technologies for monitoring MRD, flow cytometry has the most potential for clinical usage due to its ease of use and accessibility. Numerous investigations have supported the validity of the method by demonstrating high relationships between MRD levels measured by flow cytometry during clinical remission and treatment results.

Identification of the immune-phenotypic combinations which are expressed in the leukemic cells but not in the healthy hematopoietic cells forms the basis for the flow cytometry detection of MRD. The specificity of the immunophenotypes employed to identify the leukemic cells and the quantity of study cells determine the sensitivity of the method. A cancer cell can be found with this technology out of 10,000 to 100,000 healthy bone-marrow cells, depending on the flow cytometry setting and results can be available in less time than a day.

End User Analysis

In 2024, the segment that accounted for the largest revenue share is hospitals and specialist clinics. The primary reason for driving the market is that hospitals have professionals that can assist patients in selecting relevant MRD tests. The prevalence of the target ailment is on the rise, there are many testing alternatives available, and new tests are being introduced for more accurate and efficient patient screening.

Additionally, hospitals routinely provide services for both acute and complex disorders, which enhances and supplements the functioning of numerous other components of the healthcare system. External influences, shortcomings in health systems, and issues with the hospital industry globally are currently driving a new vision for hospitals. They are essential to the vision's efforts to reach out to the local population, offer services at home, and assist other healthcare providers.

Regional Analysis

North America Minimal Residual Disease Market Assessment

North America dominated the market in 2024 due to rising healthcare affordability in the U.S. North America is controlling the minimal residual disease industry. Due to a high level of patient and physician awareness of the advantages associated with screening, the U.S. and Canada are the two main markets for cancer screening in North America. Additionally, a number of projects are being implemented to offer MRD testing in the area. For instance, Natera secured a country-wide minimal residue disease testing contract with the U.S. Department of Veterans Affairs (VA) National Precision Oncology Program, in November 2022.

Asia Pacific Minimal Residual Disease Market insights

Asia Pacific market is expected to witness significant growth during the forecast period due to the rise in disease burden. The rise in disease incidence of hematological cancers such as lumphoma and leukemia is due to the changing lifestyles, aging populations, and improved diagnostic capabilities. The prevelence of these disease creates expanding number of cases which requires proper monitoring, contributing to the demand for refined MRD testing solutions for treatment decisions and also for long term outcomes.

Source: Polaris Market Research Analysis

Competitive Insight

Some of the major players

- Sysmex Corporation

- ArcherDX

- Adaptive Biotechnologies

- Natera

- Inivata

- Asuragen

- Guardant Health

- Cergentis

- Invivoscribe

- Mission Bio

- ARUP Laboratories

- NeoGenomics Laboratories

- Bio-Rad Laboratories

- Opko Health

- Sysmex Corporation

- Quest Diagnostics.

Recent Developments

- June 2025: QIAGEN collaborated with Tracer Biotechnologies and Foresight Diagnostics to advance the use of minimal residual disease (MRD) testing in clinical trials to support pharma co-development projects for companion diagnostics.

- August 2022: Roche launched the company’s first digital polymerase chain reaction (PCR) system named the Digital LightCycler System which detect diseases and is designed to accurately quantify trace amounts of specific RNA and DNA.

- February 2021: Guardant launched a test for recurrence monitoring and residual disease named Guardant Reveal Liquid Biopsy Test.

Minimal Residual Disease Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 2.53 billion |

| Market size value in 2025 | USD 2.87 billion |

| Revenue forecast in 2034 | USD 9.16 billion |

| CAGR | 13.7% from 2025 - 2034 |

| Base year | 2024 |

| Historical data | 2020 - 2023 |

| Forecast period | 2025 - 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Segments covered | By Detection Target, By Test Technique, By End Use, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Key companies | Sysmex Corporation, ArcherDX, ICON plc, Asuragen, Mission Bio, ARUP Laboratories, Guardant Health, Cergentis B.V., Invivoscribe, NeoGenomics Laboratories, Bio-Rad Laboratories, Opko Health, Adaptive Biotechnologies, Natera, Inivata, Sysmex Corporation, and Quest Diagnostics |

Source: Polaris Market Research Analysis

We strive to offer our clients the finest in market research with the most reliable and accurate research findings. We use industry-standard methodologies to offer a comprehensive and authentic analysis of the minimal residual disease market. Besides, we have stringent data-quality checks in place to enable data-driven decision-making for you.

minimal residual disease market FAQ's

key segments are detection target, test technique, end-user and region.

Minimal Residual Disease Market Size Worth USD 9.16 Billion By 2034.

The global minimal residual disease market expected to grow at a CAGR of 13.7% during the forecast period.

North America is leading the global market in 2024.

key driving factors are Increasing Prevalence Of Cancer and Growing Investment For Research.

Download Sample Report of minimal residual disease market

Please fill out the form to request a customized copy of the research report.