Nanosatellite and Microsatellite Market Research Report, Share and Forecast, 2026 – 2034

REPORT DETAILS

Nanosatellite and Microsatellite Market Summary

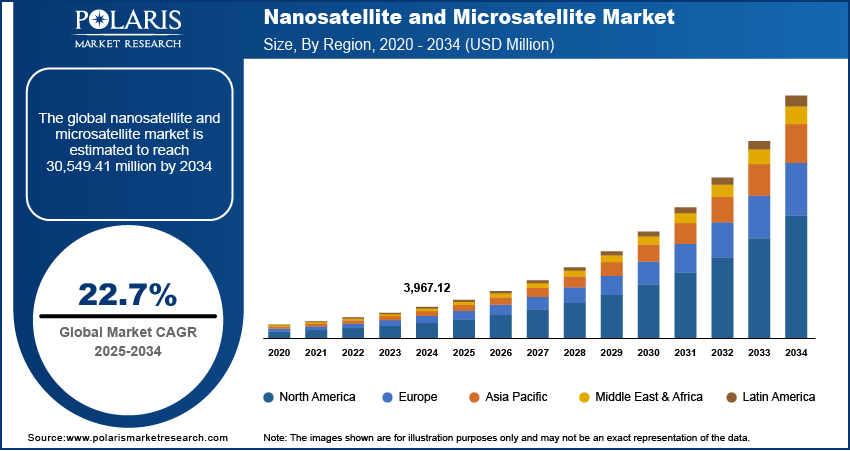

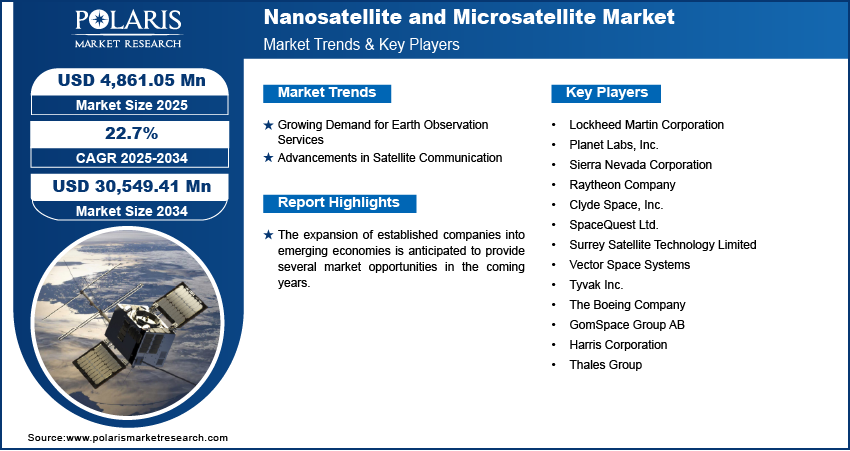

The global nanosatellite and microsatellite market size was valued at USD 4,861.05 million in 2025. The market is projected to account for a CAGR of 22.7% between 2026 and 2034. Market growth is primarily driven by increasing demand for cost-effective, lightweight platforms for Earth observation and satellite communication. It also benefits from technological advancements and expanding government and commercial applications.

Market Statistics

Key Takeaways

- The North America nanosatellite and microsatellite market led the market with a 42.4% revenue share in 2025 due to significant funding for advanced satellites from both government and private bodies.

- In Europe, the market is projected to register a notable CAGR of 24% due to the advancement of microsatellite technology for Earth observation and scientific endeavors.

- The nanosatellite segment accounted for the largest market share of 76.41% in 2025. This is due to the increased deployment of nanosatellites for various applications.

- The scientific research & academic training segment is projected to account for a significant CAGR of 20.4% from 2026 to 2034 because of the growing usage of nanosatellites and microsatellites in academic and research bodies.

- The commercial segment held the largest nanosatellite and microsatellite market share of 47.1% in 2025. Rising usage of nanosatellites and microsatellites for various commercial applications contributes to the segment’s leading market position.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The requirement for high-resolution earth imaging has escalated across several sectors, as it can be used for various applications and productive management of forest, land, and water resources, which is driving market growth.

- Nanosatellites and microsatellites are playing a crucial role in improving satellite communication systems by configuring constellations to provide worldwide coverage and seamless connectivity.

- With firms operating extensive satellite fleets seeking lighter, more economical platforms, there is a growing demand for low-cost nanosatellites and microsatellites.

- Technical and operational challenges of nanosatellites and microsatellites may limit market growth.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

AI Impact on Nanosatellite and Microsatellite Market

- AI helps speed up data processing. This helps users get results more quickly.

- AI improves image quality and analysis. This makes it easier to track weather, crop, and environmental changes.

- The technology allows satellites to work in a more independent way. This lowers the need for constant human control.

- It lowers costs by improving performance and reducing errors.

Microsatellites are artificial satellites with a mass ranging from 10 kg to 100 kg, including fuel. They have been designed through the process of miniaturization of current satellites along with the use of advanced microsatellite technologies in imaging equipment, peripherals, construction materials, algorithms, and many others. Nanosatellites, on the other hand, are small satellite systems with a weight of about 1kg up to 10kg and size of roughly 30-by-10-by-10 cm. The satellites are characterized by affordability, lightweight nature, ease of manufacturing and development, and computational capability.

The main applications of nanosatellites include academic space missions, technology demonstration satellites, affordable communication experiments, and sensing. More advanced applications such as high-resolution imaging, military uses, commercial communication, and missions requiring better performance are done by microsatellites. The nanosatellite vs microsatellite distinction is significant for the selection process because it depends on the specific requirements of the mission, satellite payload performance, and anticipated gains from the project.

The nanosatellite and microsatellite market is mainly driven by the need for low-cost satellite platforms and rapid deployment satellites that can perform their tasks efficiently and cost less than big satellites. Nanosatellites and microsatellites have been widely adopted because of various factors. These include rapid production, lower launch costs, easy deployment in satellite constellations, and mission flexibility.

A structural shift in the industry is the transition from the use of one big satellite to multiple small satellite constellations. This improves efficiency and minimizes risk. It helps provide various services such as mapping, maritime surveillance, navigation, and environmental monitoring. This results in increased demand for nanosatellites and microsatellites not only in developed countries but also in developing ones.

The growing microsatellite and nanosatellite adoption is driving the nanosatellite and microsatellite market growth. As companies operating large satellites seek lighter, cost-effective platforms, demand for low-cost nanosatellites and microsatellites is increasing. The rising usage of data provided by nanosatellites and microsatellites in the commercial and civil sectors further boosts commercial satellite demand.

The rising interest of governments in nanosatellites for Earth observation and defense applications, and the low cost of developing and operating microsatellites, are anticipated to support the development of the nanosatellite and microsatellite markets in the coming years. For instance, according to NASA, over 1,700 small satellites (including nanosatellites) were launched globally in 2023 alone. This reflected a sharp increase in government-backed and commercial missions. The expansion of established companies into emerging economies is anticipated to provide lucrative market opportunities during the forecast period.

Market Dynamics

Growth Drivers

Rising Demand for Earth Observation Services

Earth observation (EO) is the process of collecting information about the Earth’s surface, atmosphere, and waters. Earth observation services gather data for a variety of purposes, including weather forecasting, climate monitoring, ecosystem accounting, and climate mitigation and adaptation. The need for high-resolution Earth imaging has increased across various sectors, as these images can be used for various applications, such as efficient management of forest, land, and water resources. Also, space-based imaging can help fulfill a country’s security, infrastructure analysis, and disaster management needs. For instance, in July 2025, NASA and the Indian Space Research Organisation (ISRO) collaborated to launch the NISAR mission. According to ISRO, the mission uses advanced L-band and S-band dual-frequency radar. It will provide high-resolution, time-series imagery for global monitoring of ecosystems and climate change every 12 days. Thus, the rising demand for Earth observation is fueling the nanosatellite and microsatellite market development.

Advancements in Satellite Communication

Nanosatellites and microsatellites have been critical in improving satellite communication systems over the past few years. Such satellites can form communication constellations, enabling global coverage and connectivity. For example, as of March 2026, more than 10,000 Starlink satellites from SpaceX are operating in low Earth orbit (LEO) and communicating with ground transceivers. The constellation has significantly expanded global broadband coverage. Also, nanosatellites and microsatellites can help bridge the digital divide and offer access to basic services in isolated regions, and improve remote area connectivity. Nanosatellites and microsatellites support satellite-based connectivity for remote sensing, asset tracking, and communication. Thus, the ability of nanosatellites and microsatellites to improve satellite communication systems contributes to the nanosatellite and microsatellite market expansion.

Rise of Newspace Economy

The emerging NewSpace market economy is further contributing to market development. More private firms, startups, and investors are joining the space industry, thus exploring sectors that used to be the responsibility of government agencies. For instance, in February 2026, Rocket Lab USA. Inc. signed a multi-launch deal with BlackSky Technology Inc. The company revealed that the deal will further expand its service as the primary launch provider for Blacksky. This has led to increased demand for small-satellite hardware, payload systems, and launch capabilities.

Market Restraints

Despite its rapid growth, there are some small-satellite challenges to overcome. Nanosatellites and microsatellites face constraints due to limited onboard space, which affects their payload capacity, power, and endurance. This, therefore, means that the use of these satellites may not fit into complex missions that require advanced satellite power systems and long mission endurance.

However, the nanosatellite and microsatellite market is also confronted with external problems, including launch bottlenecks, orbital congestion, spectrum management, and space debris mitigation. With the increasing number of small satellites being launched, organizations will have to adhere to stricter regulations concerning their environmental impact on space. This will affect their future designs, insurance rates, and clearance processes.

Market Opportunities

Expansion into emerging space economies by established firms presents new satellite market opportunity. There is increasing demand from nations seeking to build their own earth observation systems, low-cost communications infrastructure, and strong technological expertise.

Growth is expected in constellation-based services across sectors such as remote sensing, maritime intelligence, IoT satellite connectivity, and environmental monitoring. As satellites are becoming smaller with improved capabilities, and the reliability of launching satellites has increased significantly, investment in satellite constellations for data collection would increase rather than single satellite operations.

Source: Polaris Market Research Analysis

Segment Insights

By Type Insights

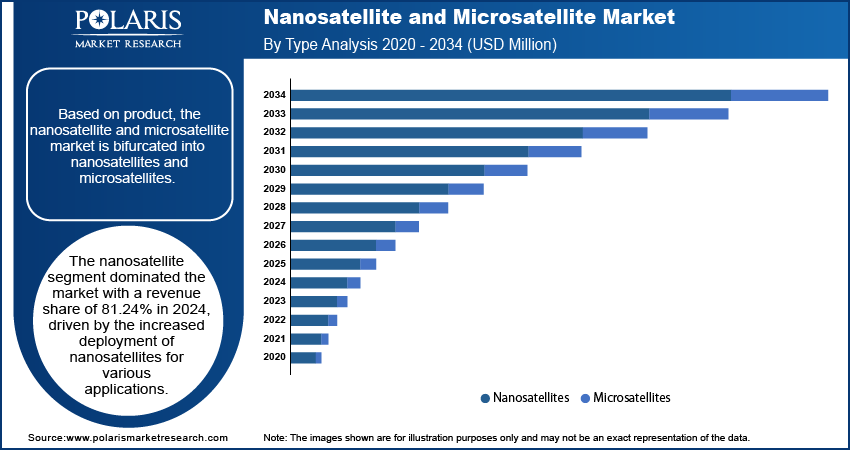

The nanosatellite and microsatellite market, based on type, is bifurcated into nanosatellites and microsatellites. The nanosatellite segment led the market with a nanosatellite market share of 76.41% in 2025, driven by the increased deployment of nanosatellites for various applications. Nanosatellites are cost-effective and can be produced more quickly than their large counterparts. Also, the versatility of these satellites enables them to be used for a range of applications, such as scientific research satellites, remote sensing nanosatellites, and data collection satellites. These benefits of nanosatellites contribute to their high popularity and solidify their position as the leading segment in the market.

Microsatellites have a smaller market share. But they are still important for missions that need higher performance. Microsatellite applications include defense, Earth observation microsatellites, and communication satellites, where better onboard systems and longer operation can justify higher costs.

By Component Insights

By component, the nanosatellite and microsatellite market can be assessed across hardware, software and data processing, launch services, and space services. The hardware segment accounted for 43% revenue share in 2025. Hardware remains a significant source of value as operators spend on payload systems, communications satellite hardware, processors, propulsion systems, sensors, attitude control, and power generation systems.

As small satellites collect more and more imagery and RF intelligence, software and data processing have become increasingly vital from a strategic perspective. As customers demand more actionable insights rather than just satellite data, there will likely be a growing need for onboard processing capabilities and AI- enabled satellite analytics.

Launch services continue to be essential to commercialization, since rideshare missions and increased orbital access have facilitated lowering the threshold to entry. At the same time, the ability to predict schedules, compatibility of launch, and mission integration have become increasingly important purchase parameters.

Space services, such as mission operators, ground segment support, and onboard data processing, are likely to be increasingly important as satellite fleets grow. The role of the space services layer is to aid the shift of the small satellite industry from hardware-driven to a holistic space ecosystem.

By Orbit Insights

By orbit, the nanosatellite and microsatellite market is segmented into low earth orbit (LEO), medium earth orbit (MEO), geostationary orbit (GEO), Sun-synchronous orbit, and polar orbit. The low earth orbit (LEO) segment dominated the market with a 78% revenue share in 2025. The LEO satellite category is significant because it enables low-latency operation, enhanced imaging resolution, and ease of constellation formation for LEO communication applications and Earth observation satellites.

Medium earth orbit (MEO) and geostationary orbit (GEO) are less used in very small satellites. However, they are important for certain navigational, communication-based, and mission-specific applications. Microsatellites, compared to nanosatellites, are more suited to fulfill the demands of these orbits if the mission requires it.

Sun-synchronous and polar orbits remain highly suitable for Earth observation applications due to their consistent illumination and good coverage. Thus, orbital considerations become a significant commercial decision rather than just an engineering one.

By Application Insights

Based on application, the market is segmented into Earth observation, communication, technology demonstration, biological experimentation, scientific research & academic training, and others. The scientific research & academic training segment is anticipated to register a significant CAGR of 20.4% from 2026 to 2034. This is because of the increasing need for satellites used in scientific research and academic training. Such satellites allow scientists and researchers to perform experiments and gather data about greenhouse gases at a more affordable price and efficiency level. Moreover, the quick development of such satellites allows for better progression of research projects.

Earth observation is among the most significant application domains of small satellites. Small and miniature satellites are extensively applied for land use mapping, crop health monitoring, weather analysis, maritime domain awareness, disaster response management, and infrastructure monitoring. The frequent data collection capability and reduced costs make them ideal for users who require timely geospatial data updates.

Other areas of use include those related to communication, where there is a requirement to establish connections with distant and disadvantaged locations. The satellites serve various purposes, including broadband satellite connectivity, Internet of Things communication, military applications, and special business communications. Small satellites are also increasingly used in constellations.

Technology demonstration is another important segment. This process enables companies and governments to experiment with advanced technologies, such as propulsion, sensing devices, artificial intelligence for control, and onboard data processing, in space without deploying everything on a large scale. Thus, technology demonstration plays a significant role in driving demand for technology demonstration satellites.

By End Use Insights

Based on end use, the market serves defense, civil and construction, government, energy, commercial, and other sectors. The commercial segment dominated the nanosatellite and microsatellite market with the largest market share of 47.1% in 2025. Small satellites have seen increased usage from commercial customers. Applications include geospatial analysis, communications, supply chain monitoring, logistics intelligence, asset tracking, and environmental risk analysis.

The government and defense sectors remain major parts of the industry. The agencies continue to invest in the areas of earth observation, surveillance, secure communications, and science applications. The national security needs and sovereignty in space are projected to ensure sustained demand.

Also, the use in civil, energy, and infrastructure purposes is on the rise. The small satellites have been used for pipeline monitoring, tracing of utilities, and renewable energy site assessment. They also help in the land use assessment and disaster preparation. This shows how versatile satellite data can be beyond the space sector.

Source: Polaris Market Research Analysis

Regional Analysis

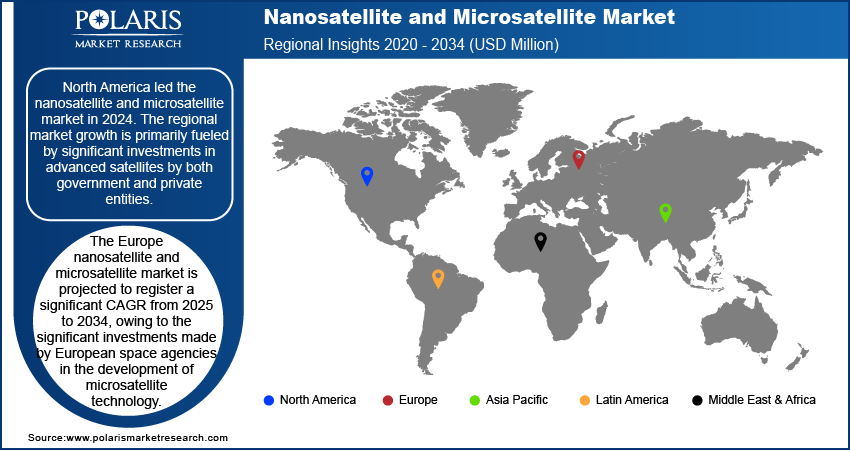

By region, the report covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America led the global market with a 42.4% revenue share in 2025. The regional market growth is primarily fueled by significant investments in advanced satellites by both government and private entities. Also, the presence of several market participants leading small satellite innovation contributes to the North America nanosatellite market development.

In addition, the prominent regional presence of North America can be attributed to its robust defense space ecosystem, its growing commercial launch environment, and more venture capital funding and institutional procurement. These have all contributed to making North America one of the key centers for the development and launching of nanosatellites and microsatellites.

The Europe nanosatellite and microsatellite market is projected to register a notable CAGR of 24% from 2026 to 2034. Space agencies across Europe are making significant investments in developing microsatellite technology for Earth observation and scientific missions. Further, market participants and European academic institutions are developing innovative solutions for microsatellites and investigating novel applications in environmental monitoring and maritime surveillance, thereby propelling market growth in the region.

The Asia Pacific region will continue to play a vital role in global growth as both governments and private companies develop satellites for communication, agriculture, emergency management, and navigation, and enhance their national space capability. The Asia Pacific satellite market is further supported by the increasing ability of local industry and government sectors to gain affordable access to space.

Latin America and the Middle East & Africa can be considered emerging opportunity areas. The potential demand is expected to be driven by climate monitoring, border surveillance, telecommunications availability, smart agriculture satellites, and government reform initiatives. Although the Latin America satellite market and Middle East satellite demand are currently smaller, they may offer lucrative opportunities for specialized, cost-effective mission implementation.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The market consists of both established nanosatellite companies and new microsatellite manufacturers that emphasize modularity, affordability, and specialization of their platforms. Major companies are constantly striving to improve their products, integrate payloads, and strategically form satellite partnerships to enhance their competitive edge.

The nanosatellite and microsatellite market research report offers a market assessment of all the leading market players, including Lockheed Martin Corporation; Planet Labs, Inc.; Sierra Nevada Corporation; Raytheon Company; Clyde Space, Inc.; SpaceQuest Ltd.; Surrey Satellite Technology Limited; Vector Space Systems; Tyvak Inc.; The Boeing Company; GomSpace Group AB; Harris Corporation; and Thales Group.

The increasing competitive pressure is being felt in differentiating oneself through satellite modularity, rapid manufacturing, mission-critical payload integration, autonomous flight, and post-flight analysis. Apart from the traditional comparison between competing firms, the competitive structure is increasingly becoming organized along the lines of ecosystems, which include platform providers, earth observation service providers, defense firms, launch providers, and analytics service providers.

Those companies capable of integrating space vehicle capabilities with analysis, operations management, and deployment support will probably gain an edge over time. This transition implies that value creation in the industry is no longer dependent solely on technology but also on comprehensive service provision.

Lockheed Martin Corporation is one of the major players in the nanosatellite and microsatellite market. This is due to its experience in the field of defense and space technology. In particular, Lockheed Martin concentrates on the creation of satellites with innovative payloads for tasks related to Earth observation, telecommunication purposes, and security projects.

The Boeing Company has been growing its presence in the small-satellite market. The company focuses on developing new satellite designs and advancing its production processes. Boeing provides scalable satellite solutions that work effectively for low Earth orbit constellations and have applications such as broadband and data analytics. Boeing’s expertise in aerospace and program management makes it easier for the company to meet demand in the nano/microsatellite market.

List of Key Companies

- Clyde Space, Inc.

- GomSpace Group AB

- Harris Corporation

- Lockheed Martin Corporation

- Planet Labs, Inc.

- Raytheon Company

- Sierra Nevada Corporation

- SpaceQuest Ltd.

- Surrey Satellite Technology Limited

- Thales Group

- The Boeing Company

- Tyvak Inc.

- Vector Space Systems

Industry Developments

- January 2025: GomSpace launched a modular nanosatellite platform. The platform is built to support high-performance payloads with advanced power systems and autonomous navigation capabilities.

- November 2024: Surrey Satellite Technology Limited made an announcement about signing a deal with the Ministry of Defense of the UK for providing an Earth observation satellite. SSTL revealed that the satellite called Juno is expected to be launched in 2027 and make pictures of the Earth’s surface during daylight hours to support military operations.

- August 2024: Surrey Satellite Technology Limited (SSTL) made an announcement about taking part in the Small Satellite Conference 2024 and discussed its progress in small satellite development as well as its role in different space missions and innovations, particularly in the area of Earth observation and communications.

- August 2024: Sierra Nevada Corporation (SNC) made an announcement about important advances in its Vindlér commercial radio frequency (RF) technology through the collaboration with Muon Space. SNC emphasized that the new partnership would contribute to producing three more satellites to SNC’s constellation.

Nanosatellite and Microsatellite Market Segmentation

By Type Outlook (Revenue, USD Million, 2021–2034)

- Nanosatellites

- Microsatellites

By Component Outlook (Revenue, USD Million, 2021–2034)

- Hardware

- Software and Data Processing

- Launch Services

- Space Services

By Orbit Outlook (Revenue, USD Million, 2021–2034)

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

- Sun-Synchronous Orbit

- Polar Orbit

By Application Outlook (Revenue, USD Million, 2021–2034)

- Earth Observation

- Communication

- Technology Demonstration

- Biological Experimentation

- Scientific Research & Academic Training

- Others

By End Use Outlook (Revenue, USD Million, 2021–2034)

- Defense

- Civil and Construction

- Government

- Energy

- Commercial

- Others

By Regional Outlook (Revenue, USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Nanosatellite and Microsatellite Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 4,861.05 million |

| Market Size in 2026 | USD 5,957.62 million |

| Revenue Forecast by 2034 | USD 30,549.41 million |

| CAGR | 22.7% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Nanosatellite and Microsatellite Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Nanosatellite and Microsatellite Market FAQ's

The global nanosatellite and microsatellite market was valued at USD 4,861.05 million in 2025 and is projected to reach USD 30,549.41 million by 2034.

The market is primarily driven by increasing demand for Earth observation and satellite communication. Improvements in miniaturization and launch access are also supporting expansion.

North America accounted for the largest market share of 42.4% in 2025. The regional market dominance is driven by strong government funding and commercial investment.

The nanosatellite segment accounted for the largest market share of 76.41% in 2025. This is owing to its lower cost and faster deployment cycle.

The scientific research & academic training segment is expected to register strong growth as universities and research bodies increase the use of small satellites for experiments and training missions.

A nanosatellite typically weighs 1–10 kg, while a microsatellite generally weighs 10–100 kg. Microsatellites usually support more complex payloads. Nanosatellites offer lower-cost access to focused missions.

The market offers exposure to hardware sales, launch services, satellite operations, analytics, and recurring data-driven business models. This creates multiple revenue opportunities.

Download Sample Report of Nanosatellite and Microsatellite Market

Please fill out the form to request a customized copy of the research report.