Needle-Free IV Connectors Market Share, Size, Trends, Industry Analysis Report, 2020-2027

REPORT DETAILS

REPORT DETAILS

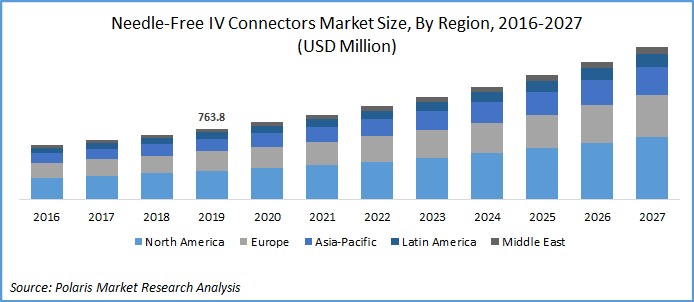

The global needle-free IV connectors market was valued at USD 763.8 million in 2019 and is expected to grow at a CAGR of 10.2% during 2020-2027. The prominent factors responsible for the market growth are rising economic burden from blood stream infections with longer hospital stays for the patient, preference of healthcare practitioners towards minimal invasive procedures, and increasing prevalence of peripheral and cardiovascular disorders. Worldwide diabetic population coupled with ever growing proportion of geriatrics also contributing to use of access devices, thereby inducing the demand for needle-free IV connectors. According to the International Diabetes Federation (IDF), the number of people suffering from diabetes was 415 million in 2015, which is expected to reach approximately 640 million by 2040.

Industry Dynamics

Growth Drivers

The increasing number of chronic ailments coupled with the rapidly aging population and increasing hospitalization rate globally is set to increase the demand needle-free IV connectors. According to WHO report, the population of people above 65 years was around 524 million in 2010, which is expected to grow to 1.5 billion by 2050; this would be 16% of the total world population. Additionally, increasing number of cardiovascular diseases drives the growth of the market. For example, according to WHO, about 17.3 million people died from cardiovascular disease (CVD) in 2008 and the number is expected to increase to 23.3 million by 2030. This increase in number of patients suffering from cardiovascular disease across the world will boost the market.

Know more about this report: Download Sample Report

Know more about this report: Download Sample Report

Moreover, the increase in hospital admissions is anticipated to increase the demand of needle-free IV connectors, which will drive the market. According to the Center for Disease and Control (CDC) statistics, published in 2014, the number of out-patient hospital visits per 100 persons was 41 and the percentage of persons with overnight hospital stays stood at 7.3%.

Furthermore, the increasing frequency of pandemic such as COVID-19 is expected to increase substantial demand for catherization in clinics, hospitals and ambulatory surgical units. This will stimulate the substantial rise in the usage of the product.

Know more about this report: Download Sample Report

Know more about this report: Download Sample Report

Challenges

The needle-free connectors market is hindered with few factors namely, risk and complications associated with the devices, stringent product approvals, competition from local players, and the increasing concerns over reimbursements. The rising incidence of catheter-associated bloodstream infections (CABSI) in patients. According to CDC estimations, more than 80,000 people develop catheter-related bloodstream infections in the US each year. The misplacement of the vascular device may result in clotting, infection, and kinking. In some cases, it might result in admixing of blood from the catheter.

Needle-Free IV Connectors Market Report Scope

The market is primarily segmented on the basis of Mechanism, Design Type, by Dwell Time, By End-Use, and by geographic region.

| By Mechanism | By Design Type | By Dwell Time | By End-Use | By Region |

|

|

|

|

|

Know more about this report: Download Sample Report

Insight by Mechanism

Based upon the mechanism, the global market is categorized into positive, negative, and neutral mechanisms. In 2019, the device with positive mechanism accounted for the largest share and it is expected to dominate over the study period. The growth was due to technological advancements such as the prevention of fluid reflux to prevent blood stream infections. According to CDC in 2014, every year nearly 30,100 CABSI cases occur in ICU and wards of hospitals in the US.

Insight by Design Type

On the basis of design type, the global market is bifurcated into straight channel, T-channel, Y-channel, and multi-channel. In 2019, Y-channel segment accounted for the largest market share. This large proportion was due to the usage of these devices in drug administration for the treatment of multiple diseases, and cancer treatments.

Insight by End Use

Based on end use, the global market is categorized as hospitals, surgical centers (ASC), and others. In 2019, the hospital segment garnered the largest market share. The high share of the segment is due to the fact that most of the vascular access procedures for medication, drug dose was carried out in hospital settings. The rising number of hospital admissions with chronic ailments and number of old age people in the high income countries also favoring this trend.

Geographic Overview

Geographically, North America is the largest contributor in the Needle-Free IV Connectors market, followed by Europe and Asia Pacific. In 2019, North America dominated the global market with 45% share. The U.S. was the largest revenue contributor to the market in this region. The increased prevalence of chronic disorders, increasing geriatric population and increased usage of safety intra-venous devices has driven the market. Manufacturers in the US are focusing on acquisitions and partnerships to increase their market share as the market is fragmented and the entry of new players is increasing the competition.

The market in this region is expected to grow at a moderate pace during the forecast period due to the end-users’ shift toward safety catheters. It is gaining popularity as healthcare cost increased in the US. The key players operating in the US are adopting strategies such as product innovation and product line extension to increase their market share.

The market in APAC is growing at a faster rate than other regions due to the growing prevalence of diabetes and other chronic diseases. The major countries contributing to the revenue of this region are Japan, India, and China. In recent years, the incidence of diabetes has increased in this region because of globalization and changes in lifestyle. The factors driving the market growth in this region are increasing disposable income, growing awareness among consumers about sophisticated self-care systems, and increasing number of new healthcare institutions and public health systems. Japan is the largest developed market in APAC, owing to the high percentage of the older adult population, who are prone to old age diseases. Also, healthcare expenditure is relatively high in Japan compared with other countries such as India and China.

APAC is anticipated to witness the fastest growth rate during the forecasted period. Rising demand, the rise in older adult population, and improvements in healthcare infrastructure are some of the significant growth drivers of the market. Local manufacturers in APAC are offering low-cost products and services, which has created stiff competition for multinational companies. China, India, Thailand, and Singapore are witnessing the rapid growth in the market and are predicted to emerge as dominating markets in the future. Therefore, growing healthcare awareness is expected to contribute to the growth of the market during the forecast period.

Competitive Insight

The global needle-free IV connectors market is highly competitive and well-organized. The key players operating in the market include RyMed Technologies, LLC, Baxter International Inc., CareFusion Corporation, B. Braun Melsungen AG, Nexus Medical LLC, Becton, Dickinson and Company, ICU Medical, Inc., and Vygon S.A.

Download Sample Report of Needle-Free IV Connectors Market Share, Size, Trends, Industry Analysis Report, 2020-2027

Please fill out the form to request a customized copy of the research report.