PAN-based Carbon Fiber Market Insights and Growth Opportunities, 2026-2034

REPORT DETAILS

PAN-based Carbon Fiber Market Summary

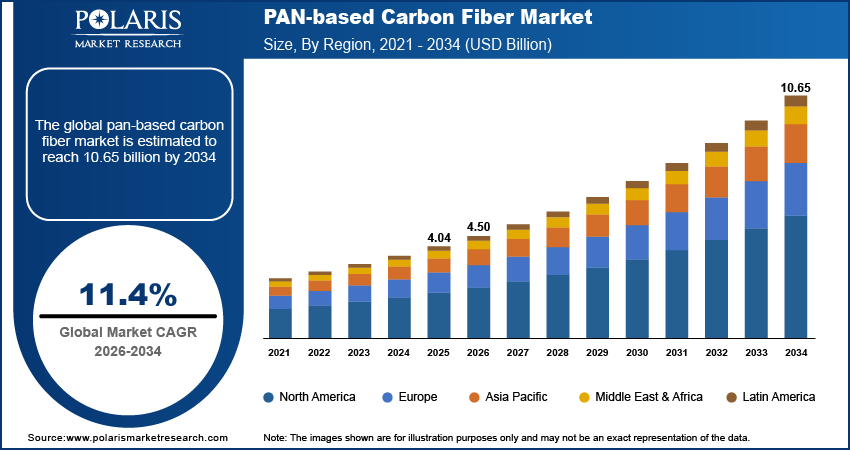

The PAN-based carbon fiber market was valued at USD 4.04 billion in 2025. The market is projected to grow at a CAGR of 11.4% from 2026 to 2034. Lightweighting in aerospace and EVs and the increased need for wind energy blades are driving global carbon fiber growth.

Market Statistics

Key Takeaways

- North America led the global market with a 37.10% revenue share in 2025. The regional market dominance is driven by strong aerospace demand.

- Asia Pacific is expected to experience a CAGR of 8.1%. This is due to the increasing application of carbon fiber in wind turbines in renewable energy projects.

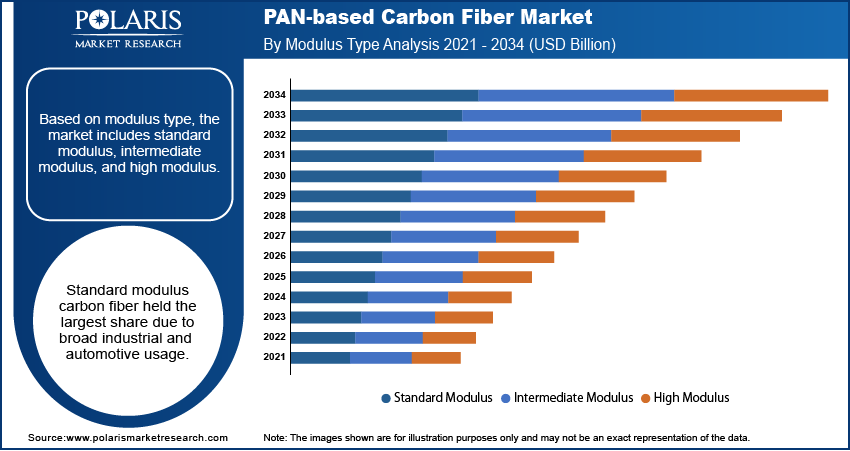

- The standard modulus category held 45.12% market share in 2025. The standard modulus provides balanced tensile strength characteristics at an optimal price level.

- The non-composites segment is projected to grow at a 7.3% CAGR, as it caters to niche PAN-based fiber applications of carbon fiber.

- The aerospace & defense segment dominated with 32.23% share in 2025, with a huge demand in the aerospace carbon fiber market for high-strength and lightweight material.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

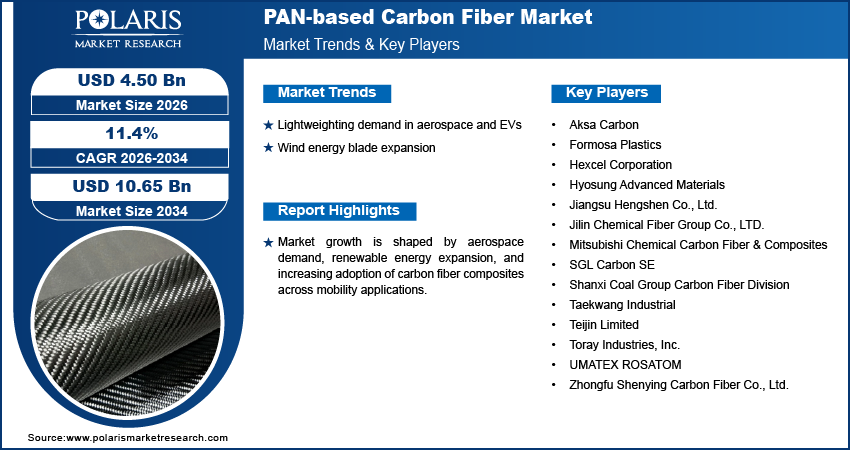

- Aerospace and EV lightweighting is boosting carbon fiber demand.

- Wind turbine installations are increasing composite consumption.

- High production cost limits mass-market adoption.

- Recycling and PAN precursor optimization support long-term growth.

AI Impact on PAN-based Carbon Fiber Market

- AI assists in improving the process of PAN-based carbon fiber manufacturing by optimizing manufacturing conditions and minimizing material waste.

- It improves quality assurance by detecting defects and ensuring uniformity of the fibers’ strength and performance.

- It facilitates predictive maintenance by enabling early detection of machine defects, thereby minimizing downtime.

- AI helps fast-track the product development process by analyzing material properties.

What is PAN-based Carbon Fiber?

The PAN-based carbon fiber market centers on carbon fibers produced using a PAN precursor, where polyacrylonitrile serves as the primary raw material rather than a finished product. PAN precursor fibers are thermally processed under control to convert into high-strength carbon fiber with a balanced combination of tensile strength, modulus, and consistency. This route of production allows for large-scale manufacture and places PAN-based carbon fiber as the dominant material in the global carbon fiber composites industry.

Compared to pitch-based carbon fibers, PAN-based carbon fibers possess higher tensile strength and improved damage tolerance. Pitch-based carbon fiber is characterized by better stiffness and thermal conductivity but represents higher cost with limited scalability. PAN precursor processing allows for better cost control and higher production volumes, with greater participation of suppliers. These factors contribute to the enhanced commercial position of PAN-based carbon fiber in industrial markets requiring reliable mechanical performance.

Source: Polaris Market Research Analysis

The applications of the market solution for PAN carbon fibers include aerospace, wind energy, automotive, pressure vessels, and sports equipment. According to the IEA, aviation accounted for 2.5% of the total energy-related CO2 emissions in 2023, and this amount has just about reached 950 MtCO2, which is above 90% of the pre-COVID levels. The strength carbon fiber from the PAN precursor helps in the development of light-weight materials with enhanced fuel efficiency and strength properties. The carbon fiber composites based on the PAN carbon fiber satisfy the requirements in the industry, which include durability, scalability, and financial viability.

Drivers & Opportunities

Lightweighting demand in aerospace and EVs: The drivers for carbon fiber are becoming more robust with the emphasis by both aerospace and electric vehicles companies on reducing weight. As per the IEA Global EV Outlook 2025, global electric car sales crossed 17 million in 2024, accounting for over 20% of new car sales worldwide. Aerospace carbon fiber demand is supported by rising aircraft production and fleet modernization, while EV lightweight materials improve driving range and battery performance. Carbon fiber composites deliver high strength-to-weight ratios across critical structural components.

Wind energy blade expansion: The demand for carbon fibers in the wind sector is rising due to the growing size of wind blades and rotor diameters. The use of carbon fibers is beneficial in a turbine as they are stiffer and offer better fatigue attributes compared to other materials. Expansion of offshore and onshore wind installations sustains long-term material demand. The Global Wind Energy Association stated that total installed wind power capacity in the world was estimated to be around 1,174 GW at the end of 2024, with new additions contributing to meeting overall power demand.

Technological Advancements in Carbon Fiber Manufacturing: New technological advancements in the PAN-based carbon fiber market have increased production efficiency and effectiveness. Research on less expensive precursors and improved carbonization processes is underway to minimize costs and facilitate the commercialization of these fibers. Recycling carbon fibers is one of the solutions companies consider to engage in sustainable operations. There are improvements in automation and the use of modern production methods, such as automated fiber placement and robotics, which minimize errors while facilitating mass production. Such trends are driving improvements in production capabilities.

Sustainable Lightweight Materials and Energy Efficiency: The concepts of sustainability and energy efficiency are now on the rise, leading to the adoption of carbon fiber composite materials made from polyacrylonitrile (PAN). The application of carbon fiber composite materials contributes to making transportation systems, aircraft, and manufacturing equipment lighter, reducing fuel consumption and increasing energy efficiency without emitting any greenhouse gases. This material is now widely used by companies in the automotive and aviation industries, as it helps make their products more efficient and eco-friendly. Another use for this material is in renewable energy. Carbon fiber composite materials are used in manufacturing wind turbine blades to increase energy efficiency.

Restraints & Challenges

High production costs: The cost associated with the processing of carbon fibers is proving to be a major hindering factor in price-sensitive applications. Processing, stabilization, as well as carbonization of PAN, add up to an additional cost associated with the processing of carbon fibers.

Energy-intensive manufacturing: Carbon fibers are engaged in a high-temperature processing procedure as they require a constant input of energy. Energy use is known to contribute to costs and carbon emissions. Scalability is affected by the use of high-priced energy and access to low-carbon energy resources.

Opportunities

Hydrogen pressure vessels: Hydrogen storage solutions also need materials that are light with high strength to be used in the fabrication of high-pressure containers. Carbon fiber materials are used in high-pressure containers to cut down on the total weight of the container. Growth in hydrogen mobility and energy storage supports new demand channels for advanced fibers. As an example, IACMI received USD 2.7 million from the U.S. DOE to cut high-performance carbon fiber manufacturing costs by 25% for composite hydrogen and natural gas storage tanks used in vehicles.

Sustainable PAN precursors and recycling: Sustainable level of carbon fiber research is ongoing via bio-based PAN precursors and composite recycling at the end-of-life products. Carbon fiber supply chain management is integrated with sustainable goals in the aviation and wind energy sectors and electric vehicles with research into bio-based PAN precursors and recycling of composite wastes.

Source: Polaris Market Research Analysis

Segmental Insights

This report provides comprehensive coverage of the PAN-based carbon fiber market by modulus type, application, and end-use industry to enable the audience to select the segment with the greatest level of growth.

By Modulus Type

-

Standard Modulus

Standard modulus carbon fiber segment had the highest market share of 45.12% in 2025, as the carbon fiber offered balanced tensile strength properties at an optimal cost. This specific type of carbon fiber has high modulus, which enables the manufacturing of products on a large scale.

-

Intermediate Modulus

The intermediate modulus carbon fiber market is expected to grow at a faster rate compared to other carbon fibers during the forecast period, as a result of an increasing number of applications, especially in the aerospace industry and pressure vessels. This type of carbon fiber has higher rigidity compared to standard carbon fibers but has higher tensile strength compared to standard carbon fibers.

-

High Modulus

The high modulus carbon fiber segment deals with the use where the highest stiffness with less deformation is required. The use of these fibers has remained niche in the field of space & satellites and special equipment. The reason for the limited use is largely attributed due to its associated cost.

Modulus-to-Application Mapping

| Modulus Type | Why This Modulus Exists | Key Applications | Buyer Relevance |

| Standard Modulus Carbon Fiber | Optimized for balanced strength, cost, and processability | Automotive components, industrial parts, sports equipment | Suitable for high-volume applications where cost control and durability matter |

| Intermediate Modulus Carbon Fiber | Designed to increase stiffness without losing tensile strength | Aerospace structures, wind turbine spar caps, pressure vessels | Supports weight reduction with higher structural stability |

| High Modulus Carbon Fiber | Engineered for maximum stiffness and minimal deformation | Satellites, space structures, precision sporting goods | Used where stiffness outweighs cost and tensile strength needs |

Source: Polaris Market Research Analysis

By Application

-

Composites

Composites led the segment in 2025 owing to their extensive usage as a structure in the aerospace industry, automobiles, and industrial wind energy. Carbon fiber composites are known to provide weight reduction, strength, and flexibility to the load-bearing component.

-

Non-composites

Non-composites is growing steadily at CAGR of 7.3%, as it caters to niche PAN-based fiber applications of carbon fiber used in textiles, insulation, and friction materials. Most of these uses depend on the thermal stability, electrical conductivity, and resistance to wear rather than their structural strength. The low volumes of demand and specialized functionalities restrict this segment to small industrial and specialty markets.

By End-Use Industry

-

Aerospace & Defense

Aerospace & defense segment dominated the market in 2025 with 32.23% share, with a huge demand in the aerospace carbon fiber market for high-strength and lightweight material. PAN-based carbon fibers are more desirable due to their superior tensile strength, damage tolerance, and consistency in quality. Primary structures of aircraft, military platforms, and space components use these properties to meet strict standards of safety and performance.

-

Wind Energy

The wind energy segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the growing adoption of wind turbine carbon fiber in increasing larger blade designs. PAN-based carbon fiber exhibits high fatigue resistance and stiffness with lower weight compared to glass fiber. These factors enable support for longer blades and more energy output in both onshore and offshore installations.

-

Automotive & EVs

The automotive and EV markets are rapidly developing their use of automotive carbon fiber composites. The lightweight design of PAN-based carbon fiber allows for more miles per charge as well as an increased range of electric vehicles. At present, it is mainly used in premium vehicles or in high-performance applications owing to its high cost.

-

Pressure Vessels & Hydrogen Storage

Pressure vessels & hydrogen storage is an emerging segment that is gaining pace due to the growing use of hydrogen mobility and energy storage solutions. Carbon fiber produced from the PAN precursor used in hydrogen pressure vessels is known for its strength/weight ratio and pressure containment ability. The sports & leisure market is another mature segment where PAN-based carbon fiber is used in high-performance sports equipment.

-

Sports & Leisure

The sports and leisure category is a steady demand segment for PAN-based carbon fiber. This segment is driven by performance-oriented products. The preference for PAN-based carbon fiber is driven by its strength-weight ratio, damping properties, and durability. These properties enable the use of carbon fiber in sports goods like bicycles, rackets, golf shafts, fishing rods, and protection gear.

Source: Polaris Market Research Analysis

Regional Analysis

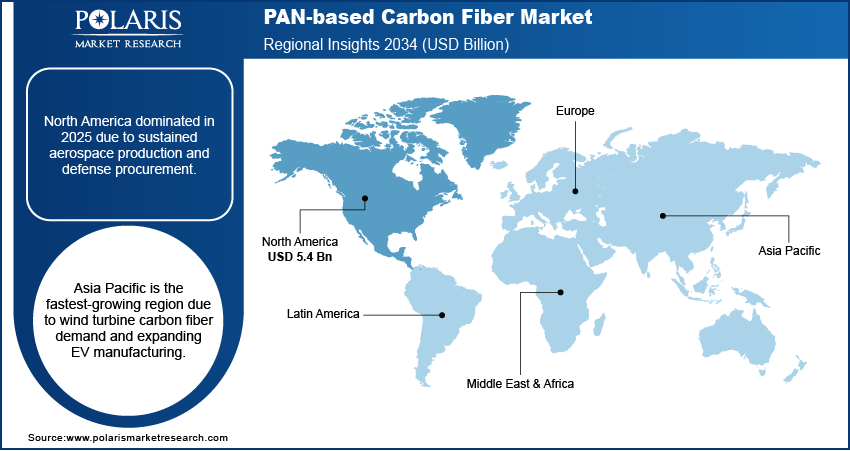

North America Market Assessment

North America dominates the market with 37.10% share due to strong aerospace carbon fiber market demand supported by large aircraft manufacturing programs. Moreover, high adoption of automotive carbon fiber composites across EV platforms supports lightweighting strategies.

The U.S. PAN-based Carbon Fiber Market Insight

The U.S. dominated the North America PAN-based carbon fiber market owing to the consumption of aerospace-grade carbon fiber products. In addition, the rising demand for hydrogen pressure vessels containing carbon fiber drives the development of clean energy infrastructure. The U.S., for instance, saw the launch of a recycled milled carbon fiber product by Carbon Fiber Recycling, which has a reduction of CO₂ emissions of more than 99% compared to the original carbon fiber product in November 2025.

Asia Pacific PAN-based Carbon Fiber Market Insights

Asia Pacific is the fastest-growing region with 8.1% CAGR driven by rapid expansion of wind turbine carbon fiber usage across large-scale renewable projects. Moreover, rising EV production increases demand for automotive carbon fiber composites to improve efficiency.

China PAN-based Carbon Fiber Market Overview

China led Asia Pacific market due to large-scale wind turbine carbon fiber adoption across onshore and offshore installations. In December 2025, China launched a T1000 carbon fiber production base led by Huayang Carbon, formed by Huayang New Material Technology Group, the Datong city government, and the Chinese Academy of Sciences. Furthermore, the growing capacity of electric vehicles will add to the demand for carbon fiber composites used in the automotive industry.

Europe PAN-based Carbon Fiber Market Overview

Europe holds a significant share due to the continued demand for carbon fibers in wind turbine construction in this region. In addition, there is significant encouragement from governments regarding reduced emissions in transportation, leading to automotive use.

Supply Chain and PAN Precursor Dependency Context

| Supply Chain Element | Role in Market | Commercial Impact |

| PAN Precursor Production | Primary raw material source for PAN-based carbon fiber | Capacity availability directly influences fiber pricing and supply security |

| Vertical Integration | Control over precursor and fiber conversion | Improves cost stability and delivery reliability |

| Energy Inputs | High-temperature stabilization and carbonization | Drives carbon fiber production cost and regional competitiveness |

| Geographic Concentration | Limited number of large-scale producers | Creates supply sensitivity for aerospace and wind energy OEMs |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The market for PAN-based carbon fiber is moderately concentrated, and the major players in the market have large capacities. Carbon fiber market participants such as Toray carbon fiber, Teijin carbon fiber, and Hexcel carbon fiber are engaged in activities such as expanding capacities, integrating with the PAN precursor, and long-term alignment with the aerospace, wind industry, or automotive consumer. Sustainability activities and recycling are increasingly impacting the competitive landscape.

The major players engaged in the PAN-based Carbon Fiber industry are Toray Industries, Inc.; Teijin Limited; Mitsubishi Chemical Carbon Fiber & Composites (MCC); Hexcel Corporation; SGL Carbon SE; Aksa Carbon; Hyosung Advanced Materials; Zhongfu Shenying Carbon Fiber Co., Ltd.; Jilin Chemical Fiber Group Co., LTD.; Jiangsu Hengshen Co., Ltd.; Taekwang Industrial; Formosa Plastics; UMATEX ROSATOM; and Shanxi Coal Group Carbon Fiber Division; among others.

Sustainability and Recycled Carbon Fiber Positioning

| Sustainability Aspect | Current Status | Market Implication |

| Sustainability Aspect | Current Status | Market Implication |

| Recycled Carbon Fiber | Growing adoption in non-structural and semi-structural uses | Reduces material cost and supports circular economy goals |

| Bio-based PAN Precursors | Early-stage development | Long-term potential to lower environmental footprint |

| Energy Efficiency Initiatives | Focus on lower-emission processing | Improves ESG alignment for aerospace and automotive customers |

Source: Polaris Market Research Analysis

Key Players

- Aksa Carbon

- Formosa Plastics

- Hexcel Corporation

- Hyosung Advanced Materials

- Jiangsu Hengshen Co., Ltd.

- Jilin Chemical Fiber Group Co., LTD.

- Mitsubishi Chemical Carbon Fiber & Composites (MCC)

- SGL Carbon SE

- Shanxi Coal Group Carbon Fiber Division

- Taekwang Industrial

- Teijin Limited

- Toray Industries, Inc.

- UMATEX ROSATOM

- Zhongfu Shenying Carbon Fiber Co., Ltd.

Industry Developments

-

March 2026: Toray Carbon Fibers Europe announced the operational startup of its new carbon fiber production facility. The new facility is located at Toray’s plant in South-West France. The company stated that it will produce T300 and high modulus (HM) carbon fibers and boost its capacity from 5,000 to 6,000 tonnes annually. (source: toray-cfe.com)

-

March 2026: Teijin Carbon showcased three new carbon fiber solutions at JEC World 2026 in Paris. According to Teijin, the new solutions are created to translate sustainability goals into scalable and high-performance applications. (source: teijincarbon.com)

PAN-based Carbon Fiber Market Segmentation

By Modulus Type Outlook (Revenue, USD Billion, 2021-2034)

- Standard Modulus

- Intermediate Modulus

- High Modulus

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Composites

- Non-composites

By End-Use Industry Outlook (Revenue, USD Billion, 2021-2034)

- Aerospace & Defense

- Wind Energy

- Automotive & EVs

- Pressure Vessels & Hydrogen Storage

- Sports & Leisure

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

PAN-based Carbon Fiber Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 4.04 Billion |

| Market Size in 2026 | USD 4.50 Billion |

| Revenue Forecast by 2034 | USD 10.65 Billion |

| CAGR | 11.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

PAN based Carbon Fiber Market FAQ's

The global market size was valued at USD 4.04 billion in 2025 and is projected to grow to USD 10.65 billion by 2034.

North America dominates with 37.10% share due to strong aerospace carbon fiber market demand and early adoption across EV lightweight materials.

Key applications include aerospace & defense, wind energy, automotive & EVs, pressure vessels, and sports & leisure.

A few of the key players in the market are Toray Industries, Inc., Teijin Limited, Mitsubishi Chemical Carbon Fiber & Composites (MCC), Hexcel Corporation, SGL Carbon SE, Aksa Carbon, Hyosung Advanced Materials, Zhongfu Shenying Carbon Fiber Co., Ltd., Jilin Chemical Fiber Group Co., LTD., Jiangsu Hengshen Co., Ltd., Taekwang Industrial, Formosa Plastics, UMATEX ROSATOM, and Shanxi Coal Group Carbon Fiber Division.

Growth is driven by lightweighting requirements, expansion of wind energy carbon fiber usage, and rising hydrogen infrastructure development.

Download Sample Report of PAN based Carbon Fiber Market

Please fill out the form to request a customized copy of the research report.