Military Simulation And Virtual Training Market Size, & Trend Analysis Report, 2026-2034

REPORT DETAILS

Military Simulation And Virtual Training Market Summary

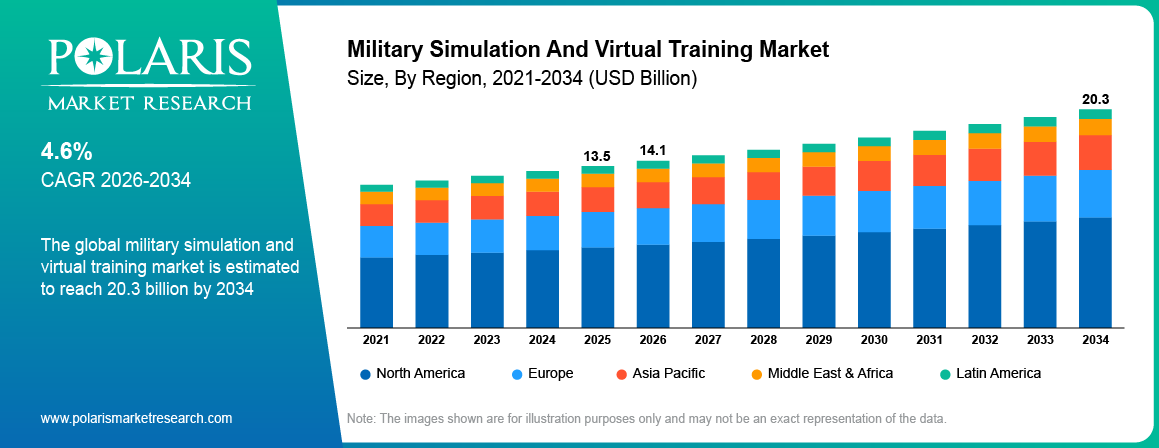

The global military simulation and virtual training market is estimated around USD 13.5 Billion in 2025,?with consistent growth anticipated during 2026–2034. This growth is driven by increasing defense modernization programs, rising demand for cost-effective military readiness solutions, and growing adoption of immersive synthetic training environments. The market is projected to grow at a CAGR of 4.6% during the forecast period.

Market Statistics

Key Takeaways

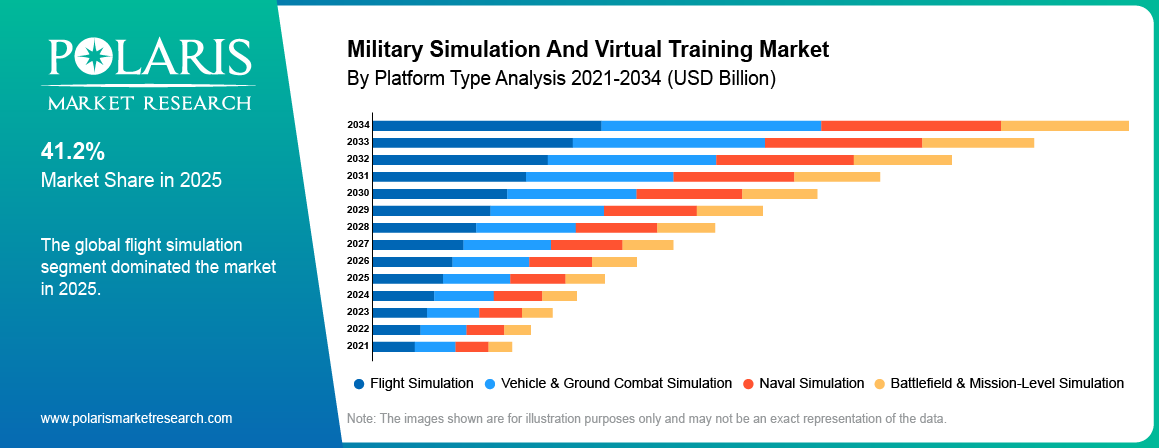

- Flight simulation segment dominated the market by 41.2% share in 2025 due to increasing pilot readiness requirements and rising aircraft modernization programs.

- Air application segment dominated the market by 48.5% share in 2025 owing to growing investments in combat aviation training systems.

- Live-virtual-constructive training segment is projected to grow at the fastest CAGR of 5.1% during the forecast period due to increasing demand for connected battlefield training environments.

- North America dominated the market by holding 42.6% share in 2025 due to high US defense spending and strong military simulation infrastructure.

- Asia Pacific is projected to grow at the fastest CAGR of 5.2% during the forecast period due to rising defense modernization programs.

Industry Dynamics

- Rising demand for cost-effective military readiness solutions supports market expansion.

- Increasing adoption of synthetic battlefield and immersive training platforms drives market growth.

- High simulator integration and procurement costs continue to create deployment challenges.

- Expansion of AI-enabled and XR-based military training systems creates long-term opportunities.

What is Military Simulation And Virtual Training?

Military simulation and virtual training refers to technologies used to recreate battlefield conditions, combat missions, aircraft operations, naval exercises, and tactical training environments through digital systems. These solutions include flight and helicopter simulators, battlefield simulators, vehicle simulators, virtual combat systems, and synthetic training platforms. It is widely used by air force, naval, infantry, and other branches of military organizations in order to improve their readiness and efficiency in operations.

The supply chain contains hardware suppliers, simulation software suppliers, defense contractors, integration providers, training service providers, military organizations, and end-users. Hardware suppliers supply the motion systems, cockpit simulators, screens, and sensors for use in simulations. The simulation software supplier supplies software that creates AI-generated scenarios and terrain data bases.

Source: Polaris Market Research Analysis

Market growth is driven by higher defense spending, improvements in military equipment, and enhanced focus on combat readiness. Simulated training has become increasingly popular among militaries to reduce costs associated with real-time training and maintain mission readiness. Growing investments in AI-enabled battlefield simulations and distributed mission training are anticipated to drive market growth in the future.

Drivers & Opportunities

Rising Demand for Cost-Effective Military Readiness: Simulation technologies are increasingly used in defense systems to help cut training costs as well as enhance preparedness for combat. The use of live military operations is associated with significant costs of fuel, ammunition, and maintenance. Virtual simulation systems enable military forces to conduct repetitive mission training without compromising expensive defense systems. Growing military modernization programs is expected to continue driving the need for virtual training systems. SIPRI revealed that military spending globally rose by 2.9% in real terms to USD 2.88 trillion in 2025, marking a 41% rise from the 2016-2025 period.[Stockholm International Peace Research Institute, ‘Trends in World Military Expenditure 2025’, sipri.org]

Increasing Adoption of Synthetic Training Environments: The armed forces have become more and more keen on leveraging the synthetic environment that is connected to enable them to operate in multi-domain environments. In February 2026, Vantor was awarded a contract worth up to USD 217 million for its globally immersive 3D terrain products, which are used in training and mission rehearsals by the U.S. Army under the One World Terrain program. Such technologies are helping soldiers rehearse missions involving urban combat, drones, cyber war, and electronic warfare.

Restraints & Challenges

High Integration and Procurement Costs: The usage of military simulation technologies requires significant capital investment in terms of hardware, software, networking, and installation. Higher costs are associated with implementing technologies such as motion simulators, cockpit simulators, visualization systems, and secure networks. It is hard for defense agencies with tight budget restrictions to implement such complicated systems.

Opportunity

Expansion of AI-Enabled Military Training Systems: The AI technology is leading to innovations in terms of military simulation technologies and military training technologies. AI technology offers more advanced ways of scenarios creation, battlefield assessment, enemy behavior intelligence, and post-assessment. In June 2025, EON Reality developed an EON Spatial AI Military Academy for delivering immersive training on artificial intelligence and virtual reality in future battlefields.[EON Reality, ‘EON Reality Unveils EON Spatial AI Military Academy’, eonreality.com] Rising investments in next-generation synthetic training ecosystems continue to create market opportunities.

Source: Polaris Market Research Analysis

Segmental Insights

The report provides a comprehensive analysis of the military simulation and virtual training market by platform type, application, training type, and component to pinpoint the key revenue generating and growth segments.

By Platform Type

-

Flight Simulation

Flight simulation segment dominated the market by 41.2% share in 2025 due to increasing pilot training requirements and rising combat aircraft modernization programs. Modern military aircraft require extensive mission rehearsal and emergency handling training before live deployment. Defense organizations continue investing in advanced flight simulators to improve combat readiness and reduce live aircraft operating costs.

-

Battlefield and Mission-Level Simulation

Battlefield and mission-level simulation segment is projected to grow at the fastest CAGR of 5.1% during the forecast period due to increasing focus on joint-force operations and multi-domain warfare training. These systems support command-level exercises, logistics coordination, and war-gaming activities. Rising adoption of connected synthetic battlefield environments continues to support segment growth.

By Application

-

Air

Air application segment dominated the market by 48.5% share in 2025 owing to increasing procurement of fighter aircraft, helicopters, and unmanned aerial vehicles across major defense economies. Air forces continue investing in pilot readiness, mission rehearsal, and combat simulation systems. Growing demand for advanced aviation training infrastructure supports segment dominance.

-

Ground

Ground application segment is projected to grow at the fastest CAGR of 5.0% during the forecast period due to increasing investments in infantry modernization and armored vehicle training systems. Military organizations are adopting simulation systems for urban warfare, convoy operations, and tactical mission planning. Rising focus on battlefield preparedness continues to support market growth.

By Training Type

-

Virtual Training

Virtual training segment dominated the market in 2025 by 43.7% of revenue share due to increasing adoption of VR-based and simulator-based military training platforms. These systems are widely used for weapons handling, procedural training, and combat mission rehearsal. Defense organizations continue investing in immersive training environments to improve personnel readiness.

-

Live-Virtual-Constructive Training

Live-virtual-constructive training segment is projected to grow at the fastest CAGR of 5.1% during the forecast period due to increasing demand for integrated battlefield training ecosystems. LVC systems connect live soldiers, virtual simulators, and computer-generated forces within a common training environment. Rising coalition exercises and distributed mission operations continue to support segment growth.

By Component

-

Hardware

Hardware segment dominated the market in 2025 by 47.6% share owing to increasing deployment of motion systems, simulator cabins, immersive displays, and haptic devices across military training centers. High-fidelity hardware remains important for aircraft, naval, and vehicle simulation platforms. Rising procurement of advanced simulator infrastructure continues to support market demand.

-

Software

Software segment is projected to grow at the fastest CAGR of 5.1% during the forecast period due to increasing adoption of AI-based scenario generation, terrain modeling, and simulation analytics platforms. Software-defined simulation systems improve interoperability and training flexibility. Growing investments in synthetic environment software continue to support segment expansion.

Source: Polaris Market Research Analysis

Regional Analysis

North America Military Simulation And Virtual Training Market Overview

North America dominated the market by holding 42.6% share in 2025 due to high defense expenditure and strong presence of military technology providers across the US and Canada. In December 2025, Thales Group improved the preparedness of soldiers by implementing drones in live combat simulation programs.[Thales Group, ‘Thales Enhances Armed Forces Readiness by Integrating Drones into Live Training’, thalesgroup.com] Rising modernization of combat aircraft, armored vehicles, and naval fleets continues to support regional market growth.

Asia Pacific Military Simulation And Virtual Training Market Insights

Asia Pacific is projected to grow at the fastest CAGR of 5.2% during the forecast period due to rising defense modernization programs across China, India, Japan, South Korea, and Australia. In May 2025, Xi’an Technological University unveiled a DeepSeek-based simulated military scenario generator designed to enhance AI-driven combat training and battlefield simulation capabilities for the PLA. Regional governments are increasing investments in military readiness, air force expansion, and naval security infrastructure.

Europe Market Insights

Europe held a substantial market share in 2025 owing to increasing NATO defense spending and rising military preparedness programs across Germany, France, the UK, and Italy. Countries in the region are investing in air defense training, armored vehicle simulation, and coalition military exercises. For instance, in December 2025, Airbus was selected by the Spanish Ministry of Defence to lead Spain’s new Integrated Combat Training System aimed at modernizing fighter pilot training and replacing the country’s aging F-5 aircraft fleet.

Middle East & Africa Market Insights

Middle East & Africa is witnessing steady growth due to rising investments in air force modernization, border security, and command-and-control training systems. Countries in the Gulf region are increasingly adopting pilot training simulators and battlefield simulation technologies. For instance, in April 2026, the UAE announced the world’s first commercial military rescue training center, featuring advanced helicopter and maritime simulation systems for high-risk defense and emergency response training.

Latin America Market Insights

Latin America is experiencing moderate growth due to increasing focus on border control, naval patrol training, and disaster response preparedness. Virtual military training is increasingly becoming an option for the countries in this region as it helps in reducing cost and increasing preparedness. According to the plans of the Ejército de Chile in May 2026, it helps to adopt the VR-Forces system, which helps to facilitate military exercises through constructive simulations.

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

Military simulation and virtual training market exhibits moderate fragmentation as there are global defense contractors, simulation technology vendors, and training systems integration companies competing. Major competitive parameters involve simulation fidelity, inter-operability, AI incorporation, product development, and lifecycle services. Firms are striving for alliances, defense deals, acquisitions, and synthetic training systems growth.

Some of the major firms operating in the market include BAE Systems plc, Boeing, CAE Inc., Collins Aerospace, Cubic Corporation, Elbit Systems Ltd., L3Harris Technologies, Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, Saab AB, Thales Group, and others.

Premium Insights

Expansion of Mission-Level Training Ecosystems

Military defense organizations are embracing technology-based ecosystems where the various forms of air, land, sea, cyber, and space warfare helps to integrate into the same simulation environment. There is increasing demand for solutions that have an open architecture, AI-based enemy forces, and battlefield integration capabilities.

Growing Role of AI in Military Simulation

Artificial intelligence is expected to contribute to the field of military simulations by enhancing the ability to automatically generate scenarios, creating adaptive learning environments, and analyzing the results of the training process.

Rising Demand for Advanced Synthetic Training Platforms

Growth prospects in the market include flight simulation, LVC training, soldier training using XR technology, UAV simulation, and naval warfare simulation. Defense organizations are also adopting flexible models such as simulation-as-a-service and managed training centers.

Key Players

- BAE Systems plc

- Boeing

- CAE Inc.

- Collins Aerospace

- Cubic Corporation

- Elbit Systems Ltd.

- L3Harris Technologies

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- Saab AB

- Thales Group

Industry Developments

- March 2026: The Danish Army selected BAE Systems’ OneARC platform to modernize its enterprise simulation infrastructure and strengthen interoperable military training capabilities across defense operations. [source: baesystems.com]

- December 2025: Varjo released its State of XR in Simulation Training Report, highlighting the shift of XR adoption from pilot testing to realistic multi-user defense and simulation training environments. [source: varjo.com]

Military Simulation And Virtual Training Market Segmentation

By Platform Type Outlook (Revenue, USD Billion, 2021-2034)

- Flight Simulation

- Vehicle & Ground Combat Simulation

- Naval Simulation

- Battlefield & Mission-Level Simulation

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Air

- Ground

- Naval

By Training Type Outlook (Revenue, USD Billion, 2021-2034)

- Virtual Training

- Constructive Training

- Live-Virtual-Constructive Training

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Hardware

- Software

- Services

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Military Simulation And Virtual Training Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 13.5 Billion |

| Market Size in 2026 | USD 14.1 Billion |

| Revenue Forecast by 2034 | USD 20.3 Billion |

| CAGR | 4.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Military Simulation And Virtual Training Market FAQ's

The global market size was valued at USD 13.5 Billion in 2025 and is projected to grow to USD 20.3 Billion by 2034.

North America dominated the market by holding 42.6% share in 2025 owing to high defense expenditure and excellent military training facilities.

Major applications include air, ground, and naval military training operations.

A few of the key players in the market are BAE Systems plc, Boeing, CAE Inc., Collins Aerospace, Cubic Corporation, Elbit Systems Ltd., L3Harris Technologies, Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, Saab AB, Thales Group, and others.

Market growth is driven by rising defense modernization programs and increasing demand for cost-effective military readiness solutions.

Flight simulation segment dominated the market by 41.2% share in 2025 due to increasing pilot training and combat mission rehearsal requirements.

Military simulation based on AI, synthetic battlefield simulation, and military training with XR technologies are expected to be the key drivers of growth.

Download Sample Report of Military Simulation And Virtual Training Market

Please fill out the form to request a customized copy of the research report.