Procurement Software Market Size, Share, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Procurement Software Market Summary

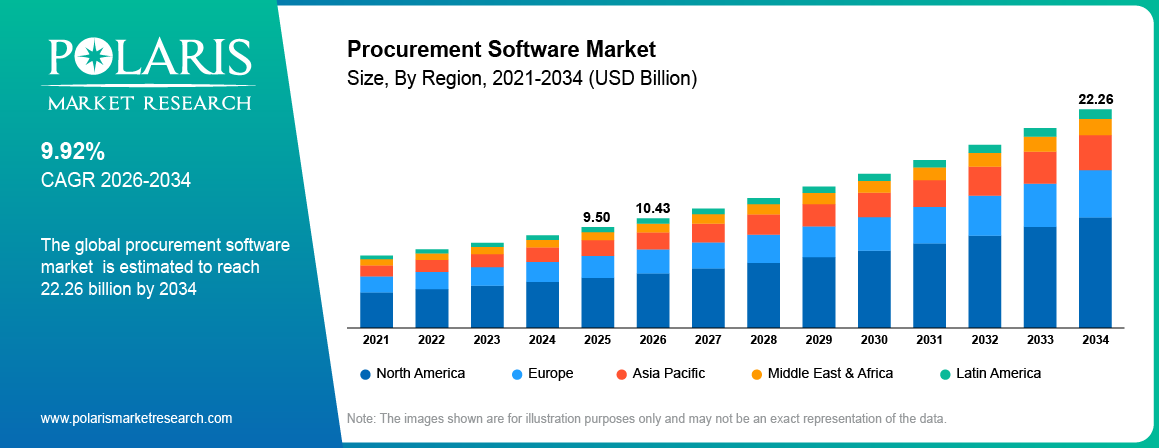

The global procurement software market is estimated around USD 9.50 Billion in 2025,?with consistent growth anticipated during 2026–2034. Expansion is driven by increasing adoption of AI-powered procurement platforms, rapid shift toward cloud-based systems, and growing need for real-time spend visibility and supplier management. The market is projected to grow at a CAGR of 9.92% during the forecast period.

Market Statistics

Key Takeaways

- North American procurement software market led the market in 2025, accounting for approximately 40.20% market share due to advanced digital adoption and strong enterprise presence.

- Europe had the second largest market share, holding approximately 28.75% due to increasing automation and regulatory compliance requirements.

- Large enterprises accounted for the highest market share, contributing approximately 42.10% due to high procurement volumes and need for integrated solutions.

- SMEs are the fastest-growing category, projected to register a CAGR of approximately 13.85% driven by increasing adoption of cloud-based procurement tools.

- In 2025, retail & e-commerce emerged as the leading vertical, accounting for approximately 36.55% market share due to high transaction volumes and supply chain complexity.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

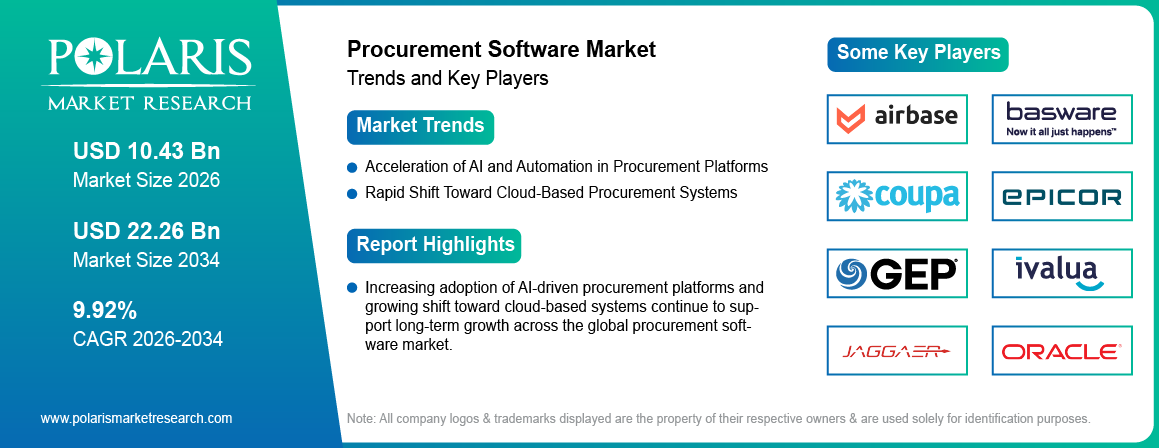

- Acceleration of generative AI in procurement platforms is increasing automation in sourcing, supplier discovery, and workflow orchestration.

- Rapid shift toward cloud-native procurement systems is strengthening demand for scalable and integrated platforms.

- Supply chain complexity and ESG compliance requirements are increasing system integration challenges.

- Embedded finance and payment innovation are opening new opportunities in procurement ecosystems.

What is the Procurement Software Market?

The Procurement Software Market refers to the global industry focused on digital solutions that automate and manage an organization’s purchasing processes—from supplier sourcing and contract management to purchase orders, invoicing, and spend analysis. Procurement software helps businesses streamline procurement workflows, reduce manual errors, ensure compliance, and gain real-time visibility into spending. These platforms often integrate with enterprise systems such as ERP and finance tools, enabling efficient vendor management and data-driven decision-making. The market is driven by increasing demand for cost optimization, process automation, and transparency across supply chains. Cloud-based procurement solutions, AI-driven analytics, and e-procurement platforms are key trends shaping the market, helping organizations improve operational efficiency and strategic sourcing capabilities across industries.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Drivers & Opportunities

Acceleration of Generative AI in Procurement Platforms: The enterprise procurement process has transitioned from rule-based automated tools to agentic artificial intelligence (AI) systems performing the tasks of sourcing, supplier discovery, and workflow management. This transformation leads to lower manual interventions, shorter cycle times, and greater sourcing accuracy. In November 2025, Coupa launched its Navi AI agents on its source-to-pay solution suite, thereby allowing autonomous sourcing and collaboration with suppliers using predictive analytics and natural language processing.

Cloud Adoption in Government Systems Accelerating Procurement Digitization: Increase in cloud infrastructure deployment is changing the procurement process from on-premises systems to scalable cloud systems. In line with the E-Government Survey by UNDESA 2024, 44% of the countries employ cloud computing within their public sector services.Procurement software running on the cloud provides spend transparency, lowers costs of service delivery, and facilitates real-time analytics. Small and medium-sized companies will join through freemium procurement solutions SaaS, while large organizations will integrate procurement processes with cloud ERP systems like SAP S/4HANA and Oracle Fusion Procurement Cloud. The shift is growing up digital transformation in procurement and increasing the total addressable market.

Restraints & Challenges

Supply Chain Complexity and ESG Compliance Mandates: Global supply chains comprise multi-level suppliers, fragmented regulations, and increasing ESG disclosure obligations. Procurement teams must track supplier emissions, ethical sourcing, and compliance within workflows, which increases system complexity. Integration of ESG metrics into procurement platforms requires data standardization and supplier transparency, creating operational challenges and slowing implementation timelines.

Opportunity

Embedded Supply Chain Finance and Payment Innovation: The combination of finance and payment solutions on procurement platforms is boosting the liquidity of suppliers while building better relationships between buyers and suppliers through embedded finance that allows early payments, dynamic discounting, and working capital management, adding new value layers to procurement platforms.

Source: Polaris Market Research Analysis

Segmental Insights

This study provides thorough insights into the procurement software market segmented on the basis of deployment model, software module, organization size, and end-user vertical to help readers identify the fastest expanding and most attractive demand segments.

By Deployment

-

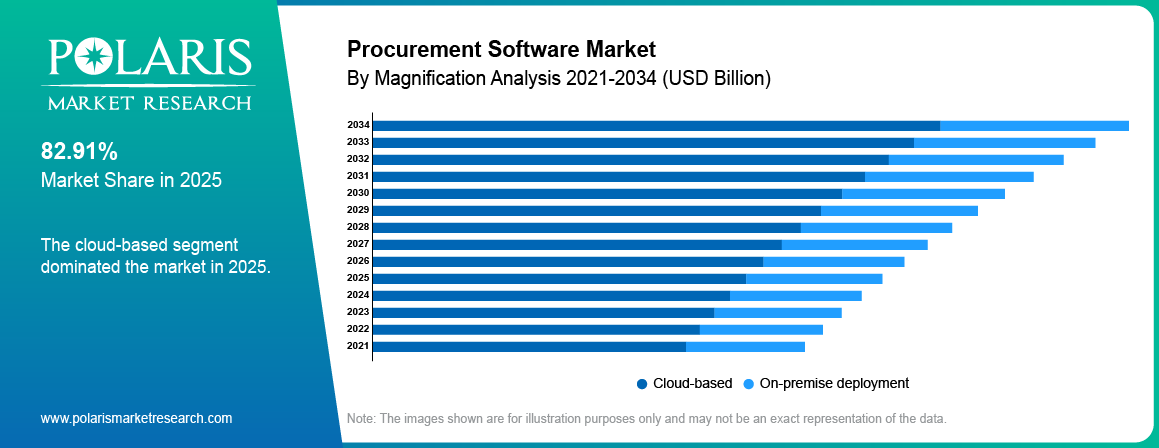

Cloud-based

In 2025, cloud procurement software accounted for a substantial market share, mainly attributed to the rising use of cloud procurement platforms and reduced total cost of ownership. With cloud deployment, companies benefit from timely collaboration and easy scalability. Shielded SaaS procurement software, which is suitable for the BFSI industry and governments for e-procurement software, is gaining rapid adoption.

-

Hybrid

The hybrid deployment category is experiencing rapid growth as companies are moving from traditional solutions. The hybrid deployment approach for procurement enables the company to keep its critical information behind the firewall while using cloud capabilities for analysis and collaboration with suppliers.

Cloud vs On-Premise Comparison

| Factor | Cloud Procurement Software | On-Premise Procurement Software |

| Pros | Scalable, low upfront cost, real-time updates | High data control, customization |

| Cons | Data residency concerns in some sectors | High TCO, slow upgrades (6–12 months) |

| Best For | SMEs, distributed enterprises, SaaS-first orgs | Highly regulated, legacy-heavy orgs |

Source: Polaris Market Research Analysis

By Software Module

| Module | 2026 Market Share / Growth | Key Use Case | AI Impact |

| Procure-to-Pay (P2P) | Dominant | End-to-end workflow: requisition, PO, invoicing, payment | Automation of invoice matching and approvals |

| Contract Lifecycle Management (CLM) | Fastest-growing | Contract creation, compliance, renewal tracking | AI-driven contract analytics and risk detection |

| Spend Analysis | High adoption | Cost visibility, supplier spend tracking | AI-led insights and predictive savings |

| E-Sourcing | Rapid adoption | RFP/RFQ automation | 42.33% using GenAI for sourcing optimization |

| Supplier Management | Growing steadily | Risk scoring, ESG evaluation | Real-time supplier intelligence |

Source: Polaris Market Research Analysis

By Organization Size

-

Large enterprises

Large enterprises accounted for the highest market share due to their more complicated procurement requirements, including bill of material management, multilevel supplier relationship management, and compliance considerations. Big enterprise procurement software emphasizes integration, visibility, and optimized global sourcing.

-

SME

SMEs are the fastest-growing category due to increasing SaaS procurement software adoption. SME procurement software market growth is facilitated by freemium pricing, modular applications, and embedded financial capability, which converts capital expenditure to operational expenditure.

By End-User Vertical

-

Retail & e-commerce

In 2025, retail & e-commerce emerged as the verticals leading the market due to their high volumes of procurements, the number of SKUs, and constant need for cost optimization. E-commerce procurement systems in retail provide real-time coordination of suppliers and inventory management that influences margins directly.

-

Healthcare

The healthcare industry represents the highest growth vertical due to cost-cutting measures associated with the value-based reimbursement model. More healthcare organizations implement procurement management software as every percent of supply cost saving directly contributes to their bottom line.

Premium Insights:

Manufacturing procurement systems are built based on the complexity of the bill of materials and just-in-time inventory techniques. The procurement software adopted by the BFSI industry is compliance and vendor-centric. Procurement software adopted by the IT/Telecom industry is primarily subscription and cloud spend management-oriented.

Source: Polaris Market Research Analysis

Regional Analysis

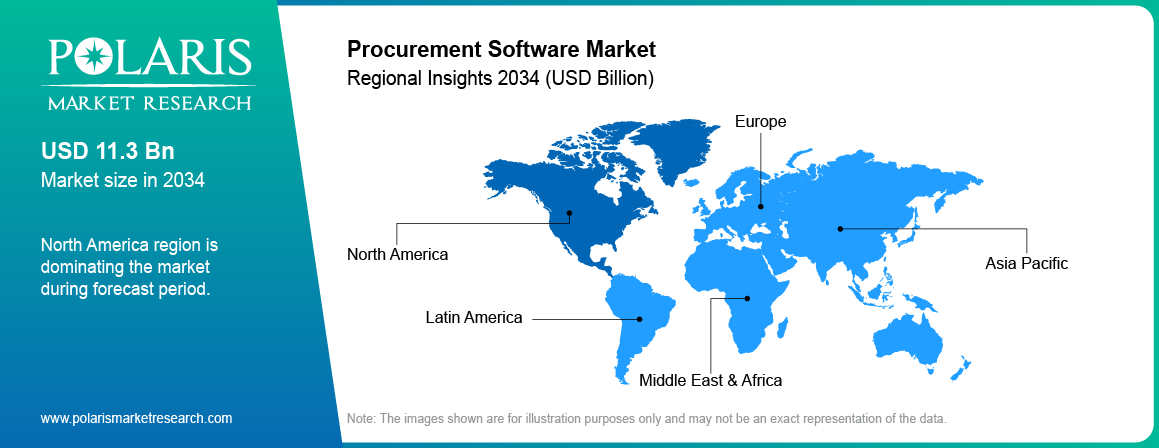

North America Procurement Software Market Assessment

The North American procurement software market led the market in 2025. This is primarily propelled by the modernization of public sectors and IT procurement improvements in the US. Digital procurement platforms are implemented for enhancing transparency and efficiency. The enactment of the Infrastructure Investment and Jobs Act (IIJA) in 2021 boosted modernization efforts in the IT system procurement sector.This push is strengthening adoption of government e-procurement solutions and expanding the US procurement software market size.

Asia Pacific Procurement Software Market Insight

Asia Pacific region will register the highest growth rate during the forecast period. This is owing to wide-scale adoption of cloud-based procurement solutions by organizations and digitally supported initiatives from the government. The transition to cloud-native technologies allows organizations to automate processes and make decisions instantly. In January 2026, Zoho released a cloud-based ERP platform, which uses AI technology and integrates procurement with finance and supply chain operations in India. There is also a significant adoption of cloud procurement platforms in China which in turn thrives the market growth in this region.

Europe Procurement Software Market Overview

Europe had the second largest market share in the base year, due to stringent compliance mandates such as the GDPR and EU AI Act. Organizations are implementing procurement software systems that are centered around data protection, auditability, and artificial intelligence regulation. Procurement technology adoption is increasing in regions such as the UK and Germany owing to compliance considerations. There is a shortage of talent in procurement and digital capabilities that will impact adoption. The above-mentioned trends will boost adoption in the region.

Middle East, Africa & Latin America Procurement Software Market Assessment

Middle East procurement software market is expanding through government digitization programs such as Saudi Arabia Vision 2030 and UAE Smart Government initiatives.These programs are increasing adoption of e-procurement systems across public sectors. Latin America e-procurement adoption is growing with gradual digital transformation and regulatory improvements. Increasing transparency and efficiency is fueling the procurement software market in emerging economies.

Source: Polaris Market Research Analysis

Competitive Landscape

Key Players & Strategic Developments

The procurement software industry is moderately concentrated with growing consolidation trends fueled by expensive mergers & acquisitions, as well as platform extension. For example, Oracle Corporation acquired Determine to expand its ERP software portfolio, and Coupa Software Incorporated focused on investing in the development of autonomous procurement agents. Workday, Inc., for its part, extended its business into embedded supply chain finance. This implies the adoption of artificial intelligence-powered automation and platformization among procurement software providers in 2026.

Major companies operating in the market include Airbase Inc., Basware Corporation, Coupa Software Incorporated, Epicor Software Corporation, GEP Worldwide, Ivalua Inc., Jaggaer LLC, Oracle Corporation, Precoro Inc., Proactis Holdings PLC, Procurify Inc., SAP SE, Tipalti Inc., Workday, Inc., Zycus Inc.

Buyer’s Guide: Evaluating & Selecting Procurement Software

criteria for evaluating procurement software

- Deployment model & scalability- When evaluating procurement software, you should assess whether cloud SaaS, on-premise, or hybrid deployment fits your IT strategy.

- AI & automation capabilities- When evaluating procurement software evaluation criteria, your team should examine AI depth beyond basic automation. Search for generative AI co-pilots, agentic workflows, and machine learning-based spend categorization, in addition to gauging the provider's innovative trajectory.

- ERP & ecosystem integration depth- In considering integration capabilities, it is important to weigh solutions that feature advanced API architecture and connectivity to applications like SAP S/4HANA, Oracle Fusion, or Workday.

- Compliance & data sovereignty- When evaluating procurement software compliance features, your team should verify certifications such as GDPR, SOC 2, and ISO 27001.

- Total cost of ownership (TCO) vs. ROI timeline- In calculating the total cost of ownership for procurement solutions, one must balance license fees, deployment expenses, and change management considerations against anticipated savings.

Common implementation challenges

Procurement software implementation requires careful consideration of potential operational obstacles and corresponding mitigation efforts.

- Skills gap regarding technology still continues to be an issue, where many organizations do not have skilled personnel in their procurement technology.

- Change management becomes difficult as there are delays between procurement maturity and other departments within an organization.

- Some integration issues to consider include ERP data migration and master data synchronization.

- Stakeholder agreement becomes crucial due to its benefits that will arise from the implementation may not be direct but may take time.

- It is important to assess vendor lock-in risks in relation to how well an exit strategy can be developed.

ROI expectations & success metrics

The ROI analysis of the procurement software must consider the performance measurement criteria linked to the KPIs at the board level focused on efficiency and cost management.

- Reduced cycle times from sourcing and procurement processes.

- Savings in costs due to AI-powered sourcing and supplier optimization.

- Improved on-contract spend rate.

- Decreased maverick spend by leveraging maverick spend control software feature.

- Decreased cost-to-serve and increasing procurement efficiency.

Key Players

- Airbase Inc.

- Basware Corporation

- Coupa Software Incorporated

- Epicor Software Corporation

- GEP Worldwide

- Ivalua Inc.

- Jaggaer LLC

- Oracle Corporation

- Precoro Inc.

- Proactis Holdings PLC

- Procurify Inc.

- SAP SE

- Tipalti Inc.

- Workday, Inc.

- Zycus Inc.

Industry Developments

- March 2026: GEP launched an AI-driven total orchestration platform to unify procurement and supply chain operations through intelligent automation and real-time decision-making. [source: www.gep.com]

Procurement Software Market Segmentation

By Deployment Model Outlook (Revenue, USD Billion, 2021-2034)

- Cloud-based

- On-premise deployment

By Software Module Outlook (Revenue, USD Billion, 2021-2034)

- Procure-to-pay software (P2P)

- Contract lifecycle management software (CLM)

- Spend analysis software

- E-sourcing software

- Supplier management software

By Organization Size Outlook (Revenue, USD Billion, 2021-2034)

- Large enterprise

- SME

By End-User Vertical Outlook (Revenue, USD Billion, 2021-2034)

- Manufacturing

- Retail & e-commerce

- Healthcare

- BFSI

- IT & Telecom

- Government

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Procurement Software Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 9.50 Billion |

| Market Size in 2026 | USD 10.43 Billion |

| Revenue Forecast by 2034 | USD 22.26 Billion |

| CAGR | 9.92% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Procurement Software Market FAQ's

The global market size was valued at USD 9.50 Billion in 2025 and is projected to grow to USD 22.26 Billion by 2034.

North America dominated the market due to strong enterprise adoption, government digitization initiatives, and advanced IT infrastructure.

The Retail & e-commerce category has the highest share owing to procurement volumes.

A few of the key players in the market are Airbase Inc., Basware Corporation, Coupa Software Incorporated, Epicor Software Corporation, GEP Worldwide, Ivalua Inc., Jaggaer LLC, Oracle Corporation, Precoro Inc., Proactis Holdings PLC, Procurify Inc., SAP SE, Tipalti Inc., Workday, Inc., Zycus Inc.

Factors influencing the growth of the market include increasing AI usage, cloud adoption as well as growing spending and supplier management visibility needs.

Key trends shaping the market include the rise of AI automation, embedded financial capabilities, cloud-first technologies, and integration with enterprise resource planning software.

Agentic AI streamlines sourcing, supplier discovery, and approvals processes.

The ROI stems from lower procurement costs, increasing efficiency, and effective supplier management.

SAP SE (Ariba) concentrates on extensive ERP integration and compliance capabilities, whereas Coupa Software Inc.'s key strengths lie in artificial intelligence and spend management capabilities.

Download Sample Report of Procurement Software Market

Please fill out the form to request a customized copy of the research report.