Silica Market Trends, Forecasts, and Key Players, 2026-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

Silica Market Overview

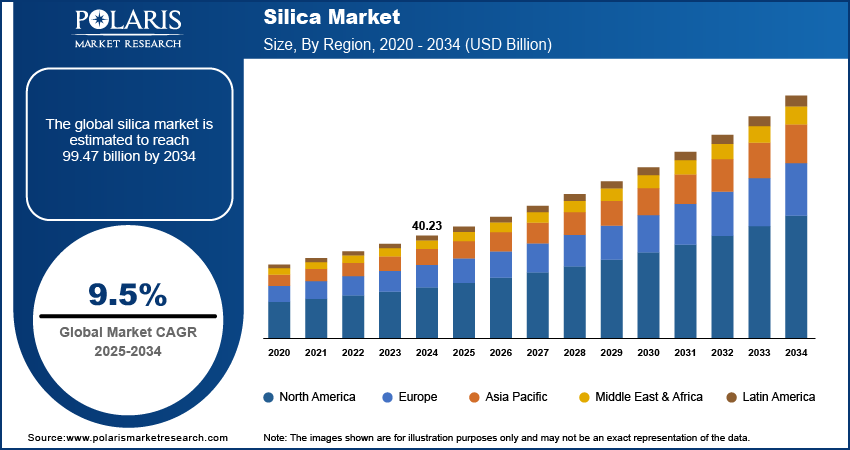

The silica market size was valued at USD 45.66 billion in 2025. The market is projected to account for a CAGR of 7.90% during 2026 to 2034. Rising electronics and semiconductor manufacturing, along with growth in automotive and transportation applications, are boosting market growth.

Key Takeaways

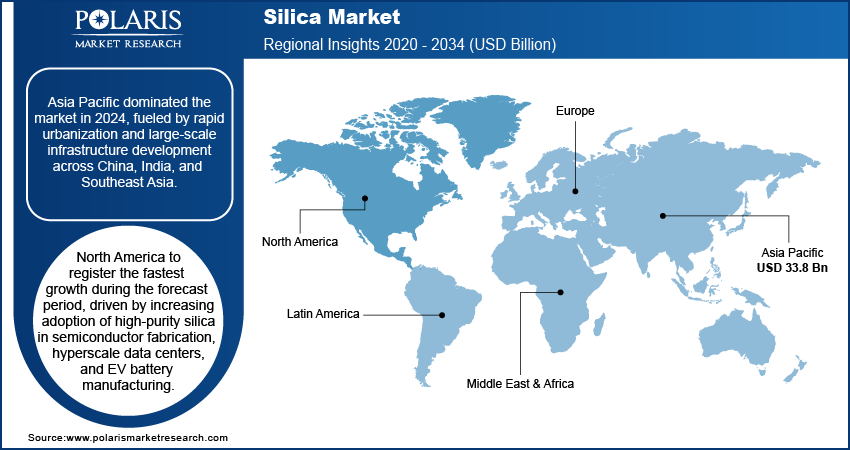

- Asia Pacific accounted for a 46.56% revenue share of the global silica market in 2025 due to faster urbanization and large-scale infrastructure growth throughout China, India, and Southeast Asia.

- China dominated the regional market. It is driven by the robust electronics manufacturing, semiconductor fabs, and solar module production.

- North America is forecast to grow at a 7.6% CAGR during the forecast period. The regional market is led by increasing demand for high-purity silica in semiconductor production, hyperscale data centers, and EV battery production.

- The U.S. led the regional market owing to increasing solar panel installations. This has increased demand for high-grade silica employed in photovoltaic glass and wafer manufacturing.

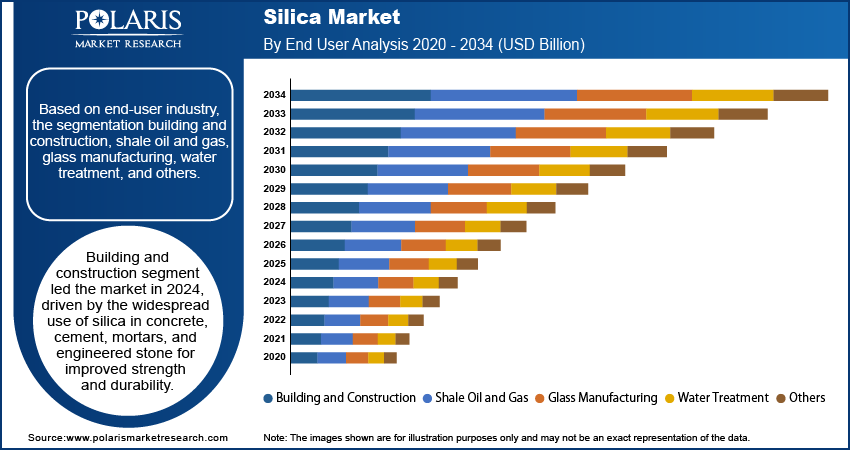

- Amorphous silica is expected to grow at the fastest CAGR of 8.1% during the forecast period. The growing usage of these products in rubber, coatings, adhesives, and food-grade applications has been contributing to the leading position of this market segment.

- The shale oil and gas segment is expected to grow at an 8.00% CAGR. The segment’s growth is supported by the widespread application of silica sand as a proppant material during hydraulic fracturing.

Market Statistics

- 2025 Market Size: USD 45.66 Billion

- 2034 Projected Market Size: USD 89.83 Billion

- CAGR (2026–2034): 7.90%

- Asia Pacific: Largest Market Share in 2025

Industry Dynamics

- Increasing demand from the electronics and semiconductor manufacturing industry is boosting silica consumption.

- Rising automotive and transportation applications are further boosting market growth.

- The market is witnessing increasing demand from AI data centers and chip manufacturing ecosystems.

- There have been rising investments in green silica and bio-based silica production.

- Raw material price volatility hinders market stability and investment planning. Silica mining is under increased scrutiny due to environmental concerns and emissions. It is creating silica market challenges for supply chain stability.

- Ultra-purification technologies and nano-silica innovations offer strong market opportunities. New high-value opportunities are also being created in the silica market due to emerging uses in nanotechnology, biomedical materials, and energy storage.

How Electric Vehicles, Semiconductors, and Green Tires Are Reshaping Silica Demand?

The global silica industry is shifting from its traditional consumption areas, such as building construction and glass production, into emerging sectors tied to technology and sustainability. Electric cars, silicon wafer production, green energy systems, and eco-friendly transportation represent promising markets for silica makers. Consumers are increasingly seeking higher purity, superior product functionality, and sustainable raw material sourcing.

Applications like cement production, casting sand, and fillers remain strong sources of consistent demand. Nonetheless, rapid expansion is now being driven by sectors requiring specialized silica grades. This has encouraged manufacturers to invest in purification technologies and regional supply chain expansion.

Green Tires and Electric Vehicles

The use of green tires and electric cars is expected to be among the major drivers of market growth for silica in the near future. The precipitated silica is applied extensively in tires to decrease the rolling resistance, ensure better grip on wet surfaces, and increase fuel efficiency.

In addition, the demand for the material becomes even higher in the context of electric cars. The cars are heavier due to battery packs, which require tires that are more durable and energy-efficient. In such circumstances, silica-based tires offer a significant advantage to electric car manufacturers, as they can increase driving range.

Furthermore, silica is used in battery components, insulation materials, sealants, and lightweight composites. With the growing trend towards the development of electric cars, the use of silica will expand outside tires to other car components.

Semiconductor Fabrication and Solar Photovoltaics

High-purity silica is growing in relevance to semiconductor manufacturing and solar photovoltaic technology. Silica is used in semiconductor fabrication applications such as wafer fabrication equipment, CMP slurry, insulating agents, quartz parts, and electronics packaging.

The increasing demand for artificial intelligence chips, hardware for cloud computing, memory components, and advanced processors is prompting the expansion of semiconductor fabrication facilities worldwide. This leads to higher demand for extremely pure silica-based materials meeting certain criteria.

Solar power is another important sector where silica finds applications. It is used as a base material for producing photovoltaic glass, silicon wafer production, and various other materials used in solar manufacturing processes. Higher installations of solar panels worldwide are expected to ensure consistent demand for silica.

What this Structural Shift Means for the Broader Silica Market?

The shift towards these trends is transforming the silica industry from a commodity business focused on volumes to a specialty materials industry based on value-added applications.

Companies related to EV tires, semiconductor supply chain management, batteries, and solar power generation are likely to gain better margins. Meanwhile, regional security of supply has become significant as nations produce their semiconductors and clean energy locally. The silica industry is expected to be driven more by innovations and technology-based demand than by its traditional uses.

The silica market includes high-purity silicon dioxide products, which are used in various glass production, electronics, foundry, construction, personal care, and industrial processes. The market is driven by rising specialty glass and semiconductor part usage, growth in the coatings and rubber industries, and the increasing application of high-performance silica in filtration, additives, and reinforcement processes.

With ongoing advancements in silica processing technology, manufacturers are able to produce high-purity specialty-grade silica for use in specialized industrial applications. The processors are also focusing on engineered particle size, surface treatment, and functionalization grades of silica to address performance criteria through advanced formulation. This is leading to an expansion of silica use in new industries.

The rising rate of high-purity silica consumption in semiconductor manufacturing, production of photovoltaic glass, and various components of EV batteries is transforming the global silica value chain. In addition, the use of silica in advanced coatings, specialty chemicals, and green materials is creating new business opportunities for silica manufacturers.

To Understand More About this Research: Download Sample Report

Market Dynamics

Rising Demand from Semiconductor & Electronics Industry

High purity silica is employed in the semiconductor industry for the manufacture of optical fibers and photovoltaic cells for solar energy systems. According to the Semiconductor Industry Association, global semiconductor sales in 2024 were recorded at USD 627.6 billion, showing a growth of 19.1% from 2023. Silica is employed in chip wafers, insulation, and micro-electronics packaging. Silica plays a significant role in AI, cloud computing, and electronics manufacturing. Thus, the increasing use of high purity silica in the semiconductor and electronics industry is creating demand.

Growth in Automotive & EV Applications

The growing automotive industry is propelling increasing silica consumption for application in tires, light-weight composites, and innovative material blends that enable fuel efficiency and performance. As per the European Automobile Manufacturers Association, worldwide auto sales amounted to 74.6 million units during 2024, posting a 2.5% increase compared to the prior year. The rise of electric vehicles is also driving increased demand for silica-based products as separators, thermal insulation agents, and energy-efficient tire products. This factor is contributing to the long-term growth of the silica market.

Pricing Analysis

The cost of silica varies based on several factors. These include the product's purity, area of application, and region. The price of industrial-grade silica is typically between USD 30 and USD 80 per ton. However, for electronic products, silica prices per ton may reach USD 5,000 due to complex processing and quality requirements.

Moreover, prices are influenced by demand as well as energy, transport, and regulatory costs. In the Asia Pacific, for example, prices tend to be lower than in North America and Europe. This is because of the easy availability of raw materials and lower production costs in the Asia Pacific region.

Segmental Insights

Precipitated Silica Market — Size, Growth, and Key Applications

The precipitated silica market is significant in the global silica industry, valued at USD 7.31 billion in 2025. This is owing to its extensive usage in tires, rubber reinforcement, oral hygiene, food processing, and specialty industrial goods. The demand for precipitated silica continues to grow as producers look towards improving their products and finding environmentally friendly raw materials. Precipitated silica finds value in its controllable particle size, absorbency, and reinforcing capability.

Tire and Rubber – Major End Use

Tires and rubber account for the largest share of the end-use market for precipitated silica. This material is used in passenger cars, trucks, and electric vehicle tires. The trend towards using green tires and eco-friendly mobility solutions is contributing to the rise in its demand. The application of precipitated silica in the manufacturing of hoses, belts, seals, and footwear rubber is another area where it finds usage in industrial rubber products.

Oral Care, Food, and Pharma — Secondary Demand Drivers

Precipitated silica is extensively utilized in toothpaste as a thickening and abrasive agent to help keep performance at maximum while keeping the enamel protected. In foods, the material acts as a flow aid and anti-caking agent. The use of this material in pharmaceuticals for making tablets and handling powdered formulations is also a source of ongoing demand for the product outside of automobiles.

Key Producers and Regional Leadership

Top producers are Evonik Industries AG, Solvay, Tata Chemicals, PPG, and PQ Corporation. The Asia Pacific region leads demand for precipitated silica in the world owing to strong tire manufacturing operations in the area. Europe also plays a significant role due to green tire regulations. Investment is being made in North America to meet demand for tires and chemicals.

Fumed Silica Market — Size, Share, and Industrial Applications

The fumed silica market was valued at USD 8.22 billion in 2025. The market is projected to witness a CAGR of 8.70% from 2026 to 2034.

The market for fumed silica is witnessing rapid growth due to increased usage in various top-notch coatings, adhesives, sealants, electronics, and industrial specialties. Fumed silica is produced through the flame hydrolysis technique and is known for its characteristics of fine particle size, high surface area, thickening properties, and moisture control features. Due to these characteristics, fumed silica is considered a superior-grade silica product.

Production Process and Core Properties

Fumed silica, also known as pyrogenic silica, is obtained through a reaction between silicon tetrachloride in a hydrogen-oxygen flame at high temperatures. These properties yield highly pure silica with excellent dispersion ability. The major advantages of fumed silica include rheological behavior, caking resistance, reinforcing capability, and surface modification compatibility.

Primary Applications — Coatings, Adhesives, and Electronics

Fumed silica is extensively employed in paint and coating formulations to inhibit sagging, enhance suspension capability, and improve scratch resistance. It acts as a thickening agent in adhesives and sealants and as an additive in silicone elastomers and building chemicals to improve their physical strength. In electronic devices, fumed silica finds application in encapsulants, thermal pastes, and specialized materials requiring high purity and viscosity control.

Emerging EV and Battery Applications

The rise of electric vehicles opens new opportunities for fumed silica in the manufacture of batteries, thermal interface materials, sealing agents, and lightweight parts. The compound may help increase thermal resistance, electrical insulation, and mechanical properties. With rising demand for batteries with improved safety features, the use of fumed silica in mobility applications will continue to grow.

Silica Gel Market — Desiccant Applications and Growth Outlook

The silica gel market stood at USD 4.11 billion in 2025. The market is anticipated to register a CAGR of 7.60% from 2026 to 2034.

The demand for silica gel is fueled by the growing need for moisture-control products across various sectors. These include the pharmaceutical, electronics, food packaging, industrial packaging, and logistics industries. Silica gel is an amorphous silica-based material that is highly absorbent. The increasing emphasis on quality in the supply chain drives the need for effective packaging.

Pharmaceutical and Electronics Packaging

The silica gel pack and canister serve as a moisture protection agent for tablets, capsules, and diagnostics. As far as electronic packaging is concerned, silica gel prevents condensation and corrosion in the packaging process. Increasing global trade in pharmaceuticals, semiconductors, sensors, and consumer electronics will further enhance the market growth for packaging-grade silica gel.

Industrial and Specialty Applications

Silica gel is employed in air drying systems, purified gas processing, museum preservation, leather storage, and chromatography processes. The reusable and consistent absorption nature makes silica gel an important material for many industries. The growing awareness of shelf life and moisture management issues is driving demand for silica gel.

Regional Demand and Key Producers

The Asia Pacific region has the leading share of demand due to the availability of substantial production and packaging facilities for pharmaceutical products. North America and Europe are critical regions for the healthcare sector and electronics industry. The prominent companies are Fuji Silysia Chemicals, Clariant, Grace, PQ Corporation, and local makers of specialty silica.

Fused Silica Market — Semiconductor, Optics, and Photovoltaic Applications

Fused silica industry growth is attributed to increasing requirements for semiconductor fabrication, photovoltaics, optical technology, and high-temperature industrial uses. Fused silica refers to a highly pure form of amorphous silicon dioxide characterized by its low coefficient of thermal expansion, high level of transparency, resistance to chemicals, and high heat stability. These properties make it important in precision manufacturing environments.

Semiconductor Lithography and Silicon Crystal Growth

Fused silica is used in semiconductor lithography equipment, wafer processing equipment, quartz ware, diffusion tubes, and crystal growth equipment. Due to its high purity and thermal shock resistance, fused silica is very essential in the manufacture of chips. As more semiconductor plants are being built worldwide to meet the increasing demands for AI, memory, and logic chips, there will be an increasing consumption of fused silica products.

Solar Photovoltaic and Optical Applications

Fused silica is used for photovoltaic applications in specialized glass, wafer-processing equipment, and thermal processing. Fused silica has its uses in optics, lasers, fiber optics, lenses, and applications requiring UV transmission because of its high optical clarity. The expansion of the renewable energy sector, together with photonics industries, has been driving growth in demand.

Key Producers and Market Outlook

Key producers are Heraeus, Corning, Tosoh, Shin-Etsu Quartz, and engineering materials companies. The Asia-Pacific region dominates production and usage because of its semiconductor manufacturing operations. North America and Europe are key markets for photonics and manufacturing.The industry outlook remains positive, as technology sectors keep growing globally.

Colloidal Silica Market — Semiconductor CMP and Precision Casting

The colloidal silica market is projected to register a CAGR of 8.40% from 2026 to 2034. The demand for colloidal silica is rising steadily owing to its widespread applications in semiconductor production, precise casting, paper processing, catalysis, and specialty industrial goods. The colloidal silica product is composed of silica nanoparticles suspended in a liquid medium that provides excellent stability, polishing, and bonding capabilities.

Chemical Mechanical Planarization — Primary Growth Engine

Chemical mechanical polishing (CMP) use is expected to continue to boost the demand for colloidal silica. The CMP process involves the use of CMP slurry made from colloidal silica to smooth semiconductor wafer surfaces, creating multilayered chips at the nanoscale levels. With growing demand for chip node fabrication, artificial intelligence processors, and memory technology, there will be a rising demand for high-purity colloidal silica CMP.

Precision Casting, Paper Coating, and Industrial Uses

Colloidal silica is extensively applied in investment casting for aerospace and automobile industry metal parts. It is also used in paper coatings, refractory products, catalyst carriers, textile finishes, and specialized surface treatments. This wide variety of applications ensures steady long-term demand outside the electronics sector.

Regional Analysis

Asia Pacific

Asia Pacific accounted for over 46.56% revenue share of the global silica market in 2025. This is due to rapid urbanization and bulk infrastructure development in China, India, and Southeast Asia in construction, glass, and industry end uses. Also, growth in automotive and tire manufacturing bases is pushing increased consumption of reinforcing silica used in rubber and tire compounding.

China led the Asia Pacific market in 2025, driven by the growing electronics, semiconductor fabs, and solar module production. According to the Semiconductor Industry Association, the Chinese government is investing over USD 150 billion between 2014 and 2030 to enhance its semiconductor ecosystem, contributing enormously to the demand for high-quality silica materials.

North America

North America is projected to grow at a 7.6% CAGR during the projection period. This is due to rising demand for high-purity silica in semiconductor production, hyperscale data centers, and EV battery manufacturing. Also, the rising oil & gas industry, particularly for hydraulic fracturing (frac sand) applications, is accelerating the market growth.

The U.S. dominated the North America market due to high growth in solar panel installations, which generated huge demand for high-quality silica in solar photovoltaic glass and wafer production. Solar represented 56% of all new electricity-generating capacity added to the U.S. grid in the first half of 2025, totaling 18 GW installed, according to the Solar Energy Industries Association.

Europe

Europe held a significant share of 22.0% in 2025. The regional market is driven by increasing investments in EV and battery production. In 2025, six flagship EV battery cell manufacturing projects received around USD 920 million in grants from the European Commission under the Innovation Fund, funded by revenues from the EU ETS. Also, stringent environmental laws are driving the application of low-emission and green materials, increasing silica adoption in coatings, polymers, and rubber substitutes.

Latin America

Latin America is one of the developing markets for silica, accounting for 6.0% revenue share in 2025. Brazil, Mexico, and Argentina are among the major countries in the region. Some of the driving forces behind the consumption of silica in the region include construction activities, glass manufacturing, ceramics, and industries. Urbanization and manufacturing growth are expected to further support market development.

Middle East & Africa

The Middle East & Africa is projected to grow at a 5.0% CAGR. The market is driven by investments in infrastructure, water desalination facilities, and water treatment systems, as well as diversification across industries. Countries like Saudi Arabia, the UAE, and South Africa have been investing in construction and specialized construction materials. Growth can be expected in the long run as industrial sectors expand.

Key Players and Competitive Analysis

The global silica market is moderately competitive. Firms are focusing on product purity, particle size management, and specialty applications across sectors such as chemicals, construction, coatings, electronics, and pharmaceuticals. Companies are also investing in innovative technologies for product processing, which will help them meet the increased demand for silica across different sectors. Sustainability drivers, regulatory compliance, and strategic alliances with end users are becoming major factors in shaping market competition and expansion.

A few of the key silica market companies are Cabot Corporation, Evonik Industries AG, Fuso Chemical Co., Ltd., Glimmerglass Ltd., Grace Davison (a division of W. R. Grace & Co.), Imerys S.A., J.M. Huber Corporation, Kao Corporation, Lorde Silica Industries Ltd., Nissan Chemical Corporation, Omya International AG, PPG Industries Inc., Red River Silica Inc., Sibelco NV, and Tosoh Corporation.

Evonik Industries AG is a major manufacturer of synthetic amorphous silica. It is headquartered in Germany. Evonik has a strong portfolio of products and is a key player in the field of high-performance products and sustainability. They have a strong R&D base and a global footprint.

Nissan Chemical Corporation is a Japanese company specializing in high-purity colloidal silica products. Their products under the SNOWTEX brand are commonly used in the semiconductor, electronics, and coatings industries. Nissan Chemical is renowned for its advanced nano-particle technologies and innovation capabilities for high-precision applications.

List of Key Companies

- Cabot Corporation

- Evonik Industries AG

- Fuso Chemical Co., Ltd.

- Glimmerglass Ltd.

- Grace Davison

- Imerys S.A.

- J.M. Huber Corporation

- Kao Corporation

- Lorde Silica Industries Ltd.

- Nissan Chemical Corporation

- Omya International AG

- PPG Industries Inc.

- Red River Silica Inc.

- Sibelco NV

- Tosoh Corporation

Industry Developments

- January 2026: Solvay inaugurated Europe's first bio-circular silica plant in Livorno, Italy. The company stated that the facility will produce highly dispersible silica (HDS) from rice husk ash for sustainable tires. (source: solvay.com)

- October 2025: HPQ Silicon Inc. completed the seventh test series of its Fumed Silica Reactor (FSR) pilot plant, which is a proprietary reactor, under a collaborative development with PyroGenesis Inc. This is a milestone towards commercializing a direct-quartz-to-fumed-silica process that is energy-saving and has lower carbon emissions than conventional processes. (Source: hpqsilicon.com)

- January 2025: Evonik announced the closure of its silica plants in Waterford, New York (mid-2025), and Havre de Grace, Maryland (mid-2026). The move helps network optimization. (Source: evonik.com)

- January 2025: PQ completed the acquisition of Sibelco Group’s specialty silicate business at the Lödöse facility in Sweden. The company stated that the move will strengthen its footprint in the Nordic region. It will enable the company to extend its silicate products and services to a broader customer base. (Source: pqcorp.com)

- November 2024: Qemetica completed the acquisition of PPG’s silica business for around USD 310 million. The deal includes production sites in the US and Netherlands. (Source: qemetica.com)

- October 2024: Evonik Industries announced a project at its Charleston site in Berkeley County, South Carolina. According to Evonik, the project would increase its production of precipitated silica by 50%. It would help meet the increasing demand from the U.S. tire industry, especially for green tire use. (Source: evonik.com)

Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Crystalline Silica

- Quartz

- Cristobalite

- Tridymite

- Amorphous Silica

- Precipitated Silica

- Silica Gel

- Colloidal Silica

- Fumed Silica

- Fused Silica

- Other Amorphous Silica

By End-User Industry Outlook (Revenue, USD Billion, 2021–2034)

- Building and Construction

- Shale Oil and Gas

- Glass Manufacturing

- Water Treatment

- Electronics & Semiconductors

- Automotive & Transportation

- Healthcare & Pharmaceuticals

- Food & Beverages

- Personal Care & Cosmetics

- Chemicals & Industrial Processing

- Agriculture

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Silica Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 45.66 billion |

| Market Size in 2026 | USD 49.06 billion |

| Revenue Forecast by 2034 | USD 89.83 billion |

| CAGR | 7.90% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Silica Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market for silica was valued at USD 45.66 billion in 2025 and is projected to grow to USD 89.83 billion by 2034.

The global market is projected to register a CAGR of 7.90% during the forecast period.

Asia Pacific led the global market in 2025. This is due to rising urbanization and infrastructure development in the region.

A few of the key silica market companies are Cabot Corporation, Evonik Industries AG, Fuso Chemical Co., Ltd., Glimmerglass Ltd., Grace Davison (a division of W. R. Grace & Co.), Imerys S.A., J.M. Huber Corporation, Kao Corporation, Lorde Silica Industries Ltd., Nissan Chemical Corporation, Omya International AG, PPG Industries Inc., Red River Silica Inc., Sibelco NV, and Tosoh Corporation.

The amorphous segment accounted for the largest market share in 2025. This is due to its wide use in industries such as rubber, coatings, adhesives, and food products.

The shale oil and gas segment is projected to witness the fastest growth during the forecast period. The high use of silica sand in hydraulic fracturing as a proppant material contributes to the segment’s rapid growth.

The silica market is expected to grow significantly due to rising demand in semiconductors, EVs, and renewable energy sectors.

Silica is used in wafer production, insulation, and chip manufacturing.

The increased usage in construction, electronics, automotive, and energy industries drives market demand.

Silica is used in thermal insulation and separators in EV batteries.

Download Sample Report of Silica Market

Please fill out the form to request a customized copy of the research report.