Semiconductor Market Demand, Opportunity, Industry Report, 2026-2034

REPORT DETAILS

Semiconductor Market Summary

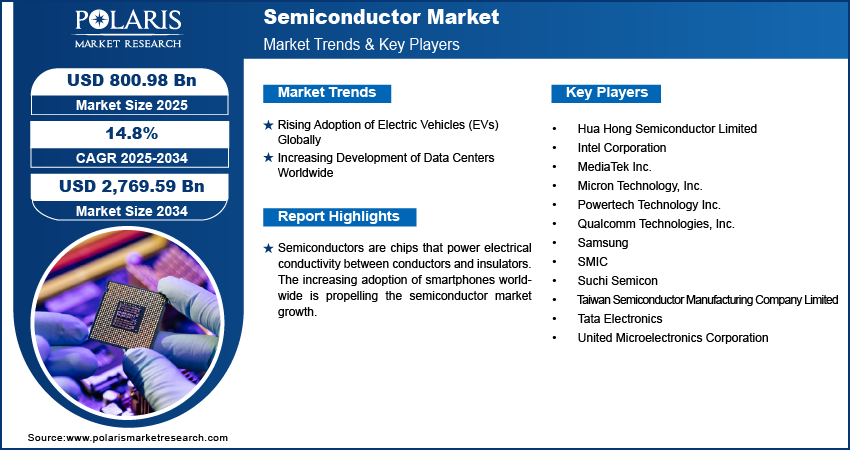

Semiconductor market size was valued at USD 799.38 billion in 2025. The market is projected to grow from USD 914.80 billion in 2026 to USD 2,768.34 billion by 2034, exhibiting a CAGR of 14.8% during 2026-2034. The market is driven by rising demand for consumer electronics, AI, 5G, and electric vehicles, alongside advancements in chip design, miniaturization, and fabrication. Government investments, supply chain localization, and increasing automation further accelerate market growth and innovation globally.

Market Statistics

Key Takeaways

- The consumer electronics segment dominated the market in 2025, accounting for 34.5% of total revenue. This growth was backed by strong demand for smartphones, laptops, and smart devices.

- The logic devices segment held a significant market share of 30.6% in 2025, driven by rising demand for high-performance computing, artificial intelligence applications, and cutting-edge consumer electronics. These sectors require powerful and efficient logic chips to support complex processing tasks.

- The automotive segment is poised for rapid growth at CAGR of 15.5%, fueled by the increasing electrification of vehicles and advancements in autonomous driving technologies. These trends are pushing demand for specialized semiconductors that enhance vehicle safety, efficiency, and connectivity.

- The Asia Pacific dominated the market in 2025, accounting 59.5% revenue share, driven by robust manufacturing infrastructure, strong consumer demand, and proactive government initiatives that promoted innovation and technology adoption. This region remains a global hub for semiconductor production and development.

- North America’s semiconductor market is expected to growth at CAGR of 14.0% during the forecast period, driven by substantial investments in new fabrication plants, strategic collaborations with international technology companies, and increasing demand from the AI, cloud computing, and automotive sectors.

Industry Dynamics

- The rising demand for consumer electronics and growing adoption of IoT devices are accelerating the market growth, as these technologies require advanced chips for improved performance and enhanced connectivity.

- The expansion of automotive electronics and increasing investments in 5G infrastructure are further propelling market growth by driving the demand for high-performance semiconductors.

- Supply chain disruptions and raw material shortages are limiting production capacities, resulting in delays and increased costs across the semiconductor industry.

- Advancements in AI and machine learning present significant opportunities for semiconductor innovation, enabling the development of smarter, faster chips that support emerging applications across multiple sectors.

Source: Polaris Market Research Analysis

What is Semiconductor?

Semiconductors are chips that power electrical conductivity between conductors and insulators. They are typically solid chemical elements or compounds, such as silicon, germanium, and gallium arsenide, which conduct electricity under certain. This unique property makes them ideal for controlling electrical currents in electronic devices. Semiconductors are crucial components in electronic devices such as diodes, transistors, and integrated circuits. Semiconductors are also found in computers, smartphones, medical equipment, automotive systems, and others.

The increasing adoption of smartphones worldwide is propelling the semiconductor market growth. Smartphones rely heavily on various semiconductors such as processors, memory chips, sensors, and communication modules to enhance device performance, improve energy efficiency, and support new features, including artificial intelligence and augmented reality. The increasing adoption of smartphones also boosts demand for wireless chargers and smartwatches, which rely on semiconductors. Moreover, the rising adoption of smartphones propels manufacturers to continuous innovation in smartphone technology, which drives demand for advanced semiconductors. Features such as high-resolution cameras, 5G connectivity, and artificial intelligence capabilities necessitate advanced semiconductor chips. Therefore, the demand for semiconductors is increasing with the rising adoption of smartphones worldwide. For instance, according to the Groupe Speciale Mobile Association (GSMA) annual State of Mobile Internet Connectivity Report 2023, over half (54%) of the global population, or some 4.3 billion people, owns a smartphone.

The market demand is driven by the growing shift toward automation in industries. Automated systems industries rely heavily on semiconductor components to function effectively. These systems require processors, sensors, and other chips to perform tasks, gather data, and make decisions, thereby increasing the need for advanced semiconductor chips. Moreover, automation drives the development of advanced technologies such as robotics, artificial intelligence, and machine learning. These technologies demand high-performance semiconductors to process complex algorithms and handle large datasets efficiently. Hence, as more industries adopt automation into their operation, the production of semiconductors surges.

Types of Semiconductors

| Type | Function | Application | Role |

| Logic Devices | Processes data and calculations | CPUs, GPUs, smartphones, computers | Acts as the brain |

| Memory Devices | Stores data | RAM, SSDs, mobile storage | Stores data and programs |

| Analog IC | Handles continuous signals | Audio, power systems, signal processing | Converts real signals |

| Sensors | Detects physical changes | Phones, cars, industrial systems | Senses environment |

| Power Devices | Manages electrical power | EVs, power supplies, machines | Controls power flow |

Source: Polaris Market Research Analysis

Market Dynamics

Rising Adoption of Electric Vehicles (EVs) Globally

Electric vehicles (EVs) rely on semiconductor-based power management systems, battery controllers, and motor drivers to ensure efficient energy consumption and optimal performance. Automakers are further continuously developing more advanced EV models, which necessitate the use of high-performance semiconductor chips to enhance battery efficiency, driving range, and overall vehicle safety. Additionally, EVs incorporate advanced electronic systems for features such as advanced driver-assistance systems (ADAS), infotainment, and connectivity. These systems demand high-performance semiconductors to process data, enable real-time decision-making, and support seamless communication. Thus, the market revenue is growing with the increasing adoption of electric vehicles. For instance, according to data published by the International Energy Agency, almost 14 million new electric cars were registered globally in 2023, bringing their total number on the roads to 40 million.

Increasing Development of Data Centers Worldwide

Organizations across the world are building data centers to support cloud computing, artificial intelligence, and big data analytics, all of which require semiconductor components such as powerful processors, memory chips, and specialized accelerators. These semiconductor components ensure fast data processing, efficient energy consumption, and reliable system performance, enabling data centers to handle massive workloads seamlessly. Furthermore, the focus on energy efficiency in data centers also boosts semiconductor demand. Data centers consume significant amounts of energy, and semiconductor components play a crucial role in reducing power consumption and improving cooling efficiency, which increases their adoption in data centers. Thus, as the development of data centers increases, the semiconductor market expansion also spurs. For instance, in April 2024, Dublin-based data center developer Chirisa announced to build a new data center in Virginia’s Meadowville Technology Park of about 139,000 square feet.

Source: Polaris Market Research Analysis

Segment Analysis

By Component Insights

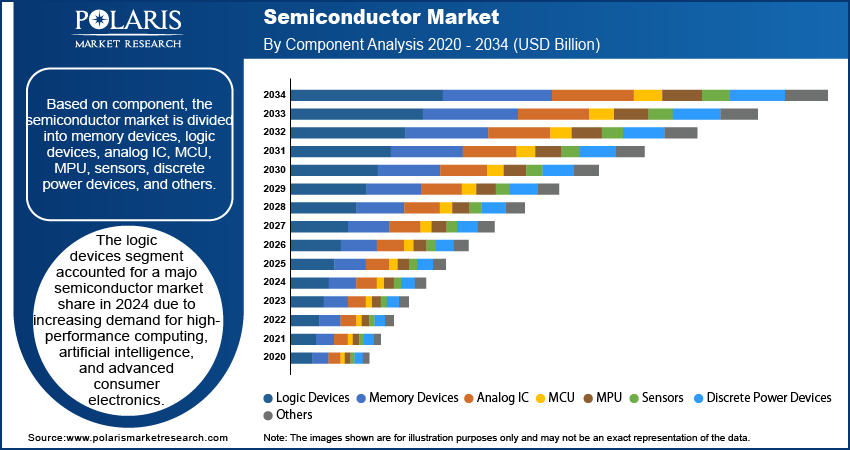

Based on component, the semiconductor market is divided into memory devices, logic devices, analog IC, MCU, MPU, sensors, discrete power devices, and others. The logic devices segment accounted for a major market share in 2025 due to increasing demand for high-performance computing, artificial intelligence, and advanced consumer electronics. The rapid adoption of 5G networks further contributed to the segment growth, as modern communication infrastructure relies heavily on high-speed logic processing chips. Major technology firms and automotive manufacturers also accelerated the integration of logic devices in electric vehicles, autonomous driving systems, and smart devices. This increases the need for logic chips capable of handling complex computational tasks efficiently.

By Application Analysis

In terms of application, the semiconductor market is segregated into telecommunication, defense & military, industrial, consumer electronics, automotive, and others. The automotive segment is expected to grow at a rapid pace in the coming years, owing to the rapid electrification of vehicles and advancements in autonomous driving technology. Automakers are integrating advanced driver-assistance systems (ADAS), AI-powered infotainment platforms, and high-performance computing units into their models, which drives demand for semiconductors. The shift toward electric vehicles (EVs) has also increased the need for power management chips, microcontrollers, and sensors that optimize battery efficiency and enhance vehicle safety. Governments worldwide are enforcing stricter emissions regulations and promoting sustainable transportation, driving investments in EV technology and smart mobility solutions, thereby fueling demand for semiconductor chips.

Semiconductor Value Chain

| Stage | What happens | Key activities | Output | Importance |

| Design | Chip idea is created based on use like mobile, EV, AI | Circuit design, chip architecture, simulation, IP integration | Chip blueprint/design file | Sets performance, speed, power use |

| Fabrication | Design is made into real chip on silicon wafer in fab | Lithography, etching, deposition, doping | Silicon wafer with multiple chips | Turns design into physical chip |

| Packaging | Chips are separated and packed for use | Dicing, bonding, encapsulation | Packaged semiconductor chip | Protects chip and allows connection |

| Testing | Chips are checked before sending to market | Functional testing, reliability testing, defect check | Tested and approved chips | Ensures chip works properly and reduces failure |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

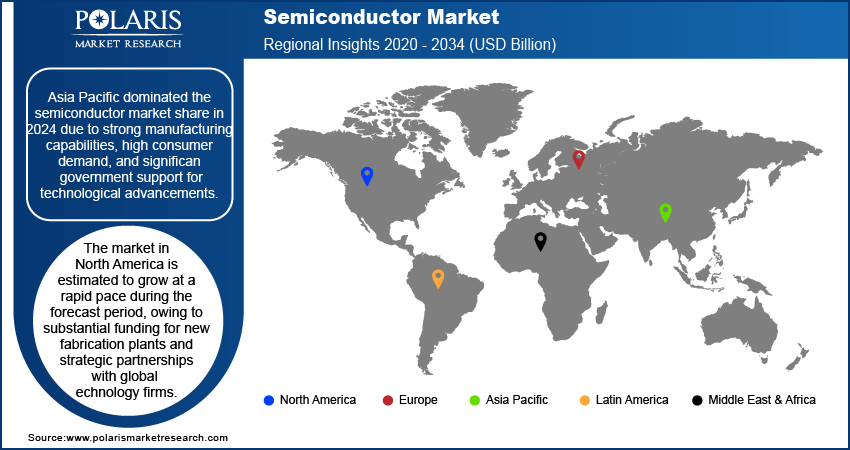

By region, the report covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominated the market share in 2025 due to strong manufacturing capabilities, high consumer demand, and significant government support for technological advancements. Countries such as China, South Korea, Taiwan, and Japan led semiconductor production, research, and development efforts, ensuring a steady supply of advanced chips for various industries. China dominated the region due to its massive electronics manufacturing ecosystem, extensive investments in fabrication plants, and increasing self-sufficiency initiatives. The country accelerated domestic chip production to reduce reliance on imports while companies expanded facilities to meet the growing needs of the automotive, consumer electronics, and industrial sectors. Taiwan, home to leading semiconductor foundries, played a crucial role in supplying advanced logic and memory chips to global markets, further strengthening Asia Pacific’s dominance.

The semiconductor market in North America is estimated to grow rapidly during the forecast period. This is due to rising substantial funding for new fabrication plants, strategic partnerships with global technology firms, and growing demand from artificial intelligence, cloud computing, and automotive industries. Companies in the region are establishing advanced semiconductor manufacturing facilities to counter supply chain disruptions and reduce dependence on foreign suppliers. The rising adoption of electric vehicles, high-performance computing, and defense applications further fuels the demand for semiconductor chips.

Source: Polaris Market Research Analysis

Key Market Players & Competitive Analysis Report

Major semiconductor companies are aggressively investing in R&D to diversify their product portfolios and drive market expansion. These key players are also pursuing strategic initiatives to strengthen their global presence, such as launching innovative products, forming international partnerships, increasing capital expenditures, and engaging in mergers and acquisitions. Such efforts are accelerating growth and fostering technological advancements in the market.

The market is fragmented, with the presence of numerous global and regional market players. Major players in the market include Hua Hong Semiconductor Limited; Intel Corporation; MediaTek Inc.; Micron Technology, Inc.; Powertech Technology Inc.; Qualcomm Technologies, Inc.; Samsung; SMIC; Suchi Semicon; Taiwan Semiconductor Manufacturing Company Limited; Tata Electronics; and United Microelectronics Corporation.

Qualcomm Technologies, Inc. is a major developer and supplier of advanced semiconductor products and services, particularly in the wireless communications sector. Headquartered in San Diego, California, Qualcomm has been at the forefront of innovation in digital wireless communications since its establishment in 1985 by Irwin Jacobs and six other co-founders. Qualcomm is renowned for its semiconductor technology, which powers a vast array of devices, including smartphones, laptops, tablets, and automotive systems. The company operates primarily as a fabless semiconductor manufacturer, meaning it designs and develops semiconductor products but outsources its physical manufacturing to other companies. Qualcomm's semiconductor products include system processors, audio components, wireless networking components, and radio frequency components, which are integral to modern wireless communication systems.

Micron Technology, Inc. is a prominent American semiconductor company specializing in the design, manufacture, and sale of memory and storage products. Founded in 1978 in Boise, Idaho, Micron has grown to become one of the largest semiconductor companies globally, ranking as the fifth largest in 2024. Micron operates through several business units, including the Compute and Networking Business Unit (CNBU), Mobile Business Unit (MBU), Storage Business Unit (SBU), and Embedded Business Unit (EBU). The company's product portfolio includes dynamic random-access memory (DRAM), NAND flash, NOR flash, and solid-state drives (SSDs), which are crucial components in a wide range of applications, from consumer electronics and data centers to automotive and industrial systems

List of Key Companies

- Hua Hong Semiconductor Limited

- Intel Corporation

- MediaTek Inc.

- Micron Technology, Inc.

- Powertech Technology Inc.

- Qualcomm Technologies, Inc.

- Samsung

- SMIC

- Suchi Semicon

- Taiwan Semiconductor Manufacturing Company Limited

- Tata Electronics

- United Microelectronics Corporation

Benefits vs Challenges of Semiconductors

Semiconductors provide benefits like better performance, faster processing, and smaller size, which help make devices more efficient and powerful. They are largely used in AI, 5G, consumer electronics, and automotive systems. However, there are some challenges including high manufacturing cost because of complicated production and expensive setup. Supply chain complexes like raw material shortages and global tensions can also affect production and increase costs. Managing cost, supply, and continuous innovation remains a problem for organizations.

Semiconductor Industry Developments

- April 2026: Samsung Active Asset Management launched the KoAct Global AI Memory ETF. The fund aims growth opportunities in AI memory semiconductors. (Source: etfexpress.com)

- September 2025: Tata Electronics signed a memorandum of understanding (MoU) with Merck Electronics. The company stated that the strategic collaboration will focus on developing capabilities in semiconductor fabrication infrastructure and semiconductor materials in India. (Source: economictimes.indiatimes.com)

- September 2025: Intel Corporation announced a strategic collaboration with NVIDIA. The partnership will focus on the development of multiple generations of custom datacenter and personal computing products. (Source: newsroom.intel.com)

- December 2024: Suchi Semicon, an India-based semiconductor company, inaugurated its Outsourced Semiconductor Assembly and Testing (OSAT) plant in Surat to enhance India's semiconductor manufacturing capabilities. (Source: government.economictimes.indiatimes.com)

- February 2024: Tata Electronics announced that it will build a mega semiconductor fabrication facility in Dholera, Gujarat, India, in partnership with Powerchip Semiconductor Manufacturing Corporation (PSMC). The project will cost up to INR 91,000 crores (~US$11bn). (Source: tata.com)

- September 2024: The Chief Minister of Maharashtra, India, inaugurated the state’s first semiconductor manufacturing plant in Navi Mumbai, India, to reduce the country’s reliance on imported semiconductor chips. (Source: indiatoday.in)

Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Memory Devices

- Logic Devices

- Analog IC

- MCU

- MPU

- Sensors

- Discrete Power Devices

- Others

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Telecommunication

- Defense & Military

- Industrial

- Consumer Electronics

- Automotive

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 799.38 Billion |

| MMarket Forecast in 2026 | USD 914.80 Billion |

| Revenue Forecast by 2034 | USD 2,768.34 Billion |

| CAGR | 14.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021– 2024 |

| Forecast Period | 2026 – 2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Semiconductor Market FAQ's

The global semiconductor market size was valued at USD 799.38 billion in 2025 and is projected to grow to USD 2,768.34 billion by 2034.

The global market is projected to register a CAGR of 14.8% during the forecast period.

Asia Pacific had the largest share of the global market in 2025.

Some of the key players in the market are Hua Hong Semiconductor Limited; Intel Corporation; MediaTek Inc.; Micron Technology, Inc.; Powertech Technology Inc.; Qualcomm Technologies, Inc.; Samsung; SMIC; Suchi Semicon; Taiwan Semiconductor Manufacturing Company Limited; Tata Electronics; and United Microelectronics Corporation.

The logic devices segment dominated the semiconductor market in 2025.

Download Sample Report of Semiconductor Market

Please fill out the form to request a customized copy of the research report.