Surgical Robots Market Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

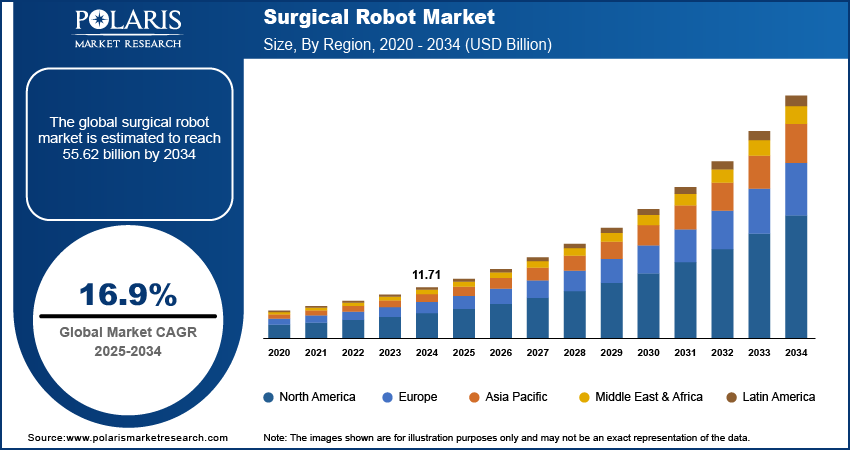

Surgical Robot Market Summary

The surgical robot market size was valued at USD 13.69 billion in 2025 and is expected to register a CAGR of 16.9% from 2026 to 2034. The market for surgical robots is primarily driven by technological advancement in medical devices by leading players in the market. Further, rising number of complex surgeries propels the demand for surgical robots.

Market Statistics

Key Takeaways

- The instruments and accessories segment is expected to experience the highest CAGR of 22.5% during the forecast period. This is due to the constant need to repurchase instruments and accessories for maintenance, repairs, or modifications.

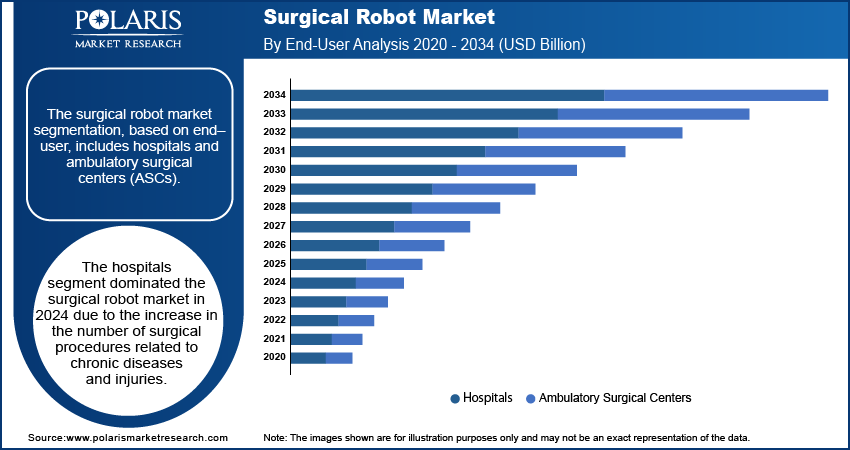

- The hospitals segment dominated the market with 80.0% in 2025. This growth is attributed to the increase in the number of surgical procedures related to chronic diseases and injuries.

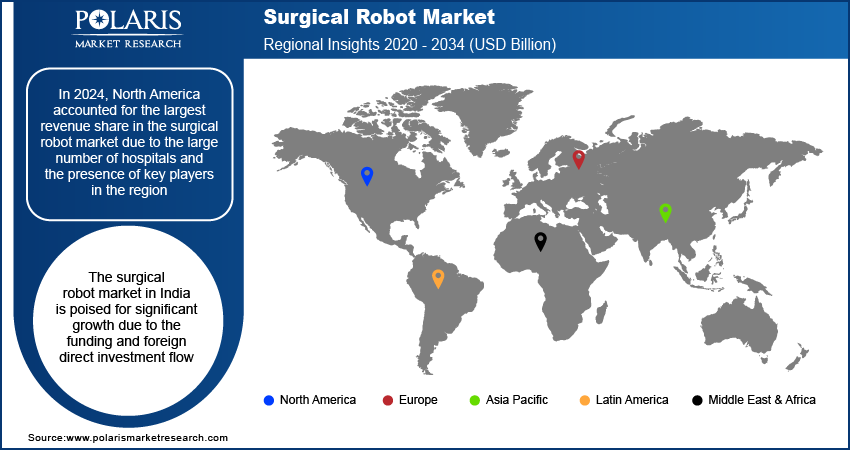

- In 2025, North America accounted for the largest revenue share accounting for 40.0%. The large number of hospitals and the presence of key players in the region contributed to the leading position.

- The industry in Asia Pacific is projected to register a substantial CAGR of 21.0% during the forecast period. The growth is primarily attributed to rising partnerships between global and local players.

- The India surgical robot market is expected to register the highest CAGR of 18.5% during the forecast period. The growth is attributed to the rising funding and foreign direct investment and the entry of new players with advanced technology.

Industry Dynamics

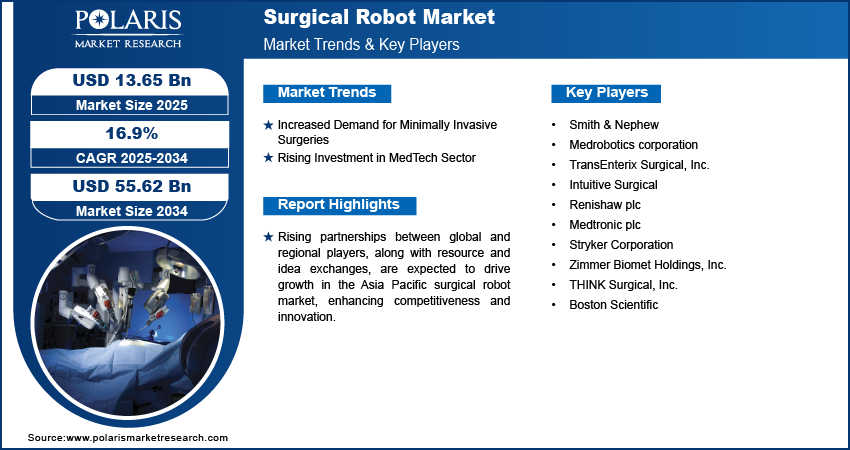

- Increasing demand for minimally invasive surgeries is driving the adoption of surgical robots.

- Rising investments in the medtech sector is propelling the market size.

- Lack of a skilled workforce hinders the demand for surgical robots.

- Technological advancements in surgical robots are expected to offer lucrative opportunities in the coming years.

AI Impact on Surgical Robot Market

- Artificial intelligence (AI) algorithms analyze patient data and surgical history. It helps surgeons with predictive insights during surgeries.

- Machine learning (ML) and computer vision enhance accuracy, minimize the risk of human error, and reduce recovery times.

- The adoption of AI facilitates intuitive interaction between robotic systems and surgeons, which streamlines complex procedures.

- AI-integrated robots are used for laparoscopic procedures.

Source: Polaris Market Research Analysis

What are Surgical Robots?

Surgical robots are advanced medical devices that are designed to assist doctors during complex surgical procedures. Major companies worldwide with large research and development facilities have started targeting new scopes of technology and current areas of applications, which are anticipated to fuel the surgical robot market in the forecast years. For instance, in 2020, Sina Robotics and Medical Innovators introduced robotic telesurgery. Robotic telesurgery involves using robotic systems and telecommunication technology to perform surgical procedures remotely. Surgeons control robotic arms from a distance, allowing precise and minimally invasive operations, improving access to expert care, and enhancing patient outcomes. If a surgeon wants to perform surgery on patients situated on different continents, it is possible with robotic telesurgery. This advancement in technology has led to the expansion of the surgical robot market

The surgical robot market is expected to grow due to the increased number of complex surgeries globally attributed to chronic diseases or injuries. The increasing geriatric populations with chronic conditions in major countries have led to a higher number of surgeries performed annually, which is anticipated to boost the demand for the surgical robot in the near future. For instance, according to the World Health Organization, the number of inpatient surgical procedures performed in the European region reached an estimated 15 million procedures in 2020, up from an estimated 5 million in 2009. Similarly, an estimated 32 million surgeries are performed in India annually. In May 2024, the Government of Saskatchewan reported that more than 96,000 surgeries were performed in the country during 2023–2024, marking the highest number of surgeries ever performed in a single year. Therefore, growing number of complex surgeries is anticipated to drive the surgical robot market growth.

Comparison Matrix: Robotic vs. Traditional Surgery

| Parameter | Robotic Surgery | Traditional Surgery |

| Initial Investment | High capital expenditure for robotic systems, software, and maintenance | Lower upfront investment with standard surgical equipment |

| Operating Cost | Higher due to service contracts, disposable instruments, and staff training | Lower operating costs with familiar tools and existing workforce |

| Return on Investment (ROI) | Higher long-term ROI through premium procedures, patient attraction, and efficiency gains | Stable ROI but limited premium pricing opportunities |

| Hospital Positioning | Enhances brand value and supports advanced-care positioning | Standard offering with less competitive differentiation |

| Patient Demand | Attracts patients seeking minimally invasive and advanced procedures | Preferred mainly for routine and emergency procedures |

| Surgeon Training | Requires specialized certification and continuous technical training | Conventional training already widely established |

| Procedure Efficiency | Faster recovery improves bed turnover and operational efficiency | Longer recovery may reduce patient throughput |

| Reimbursement Potential | May support higher-value procedures depending on healthcare system | Standard reimbursement structure |

| Technology Dependency | High dependence on software updates, vendor support, and system uptime | Low technology dependency and easier workflow continuity |

| Best Suited For | Urology, gynecology, cardiac, orthopedic, and complex minimally invasive procedures | Emergency surgeries, trauma cases, large tumor removal, and organ transplants |

| Adoption by Hospitals | Mostly adopted by large hospitals, specialty centers, and premium healthcare providers | Common across hospitals of all sizes, including smaller facilities |

Source: Polaris Market Research Analysis

Market Drivers

Increased Demand for Minimally Invasive Surgeries

There is an increasing demand for minimally invasive surgeries to manage chronic diseases and avoid complications related to complex surgeries, due to which the demand for the surgical robot is growing. For instance, according to the American Society of Plastic Surgeons, a total of 23 million minimally invasive cosmetic surgeries were performed in 2022, an increase from 8 million such surgeries before 2019. This represents an increase of 15 million surgeries and a 188% change between 2019 and 2024 over six years. Minimally invasive surgeries, which involve smaller incisions and reduced trauma compared to traditional surgeries, are increasingly favored due to their numerous benefits. Patients experience shorter recovery times, less pain, and fewer complications, all of which contribute to a faster return to normal activities and improved overall outcomes. As awareness of these advantages spreads, patient preference shifts towards minimally invasive options, compelling healthcare providers to adopt advanced robotic systems to meet this demand and provide optimal care. Consequently, an increase in demand for minimally invasive surgeries is anticipated to drive the surgical robot market in the forecast years.

Rising Investment in MedTech Sector

Increased investment in the medical device industry is significantly boosting the surgical robot market by fueling technological advancements and enhancing surgical outcomes. As funding grows, it accelerates the development of sophisticated robotics, artificial intelligence, and machine learning technologies, thereby enhancing the precision and capabilities of surgical robots. For Instance, in May 2024, Kotak Alternate Asset Manager Ltd. invested 48.2 million USD in medical device manufacturer Biorad Medisys to set up a new manufacturing plant. Moreover, expanded healthcare infrastructure often incorporates these advanced systems, driven by increased investment and overall healthcare expenditure. The competitive dynamics among manufacturers, driven by higher investment, lead to more innovative and cost-effective solutions, while regulatory and clinical support accelerates the introduction of new robotic systems. Additionally, investment in training and support services ensures that healthcare professionals are adept at using these advanced technologies, further promoting their adoption and simultaneously accelerating surgical market growth during the forecast period.

Source: Polaris Market Research Analysis

Segment Insights

Market Breakdown by Product Type Insights

The surgical robot market segmentation based on product type includes robotic systems, laparoscopy robotic systems, orthopedic robotic systems, neurological robotic systems, and instruments and accessories. The instruments and accessories segment is expected to experience significant growth with a high CAGR during the forecasted period. This is due to the constant need to repurchase instruments and accessories for maintenance, repairs, or modifications. For instance, according to the Journal of Minimal Access Surgery, maintaining the da Vinci surgical robot system costs around 1 million USD every year.

Real-World Applications of Surgical Robot Types

| Segment | Real-World Application |

| Robotic Systems | Multi-specialty robotic platforms used for minimally invasive procedures, such as urology, gynecology, and general surgery |

| Laparoscopy Robotic Systems | Robotic-assisted laparoscopic surgeries for prostatectomy, hysterectomy, gallbladder removal, and colorectal procedures |

| Orthopedic Robotic Systems | Robotic-guided knee and hip replacement surgeries with improved implant positioning and surgical precision |

| Neurological Robotic Systems | Robot-assisted brain and spine surgeries, including deep brain stimulation and minimally invasive spinal procedures |

Source: Polaris Market Research Analysis

Market Breakdown by End–User Insights

The surgical robot market segmentation, based on end–user, includes hospitals and ambulatory surgical centers (ASCs). The hospitals segment dominated the surgical robot market in 2024. This growth is attributed to the increase in the number of surgical procedures related to chronic diseases and injuries. Hospitals are mainly in demand for surgeries due to their better availability of resources and skilled workforce. Therefore, hospitals are considered major consumers in the surgical robot market.

Source: Polaris Market Research Analysis

Market Breakdown by Regional Insights

By region, the study provides the surgical robot market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, North America accounted for the largest revenue share in the surgical robot market due to the large number of hospitals and the presence of key players in the region. For instance, according to the American Hospital Association and the Government of Canada, there were 7,066 hospitals in North America as of 2024. Of these, 6,120 were located in the United States and 946 in Canada. Of the 946 hospitals in Canada, 317 were large, with an average of 939 beds; 230 were tiny, with an average of 30–40 beds; 71 were micro, with an average of 15 beds. The remaining 328 hospitals were medium-sized. As of 2024, there were 916,752 beds in the United States. Moreover, major players involved in mergers and acquisitions and expanding product offerings with the latest technology are anticipated to fuel the surgical robot market in North America.

Source: Polaris Market Research Analysis

Asia Pacific is projected to register a substantial CAGR during the forecast period, primarily due to rising partnerships between global and local players. These partnerships facilitate the exchange of established resources of global players and innovative ideas and technologies from startups. In 2024, MedTech Innovator, a US-based non-profit organization established to accelerate medical device companies worldwide, launched a program called 'MedTech Innovator Asia Pacific 2024 Cohort.' The main purpose of the program is to support startups with funding and by leveraging available networks. The program's leadership team, which includes investors, providers, and senior executives from world-class multinationals and medtech companies, will partner with startups. The most innovative startups will receive a reward of 3 million USD cash awards and the opportunity to partner with global players. Consequently, increasing partnerships between global and regional players, along with the exchange of ideas and resources, is expected to empower regional players with competitive and resource advantages and contribute to the surgical robot market growth in Asia Pacific.

The surgical robot market in India is poised for significant growth due to the funding and foreign direct investment flow. For instance, according to India Brand Equity Foundation, the foreign direct investment inflow in medical device manufacturing companies was 3.28 billion USD between 2000-2024. According to WIR 2024, India is the second-largest host country in terms of number of international project finance deals. In the second quarter of 2023, the FDI inflow into the hospital sector increased by 90%, rising to 1.08 billion USD from 570.6 million USD in the same quarter of 2022. Additionally, India and Russia have set a bilateral trade target of 30 billion USD for 2025, by which trade between the two countries is expected to increase by 5 billion USD per annum. As a result, the entry of new players with advanced technology is anticipated to increase, leading to overall surgical robot market growth in India in study years.

Key Players & Competitive Insights

The surgical robot market is continuously evolving, with numerous companies striving to innovate and distinguish themselves. Leading global corporations dominate the market by leveraging extensive research and development, advanced manufacturing technologies, and significant capital to maintain a competitive edge. These companies pursue strategic initiatives such as mergers, acquisitions, partnerships, and collaborations to enhance their product offerings and expand into new markets.

New companies are impacting the market by introducing innovative medical devices and meeting the needs of specific market sectors. This competitive environment is amplified by continuous progress in product offerings and new applications, greater emphasis on sustainability, and the rising requirement for tailor-made single-use products in diverse industries. Major players in the surgical robot market include Smith & Nephew; Medrobotics Corporation; TransEnterix Surgical, Inc.; Intuitive Surgical; Renishaw plc; Medtronic plc; Stryker Corporation; Zimmer Biomet Holdings, Inc.; THINK Surgical, Inc.; and Boston Scientific.

Medtronic, headquartered in Dublin, Ireland, is a prominent global leader in medical technology, committed to improving patient outcomes across various therapeutic areas. Established in 1949, the company specializes in developing and manufacturing a diverse range of advanced medical devices, including pacemakers, insulin pumps, spinal implants, robotic surgical systems, and deep brain stimulation systems. Medtronic's innovations are pivotal in treating conditions related to cardiovascular health, diabetes, neurological disorders, and spinal issues. With a presence in over 150 countries, the company leverages its extensive expertise and research capabilities to address critical healthcare challenges. Medtronic’s mission is to alleviate pain, restore health, and extend life, reflecting its dedication to enhancing the quality of care and advancing medical science. Through continuous innovation and a focus on patient-centered solutions, Medtronic plays a crucial role in shaping the future of healthcare on a global scale. In April 2024, the company launched its new Live Stream function for the Touch Surgery ecosystem, featuring AI-driven enhancements for post-operative analysis. Unveiled in April and showcased at DeviceTalks Boston, this technology supports secure live streaming of surgeries, offering immersive virtual learning and expert insights for procedures like laparoscopic cholecystectomy and robotic-assisted hysterectomy. The platform is now available in the US and Western Europe.

Smith & Nephew is a global medical technology company headquartered in London, England, specializing in advanced wound management, orthopedic reconstruction, and sports medicine. Established in 1856, the company is known for its innovative solutions that aim to improve patient outcomes and enhance the quality of care. Smith & Nephew’s product portfolio includes advanced wound care dressings, arthroscopic instruments, joint reconstruction implants, and trauma devices. With a strong commitment to research and development, the company operates in over 100 countries, focusing on providing advanced technologies and services to address a broad range of medical needs and challenges. In June 2024, the company launched its CORIOGRAPH Pre-Operative Planning and Modeling Services, offering a customized solution for partial and total knee arthroplasty. This new service is designed for use with the CORI Surgical System, which uniquely allows surgeons to opt for either image-free or image-based registration, eliminating the necessity for a pre-operative MRI scan. The launch marks a significant advancement in personalized surgical planning and robotic-assisted orthopedic procedures.

List of Key Companies

- Smith & Nephew

- Medrobotics corporation

- TransEnterix Surgical, Inc.

- Intuitive Surgical

- Renishaw plc

- Medtronic plc

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- THINK Surgical, Inc.

- Boston Scientific

Surgical Robots Industry Developments

March 2026: Healinno Tech (Beijing) Co., Ltd. (Healinno Tech) introduced the metaFlow Waterjet Surgical Robot. It is an AI-enabled system designed to improve precision, efficiency, and safety in urological surgery. (Source: PRNewswire.com)

June 2025: SS Innovations made history by performing the first robotic heart surgery in the Americas at Interhospital, Ecuador, using their SSi Mantra 3 system. The patient recovered successfully, marking a milestone for the company that now operates 80 robotic systems across 75 hospitals worldwide and is working toward FDA approval by 2026. (Source: ssinnovations.com)

April 2024: Intuitive Surgical announced that its next-generation da Vinci 5 system has received FDA clearance and will undergo a limited launch. Featuring over 150 enhancements from its predecessor, the da Vinci Xi system boasts improved precision, imaging, ergonomics, and force feedback. (Source: intutivesurgical.com)

Surgical Robot Market Segmentation

By Product Type Outlook (USD billion, 2021- 2034)

- Robotic Systems

- Laparoscopy Robotic Systems

- Orthopedic Robotic Systems

- Neurological Robotic Systems

- Instruments and Accessories

By Application Outlook (USD billion, 2021- 2034)

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Neurosurgery

- Orthopedic Surgery

- Others

By End–User Outlook (USD billion, 2021- 2034)

- Hospitals

- Ambulatory Surgery Centers (ASC’s)

By Regional Outlook (USD billion, 2021- 2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future of Surgical Robot Market

The future of the surgical robot market is expected to be driven by AI-powered precision and real-time imaging. Advanced data analytics are expected to improve surgical accuracy and patient outcomes. Remote and telesurgery capabilities are gaining attention. They enable surgeons to operate across distances with robotic assistance. Adoption of robots is rising in orthopedic, neurological, and minimally invasive procedures. It is expanding the market across hospitals and specialty centers. In addition, growing investments in healthcare automation and improved reimbursement support would boost the adoption of surgical robots. Continuous innovation in robotic platforms will accelerate global market growth.

Surgical Robot Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 13.69 billion |

| Market Size Value in 2026 | USD 15.98 billion |

| Revenue Forecast in 2034 | USD 55.74 billion |

| CAGR | 16.9% from 2026–2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report End-User |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Download Sample Report of Surgical Robots Market

Please fill out the form to request a customized copy of the research report.