U.S. Phenolic Resins Market Size, Share Report 2026-2034

REPORT DETAILS

REPORT DETAILS

U.S. Phenolic Resins Market Summary

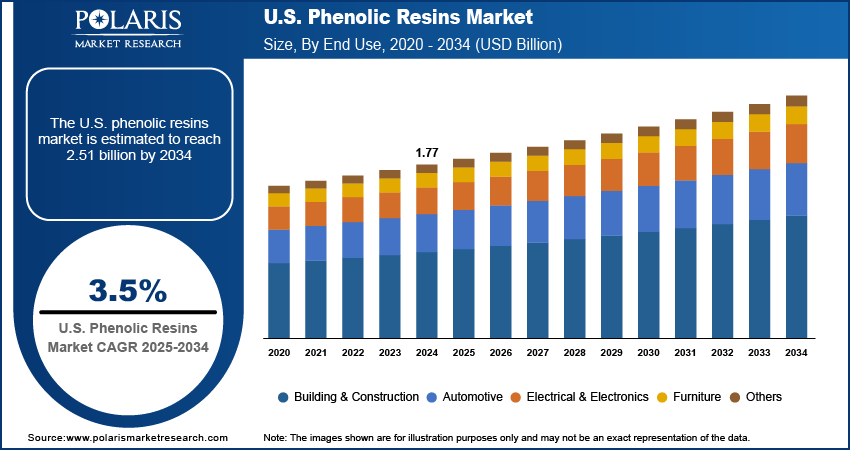

The U.S. phenolic resins market size was valued at USD 1.83 billion in 2025. The market is projected to grow at a CAGR of 3.5% from 2026 to 2034. Key factors driving demand include the development of sustainable and bio-based phenolic resins and the increasing use of phenolic resins in electronics and electrical applications.

Market Statistics

Key Takeaways

- The novolac resins segment held 49.09% revenue share in 2025 . The segment is driven by its exceptional heat resistance and mechanical strength.

- The wood adhesives segment held 40.10% of the revenue share in 2025 . This is due to the extensive use of phenolic resins in engineered wood products.

- The molding segment is projected to register a 4.6% CAGR . The segment's growth is fueled by rising demand for phenolic molding compounds in electronics and consumer goods.

- The automotive segment held 34.94% revenue share in 2025 . Phenolic resins are primarily used in brake systems and engine compartment applications.

- The building & construction segment is expected to witness a 5.7% CAGR . This is owing to the rising demand for engineered wood and insulation materials.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The demand for phenolic resins is rising in circuit boards, switches, and connectors due to their superior insulation, thermal stability, and flame resistance, ensuring reliability in critical electrical applications.

- Industrial & wood adhesives durable, moisture-resistant bonding properties make phenolic resins essential for plywood, LVL, and engineered wood, fueling growth in construction and furniture industries.

- Stricter environmental regulations on formaldehyde emissions pressure manufacturers to reformulate phenolic resins, increasing R&D costs and compliance complexities.

- Growing demand for bio-based phenolic resins in sustainable construction and electronics presents a high-growth niche, driven by green building trends.

Phenolic resins, a class of synthetic polymers formed by the reaction of phenol with formaldehyde, are widely recognized for their excellent thermal stability, mechanical strength, and resistance to chemicals. In the U.S., the market is driven by the rising focus on sustainability and the development of bio-based phenolic resins. Bio-based alternatives are being increasingly integrated into manufacturing processes, offering reduced environmental impact without compromising performance, with industries shifting toward eco-friendly solutions. This transition aligns with broader sustainability goals, as these resins are sourced from renewable feedstocks, making them a viable choice for companies looking to balance efficiency with environmental responsibility. As a result, the adoption of bio-based phenolic resins is expected to strengthen their role in diverse industrial applications.

Source: Polaris Market Research Analysis

Sustainability and regulatory influence contribute to the growth opportunities, as industries face growing pressure to adopt environmentally responsible materials while adhering to strict compliance standards. Regulatory bodies are increasingly emphasizing the reduction of carbon emissions, formaldehyde content, and overall environmental impact, which has encouraged manufacturers to innovate with greener formulations and bio-based alternatives. A May 2025 report from the U.S. EPA stated that U.S. energy-related CO₂ emissions decreased by less than 1%, 23 million metric tons, in 2024. Phenolic resins, known for their durability, fire resistance coating, and recyclability, align well with these evolving requirements, making them a preferred choice in industries seeking sustainable solutions. This dual push from regulatory frameworks and corporate sustainability goals accelerates the adoption of eco-friendly phenolic resins and also strengthens their long-term role as essential materials in modern industrial practices.

Phenolic Resins vs Epoxy Resins

| Property | Phenolic Resins | Epoxy Resins |

| Strength | High heat resistance and fire retardance properties | High adhesion and strength |

| Primary Purpose | Heat resistance and high rigidity | Good adhesion for use in structural bonding |

| Flexibility | Lower flexibility, making it less flexible | Greater flexibility and good impact resistance |

| Resistance | High chemical and thermal resistance | Outstanding chemical and moisture resistance |

| Electrical Characteristics | Outstanding electric insulation and fire resistance | Outstanding electrical insulation and durability |

| Common Uses | Brake systems in automobiles, insulation material, industrial parts | Used as coatings, adhesives, composites, electronic equipment |

Source: Polaris Market Research Analysis

Drivers & Opportunities

Increasing Use in Electronics & Electrical Applications: The increasing use of phenolic resins in electronics and electrical applications is boosting the growth opportunities, owing to their excellent insulating properties, thermal stability, and flame resistance. These characteristics make them ideal for use in circuit boards, switches, connectors, and insulation materials where reliability and safety are critical. The demand for materials that resist high temperatures and electrical stress continues to rise as electronic devices become more compact and powerful. Phenolic resins address these needs effectively, ensuring performance durability while meeting strict safety standards. This growing reliance on phenolic resins in the electronics sector strengthens their market position by supporting advancements in consumer electronics, automotive electronics, and industrial electrical systems.

Growing Demand in Industrial and Wood Adhesives: The U.S. phenolic resins market is driven by the growing demand in industrial and wood adhesives, where their strong bonding properties, durability, and resistance to moisture make them highly preferred. Phenolic resins are extensively used in plywood, laminated veneer lumber, and other engineered wood products, supporting the growth of the construction and furniture industries. According to an August 2025 report from the U.S. Census Bureau, in the U.S., total construction spending reached USD 2.136 trillion in June 2025, an increase of 0.4%, highlighting growth opportunities for plywood, OSB, and laminated veneer lumber. In addition, their application extends to industrial adhesives in sectors such as automotive and electronics, where high performance under extreme conditions is required. This expanding use across critical sectors enhances product performance and also reinforces the versatility of phenolic resins, positioning them as an important material driving innovation and reliability in adhesive technologies.

Rise of Bio-Based Phenolic Resins: The market for phenolic resins is slowly moving towards the production of bio-based products derived from natural raw materials, including lignin, natural phenols, and biomass. The factors behind this trend include increased ESG objectives, regulations regarding formaldehyde emissions, and rising demand for emission-free materials. In the industries of automobiles, construction, and lumber, there is increasing pressure to reduce the carbon footprint. This shift is resulting in the development of bio-based phenolic resins as a sustainable substitute for conventional phenolic resins.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

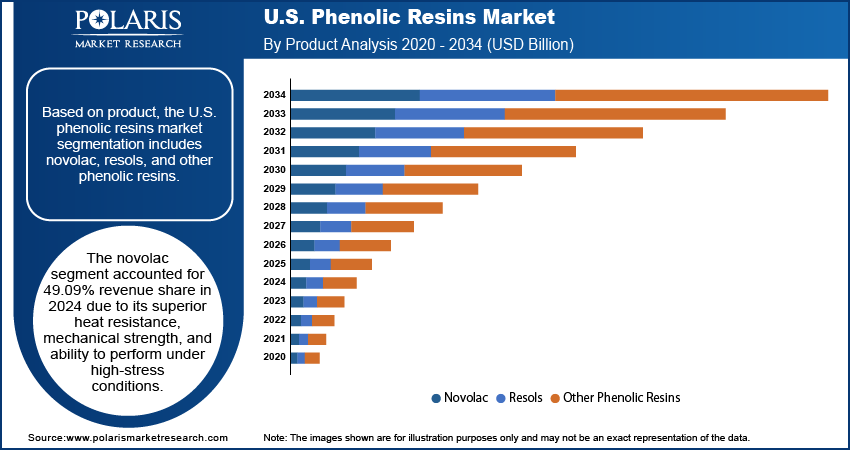

Based on product, the U.S. phenolic resins market segmentation includes novolac, resols, and other phenolic resins. The novolac segment accounted for 49.09% revenue share in 2025 due to its superior heat resistance, mechanical strength, and ability to perform under high-stress conditions. These properties make novolac resins highly suitable for applications such as coatings, abrasives, and insulation materials, where durability and thermal stability are essential. Their consistent performance and compatibility with various additives further enhance their adoption across industries. Additionally, their versatility in manufacturing processes makes them a preferred choice for sectors seeking reliable materials with long service life.

The resols segment is expected to witness the highest CAGR of 5.0% during the forecast period, owing to its wide applicability in adhesives, laminates, and molding compounds. Resols cure under heat and pressure without requiring additional hardeners, making them cost-effective and efficient for large-scale applications. Their strong adhesion, water resistance, and flame-retardant properties add to their appeal in industries such as construction, automotive, and electrical. Resols are positioned as a major growth driver in the U.S. phenolic resins market with the rising demand for advanced composites and high-performance adhesives.

Application Analysis

In terms of application, the U.S. phenolic resins market segmentation includes wood adhesives, molding, insulation, laminates, paper impregnation, coatings, refractory materials, friction material, rubber & tire, electronics, and abrasives. The wood adhesives segment held 40.10% of the revenue share in 2025 due to the extensive use of phenolic resins in engineered wood products such as plywood, particleboard, and laminated veneer lumber. Their strong bonding strength, resistance to moisture, and long-lasting performance make them a reliable choice in the woodworking and construction industries. Wood adhesives based on phenolic resins continue to gain prominence in both residential and commercial projects as demand for durable and sustainable building materials rises.

The molding segment is expected to witness the highest CAGR of 4.6% during the forecast period due to the increasing adoption of phenolic molding compounds in automotive, electronics, and consumer goods. These resins offer excellent dimensional stability, thermal resistance, and mechanical strength, making them ideal for manufacturing precision components. Their ability to replace traditional metals and plastics in high-stress applications drives their usage. Moreover, the growing demand for lightweight and durable materials across industries is expected to propel the expansion of phenolic resin-based molding applications.

End Use Analysis

The U.S. phenolic resins market segmentation, based on end use, includes building & construction, automotive, electrical & electronics, furniture, and other end uses. The automotive segment held 34.94% share in 2025, attributed to the extensive use of phenolic resins in brake pads, clutches, filters, and under-the-hood components. Their heat resistance, mechanical stability, and ability to perform in high-friction environments make them indispensable in ensuring vehicle safety and efficiency. Phenolic resins are increasingly being adopted in both conventional and electric vehicles with the shift toward lightweight yet durable materials, further consolidating their dominance in the automotive sector.

The building & construction segment is expected to witness a substantial CAGR of 5.7% during the forecast period due to the rising demand for engineered wood, laminates, and insulation materials. Phenolic resins provide excellent durability, fire resistance, and strong bonding properties, which are highly valued in modern construction practices. Their role in energy-efficient insulation products also aligns with the industry’s focus on sustainable and environmentally friendly building solutions. Continued infrastructure development and residential projects will further support the segment’s steady expansion in the coming years.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The U.S. phenolic resins industry is shaped by strategic investments, emerging market segments, and sustainable value chains, with players such as Hexion, SI Group, and Kolon Industries driving revenue growth through innovation. Disruptions and trends, such as bio-based resin development and stricter environmental regulations, are reshaping competitive positioning, pushing companies to adopt future development strategies. Small and medium-sized businesses are leveraging technological advancements to capture niche demand in high-performance adhesives and electronics. Economic and geopolitical shifts, including supply chain disruptions, influence pricing insights and vendor strategies, while expansion opportunities in the construction and automotive sectors fuel long-term growth projections. Leading firms are also exploring joint ventures and mergers and acquisitions to strengthen their regional footprint and meet latent demand. Industry trends highlight a shift toward eco-friendly formulations, creating revenue opportunities for agile competitors as sustainability becomes a priority. Expert insights suggest that business transformation and supply chain management will be critical in maintaining dominance in this evolving landscape.

A few major companies operating in the U.S. phenolic resins industry include Arclin Inc., Ashland Inc., Bakelite Synthetics, Eastman Chemical Company, Hexcel Corp., Hexion, Kraton Corporation, Olympic Panel Products LLC, Owens Corning, and SI Group.

Key Players

- Arclin Inc.

- Ashland Inc.

- Bakelite Synthetics

- Eastman Chemical Company

- Hexcel Corp.

- Hexion

- Kraton Corporation

- Olympic Panel Products LLC

- Owens Corning

- SI Group

U.S. Phenolic Resins Industry Developments

-

January 2026: BASF introduced a new near-zero Semi-Volatile Organic Compound (SVOC) resin technology for interior coatings. The company stated that the technology enables low-odor and high-performance coatings. (source: basf.com)

-

June 2025: Hexion announced a partnership with Bloom Biorenewables. According to Hexion, the collaboration aims at commercializing a renewable, high-performance alternative to synthetic adhesives. (source: hexion.com)

U.S. Phenolic Resins Market Segmentation

By Product Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Novolac

- Resols

- Liquid Resols

- Solid Resols

- Other Phenolic Resins

By Application Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Wood Adhesives

- Molding

- Insulation

- Laminates

- Paper Impregnation

- Coatings

- Refractory Materials

- Friction Material

- Rubber & Tire

- Electronics

- Abrasives

By End Use Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Building & Construction

- Automotive

- Electrical & Electronics

- Furniture

- Other End Uses

U.S. Phenolic Resins Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.83 Billion |

| Market Size in 2026 | USD 1.89 Billion |

| Revenue Forecast by 2034 | USD 2.51 Billion |

| CAGR | 3.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Volume, Kilotons; Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization |

|

FAQ's

The market size was valued at USD 1.83 billion in 2025 and is projected to grow to USD 2.51 billion by 2034.

The market is projected to register a CAGR of 3.5% during the forecast period.

A few of the key players in the market are Arclin Inc., Ashland Inc., Bakelite Synthetics, Eastman Chemical Company, Hexcel Corp., Hexion, Kraton Corporation, Olympic Panel Products LLC, Owens Corning, and SI Group.

The novolac segment accounted for 49.09% revenue share in 2025.

The molding segment is expected to witness the highest CAGR of 4.6% during the forecast period.

Download Sample Report of U.S. Phenolic Resins Market

Please fill out the form to request a customized copy of the research report.