Veterinary Pharmacovigilance Market Size Report 2025-2034

REPORT DETAILS

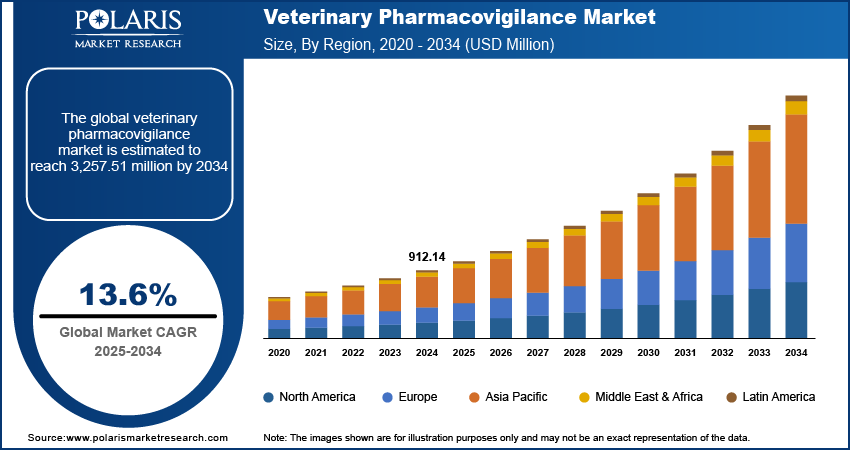

Veterinary Pharmacovigilance Market Summary

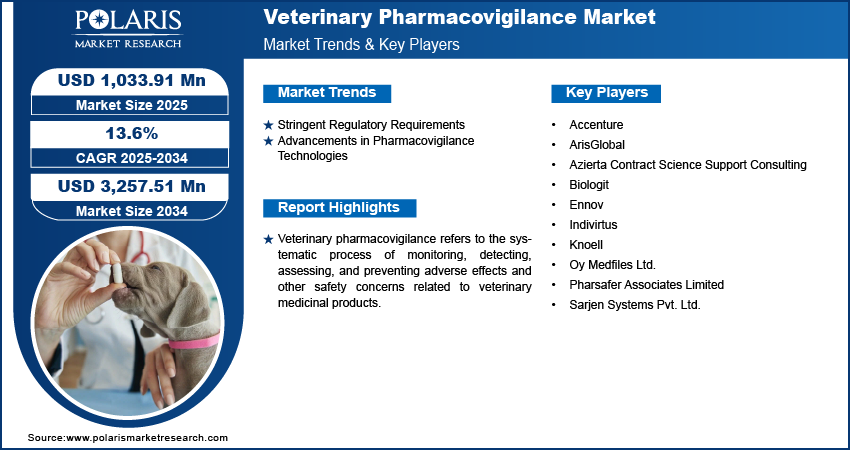

The global veterinary pharmacovigilance market size was valued at USD 912.14 million in 2024, exhibiting a CAGR of 13.6% from 2025 to 2034.

Market Statistics

Key Takeaways

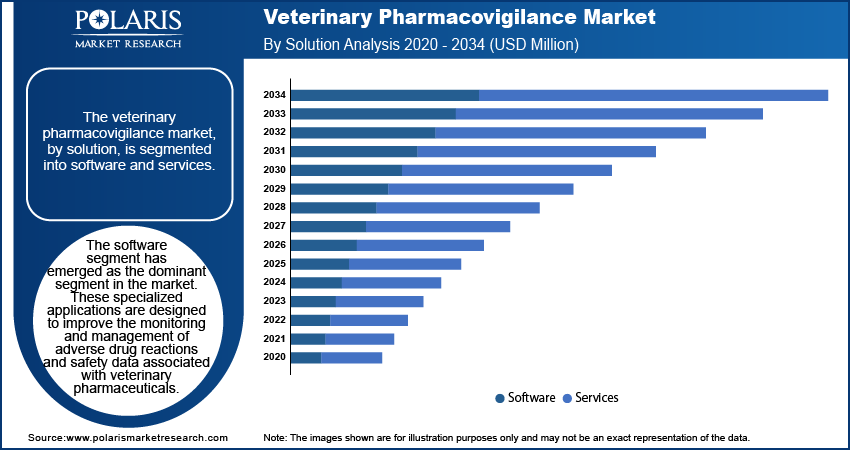

- Based on solution, the software segment dominated the revenue share in 2024. The software are designed to enhance the monitoring and management of adverse drug reactions and safety data associated with veterinary pharmaceuticals.

- By type, the in-house segment held the largest revenue share in 2024. In-house systems allow for greater control over processes, direct oversight of data, and the ability to tailor pharmacovigilance activities to specific organizational needs.

- In terms of product, the biologics segment is expected to register the highest growth rate during the forecast period. Veterinary biologics are increasingly utilized to prevent and treat various animal diseases.

- By animal type, the dog segment held the largest share in 2024, owing to the increasing adoption of dogs as companion animals, leading to heightened attention to their health and well-being.

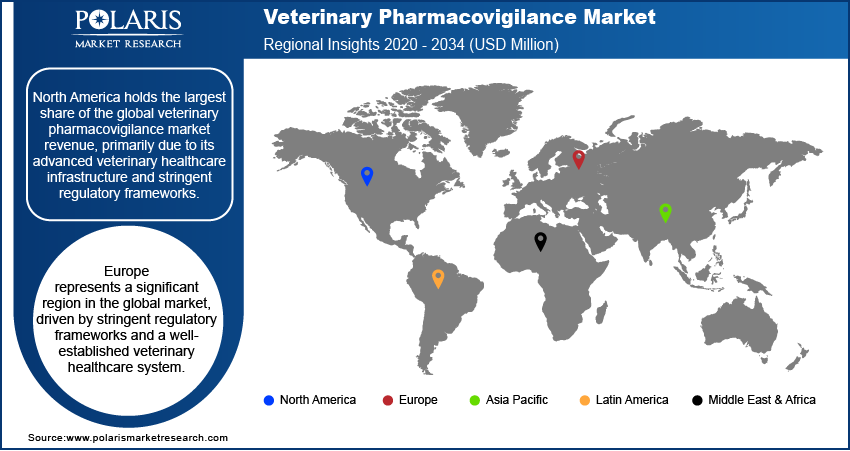

- North America held the largest share of the global veterinary pharmacovigilance market in 2024, primarily due to its advanced veterinary healthcare infrastructure and stringent regulatory frameworks.

- The industry growth in Europe is driven by stringent regulatory frameworks and a well-established veterinary healthcare system.

Industry Dynamics

- Growing awareness among veterinarians and pet owners regarding the potential side effects of veterinary drugs is fueling demand for robust pharmacovigilance systems.

- Regulatory bodies such as the European Medicines Agency (EMA) and the U.S. Food and Drug Administration (FDA) are enforcing stricter guidelines, compelling pharmaceutical companies to enhance their veterinary pharmacovigilance capabilities.

- The increasing digitalization of pharmacovigilance processes and growing investments in veterinary healthcare infrastructure are expected to support the market's long-term growth during the forecast period.

- Lack of standardized reporting systems hinders the market growth.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

AI Impact on Veterinary Pharmacovigilance Market

- In the veterinary pharmacovigilance industry, AI is used to accelerate innovation and safeguard public health and animal welfare by improving drug safety oversight.

- AI tools analyze vast datasets of molecular structures, pharmacokinetics, and pharmacodynamics to predict promising drug candidates.

- The technology enables tailored treatment regimens based on breed, age, species, and genetic markers. It leads to effective dosing and reduced risk of adverse side effects.

The veterinary pharmacovigilance market involves the monitoring, detection, assessment, and prevention of adverse effects or any other drug-related concerns associated with veterinary medicinal products. This industry is driven by stringent regulatory frameworks established by government agencies to ensure the safety and efficacy of veterinary drugs. The increasing adoption of companion animals and the rising prevalence of zoonotic diseases further contribute to industry growth. Additionally, advancements in pharmacovigilance technologies, such as artificial intelligence (AI) and data analytics, are improving the efficiency of adverse event reporting and risk assessment in veterinary medicine.

Technological advancements are revolutionizing pharmacovigilance processes. The technologies are used to improve the efficiency and accuracy of adverse event reporting and data analysis in veterinary medicine. The adoption of electronic reporting systems and data analytics tools enables more effective monitoring of adverse events, facilitating the early identification of potential safety issues. These technological innovations are pivotal in strengthening pharmacovigilance frameworks, thereby supporting the industry development.

Drivers and Opportunities

Stringent Regulatory Requirements

Regulatory organizations are enforcing stringent requirements aimed at ensuring the safety and efficacy of veterinary medicinal products. Government agencies worldwide have implemented comprehensive guidelines mandating the monitoring and reporting of adverse drug reactions in animals. In 2023, the European Medicines Agency (EMA) introduced guidelines on veterinary good pharmacovigilance practices. They emphasize continuous signal management and the maintenance of a pharmacovigilance master file by marketing authorization holders. Such regulatory requirements compel pharmaceutical companies to enhance their pharmacovigilance systems, thereby driving market demand.

Increasing Prevalence of Adverse Drug Events

The rising incidence of adverse drug events (ADEs) in animals propels the demand for robust pharmacovigilance systems to monitor and mitigate potential risks associated with veterinary medicinal products. A narrative review published in Frontiers in Veterinary Science in 2024 highlighted that approximately 50% of veterinary medications marketed in regions of Asia and Africa are considered substandard and falsified. It is leading to drug toxicity, drug resistance development, and animal fatalities. This alarming statistic underscores the critical need for effective pharmacovigilance practices to ensure animal safety and maintain public trust in veterinary healthcare.

Source: Polaris Market Research Analysis

Segmental Insights

Solution Analysis

The segmentation, by solution, includes software and services. The software segment dominated the revenue share in 2024. These specialized applications are designed to improve the monitoring and management of adverse drug reactions and safety data associated with veterinary pharmaceuticals. The software significantly improves the efficiency and accuracy of pharmacovigilance activities by streamlining data collection, analysis, and reporting processes. Also, there is a growing integration of AI and machine learning technologies. The use of such technologies enables predictive analytics for the early detection of potential safety issues. Additionally, the adoption of cloud-based platforms is on the rise. It offers real-time data access and facilitates seamless collaboration among stakeholders, thereby strengthening the overall effectiveness of veterinary pharmacovigilance efforts.

The services segment is expected to record the highest growth rate during the forecast period. This segment encompasses comprehensive offerings such as data collection, assessment, and management of adverse drug reactions in animals. The increasing complexity of veterinary pharmaceuticals and the necessity for specialized expertise have led many pharmaceutical companies and animal health organizations to outsource these critical functions. Recent developments in this sector include the incorporation of advanced technologies such as AI and data analytics to enhance monitoring efficiency and accuracy. Moreover, there is a concerted effort to harmonize international standards and regulations within the industry. The growing demand for real-time monitoring and the expansion of service portfolios to cover a broader range of animal species reflect the evolving landscape of animal healthcare and pharmaceutical safety.

Type Analysis

The segmentation, by type, includes in-house and contract outsourcing. The in-house segment held the largest revenue share in 2024. These services involve pharmaceutical companies and animal health organizations. They manage their pharmacovigilance activities internally, from data collection and adverse event reporting to regulatory compliance. This approach allows for greater control over processes, direct oversight of data, and the ability to tailor pharmacovigilance activities to specific organizational needs. Companies investing in in-house teams often focus on developing specialized expertise and integrating advanced data management systems to enhance the efficiency of their pharmacovigilance operations.

The contract outsourcing segment is projected to experience the highest growth rate during 2025–2034. The increasing complexity of regulatory requirements and the need for specialized expertise prompt many companies to outsource their pharmacovigilance activities to external service providers. Contract Research Organizations (CROs) offer comprehensive services, including data collection, analysis, and regulatory submissions, providing cost-effective solutions and access to specialized knowledge. The flexibility and scalability offered by outsourcing allow companies to adapt to changing regulatory landscapes and focus on their core competencies.

Product Analysis

The segmentation, by product, includes biologics, anti-infective, and other product. The anti-infectives segment held the largest revenue share in 2024. These products, including antimicrobials and treatments for external and internal parasites, are essential in preventing and treating infections in animals. Their widespread use leads to a higher volume of pharmacovigilance reports. A 2021 post-marketing surveillance review by the French Agency for Food, Environmental, and Occupational Health and Safety (ANSES) identified external parasites, antimicrobials, internal parasites, and ectoparasiticides as among the most frequently reported categories in pharmacovigilance reports.

The biologics segment is expected to register the highest growth rate during the forecast period. Veterinary biologics, such as vaccines and monoclonal antibodies along with veterinary antibiotics, are increasingly utilized to prevent and treat various animal diseases. The rising demand for these advanced therapies necessitates stringent pharmacovigilance practices to monitor their safety and efficacy. This trend reflects a broader shift toward innovative treatments in veterinary medicine, highlighting the importance of robust pharmacovigilance systems to ensure animal health and safety.

Animal Type Analysis

The veterinary pharmacovigilance market, by animal type, is segmented into dogs, cats, and other animal types. The dog segment held the largest revenue share in 2024. This dominance is attributed to the increasing adoption of dogs as companion animals, leading to rising attention to their health and well-being. As a result, there is a substantial demand for dog vaccines and medicines, necessitating rigorous pharmacovigilance practices to monitor drug safety and efficacy. The trend of humanizing pets has further intensified the focus on canine health. It prompts pharmaceutical companies to invest in comprehensive pharmacovigilance systems tailored to this segment.

The cat segment is expected to register the highest growth rate during the forecast period. This surge is driven by a notable increase in cat ownership, as more individuals and families choose cats as pets. The rising popularity of cats has led to a greater need for specialized veterinary products and treatments, thereby amplifying the importance of pharmacovigilance in this segment. Veterinary pharmaceutical companies are responding to this trend by enhancing their pharmacovigilance activities to ensure the safety and effectiveness of products designed for feline health.

Source: Polaris Market Research Analysis

Regional Insights

By region, the study provides insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America veterinary pharmacovigilance market held the largest share in 2024, primarily due to its advanced veterinary healthcare infrastructure and stringent regulatory frameworks. The region's high awareness of animal health and safety, coupled with significant investments in veterinary pharmacovigilance systems, contributes to its dominance. Furthermore, the presence of major pharmaceutical companies and contract research organizations (CROs) specializing in pharmacovigilance services enhances the region's capacity to monitor and ensure drug safety effectively.

The Europe veterinary pharmacovigilance market holds a significant revenue share. The regional market expansion is driven by stringent regulatory frameworks and a well-established veterinary healthcare system. The European Medicines Agency (EMA) plays a pivotal role in overseeing pharmacovigilance activities, ensuring the safety and efficacy of veterinary medicinal products. The region's commitment to animal health and welfare, coupled with robust reporting systems, contributes to the veterinary pharmacovigilance market expansion in Europe.

The Asia Pacific veterinary pharmacovigilance market is experiencing rapid growth, propelled by increasing awareness of animal health and the expansion of the veterinary pharmaceutical industry. Countries such as China, Japan, and India are witnessing a surge in demand for veterinary services, leading to rising focus on monitoring adverse drug reactions in animals. The adoption of advanced technologies and the establishment of regulatory frameworks are enhancing pharmacovigilance activities in the region. Additionally, the growing pet ownership and livestock industries contribute to the need for effective pharmacovigilance systems to ensure the safety of veterinary medicinal products.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The veterinary pharmacovigilance market comprises several active companies dedicated to ensuring the safety and efficacy of veterinary medicinal products. The competitive landscape is characterized by a focus on innovation and technological integration. Companies are increasingly adopting advanced technologies, such as AI and machine learning, to enhance data analysis and signal detection capabilities. Additionally, there is a growing emphasis on expanding service portfolios to cater to a broader range of animal species and therapeutic areas. Collaborations and partnerships among these companies are also prevalent, aiming to harmonize international standards and regulations within the industry. This dynamic environment underscores the commitment to advancing animal healthcare and pharmaceutical safety.

A few notable industry players are Accenture, ArisGlobal, Azierta Contract Science Support Consulting, Biologit, Ennov, Indivirtus, Knoell, Oy Medfiles Ltd., Pharsafer Associates Limited, and Sarjen Systems Pvt. Ltd.

Key Companies

- Accenture

- ArisGlobal

- Azierta Contract Science Support Consulting

- Biologit

- Ennov

- Indivirtus

- Knoell

- Oy Medfiles Ltd.

- Pharsafer Associates Limited

- Sarjen Systems Pvt. Ltd.

Veterinary Pharmacovigilance Industry Developments

- February 2025: Merck Animal Health’s injectable BRAVECTO (fluralaner) received the 2024 Best New Companion Animal Product award from S&P Global Animal Health. The parasiticide delivers up to 12 months of flea and tick protection for dogs with a single injection. Approved in more than 30 countries (excluding the U.S. as of February 2025), it provides continuous coverage and helps overcome compliance challenges associated with monthly dosing. Ongoing development and post-market monitoring of BRAVECTO incorporate veterinary pharmacovigilance to maintain product safety and effectiveness.

Market Segmentation

By Solution Outlook (Revenue – USD Million, 2020–2034)

- Software

- Services

By Type Outlook (Revenue – USD Million, 2020–2034)

- In-house

- Contract Outsourcing

By Product Outlook (Revenue – USD Million, 2020–2034)

- Biologics

- Anti-Infective

- Other Product

By Animal Type Outlook (Revenue – USD Million, 2020–2034)

- Dogs

- Cats

- Other Animal Types

By Regional Outlook (Revenue – USD Million, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 912.14 million |

| Market Size in 2025 | USD 1,033.91 million |

| Revenue Forecast by 2034 | USD 3,257.51 million |

| CAGR | 13.6% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Veterinary Pharmacovigilance Market FAQ's

The market size was valued at USD 912.14 million in 2024 and is projected to grow to USD 3,257.51 million by 2034.

The market is projected to register a CAGR of 13.6% during the forecast period.

North America held the largest share of the market in 2024.

The market comprises several active companies dedicated to ensuring the safety and efficacy of veterinary medicinal products. A few notable companies are Accenture, ArisGlobal, Azierta Contract Science Support Consulting, Biologit, Ennov, Indivirtus, Knoell, Oy Medfiles Ltd., Pharsafer Associates Limited, and Sarjen Systems Pvt. Ltd.

The software segment dominated the market share in 2024.

Veterinary pharmacovigilance refers to the monitoring, detection, assessment, and prevention of adverse events and other safety-related issues associated with veterinary medicinal products.

Download Sample Report of Veterinary Pharmacovigilance Market

Please fill out the form to request a customized copy of the research report.