Water Treatment Chemicals Market Size, Share, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Water Treatment Chemicals Market Summary

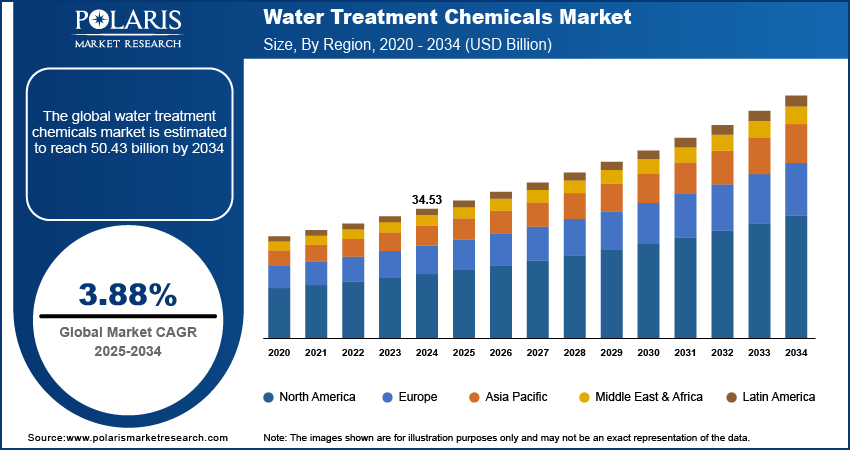

The global water treatment chemicals market size was valued at USD 35.70 billion in 2025. The market is projected to grow at a CAGR of 3.88% during 2026 to 2034. Key factors driving demand for water treatment chemicals include rapid industrialization and urbanization, increasing water scarcity, and stringent environmental regulations.

Market Statistics

Key Takeaways

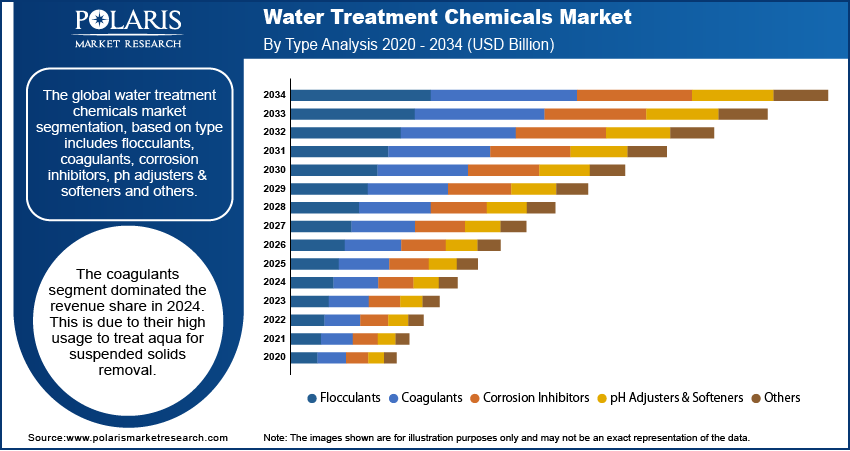

- The coagulants segment dominated the revenue share of 39.8% in 2025. This is due to their high usage to treat aqua for suspended solids removal.

- The industrial segment dominated the global market share of 45.7% in 2025 due to greater aqua treatment in industries such as chemical, food and beverages, and mining.

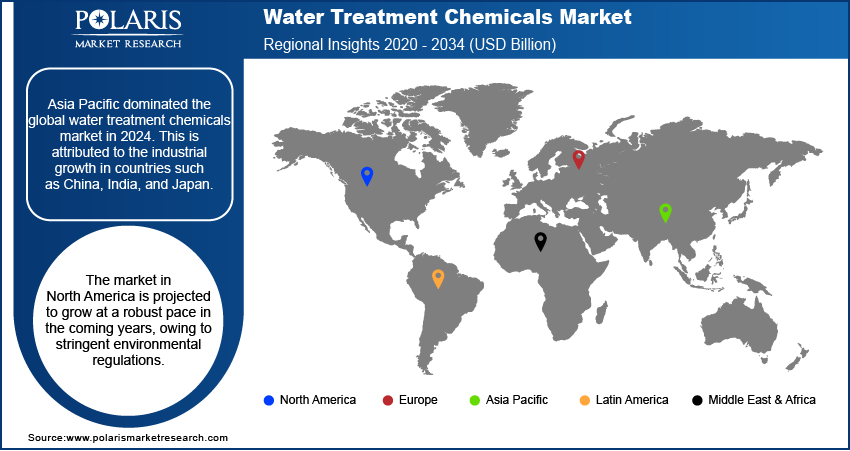

- Asia Pacific dominated the global water treatment chemicals market by 43.55% share in 2025. This is attributed to the industrial growth in countries such as China, India, and Japan.

- The market in North America is projected to grow at a robust pace at 4.5% in the coming years, owing to stringent environmental regulations.

- The flocculants segment is the fastest growing, with a CAGR of 5.1% from 2026 to 2034. This is because of better particle aggregation and water clarity.

- The municipal segment contributed for over 43.2% of the revenue share in 2025. The share is because of increasing demand for clean water and infrastructure investment.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

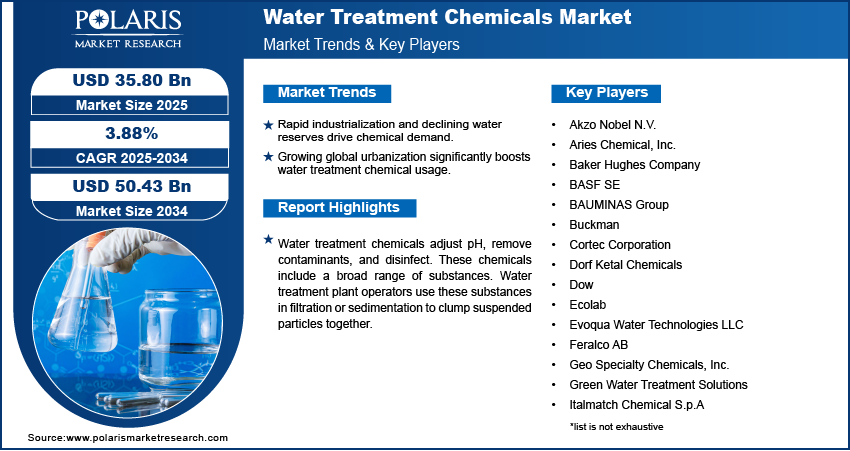

- Economic growth in developing countries, rising industrialization, and declining water reserves are leading to high demand for water treatment chemicals.

- The growing urbanization across the globe is also increasing the demand for water treatment chemicals.

- Technological advancements and initiatives & regulations introduced by governments are creating a lucrative market opportunity.

- Alternative water treatment technologies may hamper the market growth.

Water Treatment Chemicals Market Definition

Water treatment chemicals are chemical substances such as coagulants, flocculants, disinfectants, and corrosion inhibitors used to remove contaminants, pathogens, and impurities from water. They improve the quality and efficiency of water treatment in order to make it fit for drinking, industrial use and discharge into the environment.

Source: Polaris Market Research Analysis

Water treatment chemicals adjust pH, remove contaminants, and disinfect. These chemicals include a broad range of substances. Water treatment plant operators use these substances in filtration or sedimentation to clump suspended particles together. These chemicals eliminate pathogens, including bacteria and viruses, to ensure safe drinking water or process water. The growing demand for safe and freshwater for residential applications has increased the requirement for water treatment chemicals. Different chemicals are used during water treatment. These chemicals include flocculants, corrosion inhibitors, coagulants, biocides & disinfectants, and deforming agents, among others.

These chemicals remove minerals, solids, algae, and other microbes during the treatment process. Growing urbanization and economic development have increased the demand for clean water treatment chemicals across the globe. Rising environmental regulations, scarcity of freshwater resources, and growth in industrial water consumption have increased the adoption of water treatment chemicals. The different kinds of corrosion inhibitors include precipitation-inducing inhibitors, passivity inhibitors, cathodic inhibitors, organic inhibitors, and volatile corrosion inhibitors.

Industry Dynamics

Growth Drivers

Economic growth in developing countries, rising industrialization, and declining water reserves have resulted in greater demand for water treatment chemicals. Industries such as oil and gas, power generation, mining, and paper and pulp, are heavily adoptiong water treatment chemicals. The growing population and increasing focus on river cleaning programs, especially in emerging nations such as India is propelling the demand for water treatment chemicals. The growing diseases due to poor water quality is also encouraging municipalities to use these chemicals. Moreover, technological advancements and initiatives & regulations introduced by governments have strengthened the water treatment chemical market.

What is the impact of regulations or standards on the water treatment chemicals market?

The government and private organizations are imposing stringent regulations on the water treatment chemicals market. The evolving regulatory landscape across the world is attributed to increasing environmental concerns and public health priorities. Further, there is an increasing focus on industrial compliance. The regulations and standards vary as per the water applications and regions. The following table includes key regulations and standards influencing the industry:

| Region/Country | Regulatory Authority/Law | Key Points | Impact on Water Treatment Chemicals Market |

| U.S. | U.S. Environmental Protection Agency (EPA) – Effluent Guidelines | Sets limits on the discharge of industrial wastewater under the Clean Water Act | Fuels the demand for advanced water treatment chemicals to adhere to discharge standards |

| EPA – PFAS Regulations | Puts limits on PFAS (polyfluoroalkyl substances) in drinking water | Accelerates the development of PFAS removal chemicals and technologies | |

| European Union (EU) | EU Water Framework Directive | Aims for “good water status” in surface and groundwater | Promotion of sustainable water treatment practices |

| REACH Regulation | Requires registration, evaluation, authorization, and restriction of chemicals | Ensures compliance with safety and environmental standards | |

| France | PFAS Legislation | Ban on the manufacturing, imports, and sale of PFAS-containing products starting in 2026 | Drives demand for PFAS-free water treatment chemicals |

| India | Central Pollution Control Board (CPCB) – BIS IS 10500:2012 | Quality standards on drinking water defining permissible chemical limits | Provides guidance on the selection of safe and effective water treatment chemicals |

| CPCB – Effluent Discharge Standards (Water Act 1974) | Regulates industrial effluent discharge | Requires the use of compliant treatment chemicals in industrial applications | |

| State Pollution Control Boards (SPCBs) | Implement and monitor water quality and water treatment chemical use | Enforces adherence at the regional and state levels | |

| Chemicals (Management & Safety) Rules | Align with international chemical safety standards (similar to EU REACH) | Promotes registration of water treatment chemicals and safer chemical use |

Source: Polaris Market Research Analysis

Manufacturers focus on innovating and developing efficient and eco-friendly water treatment chemicals to comply with these stringent regulatory standards. Further, the regulatory landscape varies across regions, necessitating customized approaches to market strategies and compliance in different jurisdictions. Thus, upsurging demand for sustainable and compliant water treatment chemicals across various sectors propel the industry expansion.

Source: Polaris Market Research Analysis

The market is primarily segmented on the basis of type, end use, and region.

| By Type | By End Use | By Region |

|

|

|

Source: Polaris Market Research Analysis

Insight by Type

Based on type, the market is segmented into flocculants, coagulants, corrosion inhibitors, pH adjusters & softeners, and others. The coagulants segment dominated the revenue share of 39.8% in 2025, due to its ability in removing suspended solids, organic matter, and pollutants from contaminated water sourcesis. Coagulants are added to the solution to accomplish charge neutralization. Governments strict regulations and water quality standards further contributed to the segment's dominance.

Source: Polaris Market Research Analysis

Type Analysis

| Type | Function | Use Areas | Demand Drivers | Business Relevance |

| Coagulants | Remove suspended solids by charge neutralization | Municipal, industrial wastewater | Regulations, dirty water levels | High usage, steady demand |

| Flocculants | Form larger particles for easy removal | Mining, wastewater, paper & pulp | Need for better clarity | Growing industrial demand |

| Biocides | Kill bacteria and control microbes | Cooling systems, oil & gas | Hygiene needs, contamination | Important for system safety |

| Corrosion Inhibitors | Protect pipes and equipment from corrosion | Power, chemical, oil & gas | Maintenance cost reduction | Needed for longer equipment life |

Source: Polaris Market Research Analysis

Insight by End Use

The end use industry segment has been divided into municipal, industrial, and others. The industrial segment dominated the global market share of 45.7% in 2025 due to water treatment needs in industries such as chemical, food and beverages, mining, power, and paper and pulp, among others. The increasing industrialization in developing countries and the introduction of stringent safety regulations further supported the segment's growth. High wastewater generation from industrial sectors, scarcity of clean water, and technological advancements in the development of efficient treatment processes, contributed to segment's major revenue share.

Geographic Overview

Asia Pacific dominated the global water treatment chemicals market by 43.55% share in 2025. The industrial growth in countries such as China, India, and Japan and the growing population drove this region's growth. Increasing urbanization, expansion of international players in this region, and technological advancements are some of the other factors attributed to the region's dominance. Rising environmental concerns and stringent regulations regarding the treatment of water in developing countries of this regin offered a lucrative opportunities for the market.

The market in North America is projected to grow at a robust pace at 4.5% in the coming years. This is attributed to the stringent environmental regulations, urbanization and population growth, and aging infrastructure. The high awarness about water-borne disease in the region is also leading to adoption of water treatment chemicals. The presence of high numbers of swimming pools and traning centers in the region are further propellin the demand for water treatment chemicals. Moreover, high government spending on people's health in the region is leading to the demand for water cure chemicals.

Source: Polaris Market Research Analysis

Competitive Landscape

The leading players in the water treatment chemicals market include Akzo Nobel N.V., Aries Chemical, Inc. Baker Hughes Company, BASF SE, BAUMINAS Group, Buckman, Cortec Corporation, Dorf Ketal Chemicals, Dow, Ecolab, Evoqua Water Technologies LLC, Feralco AB, Geo Specialty Chemicals, Inc., Green Water Treatment Solutions, Italmatch Chemical S.p.A, Kemira, Kurita Europe GmbH, LANXESS, Lonza, SNF CHINA FLOCCULANT CO., LTD., Solenis, Somicon ME FZC, and Suez S.A. These players are expanding their presence across various geographies and entering new markets in developing regions to expand their customer base and strengthen their presence in the market. The companies are also introducing new innovative products in the market to cater to the growing consumer demands.

Industry Developments

- April 2026, Vipul Organics entered the water treatment market through its AdiMem membrane unit. It targets around 25% revenue contribution from this segment within three years. Source: business-standard.com

- December 2025, Ecolab acquired Ovivo’s Electronics Ultra-Pure Water business for about USD 1.8 billion, adding advanced ultra-pure water technologies to support semiconductor and high-tech industry water management needs. Source: ecolab.com

- November 2025, Solenis completed the acquisition of NCH Corporation, expanding its global footprint and strengthening its water treatment and industrial solutions portfolio, while enabling cross-selling across sustainable and digital solutions. Source: prnewswire.com

- March 2025, DuPont Water Solutions launched WAVE PRO, an advanced online modeling tool for ultrafiltration (UF) water treatment applications, including drinking water, industrial water, wastewater, and seawater desalination. Source: dupont.com

- March 2025, Whitewater Management acquired Orion Water Solutions, strengthening its wastewater treatment capabilities and supporting growth through its production chemical company, Catalyst Production Services. Source: prnewswire.com

Future of Water Treatment Chemicals Market

The market will grow due to increasing water reuse and desalination projects. Demand for eco-friendly and low-toxicity chemicals is rising. Digital water management systems are getting adopted in industries. Regulations are becoming stricter in regions. Overall, the market will continue to grow steadily with concentration on sustainability and compliance.

Water Treatment Chemicals Market Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 35.70 billion |

| Market size value in 2026 | USD 36.95 billion |

| Revenue forecast in 2034 | USD 49.93 billion |

| CAGR | 3.88% from 2026 - 2034 |

| Base year | 2025 |

| Historical data | 2021 - 2024 |

| Forecast period | 2026 - 2034 |

| Quantitative units | Revenue in USD Billion and CAGR from 2026 - 2034 |

| Segments covered |

|

| Regional scope |

|

| Key Companies | Akzo Nobel N.V., Aries Chemical, Inc. Baker Hughes Company, BASF SE, BAUMINAS Group, Buckman, Cortec Corporation, Dorf Ketal Chemicals, Dow, Ecolab, Evoqua Water Technologies LLC, Feralco AB, Geo Specialty Chemicals, Inc., Green Water Treatment Solutions, Italmatch Chemical S.p.A, Kemira, Kurita Europe GmbH, LANXESS, Lonza, SNF CHINA FLOCCULANT CO., LTD., Solenis, Somicon ME FZC, and Suez S.A. |

Source: Polaris Market Research Analysis

Water Treatment Chemicals Market FAQ's

The global market size was valued at USD 35.70 billion in 2025 and is projected to grow to USD 49.93 billion by 2034.

The global market is projected to register a CAGR of 3.88% during the forecast period.

Asia Pacific dominated the global water treatment chemicals market by 43.55% share in 2025.

A few of the key players in the market are Akzo Nobel N.V., Aries Chemical, Inc. Baker Hughes Company, BASF SE, BAUMINAS Group, Buckman, Cortec Corporation, Dorf Ketal Chemicals, Dow, Ecolab, Evoqua Water Technologies LLC, Feralco AB, Geo Specialty Chemicals, Inc., Green Water Treatment Solutions, Italmatch Chemical S.p.A, Kemira, Kurita Europe GmbH, LANXESS, Lonza, SNF CHINA FLOCCULANT CO., LTD., Solenis, Somicon ME FZC, and Suez S.A.

The coagulants segment dominated the revenue share of 39.8% in 2025

Main types include coagulants, flocculants, disinfectants, and corrosion inhibitors. Each has a different role in cleaning water.

They are used in drinking water plants, industries, wastewater treatment, and power plants.

Industrial use is for factories and plants. Municipal use is for public water supply and sewage treatment.

Download Sample Report of Water Treatment Chemicals Market

Please fill out the form to request a customized copy of the research report.