Drinking Water Adsorbents Market Size, Share & Growth Report, 2025-2034

REPORT DETAILS

Drinking Water Adsorbents Market Summary

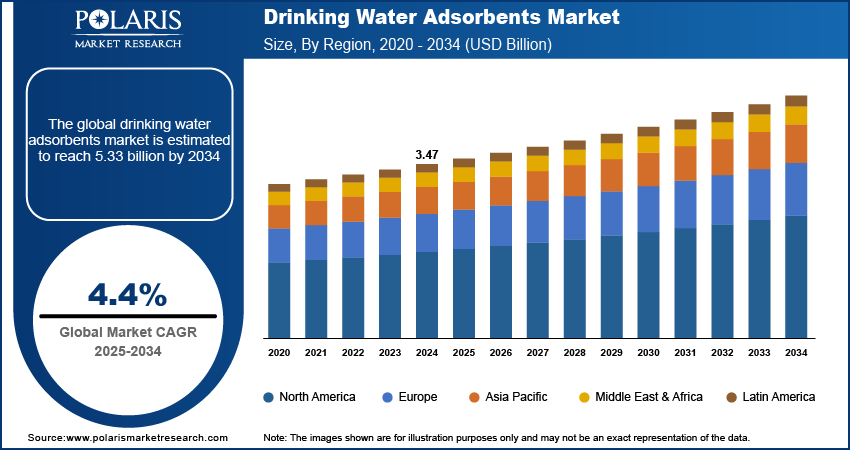

The global drinking water adsorbents market size was valued at USD 3.47 billion in 2024, growing at a CAGR of 4.4% from 2025 to 2034. Stringent regulations and rising water contamination coupled with expansion of municipal and industrial water treatment infrastructure is propelling the market growth.

Market Statistics

Key Takeaways

- Activated carbon led the market in 2024 due to its superior adsorption capacity, efficiency in the removal of organic substances, and extensive application across domestic and industrial water purification systems.

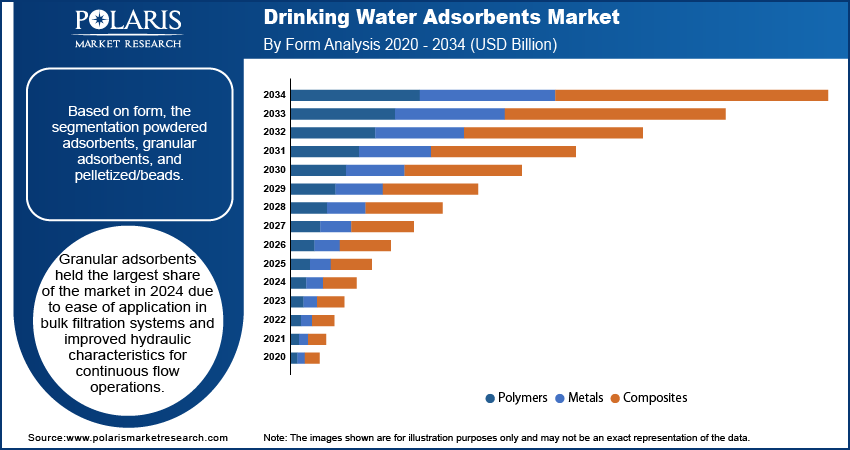

- Powdered adsorbents held the dominating share in 2024, due to its high surface area and rapid adsorption kinetics, rendering them ideal for batch treatment and niche industrial applications.

- North America dominated the market in 2024, due to consistent investments in municipal water treatment facilities to address increased demand for clean and safe water.

- The U.S. dominated the North American market, driven by strict regulatory policies from institutions like the EPA to ensure better water quality.

- Asia Pacific projected to grow rapidly during the forecast period, fueled by swift urbanization, industrialization, and population growth in the region.

- India led the market in Asia Pacific, fueled by the accelerating growth of water treatment and recycling facilities as well as increasing water requirements and pollution issues.

- Key players operating in the market include Arkema S.A., BASF SE, Cabot Corporation, Calgon Carbon Corporation, CycloPure Inc., DuPont de Nemours, Inc., Evoqua Water Technologies LLC, GEH Wasserchemie GmbH & Co. KG, KMI Zeolite, Inc., Kuraray Co., Ltd., Lenntech B.V., Purolite Corporation, TIGG LLC, Thermax Limited, and The Dow Chemical Company.

Industry Dynamics

- Strict regulations and increasing water pollution are fueling demand for high-performance drinking water adsorbents for residential, municipal, and industrial use.

- Investment in municipal and industrial water treatment plants is increasing adoption of high-performing adsorbents.

- High price of high-tech adsorbents is a major deterrent, especially for small municipalities and industrial facilities.

- Implementation of AI and machine learning solutions offers opportunities for growth through process optimization, efficiency gain, and reduced operational expenses.

The drinking water adsorbents market comprises advanced materials used to eliminate impurities, contaminants, and pollutants from water to provide secure and clean drinking water in residential, commercial, and industrial sectors. Adsorbents are extensively applied in heavy metal removal, decolorization, and purification owing to their high surface area, reusability, and chemical stability. Improvements in activated carbon, biochar, and synthetic adsorbent technologies are becoming more efficient, selective, and cost-effective.

Increasing demand for safe drinking water is boosting the need for water absorbents across home, municipal governments, and industrial plants. Organizations and customers are increasingly looking for effective solutions to counter water contaminants. Advanced technologies are used to preserve water quality in an efficient manner while satisfying changing health and hygiene requirements.

Source: Polaris Market Research Analysis

Innovations in technology such as adsorption, ion exchange, and modular systems to efficiently remove heavy metals, organic matter, and other contaminants are fueling the market growth. In August 2025, Saltworks Technologies launched Xtract, a modular ion exchange and adsorption system for the selective removal and recovery of ions from industrial water to market. Xtract is designed for underserved markets that tend to need breakthrough curve testing for proper costing and sizing. These developments enhance treatment effectiveness and complement sustainable water management strategies.

Drivers & Opportunities

Stringent Regulations and Rising Water Contamination: The growing occurrence of water pollution, coupled with stringent regulatory requirements, is fueling market growth. According to the World Health Organization, in 2022, approximately 1.7 billion people globally relied on drinking water sources contaminated with faces, highlighting the critical need for safe water solutions. This surge in need is fueling the requirement for safe water solutions.

Expansion of Municipal and Industrial Water Treatment Infrastructure: Drinking water adsorbents are witnessing high demand due to rapid expansion of municipal water treatment plants and industrial solutions. In August 2025, Singapore's Public Utilities Board launched the third stage of expansion for the Changi Water Reclamation Plant, the world's largest wastewater treatment plant. Large-scale infrastructure developments are fueling growth of next-generation water treatment technologies to provide safe, high-quality water to communities and industries.

Source: Polaris Market Research Analysis

Segmental Insights

By Product

On the basis of type of product, the market for drinking water adsorbents is divided into zeolite, clay, activated alumina, activated carbon, manganese oxide, cellulose, and others. Activated carbon held the highest market share in 2024 due to its extremely high adsorption capacity, excellent capability to adsorb organic compounds, and extensive applications both in home water treatment and industrial water treatment systems.

Zeolite is anticipated to experience rapid growth throughout the forecast period due to its effectiveness in the removal of heavy metals and regeneration processes.

By Form

Based on form, the market is segmented into powdered adsorbents, granular adsorbents, and pelletized/beads. Granular adsorbents held the largest share of the market in 2024 due to ease of application in bulk filtration systems and improved hydraulic characteristics for continuous flow operations.

Powdered adsorbents are anticipated to experience fastest growth due to their large surface area and rapid adsorption rates, which are compatible with batch treatment and niche industrial uses.

By End-User

On the basis of end-user, the industry is divided into households, municipal authorities, and industrial facilities. Households dominated the market in 2024 due to growing concerns regarding safe drinking water and the implementation of point-of-use filtration systems.

Municipal authorities is anticipated grow at a rapid pace, driven by initiatives from governments to supply clean water, develop urban water infrastructure, and respond to regulatory requirements.

Source: Polaris Market Research Analysis

Regional Analysis

North America led the global drinking water adsorbents market, driven by continuous investments in municipal water treatment facilities in order to keep up with increasing demand for clean and safe water. Increasing public concern about such contaminants as lead, PFAS, and microplastics is encouraging municipalities and industries to invest in state-of-the-art adsorbent technology to provide protection for water safety.

The U.S. Drinking Water Adsorbents Market Overview

The U.S. dominated the market within North America, drive by aggressive regulatory policies from organizations such as the EPA forcing improvements in water quality. For example, in April 2024, PFAS initiated National Primary Drinking Water Regulation, which sets legally binding standards for six classes of per- and polyfluoroalkyl substances in public water supplies. The regulation is boosting demand for unique adsorbents with the ability to remove emerging contaminants in drinking water.

Asia Pacific Drinking Water Adsorbents Market Insights

Asia Pacific is expected to witness a swift growth rate during the forecast period, driven by rapid urbanization, industrialization, and population growth across the region. Governments in the region are investing heavily in programs aimed at increasing access to safe and clean water for rural and urban dwellers.

India Drinking Water Adsorbents Market Analysis

India is dominating the market in Asia Pacific, due to the rapid expansion of water treatment and recycling infrastructure along with rising water demand and contamination concerns. According to the International Trade Administration, India ranks as the 5th largest water and wastewater treatment industry worldwide, worth about USD 11 billion in 2024, expected to expand over USD 18 billion by 2026. This expansion highlights the robust demand for novel adsorbent technologies in municipal and industrial water treatment processes.

Europe Drinking Water Adsorbents Market Assessment

Europe held significant market share led by rigorous EU water quality regulations and environmental policy, which are compelling the adoption of upgraded and effective water treatment practices. Huge investments are undertaken to modernize old infrastructure and enhance water security. The European Investment Bank (EIB) committed USD 16 billion for the period of 2025 to 2027 to fund initiatives to safeguard and develop water resources in the European Union, propelling expansion of advanced adsorbent applications.

.png)

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

Global drinking water adsorbents market is extremely competitive with demands driven by technology and growing need for pure and safe drinking water in residential, commercial, and industrial spaces. Players are concentrating on enhanced adsorption efficiency, longer material life, and sustainable and cost-effective solutions to counter upcoming contaminants and tighter water quality regulations. New technologies in activated carbon, ion exchange resins, and zeolites are allowing enhanced removal of micropollutants, organic pollutants, and heavy metals from drinking water.

Key players in the global drinking water adsorbents market include Arkema S.A., BASF SE, Cabot Corporation, Calgon Carbon Corporation, CycloPure Inc., DuPont de Nemours, Inc., Evoqua Water Technologies LLC, GEH Wasserchemie GmbH & Co. KG, KMI Zeolite, Inc., Kuraray Co., Ltd., Lenntech B.V., Purolite Corporation, TIGG LLC, Thermax Limited, and The Dow Chemical Company.

Key Players

- Arkema S.A.

- BASF SE

- Cabot Corporation

- Calgon Carbon Corporation

- CycloPure, Inc.

- DuPont de Nemours, Inc.

- Evoqua Water Technologies LLC

- GEH Wasserchemie GmbH & Co. KG

- KMI Zeolite, Inc.

- Kuraray Co., Ltd.

- Lenntech B.V.

- Purolite Corporation

- The Dow Chemical Company

- Thermax Limited

- TIGG LLC

Drinking Water Adsorbents Industry Developments

In September 2024: Kemira acquired Norit’s UK reactivation business from Purton Carbons Limited, marking its entry into the activated carbon market for micropollutant removal. The deal includes the Purton reactivation facility, which regenerates spent granular and pelletized activated carbons for reuse.

In May 2024, Calgon Carbon Corporation, a subsidiary of Kuraray Co., Ltd., entered into an exclusive agreement to acquire the industrial reactivated carbon business of Sprint Environmental Services, LLC under an exclusive agreement. The acquisition comprises one reactivation plant situated outside of Houston, Texas, and 21 carbon reactivation service experts.

Drinking Water Adsorbents Market Segmentation

By Product Outlook (Revenue, USD Billion, 2020–2034)

- Zeolite

- Clay

- Activated Alumina

- Activated Carbon

- Manganese Oxide

- Cellulose

- Others

By Form Outlook (Revenue, USD Billion, 2020–2034)

- Powdered Adsorbents

- Granular Adsorbents

- Pelletized/Beads

By End-User Outlook (Revenue, USD Billion, 2020–2034)

- Households

- Municipal Authorities

- Industrial Facilities

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Drinking Water Adsorbents Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 3.47 Billion |

| Market Size in 2025 | USD 3.62 Billion |

| Revenue Forecast by 2034 | USD 5.33 Billion |

| CAGR | 4.4% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion, Volume in Kilotons and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Drinking Water Adsorbents Market FAQ's

The global market size was valued at USD 3.47 billion in 2024 and is projected to grow to USD 5.33 billion by 2034.

The global market is projected to register a CAGR of 4.4% during the forecast period.

North America dominated the market in 2024.

A few of the key players in the market are Arkema S.A., BASF SE, Cabot Corporation, Calgon Carbon Corporation, CycloPure Inc., DuPont de Nemours, Inc., Evoqua Water Technologies LLC, GEH Wasserchemie GmbH & Co. KG, KMI Zeolite, Inc., Kuraray Co., Ltd., Lenntech B.V., Purolite Corporation, TIGG LLC, Thermax Limited, and The Dow Chemical Company.

The activated carbon segment dominated the market revenue share in 2024.

The powdered adsorbents segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of Drinking Water Adsorbents Market

Please fill out the form to request a customized copy of the research report.