Wearable Sensors Market Size, Share, Growth | Report, 2026-2034

REPORT DETAILS

Wearable Sensors Market Summary

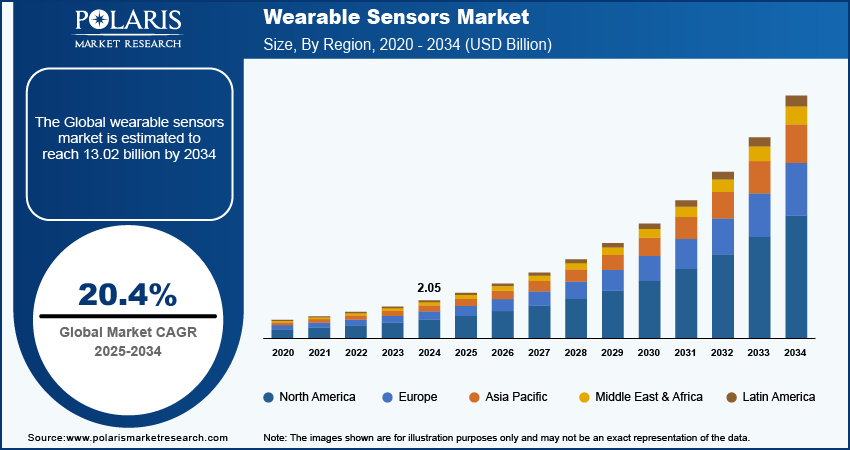

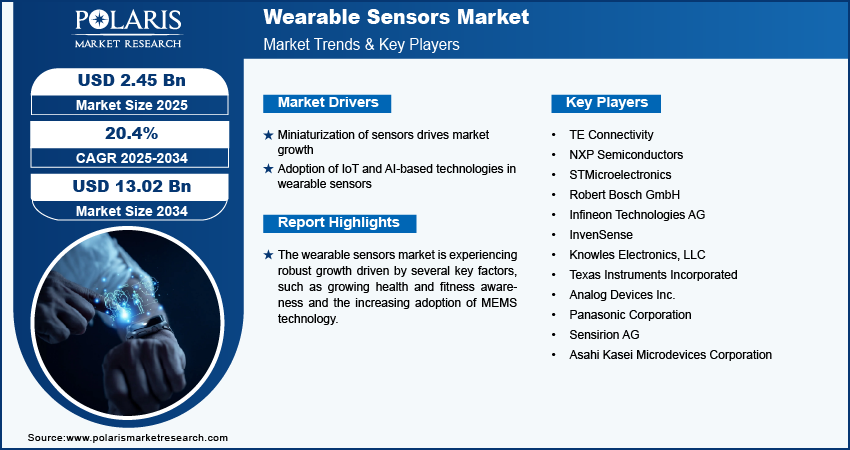

The wearable sensors market size was valued at USD 2.45 billion in 2025 and is projected exhibit a CAGR of 20.49% from 2026 to 2034. The wearable sensors demand is driven by several key factors, such as growing health and fitness awareness and the increasing adoption of MEMS technology.

Market Statistics

Key Takeaways

- North America led with a 35.90% revenue share in 2025. This is owing to increased awareness about consumer electronics and high adoption of IoT in the region.

- Asia Pacific is projected to register a 20.4% CAGR during the projection period. A growing user base and increasing disposable incomes are driving the regional market development.

- The accelerometers segment dominated with a 32.40% market share in 2025 due to its ability to accurately track physical activities.

- The fitness band segment is expected to experience significant growth at a 13.74% CAGR. This growth is driven by increasing demand from young consumers for affordable fitness trackers.

- The MEMS segment held a 40.20% market share in 2025. This is due to the low cost and high performance of these sensors.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The miniaturization of sensors is making wearable technology more appealing as devices can now perform complex functions. This, in turn, is fueling market growth.

- The rising adoption of IoT and AI-based technologies in wearable sensors is driving market development.

- Increased focus on the development of sensors for continuous monitoring of metabolic parameters is expected to create several market opportunities.

- Limited battery life and power constraints may limit market expansion.

AI Impact on Wearable Sensors Market

- AI helps in making progress in wearable technology through analysis of health and behavioral data in real time.

- AI allows for the identification of health risks based on anomalies in physiological signals and activity levels.

- It supports personalizing physical activities and wellness advice.

- AI improves the efficiency and effectiveness of the device’s functionality

Wearable sensors are advanced devices designed to monitor and collect data about an individual's physiological and biochemical parameters in real-time, often in a non-invasive manner. These sensors are integrated into various wearable technologies, such as smartwatches, fitness trackers, smart clothing, and even tattoo-like devices. They serve multiple purposes, including health monitoring, fitness tracking, and providing insights into personal well-being.

MEMS technology allows for the miniaturization of sensors, making them smaller, lighter, and more energy-efficient. This miniaturization enables seamless integration of these sensors into various wearable devices, enhancing their functionality and user comfort. The ongoing advancements in MEMS technology are expected to lead to the development of even more sophisticated and versatile sensors, further driving growth.

Source: Polaris Market Research Analysis

Rising disposable incomes, especially in developing economies, are a major factor driving the industry. Wearable sensors that monitor physical activity, heart rate, and sleep patterns align well with this trend. People are now able to invest in advanced health and fitness trackers due to their improved financial situations. This growing willingness to spend on advanced wearable technology is leading to a significant increase in revenue.

Market Dynamics

Miniaturization of Sensors

The miniaturization of sensors is transforming the wearable devices by allowing sophisticated monitoring capabilities to be incorporated into smaller designs. This advancement makes wearable technology more appealing as devices can now perform complex functions. The ability to include powerful sensors in smaller packages caters to consumers looking for efficient and user-friendly health and fitness monitoring solutions. Miniaturization allows for the development of compact, comfortable, and functional wearable devices like the OHSU-ADI smartwatch, a device developed in December 2022 by Oregon Health and Science University (OHSU) in collaboration with Analog Devices, Inc (ADI). This smartwatch serves as an early detector of suicidality or depression among teenagers, offering precise, continuous health data unobtrusively, making it suitable for everyday use by individuals of all ages, thereby driving growth.

Adoption of IoT and AI-Based Technologies in Wearable Sensors

The adoption of IoT (Internet of Things) technologies and AI (artificial intelligence) technologies in wearable sensors significantly boosts their demand by enhancing functionality, improving user experience, and expanding applications in healthcare and personal wellness. AI algorithms improve the accuracy of data collected by wearable sensors, enabling better detection of health issues. For instance, AI corrects inaccuracies in heart rate measurements, ensuring reliable data for users and healthcare providers. This reliability increases trust in wearable devices, encouraging more consumers to adopt them.

Emerging Technological Advancements in Wearable Sensors

| Company / Product | Technological advancement | What’s new vs. earlier wearables | Key use cases / benefits |

| Philips – next‑generation wearable biosensor & Healthdot / smartQare viQtor platform | Disposable, wireless chest‑worn biosensors tightly integrated with hospital monitoring platforms, providing continuous monitoring of heart and respiratory rate plus posture and activity. | Moves from wired Holter‑style monitoring to medical‑grade patches that require no cleaning or charging, stream data into clinical workflows, and support early deterioration detection. | Continuous inpatient and step‑down ward monitoring, earlier detection of patient deterioration, reduced staff workload, and support for hospital‑without‑walls models. |

| Medtronic – BioButton and Corsano multi‑parameter wearable with Vital Sync platform | Multi‑parameter, medical‑grade wearables (patch and wrist) capturing numerous vital signs continuously and connecting to cloud‑based Vital Sync remote patient‑monitoring software. | Extends conventional bedside monitoring to lightweight wearables that trend multiple vitals over time, enabling early detection of decline and remote surveillance across the hospital. | Hospital and home‑based remote patient monitoring, post‑discharge surveillance, and workflow optimization through centralized dashboards and alerts. |

| Philips – ePatch ECG sensor | Miniaturized, waterproof ECG patch that records continuous heart rhythm for several days, with AI‑assisted analysis of captured data. | Replaces bulky Holter monitors and wired electrodes with a small, discreet sensor usable during sleep, showering, and exercise, and couples it to AI algorithms for rapid arrhythmia analysis. | Long‑term ambulatory ECG monitoring, large‑scale atrial fibrillation detection studies, and improved patient comfort and adherence. |

| Bosch Sensortec – Smart Connected Sensors platform & ultra‑small MEMS accelerometers (BMA530/BMA580) for wearables | A full‑body motion‑tracking platform combining multiple wireless sensor nodes with embedded AI features, plus what Bosch calls the world’s smallest MEMS accelerometers optimized for wearables and hearables. | Shifts from single‑device motion sensing to multi‑node body tracking with onboard pattern recognition and qualitative movement feedback, while shrinking accelerometers for space‑constrained devices. | AI‑assisted rehab and fitness coaching, immersive gaming, and highly compact activity/voice‑detection sensing in smartwatches, fitness bands, and hearables. |

| WHOOP 4.0 platform (WHOOP) | Always‑on health‑performance wearable focusing on continuous strain, recovery, sleep, HRV and blood‑pressure insights, delivered through a subscription analytics model. | Moves consumer wearables beyond step counting to continuous physiological load and recovery analysis, with personalized coaching based on multi‑parameter sensor data and advanced analytics. | Athlete and lifestyle optimization, chronic stress and recovery tracking, and long‑term healthspan management using continuous sensor data and tailored recommendations. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Segment Analysis

By Sensor Type

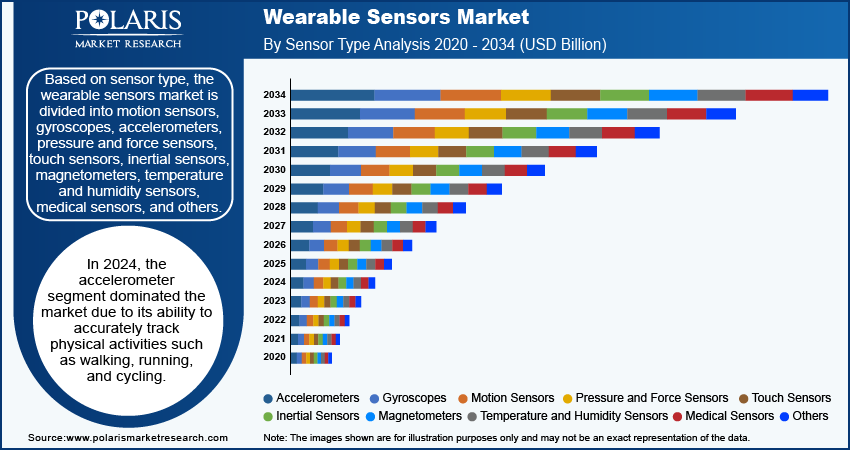

Based on sensor type, the market is segmented into motion sensors, gyroscopes, accelerometers, pressure and force sensors, touch sensors, inertial sensors, magnetometers, temperature and humidity sensors, health sensors, and others. The accelerometers segment dominated with 32.40% share in 2025 due to its ability to accurately track physical activities such as walking, running, and cycling. They provide precise measurements of movement and orientation, enabling wearable devices to differentiate between various types of physical activity. This capability is essential for fitness enthusiasts who seek detailed insights into their performance and activity levels. Moreover, the rise of smartwatches, which generally incorporate accelerometers, has significantly contributed to the demand for these sensors.

By Device

Based on device, the market is segmented into smartwatches, fitness bands, smart glasses, smart footwear, smart socks and others. The fitness band segment is expected to experience significant growth rate of CAGR 13.74%. This growth is driven by increasing demand from young consumers for affordable fitness trackers and continuous technological advancements. In March 2023, Infineon Technologies introduced SECORA Connect X, a low-power NFC chip designed for fitness bands, rings, and smartwatches. This integrated solution enables secure contactless payments and wireless charging, ultimately enhancing user experience due to its compact size and efficiency, which boosts battery life. Such developments are expected to drive the segment growth.

| Device Types | Description | Functions | Use Cases |

| Smartwatches | Wrist bands with sensors. | Monitor health, activities, and messages. | Heart rate monitoring, physical activity tracking, calls, etc. |

| Fitness watches | Wrist bands for fitness use. | Monitor daily exercise activities. | Steps monitoring, sleep monitoring, calorie consumption, etc. |

| Smart glasses | Glasses with sensors or displays. | Hands-free use of smart features. | Navigation, industrial purposes, vision assistance, etc. |

| Smart shoes | Shoes with sensors. | Track walking and running activities. | Running monitoring, steps monitoring, posture monitoring, etc. |

| Smart socks | Socks with foot sensors. | Monitor foot health and movements. | Sports training, rehabilitation, etc. |

| Others | Other smart wearable devices. | Used for monitoring and smart services. | Sports, healthcare, and other applications. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Insights

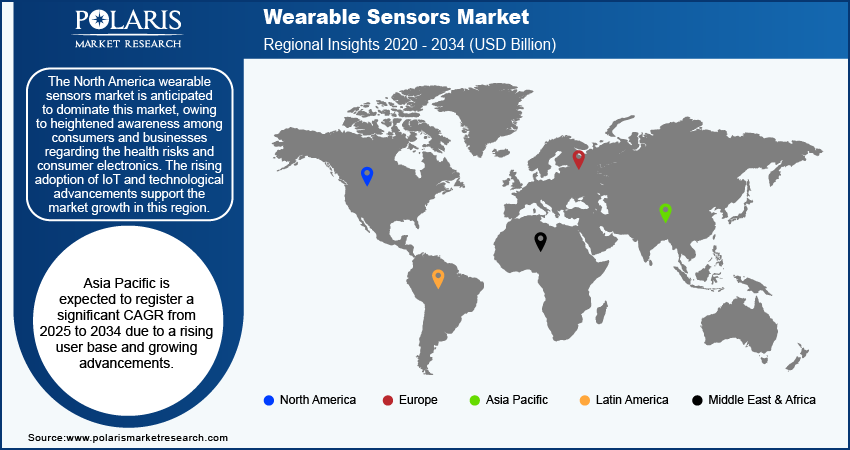

By region, the study provides insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America dominated the market with 35.90% share in 2025, owing to heightened awareness among consumers and businesses regarding health risks and consumer electronics. The rising adoption of IoT and technological advancements also support the growth in this region.

The key players are merging, acquiring, and collaborating to strengthen their presence and serve better offerings in North America, further driving the market during the forecast period. The United States wearable sensors market has garnered the largest share in the region due to the rising consumer health awareness and growing healthcare sector.

The Asia Pacific wearable sensors market, is expected to register the fastest CAGR of 20.4% from 2026 to 2034 due to the growing user base and increasing disposable incomes. Moreover, growing urbanization, expanding e-commerce industry, and advancement in technology are propelling the growth of the region. China is expected to witness significant growth in the region during the forecast period, owing to the presence of major technology companies.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

Major players are investing heavily in research and development in order to expand their product lines, which will help the market grow even more. Participants are also undertaking a variety of strategic activities to expand their global footprint, with important developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive environment, the wearable sensors industry must offer cost-effective items.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers to benefit clients and increase the sector. In recent years, the market has witnessed some technological advancements. Major players in the include Infineon Technologies AG; Texas Instruments Inc.; Broadcom Limited; Asahi Kasei Microdevices Corporation; NXP Semiconductors N.V.; Robert Bosch GmbH; Invensense, Inc.; TE Connectivity Ltd.; Knowles Electronics, LLC; and Panasonic Corporation.

Infineon Technologies AG, headquartered in Neubiberg, Germany, is a leading global semiconductor company with around 58,000 employees. Founded as a spin-off from Siemens in 1999, Infineon specializes in semiconductor solutions across four main segments. The Automotive segment provides chips for electric vehicles, automated driving, and safety systems. The Green Industrial Power segment focuses on power semiconductors for energy generation, industrial drives, and renewable energy applications. The Power & Sensor Systems segment offers power management components, sensors, and connectivity solutions for consumer electronics and IoT devices. Lastly, the Connected Secure Systems segment delivers embedded security controllers for payment systems, government IDs, and secure connectivity. Infineon operates globally with more than 150 locations, serving regions in Europe, Asia Pacific, Greater China, Japan, and the Americas. Its innovative technologies drive advancements in electromobility, energy efficiency, and digital security, making it a key player in the semiconductor industry worldwide.

STMicroelectronics (ST) is a semiconductor company headquartered in Geneva, Switzerland, established in 1987. It designs and manufactures a variety of semiconductor products used in automotive, industrial, personal electronics, and communication applications. The company’s product range includes microcontrollers, analog and power devices, MEMS sensors, application-specific integrated circuits (ASICs), and smartcards. ST’s main business segments cover automotive systems, such as electric vehicle components and driver-assistance technologies; industrial uses, including factory automation and energy management; personal electronics, like mobile devices and wearables; and communication products, such as networking and wireless connectivity chips. The company operates manufacturing sites in Italy, Singapore, France, Morocco, the Philippines, Malta, Malaysia, and China. Its sales and marketing offices are located in more than 35 countries. The Asia Pacific region accounts for about 59% of its revenue, with the Americas and Europe making up the remainder. It recently introduced advanced wearable sensors for improved health and fitness tracking, ideal for consumer and medical applications.

List of Key Companies

- Infineon Technologies AG

- Texas Instruments Inc.

- Broadcom Limited

- Asahi Kasei Microdevices Corporation

- NXP Semiconductors N.V.

- Robert Bosch GmbH

- Invensense, Inc. (TDK Corporation)

- TE Connectivity Ltd.

- Knowles Electronics, LLC

- Panasonic Corporation

- Analog Devices Inc.

Future of Wearable Sensors Market

The wearable sensors market is anticipated to grow as demand for personalized health care and fitness wearables increases. Artificial intelligence-based health data analysis and adoption of telemedicine are expected to offer additional opportunities. Technological advancements in MEMS and miniature sensors are expected to enhance user experience and sensor accuracy. The application of wearable sensors in sports, industrial applications, and connected lifestyle devices is expected to drive market growth

Wearable Sensors Industry Developments

-

March 2026: Oura acquired Doublepoint, an innovative company that develops gesture detection technologies. According to the press release, the acquisition will be helpful for improving the interaction and motion tracking abilities of the Oura Ring. (source: ouraring.com)

-

February 2026: Natus Sensory announced the acquisition of TheraB Medical. Natus Sensory stated that the strategic move will strengthen its newborn care portfolio. It will expand its phototherapy offering with the first FDA‑cleared wearable phototherapy system created as a swaddle‑style garment. (source: businesswire.com)

- January 2025: A wearable stress-detecting system, inspired by human pain perception and developed using a silver wire network, was launched by JNCASR to enable adaptive, intelligent sensing for healthcare and robotics applications. (Source: theindianpractitioner.com)

Wearable Sensors Market Segmentation

By Sensor Type Outlook

- Motion Sensors

- Gyroscopes

- Accelerometers

- Pressure and Force Sensors

- Touch Sensors

- Inertial Sensors

- Magnetometers

- Temperature and Humidity Sensors

- Medical Sensors

- Others

By Technology Outlook

- MEMS

- CMOS

- Others

By Device Outlook

- Smartwatch

- Smart Socks

- Fitness Bands

- Smart Glasses

- Smart Fabric

- Others

By End Users Outlook

- Consumer

- Healthcare

- Industrial

- Defense

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Wearable Sensors Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 2.45 billion |

| Market Size Value in 2026 | USD 2.94 billion |

| Revenue Forecast in 2034 | USD 13.02 billion |

| CAGR | 20.49% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Wearable Sensors Market FAQ's

The wearable sensors market size was valued at USD 2.45 billion in 2025 and is projected to grow to USD 13.02 billion by 2034

The market is projected to register a CAGR of 20.49% from 2026 to 2034.

North America is dominated the market with 35.90% share.

The key players in the market are Infineon Technologies AG; Texas Instruments Inc.; Broadcom Limited; Asahi Kasei Microdevices Corporation; NXP Semiconductors N.V.; Robert Bosch GmbH; Invensense, Inc.; TE Connectivity Ltd.; Knowles Electronics; LLC; and Panasonic Corporation.

The accelerometer segment dominated the market with 32.40% share in 2025.

The fitness band segment is anticipated to experience significant growth rate of CAGR 13.74% in the market.

Wearable sensors are advanced devices that monitor and collect real-time physiological and biochemical data in a non-invasive manner, integrated into smartwatches, fitness trackers, and smart clothing for health monitoring.

Key trends include sensor miniaturization through MEMS technology enabling compact, energy-efficient wearables, and growing integration of IoT and AI technologies that enhance data accuracy and expand healthcare applications.

Download Sample Report of Wearable Sensors Market

Please fill out the form to request a customized copy of the research report.