AI in Pathology Market Demand, Share Global Analysis Report, 2025-2034

REPORT DETAILS

AI in Pathology Market Summary

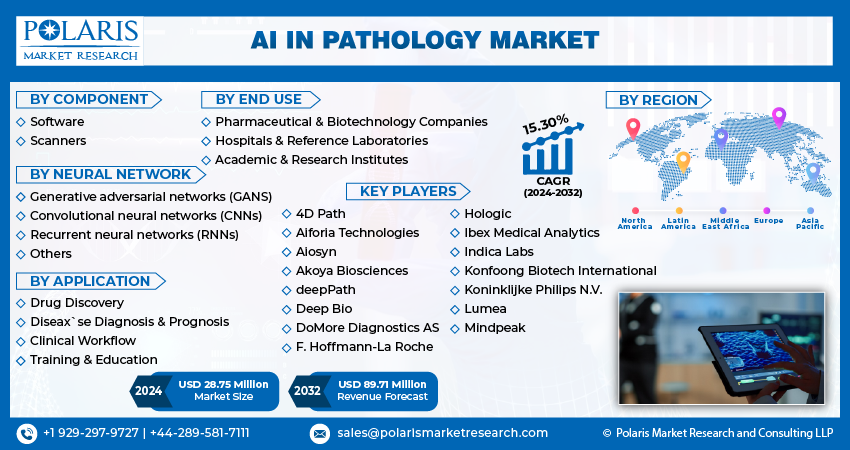

The global AI In Pathology market size was valued at USD 27.69 billion in 2024, growing at a CAGR of 15.1% from 2025 to 2034. Rising prevalence of cancer and other chronic diseases requiring precise pathology analysis along with increasing R&D investments by pharmaceutical and biotechnology companies for biomarker discovery is propelling the market growth.

Market Statistics

Key Takeaways

- End-to-end solutions led the market in 2024, fueled by their capacity to support thoroughly across the entire pathology workflow, from image acquisition to diagnostics and reporting.

- GANs (Generative Adversarial Networks) are anticipated to advance with the fastest growth rate over the forecast period, facilitating synthetic image generation, predictive modeling, and temporal analysis for advanced disease progression research.

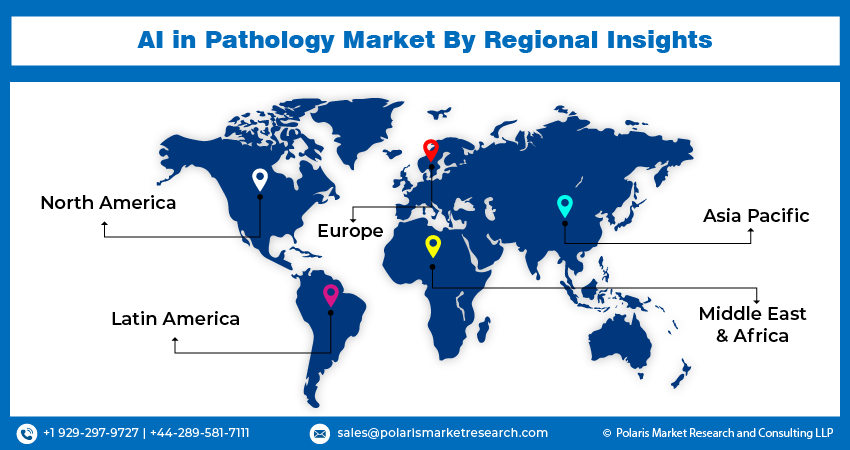

- North America dominated in 2024 due to strong use of digital pathology and AI-based solutions within hospitals and research centers.

- The U.S. held the leading share in North America, driven by increasing incidence of cancer and chronic diseases.

- Asia Pacific to register the highest growth rate over the forecast period, owing to fast digitalization of healthcare infrastructure and uptake of AI-based pathology solutions.

- India experienced robust momentum in Asia Pacific, due to increasing pharmaceutical R&D and biomarker discovery programs.

Which are the industry dynamics for AI in Pathology Market?

- Rising incidence of cancer and other long-term diseases is causing demand for accurate and exact pathology analysis, propelling market growth.

- Pharmaceutical and biotech firms' increased R&D spending to discover biomarkers are fueling growth in the adoption of AI-based pathology solutions.

- High costs of implementing AI platforms and digital pathology infrastructure are constraining market growth, especially for small laboratories and institutions.

- Explainable AI (XAI) integration is opening doors by delivering transparent and understandable outputs, facilitating clinical adoption and regulatory clearance.

The Pathology AI market includes high-level software solutions that assist medical image and pathology slide analysis with enhanced accuracy and faster processing. The machines use machine learning and deep learning algorithms to recognize patterns, classify illnesses, and assist in diagnosis. Integration of AI maximizes workflow efficiency, eradicates human errors, and enables prompter disease detection, positioning the technology as a critical one in modern diagnostic laboratories and healthcare facilities.

The AI in pathology market is expanding as machine learning and deep learning technologies enhance image identification and pattern assessment in tissue and cell samples. These devices enable pathologists to identify abnormalities quicker and with better precision. Ongoing advances in AI algorithms are increasing predictive power, enabling early diagnosis and enhancing clinical decision-making.

Source: Polaris Market Research Analysis

Regulatory authorities and governments are encouraging the uptake of AI-powered pathology solutions to further precision medicine. Digital pathology and AI verification guidelines, along with supportive policies and frameworks, are boosting the growth. Standardization and AI diagnosis system approvals are also simplifying the process of adopting these technologies in day-to-day workflows for healthcare professionals.

Drivers & Opportunities

What are the factors driving the AI in pathology market?

Rising Prevalence of Cancer and Chronic Diseases: The rising rate of cancer and other chronic diseases is fueling demand for AI-based pathology solutions. As per the World Health Organization (WHO), new cases of cancer are estimated to be more than 35 million by 2050, a 77% increase from approximately 20 million cases in 2022. Proper tissue analysis and biomarker detection are essential in diagnosis, treatment planning, and monitoring. AI assists in managing the increasing number of samples while minimizing errors, enabling timely and effective patient care.

Increasing R&D Investments in Biomarker Discovery: Biopharma and pharmaceutical firms are spending heavily on AI pathology for biomarker discovery. In March 2025, Proscia raised USD 50 million to further develop its AI-driven pathology platform, Concentriq, reflecting robust investor belief in diagnostic technologies empowered by AI. These technologies speed drug development by validating molecular targets and forecasting patient response.

Source: Polaris Market Research Analysis

Segmental Insights

By Offering

Based on offering, the AI in Pathology market is segmented into end-to-end solutions and niche point solutions. End-to-end solutions held market leadership in 2024, owing to its capability of exhaustive support throughout the whole pathology workflow, from image acquisition to diagnostics and reporting.

Niche point solutions is expected to grow at a fast pace during the forecast period as image analysis-specialized tools, predictive analytics, and automated reporting become increasingly popular among research-intensive laboratories and academic institutions.

By Neural Network

Based on neural network, the market is divided into convolutional neural networks (CNNs), generative adversarial networks (GANs), recurrent neural networks (RNNs), and other neural networks. CNNs dominated the highest share in 2024 as a result of its established competence in high-precision image recognition, segmentation, and classification in digital pathology.

GANs are anticipated to experience robust expansion across the forecasting period, owing to its increased synthetic image generation, predictive modeling, and temporal analysis for advanced disease progression studies.

By Function

By function, the market is categorized into image analysis, diagnostics, workflow management, data management, predictive analytics, clinical decision support systems (CDSS), automated report generation, and quality assurance tools. Image analysis dominated the market share in 2024 due to the rising adoption of AI to automate mundane pathology procedures, minimize human error, and enhance throughput.

Predictive analytics are projected to expand rapidly, driven by research organizations and healthcare providers increasingly turn to AI for disease outcome predictions and the simplification of reporting operations.

By Use Case

Based on use case, the market is divided into drug discovery, disease diagnosis & prognosis, clinical workflow, and training & education. In 2024, the largest share was held by disease diagnosis & prognosis, driven by increasing demand for precise, early cancer, infectious disease, and chronic condition detection.

Drug discovery are anticipated to grow rapidly in the forecast period as hospitals and pharmaceutical firms make greater use of AI for target identification, preclinical research, and optimizing laboratory efficiency.

By End User

On the basis of end user, the market is segmented into pharmaceutical & biopharmaceutical companies, hospitals & reference laboratories, and academic & research institutes. Hospitals and reference laboratories held the market in 2024 , due to digital pathology and AI-enabled diagnostic solutions are increasingly adopted for routine and specialty testing.

Pharmaceutical and biopharmaceutical firms are expected to observe rapid growth over the forecast period as AI helps drug discovery and translational research.

Source: Polaris Market Research Analysis

Regional Analysis

Which region accounted for largest market share in AI in Pathology market in 2024?

North America accounted for a major share of the worldwide AI in Pathology market in 2024. Increasing use of digital pathology and AI-based solutions across hospitals and research institutions is propelling growth. Availability of top AI technology providers and pathology solution firms is facilitating rapid implementation of new diagnostic equipment across the region.

The U.S. AI In Pathology Market Overview

The U.S. leads the North American market, fueled by increasing prevalence of cancer and chronic diseases. The U.S. Centers for Disease Control and Prevention (CDC) estimates that approximately 129 million Americans suffer from at least one significant chronic disease. Further, multiple chronic conditions are rising, with 42% of the population suffering from two or more and 12% suffering from five or more. Hospitals and diagnostic centers are more frequently utilizing AI-powered pathology solutions to enhance accuracy and efficiency in diagnosis.

Asia Pacific AI In Pathology Market Insights

Why Asia Pacific is expected to grow significantly over the upcoming years

Asia Pacific is anticipated to grow rapidly during the forecast period. This is due to the accelerating digitalization of healthcare infrastructure and uptake of AI-enabled pathology systems are major factors driving growth. Partnerships between international AI solution providers and local healthcare organizations are facilitating uptake of sophisticated diagnostic technologies across several nations.

India AI In Pathology Market Analysis

India is becoming a high-growth market due to the growing pharmaceutical R&D and biomarker discovery efforts. For example, Indian Union Budget 2025–26 provides USD 602.9 million to the Department of Pharmaceuticals (DoP), an increase of 28.8% from last year's budget of USD 468 million. The growing need for AI pathology solutions stems from attempts to improve diagnostic accuracy, velocity, and scalability in research and clinical use cases.

Europe AI In Pathology Market Assessment

Europe is expected to experience consistent growth, driven by rising adoption of digital pathology platforms in hospitals and labs. Public programs and EU funding opportunities for AI healthcare research are facilitating innovation in diagnostics and encouraging wider deployment of AI-enabled pathology solutions.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The international AI in Pathology market is extremely dynamic and influenced by technological breakthroughs in artificial intelligence, machine learning, and digital imaging technologies. Firms are investing to create sophisticated AI-driven platforms to enhance diagnostic precision, streamline workflow, and facilitate early disease detection. Strategic partnerships with hospitals, research centers, and diagnostic laboratories are defining the industry to speed up adoption of AI solutions and incorporate them into current pathology systems.

Which are the key players in AI in pathology market?

Major companies in the global AI in Pathology market are Aiforia Technologies Plc, Akoya Biosciences, Inc., Deep Bio Inc., Hologic, Inc., Ibex Medical Analytics Ltd., Indica Labs Inc., Koninklijke Philips N.V., Mindpeak GmbH, OptraScan, Inc., Paige AI, Inc., Proscia Inc., Techcyte, Inc., Tempus Labs, Inc., Tribun Health, and Visiopharm A/S.

Key Players

- Aiforia Technologies Plc

- Akoya Biosciences, Inc.

- Deep Bio Inc.

- Hologic, Inc.

- Ibex Medical Analytics Ltd.

- Indica Labs Inc.

- Koninklijke Philips N.V.

- Mindpeak GmbH

- OptraScan, Inc.

- Paige AI, Inc.

- Proscia Inc.

- Techcyte, Inc.

- Tempus Labs, Inc.

- Tribun Health

- Visiopharm A/S

AI In Pathology Industry Developments

In July 2025, PathAI introduced the Precision Pathology Network (PPN), a nationwide network of digital anatomic pathology laboratories supported by the AISight Image Management System (IMS). The platform provides advanced AI capabilities, including MET-Predict for identifying MET-amplified tumors, access to Explore for biomarker discovery, and the PLUTO foundation model to enable research collaboration and custom model development.

In August 2025, PathAI and Moffitt Cancer Center announced a multi-year strategic partnership to implement PathAI’s AISight Dx digital pathology platform across Moffitt’s pathology operations. AISight Dx is a cloud-native system that unifies enterprise-scale slide management, viewing, and collaboration with integrated AI tools to enhance diagnostic speed, accuracy, and workflow efficiency. The collaboration also supports joint research initiatives, real-world multimodal data integration, clinical trials, biopharma partnerships, and co-development of next-generation AI-powered diagnostics to advance precision medicine.

In March 2025: Aiforia partnered with PathPresenter to drive adoption of AI-assisted image analysis by implementing Aiforia's models within PathPresenter's workflow platform. Through the partnership, pathologists worldwide use AI tools more easily within their current digital pathology workflows, enhancing speed and diagnostic accuracy.

In February 2024: Roche Tissue Diagnostics (RTD) collaborated with PathAI to create AI-based digital pathology algorithms for RTD's companion diagnostics business. The algorithms was incorporated within the Roche Navify Digital Pathology platform, making it simple to adopt throughout pathology labs worldwide.

AI In Pathology Market Segmentation

By Offering Outlook (Revenue, USD Billion, 2020–2034)

- End-to-End Solutions

- Niche Point Solutions

- Technology

- Hardware

- Microscopes

- Scanners

- Storage Systems

By Neural Network Outlook (Revenue, USD Billion, 2020–2034)

- Convolutional Neural Networks (CNNS)

- Generative Adversarial Networks (GANS)

- Recurrent Neural Networks (RNNS)

- Other Neural Networks

By Function Outlook (Revenue, USD Billion, 2020–2034)

- Image Analysis

- Diagnostics

- Workflow Management

- Data Management

- Predictive Analytics

- CDSS

- Automated Report Generation

- Quality Assurance Tools

By Use Case Outlook (Revenue, USD Billion, 2020–2034)

- Drug Discovery

- Disease Diagnosis & Prognosis

- Clinical Workflow

- Training & Education

By End User Outlook (Revenue, USD Billion, 2020–2034)

- Pharmaceutical & Biopharmaceutical Companies

- Hospitals & Reference Laboratories

- Academic & Research Institutes

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

AI In Pathology Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 27.69 Billion |

| Market Size in 2025 | USD 31.81 Billion |

| Revenue Forecast by 2034 | USD 113.02 Billion |

| CAGR | 15.1% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion, Volume in Kilotons and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

AI in Pathology Market FAQ's

The global market size was valued at USD 27.69 billion in 2024 and is projected to grow to USD 113.02 billion by 2034.

The global market is projected to register a CAGR of 15.1% during the forecast period.

North America dominated the market in 2024.

A few of the key players in the market are Aiforia Technologies Plc, Akoya Biosciences, Inc., Deep Bio Inc., Hologic, Inc., Ibex Medical Analytics Ltd., Indica Labs Inc., Koninklijke Philips N.V., Mindpeak GmbH, OptraScan, Inc., Paige AI, Inc., Proscia Inc., Techcyte, Inc., Tempus Labs, Inc., Tribun Health, and Visiopharm A/S.

The end-to-end solutions segment dominated the market revenue share in 2024.

The GAN segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of AI in Pathology Market

Please fill out the form to request a customized copy of the research report.