Air Quality Monitoring System Market Growth Analysis, Global Report, 2025-2034

REPORT DETAILS

Air Quality Monitoring System Market Summary

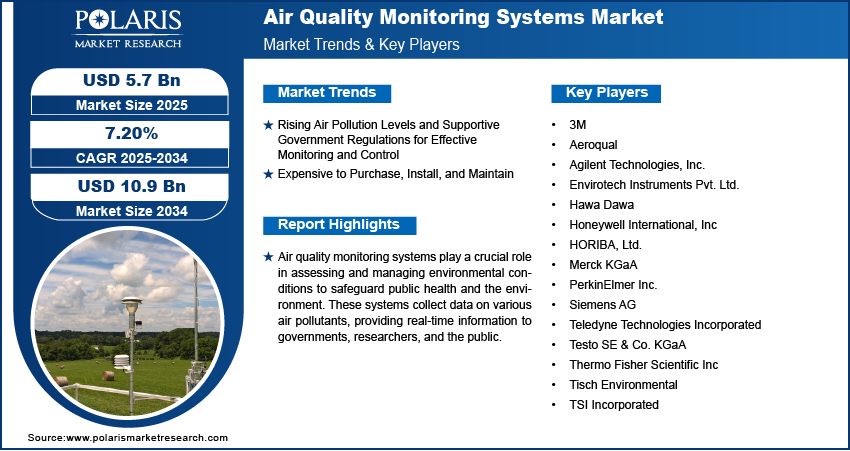

The global air quality monitoring system market size was valued at USD 5.73 billion in 2024, growing at a CAGR of 7.35% from 2025 to 2034. Key factors driving demand for air quality monitoring systems include the rising concerns surrounding indoor air quality, advancements in air quality monitoring technology, surging urban air pollution, and increasing smart city initiatives.

Market Statistics

Key Takeaways

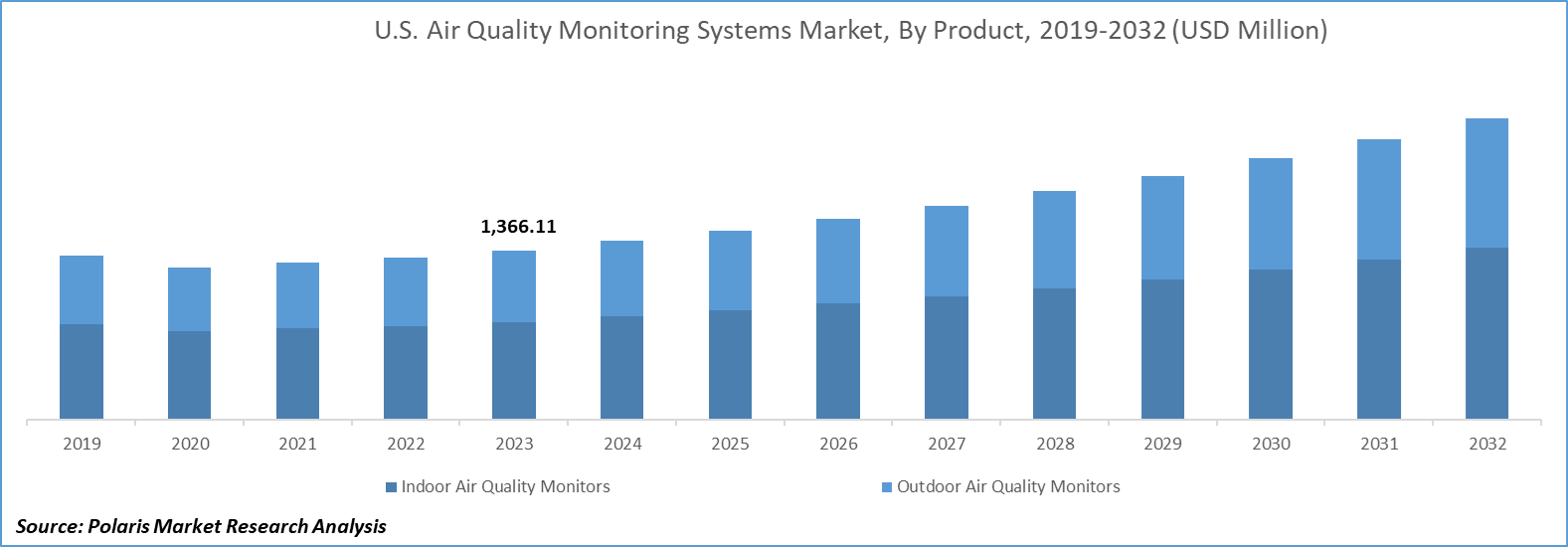

- In 2024, the outdoor air quality monitoring systems segment dominated the global market, capturing a 65% revenue share, largely due to rising demand for tracking ambient air pollutants in urban, industrial, and high-traffic areas.

- The physical monitoring segment is projected to grow the fastest in the coming years, fueled by rising concerns over particulate matter (PM2.5 and PM10), temperature, humidity, and noise pollution.

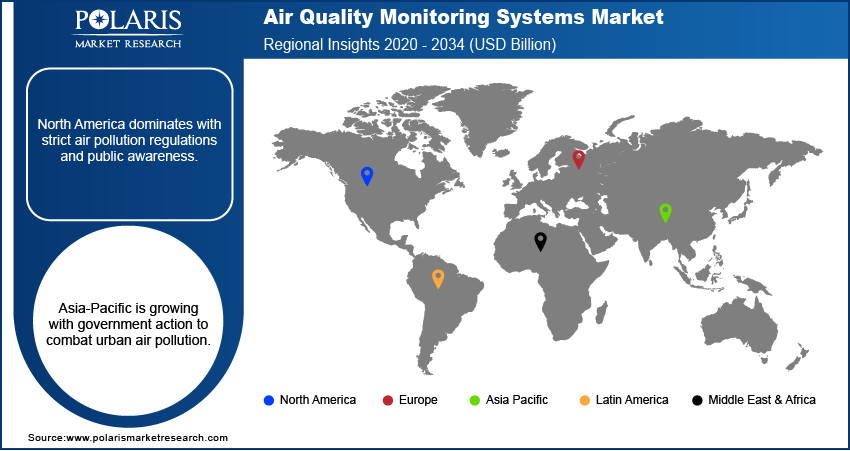

- North America led the global market in 2024 with a 36% share, supported by robust regulatory enforcement, advanced monitoring infrastructure, and high public awareness.

- The U.S. held a dominant position in 2024 due to its strong regulatory policies, government support, and widespread adoption of advanced monitoring technologies.

- The Asia Pacific market is anticipated to grow the fastest during the forecast period, driven by rapid urbanization, industrial expansion, and worsening air pollution.

- The air quality monitoring system industry in India is experiencing significant growth as rising urban and industrial pollution prompts both government and private investments in real-time air quality monitoring solutions.

Industry Dynamics

- Growing urban pollution from vehicles, industries, and construction is accelerating demand for air quality monitoring systems in densely populated areas.

- Smart city projects worldwide are integrating real-time air monitoring into sustainable infrastructure, supporting digital transformation and urban resilience.

- High costs of advanced monitoring systems limit adoption, especially in developing regions where budgets are tight but pollution levels are severe.

- Rising smart city investments create demand for scalable, IoT-enabled air quality sensors that provide real-time data for urban planning.

Source: Polaris Market Research Analysis

AI Impact on Air Quality Monitoring System Market

- AI-powered sensor networks in air quality monitoring systems analyze pollutants in real time, which offers hyperlocal insights that traditional systems can miss.

- AI calibrates low-cost Internet of Things (IoT) sensors against reference-grade instruments, which can improve accuracy and expand coverage across rural and urban areas.

- AI tools identify outliers and fill gaps in sensor data, ensuring continuous and reliable monitoring in challenging environments.

- AI-generated insights are shaping urban planning decisions and environmental policies.

Air quality monitoring system is a network of devices and sensors used to detect, measure, and report pollutants in the atmosphere, ensuring real-time assessment of air quality levels. Rising concerns surrounding indoor air quality have become a necessity, as people spend a considerable portion of their time indoors. According to an October 2024 WHO report, outdoor and indoor air pollution collectively contribute to approximately 6.7 million premature deaths each year. The findings highlight the global health impacts of exposure to polluted air in both environmental and domestic environments. Increasing awareness about the health impacts of indoor air pollutants such as volatile organic compounds (VOCs), carbon monoxide, and particulate matter has driven both residential and commercial users to adopt these systems. Moreover, the rise in urban living, airtight building structures, and widespread use of synthetic materials have further amplified the demand for accurate indoor air quality assessments. This has driven market players to offer more compact, affordable, and real-time monitoring solutions for households, workplaces, and healthcare environments.

Advancements in air quality monitoring technology are shaping market dynamics. Technological innovations such as IoT technology integration, AI-based data analytics, and miniaturized sensors are enabling more precise and real-time tracking of multiple air pollutants. According to a June 2023 PIB report, IIT Madras researchers developed a mobile air quality monitoring system using public vehicles. The IoT devices measure PM levels, NOx, SOx, road conditions, and UV index, with modular sensors and GPS/GPRS for real-time data collection and transmission. These smart systems enhance the accuracy of data collection and also offer remote access, predictive maintenance, and integration with other environmental monitoring platforms. Such improvements have expanded the application scope of these systems, ranging from industrial sites and urban traffic monitoring to personal portable devices. As a result, the market is transitioning toward more automated, connected, and user-centric solutions, paving the way for smarter environmental management.

Drivers & Opportunities

Rising Urban Air Pollution: Rising urban air pollution is driving the demand for air quality monitoring systems, as rapid industrialization, vehicular emissions, and construction activities in densely populated cities continue to degrade ambient air quality. According to a June 2025 US EPA report, the average passenger vehicle produces approximately 4.6 metric tons of carbon dioxide emissions annually. This finding quantifies the climate impact of individual automobile use in the U.S. The growing presence of harmful pollutants such as nitrogen dioxide, sulfur dioxide, ozone, and particulate matter poses serious health risks, driving the need for accurate and continuous monitoring. Government agencies, industries, and environmental organizations are adopting advanced monitoring systems to assess, regulate, and mitigate pollution levels as awareness of the adverse health and environmental impacts of urban pollution increases. This trend is reinforcing the integration of high-precision monitoring solutions across urban centers to support regulatory compliance and public health initiatives.

Increasing Smart City Initiatives: Increasing smart city initiatives are contributing to the expansion opportunities. Real-time environmental monitoring has become a fundamental component of smart infrastructure as cities worldwide move toward digital transformation and sustainable urban development. These monitoring systems are being integrated into intelligent transportation systems, energy-efficient buildings, and public health networks to ensure data-driven decision-making and enhance the quality of urban life. According to a February 2025 report, the PASSEPARTOUT project has deployed 20 AirSENCE devices across three European cities since 2022. These miniature sensors monitor pollutants, weather, noise, and light, generating over 1.2 million data points per unit while maintaining accuracy with reference stations. These systems enable city planners and policymakers to develop responsive strategies for pollution control and urban planning, aligning with broader goals of environmental sustainability and citizen well-being.

Source: Polaris Market Research Analysis

Segmental Insights

Product Type Analysis

Based on product type, the segmentation includes indoor air quality monitoring systems and outdoor air quality monitoring systems. The outdoor air quality monitoring systems segment accounted for 65% of global revenue share in 2024, primarily due to the growing focus on monitoring ambient air pollutants across urban, industrial, and traffic-dense areas. Governments and environmental agencies are increasingly deploying outdoor monitoring stations to assess air quality trends, enforce regulatory compliance, and mitigate pollution-related health risks. These systems are critical for large-scale, real-time surveillance of pollutants such as nitrogen oxides, ozone, carbon monoxide, and particulate matter. Additionally, the need for public air quality data transparency has encouraged investments in fixed and portable outdoor monitoring infrastructure. The segment benefits from broad application across sectors, such as transportation, energy, construction, and industrial manufacturing.

Pollutant Analysis

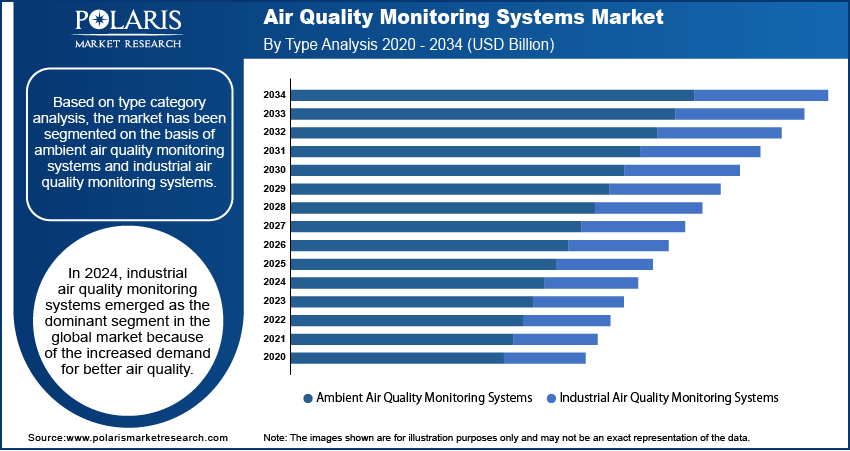

In terms of pollutant, the segmentation includes chemical and physical. The physical segment is expected to witness the fastest growth during the forecast period, driven by increasing concerns over particulate matter (PM2.5 and PM10), temperature, humidity, and noise levels. Demand for precision-based monitoring of physical parameters is gaining momentum as awareness of the direct impact of particulate pollutants on respiratory and cardiovascular health increases. The integration of advanced sensing technologies and data analytics has enhanced the ability to detect and report these pollutants in real time. Moreover, the growing presence of PM emissions from vehicular traffic, construction sites, and industrial zones is contributing to the segment’s rapid expansion. These factors are driving the adoption of physical pollutant monitoring systems across residential and urban areas.

Component Analysis

The segmentation, based on component, includes hardware, software, and services. The hardware segment held the largest revenue share in 2024 owing to the widespread deployment of air quality sensors, analyzers, and other physical components necessary for real-time environmental monitoring. The increasing demand for robust and accurate measurement tools has led to substantial investments in hardware innovation, enhancing sensor sensitivity, durability, and connectivity. These components form the backbone of air quality monitoring, enabling continuous and reliable data capture in both indoor and outdoor environments. Moreover, the rise in customized monitoring solutions for industrial and municipal applications is also fueling hardware demand, supported by the growing focus on building resilient and scalable air quality monitoring infrastructure.

End Use Analysis

Based on end use, the segmentation includes residential, commercial, and industrial. The industrial segment is expected to witness significant growth by 2034, driven by stricter regulatory frameworks aimed at controlling emissions from heavy industries such as manufacturing, energy, and mining. Industries are increasingly integrating these monitoring systems into their environmental management strategies to ensure regulatory compliance and reduce operational risks. The growing focus on workplace safety, combined with rising corporate sustainability goals, is also encouraging industrial operators to adopt advanced monitoring solutions. The demand for high-performance monitoring systems across industrial facilities is expected to accelerate as emission thresholds become stricter and environmental accountability gains importance.

Source: Polaris Market Research Analysis

Regional Analysis

The North America air quality monitoring system market accounted for 36% of global market share in 2024. This dominance is attributed to the region’s strong regulatory enforcement, well-established environmental monitoring infrastructure, and high public awareness. The presence of leading companies, with continuous investments in environmental technologies, supports the expansion of advanced monitoring systems. According to a March 2025 report, the U.S. EPA funded USD 51.5 million to support 127 air monitoring projects across 37 states. The initiative targets communities facing unnecessary pollution-related health and environmental impacts, expanding ambient air quality monitoring in underserved areas. Moreover, rising concerns over pollution-related health issues and increasing demand for data-driven policy decisions are reinforcing the deployment of monitoring networks across urban and industrial areas. The region’s proactive approach toward environmental sustainability continues to drive system upgrades and technological innovation.

U.S. Air Quality Monitoring System Market Insights

The U.S. held a significant market share in North America air quality monitoring system landscape in 2024 due to its well-established regulatory framework, strong governmental support, and widespread adoption of advanced monitoring technologies. The presence of leading industry players and a high focus on environmental compliance further support extensive system deployment across industrial, commercial, and municipal sectors. Additionally, public awareness and institutional efforts toward air pollution control contribute to the sustained demand for reliable air quality monitoring infrastructure.

Asia Pacific Air Quality Monitoring System Market Trends

The market in Asia Pacific is projected to witness the fastest growth during the forecast period fueled by rapid urbanization, industrialization, and increasing air pollution levels across the region. Rising public health concerns and supportive government initiatives are accelerating the adoption of air quality monitoring systems in both urban and rural areas. Additionally, the development of smart cities and infrastructure modernization projects is creating demand for integrated environmental monitoring solutions. According to a September 2024 PIB report, India's Smart Cities Mission has completed over 7,200 projects, with a total worth of approximately USD 17.5 billion, including 8,000 multi-sector initiatives valued at USD 19.2 billion across 100 cities, reflecting opportunities for these advance monitoring systems. The region’s growing focus on sustainability, with increasing investments in air quality management, positions it as a growth hub for monitoring technologies.

India Air Quality Monitoring System Market Overview

The market in India is expanding due to rising levels of urban and industrial air pollution, which have boosted both government and private stakeholders to invest in real-time air quality monitoring solutions. Increasing public awareness and policy focus on health and environmental sustainability are also encouraging the adoption of monitoring systems across cities and industrial zones. Furthermore, ongoing infrastructure development and smart city initiatives are creating new avenues for system deployment nationwide.

Europe Air Quality Monitoring System Market Outlook

The air quality monitoring system landscape in Europe is projected to hold a substantial share by 2034, supported by the region’s robust environmental policies and commitment to emission reduction. Europe’s regulatory landscape highlights continuous monitoring and transparent reporting of air pollutants, leading to widespread system deployment across municipal and industrial sectors. The adoption of innovative and energy-efficient monitoring solutions is also gaining traction, driven by sustainability objectives and technological advancements. Furthermore, the integration of air quality data into broader climate and health monitoring frameworks highlights the region’s strategic focus on holistic environmental management.

UK Air Quality Monitoring System Market Analysis

The growth of the UK market is driven by its strict environmental regulations and national strategies focused on reducing air pollution and protecting public health. The country’s proactive viewpoint on emission control and sustainability has led to increased implementation of monitoring systems in urban areas, transportation networks, and critical public spaces. Technological advancements and strong institutional support further strengthen the UK’s position in adopting integrated and data-driven air quality management solutions.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The air quality monitoring landscape is witnessing a rapid transformation, driven by technological advancements, sustainability strategies, and emerging market segments. Established players such as Thermo Fisher and Siemens dominate developed markets with high-precision systems, while startups are leveraging disruptive technologies such as IoT and AI to capture latent demand in cost-sensitive regions. Strategic investments in hyperspectral sensors and low-cost portable devices are reshaping competitive positioning, particularly for small and medium-sized businesses. Revenue growth is accelerating in Asia and Africa due to worsening pollution and stricter regulations, creating expansion opportunities. However, supply chain disruptions and geopolitical shifts pose challenges to regional footprint expansion. Major differentiators include product offerings in multi-pollutant detection and sustainable value chains supporting circular economy principles. Expert insights highlight untapped potential in industrial emissions monitoring, where future development strategies will focus on predictive analytics and integration with smart city infrastructure. Competitive intelligence suggests partnerships with urban planners and healthcare providers will be crucial for capturing long-term revenue opportunities.

A few major companies operating in the air quality monitoring system industry include 3M, Aeroqual, Emerson Electric Co., General Electric (GE), HORIBA Scientific, Merck KGaA, Siemens, Teledyne Technologies, Testo SE & Co. KGaA, and Thermo Fisher Scientific.

Key Players

- 3M

- Aeroqual

- Emerson Electric Co.

- General Electric (GE)

- HORIBA Scientific

- Merck KGaA

- Siemens

- Teledyne Technologies

- Testo SE & Co. KGaA

- Thermo Fisher Scientific

Air Quality Monitoring System Industry Developments

- In April 2025: Sarajevo Canton introduced a new emissions and pollutant data registry using GIS technology to strengthen air quality monitoring and support climate neutrality goals. The digital platform provides a geographic view of emission sources across the region and applies a fully digitized approach to tracking annual air emissions. Officials noted that the system aligns Sarajevo with air monitoring standards followed by more advanced European cities.

- In April 2025: China’s Ministry of Ecology and Environment announced the “National Digital and Intelligent Transformation Plan for the Eco-Environmental Monitoring Network.” The initiative mandates digital and intelligent upgrades to automatic monitoring stations and equipment for air and surface water, aiming to create a smart centralized hub, described as “the brain,” for nationwide ecological and environmental monitoring.

- In August 2024: Renesas Electronics launched the RRH62000, its first multi-sensor indoor air quality module. The compact device detects particles, VOCs, and harmful gases, using an integrated MCU for smart management in HVAC, air purifiers, and smart home systems while meeting global air quality standards.

- In May 2024: Clarity Movement Co. partnered with Australia's Thomson Environmental Systems (TES) as the exclusive Oceania distributor for its Sensing-as-a-Service air quality monitoring technology, covering Australia and New Zealand. The agreement expands regional access to Clarity's solutions.

Air Quality Monitoring System Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2020–2034)

- Indoor Air Quality Monitoring Systems

- Fixed Indoor Systems

- Portable Indoor Systems

- Outdoor Air Quality Monitoring Systems

- Fixed Outdoor Systems

- Portable Outdoor Systems

By Pollutant Outlook (Revenue, USD Billion, 2020–2034)

- Chemical

- Nitrogen Oxides

- Sulfur Oxides

- Carbon Oxides

- Volatile Organic Compounds

- Others

- Physical

By Component Outlook (Revenue, USD Billion, 2020–2034)

- Hardware

- Sensors

- Processors

- Output Devices

- Software

- Services

By End Use Outlook (Revenue, USD Billion, 2020–2034)

- Residential

- Commercial

- Industrial

- Oil & Gas

- Manufacturing

- Food & Beverages

- Pharmaceuticals

- Healthcare

- Others

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Air Quality Monitoring System Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 5.73 Billion |

| Market Size in 2025 | USD 6.14 Billion |

| Revenue Forecast by 2034 | USD 11.62 Billion |

| CAGR | 7.35% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Air Quality Monitoring System Market FAQ's

The global market size was valued at USD 5.73 billion in 2024 and is projected to grow to USD 11.62 billion by 2034.

The global market is projected to register a CAGR of 7.35% during the forecast period.

North America accounted for 36% of global share in 2024.

A few of the key players in the market are 3M, Aeroqual, Emerson Electric Co., General Electric (GE), HORIBA Scientific, Merck KGaA, Siemens, Teledyne Technologies, Testo SE & Co. KGaA, and Thermo Fisher Scientific.

The outdoor air quality monitoring systems segment accounted for 65% of global revenue share in 2024.

The physical segment is expected to witness fastest growth during the forecast period.

Download Sample Report of Air Quality Monitoring System Market

Please fill out the form to request a customized copy of the research report.