Aircraft Electrical System Market Share, Size, Trends, Industry Analysis Report, 2021 - 2028

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

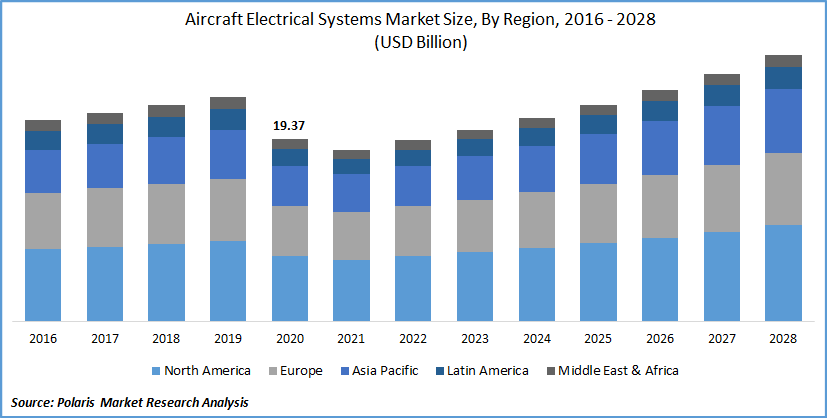

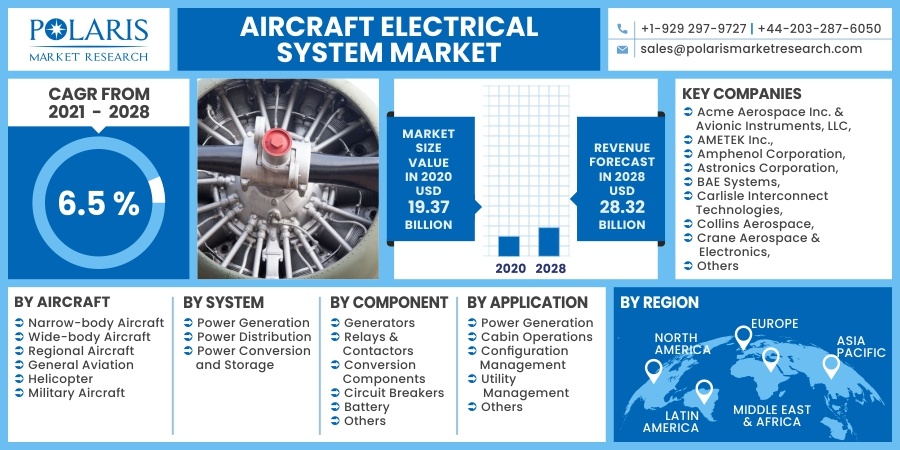

The global aircraft electrical system market was valued at USD 19.37 billion in 2020 and is expected to grow at a CAGR of 6.5% during forecast period. The trend of more electric aircraft with increasing usage of electrical machines and power electronics is one of the prime drivers for aircraft electrical systems. The aircraft industry is increasingly adopting advanced electronics to meet power demands with increased electrical loads. Furthermore, there is also a growing need for reducing carbon emissions and improving fuel economy, which can be achieved to a great extent by deploying more and more electronics in an aircraft.

Know more about this report: Download Sample Report

Know more about this report: Download Sample Report

The COVID-19 pandemic has devasted the ever-growing aircraft industry. The industry's overall demand for electrical systems is in high synergy with the growth/decline of aircraft deliveries. In 2020, the industry recorded USD 371 billion of passenger operating revenues, with an overall reduction of about 2,699 million passengers from 2019 levels.

However, as the impact of the pandemic and economic downturn continues to be acute with the high commercial roll-out of vaccination programs globally, there is a surge in air travel across the globe, with domestic air traffic bouncing back at an excellent rate.

Know more about this report: Download Sample Report

Industry Dynamics

Growth Drivers

Increasing demand for more electric aircraft, growing need for more power with modern integrated electronics, shift from conventional 120 VAC systems to 270 VDC, and 540 VDC systems demand electrical systems with high voltage switching, and organic growth in aircraft deliveries are key factors fueling the market for electrical systems in the aircraft industry.

Additionally, the growing need for reducing carbon footprints in the aircraft industry demands weight reduction, leading to shrinking electronic systems. The trend of meeting SWaP goals drives the demand for lowering power consumption and advancement throughout power generation and distribution systems.

Report Segmentation

The market is segmented in the most comprehensive way based on aircraft, system, component, application, and region.

| By Aircraft | By System | By Component | By Application | By Region |

|

|

|

|

|

Know more about this report: Download Sample Report

Insight by Aircraft

Commercial aircraft (including both narrow-body and wide-body aircraft) segment holds high dominance and offers excellent growth in the near-term as it is witnessing a gradual shift from traditional pneumatic and hydraulic components to electrical components, which substantiates the power demand and ultimately drives the electrical systems market.

For instance, thrust reverser actuation systems have evolved over the decades, with newer commercial aircraft platforms such as A350XWB and A380 having shifted to an electrically powered actuation system for the thrust reversers from traditional hydraulic systems.

The military aircraft segment is also not untouched by electrification trends in the global market. Shrinking power devices while meeting increasing power capacities and thermal management needs substantiates demand for highly reliable power sources driving the market segment. Besides, the trend of meeting SWaP (Size Weight and Power) goals and high levels of electronic system integration further drives the market demand.

Insight by System

Among system types, the power generation segment is likely to remain dominant in the global market during the forecast period. The development of high-thrust engines with increasing demand for greater efficiency substantiates the power demand, stability of engine control, highly integrated electrical power generation systems.

The power distribution segment is estimated to witness the highest CAGR during the forecast period driven by increasing demand for high power load switching and distribution devices such as relays and contactors. There is the trend of building more and more electronic intelligence with an aim to protect abnormal events and proactively detect system faults. Smart contractors are gaining prevalence to control high power circuits and protect against overcurrent and faults.

Insight by Component

Relays & Contactors are likely to offer the highest CAGR in the global market during the forecast period. Increasing demand for high-voltage AC and DC systems in aircraft drives the demand for high-power electromechanical relays and efficient contactors. Furthermore, the adoption of 270 VDC and 540 VDC among commercial and military aircraft has led to incremental technology updates in relays and contactors.

Generators hold a significant share in the global market driven by the ever-growing need for more and more power electronics in modern aircraft platforms. Growing need for reducing electronic load failures and protection from Undervoltage, which may potentially cause component failures, is driving the segment's demand in the market.

Geographic Overview

North America leads the global market with significant demand from leading OEMs and tier players. Modern aircraft platforms in the region demand more power and advancement in electrical systems. For instance, Boeing's upcoming aircraft program B777x will generate twice the current B777 system's power generation. Its electrical load management system will also monitor 30% more power in the aircraft.

Some of the key aircraft platforms in the region, such as Boeing Apache, Super Hornet, Lockheed Martin C130J, and F35; and Gulfstream 650, have modular electronic solutions with 270VDC architectures and seamless transition of power from generation to distribution which drives advancements in the electrical system.

Asia-Pacific region offers the highest growth CAGR driven by a gradual transition to more electric aircraft applications leading to new requirements for active and passive conversion interconnection within power systems to drive electric loads such as motors and pumps.

Besides, there is also a trend of shifting from hydraulic or pneumatic actuators to electric actuators among commercial aircraft and helicopters. New and upcoming aircraft programs such as COMAC C919 and Mitsubishi MRJ jet to further enhance the region's market growth.

Competitive Insight

Leading aircraft electrical systems and component manufacturers are increasingly focusing on developing efficient electronics across the application areas onboard, such as actuators, thrust reverser components, and auxiliary power units. There is also an increasing level of consolidation in the market, with major players acquiring small players in the market.

Some of the key players competing in the global market are Acme Aerospace Inc. & Avionic Instruments, LLC, AMETEK Inc., Amphenol Corporation, Astronics Corporation, BAE Systems, Carlisle Interconnect Technologies, Collins Aerospace, Crane Aerospace & Electronics, Delorean Aerospace LLC, EaglePicher Technologies, Esterline Technologies, GE Aviation, Hartzell Engine Technologies LLC, Honeywell International, Meggitt plc, PBS AEROSPACE, Pioneer Magnetics, Radiant Power Corp, Safran SA, Thales Group.

Aircraft Electrical System Market Report Scope

| Report Attributes | Details |

| Market size value in 2020 | USD 19.37 billion |

| Revenue forecast in 2028 | USD 28.32 billion |

| CAGR | 6.5 % from 2021 - 2028 |

| Base year | 2020 |

| Historical data | 2016 - 2019 |

| Forecast period | 2021 - 2028 |

| Quantitative units | Revenue in USD million/billion and CAGR from 2021 to 2028 |

| Segments covered | By Aircraft, By System, By Component, By Application, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Companies | Acme Aerospace Inc. & Avionic Instruments, LLC, AMETEK Inc., Amphenol Corporation, Astronics Corporation, BAE Systems, Carlisle Interconnect Technologies, Collins Aerospace, Crane Aerospace & Electronics, Delorean Aerospace LLC, EaglePicher Technologies, Esterline Technologies, GE Aviation, Hartzell Engine Technologies LLC, Honeywell International, Meggitt plc, PBS AEROSPACE, Pioneer Magnetics, Radiant Power Corp, Safran SA, Thales Group |

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research & Consulting, Inc. uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

1. Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

2. Data Collection

We gather information from both public and verified sources:

3. Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

| Region | Segment | VolumeUnits | Avg PriceUSD | RevenueUSD Mn | Share % |

|---|---|---|---|---|---|

| North America | Product A | 250 | 2.5 | 500 | 15% |

| Product A | XX | XX | XX | XX | |

| Product A | XX | XX | XX | XX | |

| Consistent methodology applied across regions | |||||

4. Market Estimation

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Forecasting

Step 6:

At Polaris Market Research & Consulting, Inc., we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Validation & Triangulation

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Triangulation Framework

Estimates are cross-verified across three sources:

Company-level data

• Primary inputs from industry participants

• Secondary benchmarks and published data

Variance maintained within +5-10%

Adjustments applied to align estimates

Segment values validated against overall market structure

Data Consistency & Integrity

Segment totals validated to 100%

Regional estimates aligned with global market size

Historical trends compared against forecast outputs

Assumptions reviewed for cross-segment and regional alignment

Final Outputs

Deliverables

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements

Download Sample Report of Aircraft Electrical System Market Share, Size, Trends, Industry Analysis Report, 2021 - 2028

Please fill out the form to request a customized copy of the research report.