Cervical Dysplasia Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

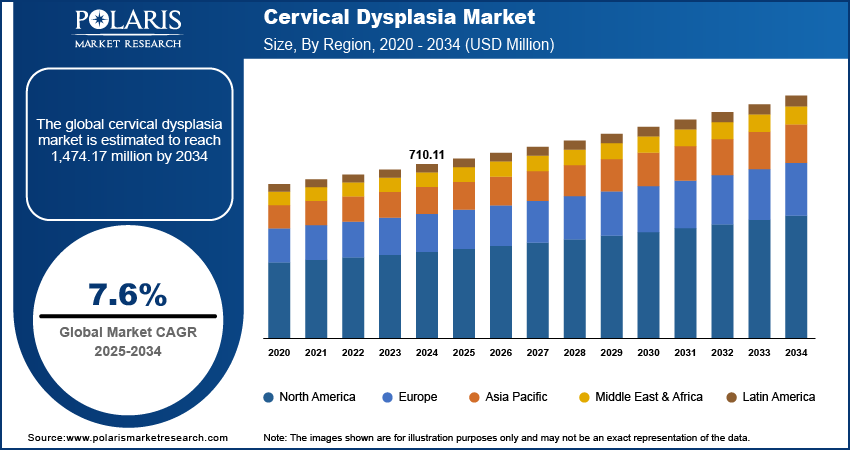

Cervical Dysplasia Market Summary

The global cervical dysplasia market was valued at USD 770.31 million in 2025 and is expected to grow at a CAGR of 6.71% during the forecast period. The growth is driven by rising prevalence of disease, rising government screening programs and technological advancement.

Market Statistics

Key Takeaways

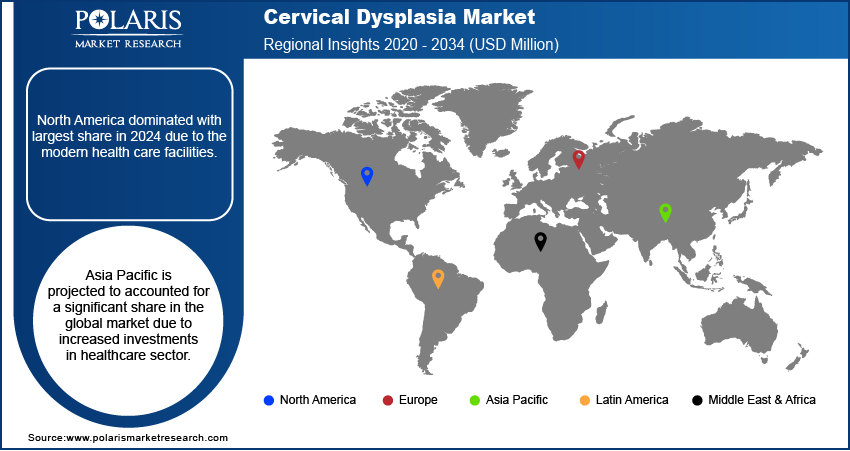

- North America dominated with largest share of 39.0% in 2025 due to the modern health care facilities.

- Asia Pacific is projected to accounted for a significant share of 24.0% in 2025 in the global market due to increased investments in healthcare sector.

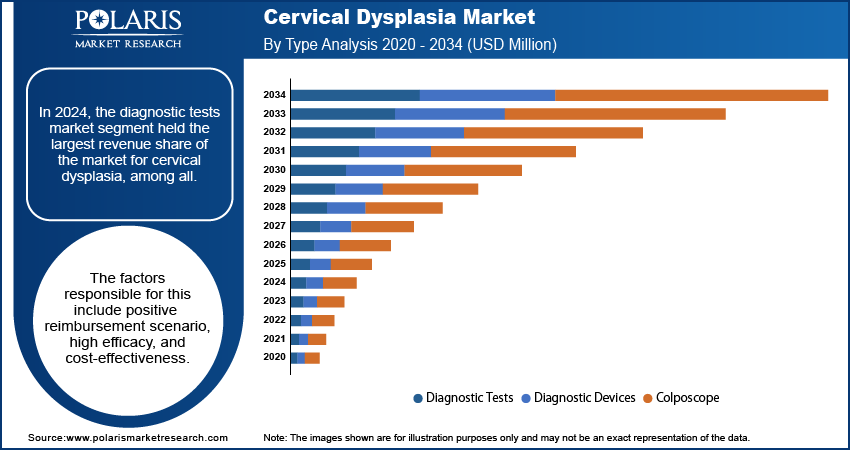

- In 2025, the diagnostic tests market segment held the largest revenue share of the market with 76.0%, driven by positive reimbursement scenario, high efficacy, and cost-effectiveness.

- In 2025, the hospital segment accounted for the largest share of 49.0%, due to the high affordability and spending capacity of hospitals.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

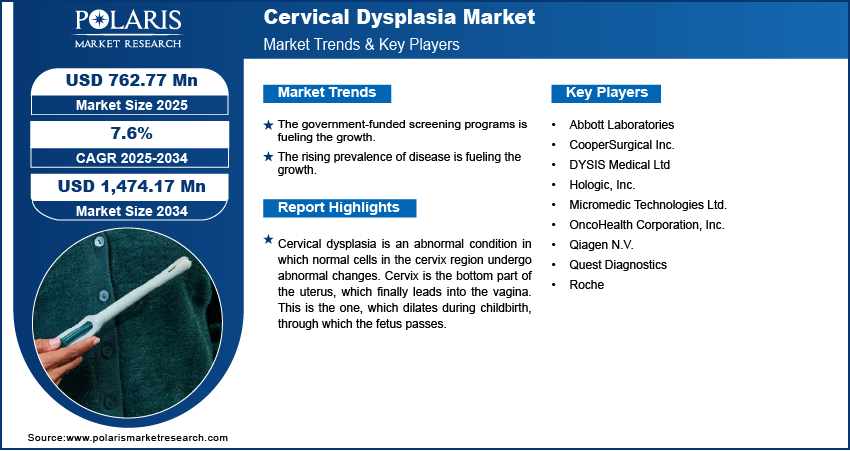

- The government-funded screening programs is fueling the growth.

- The rising prevalence of disease is fueling the growth.

- Technological advancement is driving the growth.

- Limited awareness and screening access to low-income countries is limiting the growth.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What is Cervical Dysplasia?

Cervical dysplasia is an abnormal condition in which normal cells in the cervix region undergo abnormal changes. Cervix is the bottom part of the uterus, which finally leads into the vagina. This is the one, which dilates during childbirth, through which the fetus passes. In this condition, abnormal cells are not cancerous, but in later life, the stage could mutate into cancerous cells, if not treated or diagnosed on time. The Human Papillomavirus (HPV) is the main causal agent for cervical dysplasia.

The prevalence of cervical dysplasia is driving the demand for the effective therapeutics and diagnostics globally. According to the Columbian University, in U.S. alone, 250,000 to 1 million cases of cervical dysplasia are diagnosed every year. This rise in the cases are fueling the demand for the effective diagnosis. Rise in the HPV infection, smoking habits and others are driving these cases. Moreover, expanding healthcare infrastructure and healthcare access in urban as well as rural areas are boosting the number of identified cases which fuels the demand for the diagnostics and therapeutics of this disease, thereby driving the growth.

Difference Between Low-Grade and High-Grade Cervical Dysplasia

Cervical dysplasia is categorized into low-grade and high-grade lesions. The characterization is based on the severity of abnormal cell changes in the cervix. Low-grade cervical dysplasia involves mild abnormalities. They may resolve naturally without aggressive intervention. However, high-grade cervical dysplasia is associated with more severe precancerous changes. It has a higher likelihood of progression to cervical cancer. Differentiating between these two stages is essential for determining appropriate screening frequency, treatment strategies, and long-term patient management in the cervical dysplasia market.

Low-Grade vs High-Grade Cervical Dysplasia

| Aspect | Low-Grade Cervical Dysplasia | High-Grade Cervical Dysplasia |

| Severity | Mild abnormal cellular changes | Severe precancerous cellular abnormalities |

| Common Classification | CIN 1 (Cervical Intraepithelial Neoplasia 1) | CIN 2 and CIN 3 |

| Cancer Progression Risk | Lower risk of progression to cervical cancer | Higher risk of developing cervical cancer |

| HPV Association | Often linked to transient HPV infections | Commonly associated with persistent high-risk HPV infection |

| Treatment Approach | Observation and repeat screening are often sufficient | Requires active treatment such as excision or ablation |

| Monitoring Requirements | Periodic Pap smear or HPV testing | Closer surveillance with colposcopy and follow-up procedures |

| Regression Potential | High likelihood of spontaneous regression | Lower likelihood of natural regression |

| Clinical Impact | Typically less aggressive disease management | More intensive clinical intervention and monitoring |

Industry Dynamics

Growth Drivers

The number of the government screening programs is rising worldwide. These screening programs are aimed to reduce or identify disease with low awareness among the general population, such as cervical dysplasia. This screening program is enabling the early detection of the disease, which in turn is fueling the demand for the diagnostic kits and medical devices which are required for this application. Moreover, rising screening programs in developing countries such as India, Mexico and Vietnam are further boosting the number of the identified cases and thereby fueling the growth of the industry.

Which Key Trends are Expected to Boost the Cervical Dysplasia Market During the Forecast Period?

The cervical dysplasia market is expected to experience significant transformation during the forecast period. Treatment modalities, advancements in diagnostics services, and preventive strategies will drive it. Market players are focusing on adopting technological advancements and innovation. It helps them gain benefits in the competitive landscape. The following table consists of key future trends that are shaping the market:

| Trends | Benefits |

| Integration of Artificial Intelligence (AI) in Diagnostics

|

|

| Advancements in Molecular Diagnostics |

|

| Minimally Invasive Treatments |

|

| Personalized and Immunotherapy-Based Treatments |

|

| Expansion of At-Home Screening Solutions |

|

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Cervical Dysplasia Market Report Scope

The market is primarily segmented on the basis of type, end-use, and region.

| By Type | By End-Use | By Region |

|

|

|

Source: Polaris Market Research Analysis

Know more about this report: Download Sample Report

Insight by Type

In 2025, the diagnostic tests market segment held the largest revenue share of the market accounting for 76.0%. The factors responsible for this include positive reimbursement scenario, high efficacy, and cost-effectiveness. Its low cost resulted in higher penetration in emerging countries. Moreover, strong government initiatives also boosted the adoption of PAP smear tests. This had encouraged women to do smear tests to prevent future occurrences of the concerned condition.

Comparison Matrix: Pap Smear vs HPV Testing

| Aspect | Pap Smear | HPV Testing |

| Purpose | Detects abnormal cervical cell changes | Detects high-risk human papillomavirus (HPV) infection |

| Detection Method | Microscopic examination of cervical cells | Molecular testing for HPV DNA/RNA |

| Primary Focus | Identifies precancerous or cancerous cells | Identifies virus linked to cervical cancer risk |

| Screening Accuracy | Moderate sensitivity for early lesions | Higher sensitivity for high-risk HPV detection |

| Recommended Use | Routine cervical cancer screening | Often combined with Pap smear for co-testing |

| Result Interpretation | Indicates cellular abnormalities | Indicates presence of high-risk HPV strains |

| Screening Interval | Usually every 3 years | Can extend screening interval to 5 years in some guidelines |

| Clinical Advantage | Effective for detecting existing abnormalities | Better for early risk prediction and prevention |

Source: Polaris Market Research Analysis

Insight by End-Use

In 2025, the hospital market segment accounted for the largest share of the global cervical dysplasia market valued at 49.0%. This high share is attributed to the high affordability and spending capacity of hospitals. Moreover, the presence of favorable reimbursement scenarios and the emergence of specialty hospitals, which are better equipped with advanced devices also contributing to the cervical dysplasia industry segment’s growth prospects. Several hospitals in the developing region are undertaking various initiatives to carry out an early diagnosis, thereby fueling the segment growth.

Geographic Overview

Geographically, the global market for cervical dysplasia is bifurcated into North America, Asia Pacific, Europe, Latin America, and MEA. The North America region accounted largest market share of 39.0% in 2025. Regional factors boosting the market growth of cervical dysplasia include government-sponsored screening programs, a rise in the prevalence of associated diseases, and support initiatives for the adoption of HPV testing. The North America has one of the most modern healthcare infrastructure in urban as well as rural areas. This fuels the demand for the medical devices and diagnostic kits, thereby fueling the growth in North America region.

The Asia Pacific is expected to witness significant growth at a CAGR of 9.39% during the forecast period due to rise in the government investment in the healthcare sector. Governments across major developed and developing countries such as India, China and Japan are investing heavily in the healthcare sector. These investments are aimed to improve infrastructure and access to rural areas. Consequently, the number of healthcare facilities in region is rising which is boosting the detection of cervical dysplasia in urban and rural areas. This in turn is driving the demand for the medical devices and diagnostic kits required in cervical dysplasia, thereby driving the growth in the region.

Source: Polaris Market Research Analysis

Competitive Insight

The competitive landscape is characterized by continuous innovation in diagnostic technologies, increasing focus on minimally invasive procedures, and the integration of molecular testing methods. Companies are prioritizing research and development to enhance the accuracy and efficiency of HPV testing, colposcopy, and biopsy tools. Strategic collaborations with healthcare providers and government programs are common, aiming to expand screening reach and improve early detection. Market players are also investing in digital pathology and AI-driven analysis to support faster and more precise diagnosis. Intense competition exists in both developed and emerging markets, driven by rising awareness and screening initiatives.

Key Players

- Qiagen N.V.

- Abbott Laboratories

- Hologic, Inc.

- Quest Diagnostics

- DYSIS Medical Ltd

- Micromedic Technologies Ltd.

- OncoHealth Corporation, Inc.

- CooperSurgical Inc.

- Roche

Industry Developments

May 2026: INOVIO announced that its partner for VGX-3100 in China, ApolloBio, revealed positive topline results from its Phase 3 trial of VGX-3100. It is an INOVIO's investigational DNA immunotherapy. It is developed as a potential treatment for cervical dysplasia. (Source: PRNewswire)

Cervical Dysplasia Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 770.31 Million |

| Market Size in 2026 | USD 821.69 Million |

| Revenue Forecast by 2034 | USD 1,382.57 Million |

| CAGR | 6.71% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–20243 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

cervical dysplasia market FAQ's

• The market size was valued at USD 770.31 Million in 2025 and is projected to grow to USD 1,382.57 Million by 2034.

• The market is projected to register a CAGR of 6.71% during the forecast period.

• A few of the key players in the market are Qiagen N.V., Abbott Laboratories, Hologic, Inc., Quest Diagnostics, DYSIS Medical Ltd, Micromedic Technologies Ltd., OncoHealth Corporation, Inc., CooperSurgical Inc., and Roche.

• In 2025, the hospital segment accounted for the largest share of 49.0%.

• In 2025, the diagnostic tests market segment held the largest revenue share of the market with 76.0%.

Download Sample Report of cervical dysplasia market

Please fill out the form to request a customized copy of the research report.