Critical Infrastructure Protection Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Critical Infrastructure Protection Market Summary

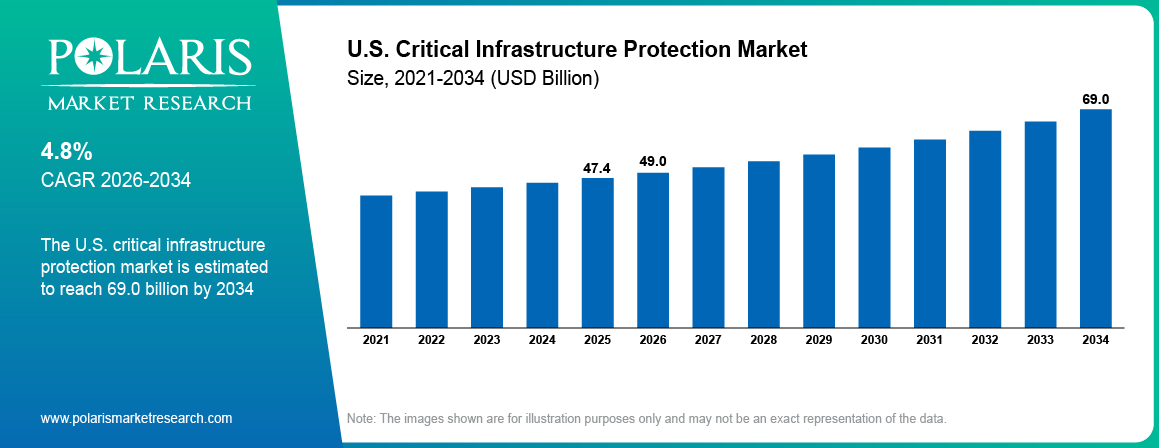

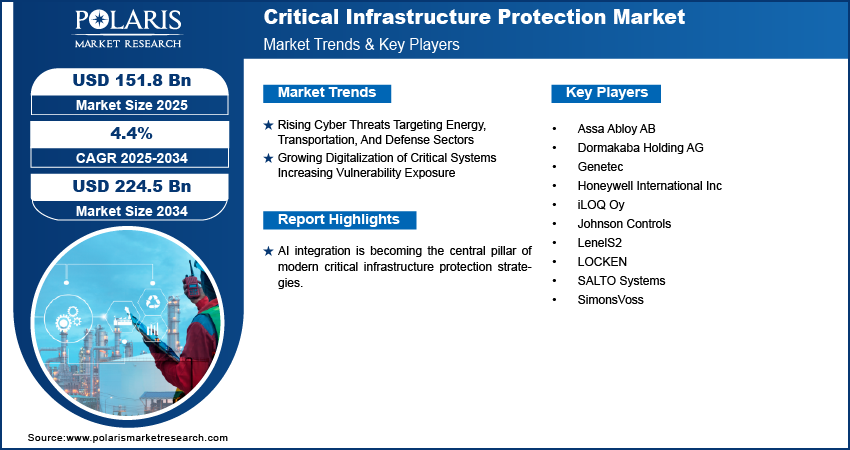

The global critical infrastructure protection market size was valued at USD 151.8 billion in 2025, growing at a CAGR of 4.4% from 2026 to 2034. The critical infrastructure protection (CIP) market comprises security solutions and services that help secure critical infrastructure in information technology and operational environments, such as utility infrastructure and industrial control systems.

Market Statistics

Key Takeaways

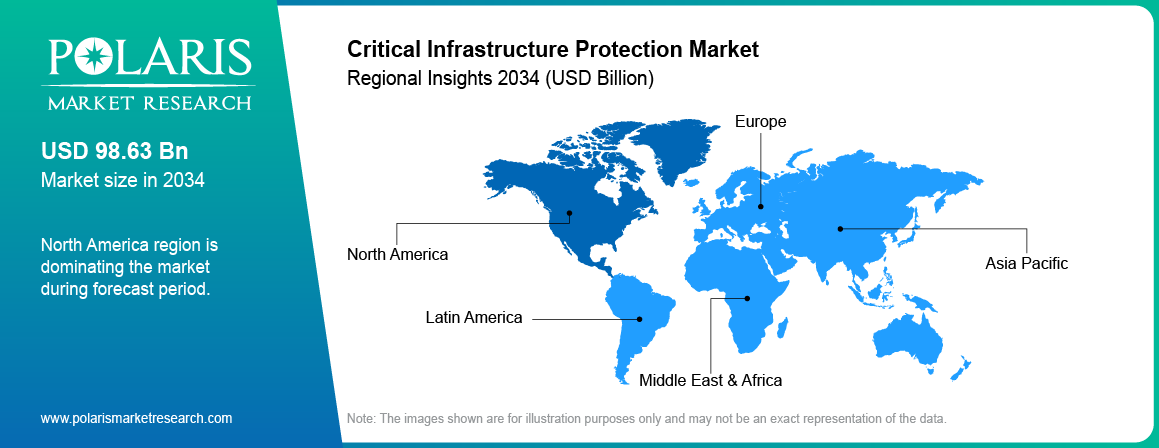

- In 2025, North America accounted for 36.5% of the global critical infrastructure protection market, driven by increased use and reliance on digital systems in critical environments. The North America CIP market leads due to its mature compliance infrastructure. The region also allocates large security budgets to the energy, defense, and transportation sectors.

- The Asia Pacific CIP market is expected to grow at the fastest rate. It is projected to have a CAGR of 4.7% from 2026 to 2034. The regional market is driven by the increased frequency of cyberattacks and natural disasters. Growth in this market is also being fueled by widespread infrastructure upgrades to improve critical infrastructure resilience in China, India, Japan, and Southeast Asia.

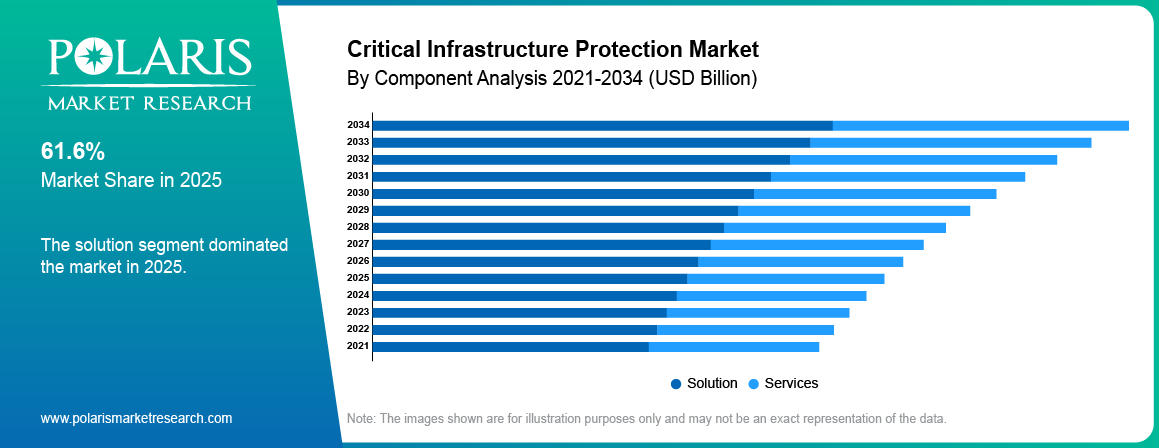

- In 2025, the solution segment accounted for 61.6% of revenue share. The segment’s growth is driven by the adoption of integrated platforms. This reflects the growing demand for unified CIP solutions that integrate physical security, identity and access management, and critical infrastructure cybersecurity monitoring.

- Cybersecurity is projected to grow the fastest, reflecting increased exposure to cyber threats as digital connectivity expands. This trend is also closely related to the convergence of IT systems, the growth of industrial IoT, and the increasing adoption of cloud-enabled operations by cybersecurity programs for critical infrastructure.

- The services segment is projected to grow at the fastest rate, with a CAGR of 4.9% from 2026 to 2034. Growth is driven by rising demand for managed services, continuous monitoring, and outsourced security support as infrastructure complexity increases.

Industry Dynamics

- Rising cyber threats to the energy, transportation, and defense sectors are driving growth. These include ransomware threats, cybersecurity risks in the value chain, insider threats, and collaborative threats targeting both digital and physical infrastructure.

- The growing digitalization of critical systems increases the threat of vulnerabilities, which will drive growth. Digital transformation has expanded the attack surface, making it imperative to enhance visibility in operational environments, increase network isolation, provide timely threat intelligence, and ensure readiness to respond to security incidents.

- Integrating legacy systems with modern cybersecurity solutions creates challenges to growth. Legacy systems may need step-by-step upgrading and enhanced security measures to ensure conformity with critical infrastructure protection standards.

- An increase in statutory global demand for resiliency and protection services further creates growth opportunities in the coming years. This is also contributing to the integration of managed security services for critical infrastructure.

AI Impact on Critical Infrastructure Protection Market

- Enhances threat detection speed and predictive security analytics.

- Automates and accelerates incident response times through complex system monitoring.

- Introduces new AI-powered vulnerabilities, which require specialized defense strategies.

- Creates demand for AI-skilled professionals and new solutions.

What is Critical infrastructure Protection?

Critical infrastructure protection involves a set of strategies, processes, and technologies designed to ensure the security of critical infrastructure resources. These include energy, transportation, communication, and water resources. Such resources are necessary for defending against physical and cyber threats. In practice, CIP encompasses not only physical security measures such as perimeter security, video surveillance, and access controls, but also cybersecurity for critical infrastructure, including monitoring, detection, and response. Currently, there has been increasing attention given to ensuring operational system security, including OT and SCADA systems.

Factors that play a significant role in fueling demand for critical infrastructure protection solutions include a surge in ransomware attacks on critical infrastructure and the ongoing rise in IT and operating system convergence. The market is also benefiting from regulatory pressures to enhance the resilience of critical assets and improve cyber-physical security.

Source: Polaris Market Research Analysis

The need for modernization in the wake of aging infrastructures is fueling the critical infrastructure protection market. Many infrastructures around the world were created many decades ago. This is increasing their vulnerability to degradation, inefficiency, and security risks. In October 2023, the U.S. Department of Energy (DOE) allocated USD 3.5 billion in funding for 58 projects in 44 states to improve the resilience of the U.S. electric grid. This is increasing the need for resilience in critical infrastructure cybersecurity. Security spending is now directly linked to security standards for resilience, reliability, continuity, and compliance. Governments and other private bodies are now interested in modernizing these systems to improve their resilience and reliability, as they tend to deteriorate over time. In addition, technologies such as advanced monitoring systems, automation systems, and predictive maintenance systems are now a necessity to ensure the uninterrupted provision of necessary services. For CIP consumers, modernization efforts focus on aligning cybersecurity and physical security policies within the scope of evolving critical infrastructure security standards.

The presence of IoT and digital transformation is also driving critical infrastructure protection market growth across industrial and utilities companies. The demand for a robust security framework to protect digital assets is also on the rise as interconnectivity and data-centricity continue to grow. This increase in interconnectivity, of course, creates a broader attack surface for cyber threats. Increasing integration of IT and operations systems also translates into the adoption of Zero Trust for critical infrastructure, enhancing OT visibility and extending continuous monitoring to contain the proliferation of attacks. Real-time monitoring and rapid identification of threats is possible by leveraging IoT-enabled devices and smart sensors. Organizations are also rapidly investing in network segmentation, data analytics, and advanced security systems to gain greater cyber resilience. For example, in January 2025, JPMorgan Chase launched the USD 1.5 Trillion Security and Resiliency Initiative to Improve Critical Industries. Therefore, with digital transformation, the way infrastructure is secured has changed. This allows a proactive, adaptive defense model that coordinates both physical protection and cyber protection. In CIP environments, these strategies also involve segmenting OT environments, implementing identity-based access management, and preparing for synchronized incident response across both cyber and physical security initiatives.

IT Security vs OT Security

| IT Security | OT Security |

| Focuses on data, networks, and enterprise systems | Focuses on industrial systems like SCADA, ICS, and operational environments |

| Protects information confidentiality and data integrity | Ensures operational continuity and physical process safety |

| Common in corporate IT environments | Common in energy, utilities, manufacturing, and transport sectors |

| Uses tools like firewalls, encryption, and access controls | Uses tools like network segmentation, anomaly detection, and SCADA monitoring |

| Can tolerate system downtime for updates | Requires minimal downtime due to continuous operations |

Source: Polaris Market Research Analysis

Drivers & Opportunities

Rising Cyber Threats Targeting Energy, Transportation, and Defense Sectors

The increasing instances and complexity of cyber attacks on the energy sector, transport sector, and defense systems trigger growth in the critical infrastructure protection market. The attack scope for malicious actors is increasing constantly. In January 2025, the UK government reported that Russian cyber-attacks against Ukrainian critical infrastructure had increased by 70%, and more than 4,300 incidents were detected throughout all of 2024. This is due to the rise in digitization of critical services and the adoption of advanced digital technologies, such as IoT, cloud computing, and automation, into critical operations. Thus, as the threat landscape expands, entities such as governments, regulatory bodies, and private stakeholders are investing heavily in cyber resilience, and demand for end-to-end protective services and solutions will continue to increase. From a control perspective, this requirement has been translating into an increasing number of demands for threat intelligence, network access controls, encryption tools, and incident response software for critical infrastructure security, OT security, and related purposes.

Growing Digitalization of Critical Systems Increasing Vulnerability Exposure

The rapid digital transformation of critical infrastructure systems is changing how critical services function. It further heightens their vulnerability to cyber and physical attacks, including in energy, transport, and healthcare infrastructure. Organizations that are part of critical infrastructure are now leveraging digital technologies such as the Internet of Things, cloud computing, artificial intelligence, and industrial automation to optimize efficiency and resilience. For example, in November 2025, Armada Technology and Galvanick partnered to provide edge computing and OT security solutions to industrial sectors worldwide. The biggest transformation trends in current infrastructure are driven by the integration of information technology and operational technology. Organizations are integrating these systems into enterprise IT networks and ultimately to the internet for visibility and remote management of these systems. Therefore, these systems are increasing the vulnerability to cyber intrusion. Consequently, SCADA security and ICS security investments are increasingly focused on network segmentation, continuous monitoring and anomaly detection, and remote access security.

Government Strategic Direction & Funding for CIP

Government initiatives are more closely linked to standards and compliance frameworks around the security of critical infrastructure, dictating how CIP procurement is approached. This ranges from provisions on risk assessment and baseline controls to incident reporting in key sectors.

| Country/Region | Strategic Direction | Funding/Initiatives |

| United States | National Security Memorandum on Critical Infrastructure Security and Resilience (2024): Defines federal roles, sets mandatory security/regulatory minimums, establishes sectoral risk management agencies, and directs coordinated funding and technical resources across sectors. | Federal grants, loans, and procurement for critical infrastructure resilience, sector-specific funding via agencies like DHS, DoD, CISA. |

| India | National Critical Information Infrastructure Protection Centre (NCIIPC) under IT Act Section 70A(1): Provides important measures for CII protection, coordination, audits, sectoral guidelines; CERT-In audits and sector-specific programs. | Direct government audits (CERT-In, NCIIPC), sectoral program funding, statutory budget allocations for technological upgrades and resilience programs. |

| OECD/EU | 78% of OECD countries have all-hazards CIP strategies. Most allocate funding for R&D and public-private sector coordination mechanisms. Policies focus on legal frameworks, threat/risk assessment, and joint initiatives. | National and regional government programs, public-private partnerships, and knowledge/expertise sharing platforms. |

| Germany | National Strategy for Critical Infrastructure Protection: Legal and policy guidance for baseline protection and sectoral risk assessment. | Federal and state budget allocations, sector-targeted grants. |

| United Kingdom | National cybersecurity strategy and critical national infrastructure protection projects focusing on national cyber resilience and incident readiness | National funding initiatives, sector development, public-private partnerships for national resilience against cyber threats |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Segmental Insights

Component Analysis

Based on component, the critical infrastructure protection market segmentation includes solution and services. For clarity, solutions in this market comprise hardware, such as sensors and access control readers, along with software for monitoring, analysis, and integration. Services encompass product integration, consultancy, and security services for critical infrastructure.

In 2025, the solution segment accounted for 61.6% of revenue. This is due to the rise in integrated platforms to ensure the safety, surveillance, and operational efficiency of essential assets. These systems allow coordination between infrastructures, helping maintain resilience and reduce downtime. Companies are investing in end-to-end protection solutions that include threat detection, incident management, access control, and network security to minimize cyber and physical threats. Therefore, the rise in automation, compliance with regulatory frameworks, and secure communication support this segment's dominance.

The services segment is expected to grow the fastest during the forecast period, with a CAGR of 4.6%. This is due to the rise in adoption of professional and managed services for continuous monitoring, threat assessment, and system maintenance. Organizations have started shifting towards specialized service providers for consultancy, integration, and maintenance support as infrastructure environments become more complex. Moreover, the increasing focus on proactive risk management and the need for customized protection strategies tailored to regional infrastructure types are further increasing the service demand. Managed security services for critical infrastructure are also on the rise. Organizations are seeking out around-the-clock monitoring, OT security expertise, and assistance with compliance reporting without adding more in-house staff. Therefore, with the shift toward subscription-based models and outsourced security operations, this segment is expected to grow.

Solution Type Analysis

In terms of solution type, the critical infrastructure protection market segmentation includes physical safety and security and cybersecurity. The cybersecurity segment is expected to witness the fastest growth due to the increased exposure of critical infrastructure systems to cyber threats as digital connectivity expands. Cloud computing, data analytics, and industrial IoT integration have increased the need for robust cybersecurity frameworks. These digital technology integration safeguard sensitive information and also help maintain smooth operations. Moreover, the implementation of advanced firewalls, intrusion detection systems, and encryption tools by organizations to protect their networked assets further boosts the expansion opportunities. This growing awareness around data integrity and national security has boosted the cybersecurity’s position in the market. The IT/OT convergence has further fueled demand for cybersecurity tools with visibility into OT infrastructure, SCADA security monitoring capabilities, and rapid response for cyber-physical security use cases.

The physical safety segment dominated the market in 2025. It accounted for 66.7% revenue share. This is due to the investments in perimeter protection, surveillance systems, and access control technologies. These technologies are keeping facilities safe from both physical threats and natural disasters. Also, they are intended to ensure the safety of the premises against threats and natural disasters. Investments made by the regional government, along with smart city initiatives, encourage enterprises to focus on improving their physical security infrastructure. In addition, there is increased awareness and real-time responses on the part of organizations with the development of integrated systems. This includes sensors, cameras, and automated alerts. Analytics solutions for video surveillance cameras, perimeter intrusion detection systems, identity access management systems, and other critical infrastructure security solutions are increasingly integrated with cybersecurity monitoring systems. These solutions support unified critical infrastructure protection programs.

Real-World Applications of Critical Infrastructure Protection

| Infrastructure | Example Use Case |

| Power Grids | Protecting grid operations, SCADA systems, and transmission networks from cyber and physical attacks |

| Water Systems | Securing water treatment plants, distribution systems, and monitoring sensors |

| Airports | Securing air traffic control, surveillance systems, and baggage handling operations |

| Telecom Networks | Protecting communication networks, data transmission systems, and network nodes |

| Oil & Gas | Securing pipelines, refineries, and monitoring systems from cyber and physical threats |

| Transportation Systems | Protecting rail networks, traffic control systems, and logistics infrastructure |

| Defense Infrastructure | Securing military communication systems, surveillance, and mission-critical operations |

| Financial Systems | Protecting banking networks, transaction systems, and sensitive financial data |

Source: Polaris Market Research Analysis

Advanced security tools will support better monitoring and faster response. Governments will introduce stricter regulations and compliance rules. IT and OT integration will increase demand for unified solutions. Future of CIP market will grow with rising cyber threats across key sectors. Infrastructure modernization and resilience investments will support growth

Source: Polaris Market Research Analysis

Regional Analysis

North America Critical Infrastructure Protection Market Overview

The North America critical infrastructure protection market accounted for 36.5% of global market share in 2025. This is due to the region’s advanced technological ecosystem and strong focus on infrastructure resilience. This growth in the region is also driven by the increased adoption of digital systems in critical sectors such as energy, finance, transportation, and communication. The increasing investments by governments and private-sector organizations to update legacy systems and deploy suitable cybersecurity solutions have contributed to market expansion. In 2025, the U.S. government allocated USD 103 million for the Cybersecurity and Infrastructure Security Agency (CISA) to advance cyberspace and make it more resilient and defensible. These development activities, well-founded infrastructure management frameworks, and organizational awareness of physical and cyber threats also support holistic protection strategies. The region’s proactive regulatory compliance efforts and public-private collaborations are also responsible for its lead position in the global market. Expenditure patterns are increasingly oriented towards enhancing OT security spending on energy grids, pipelines, ports, and public sector environments. In these sectors, regulatory compliance, continuity, and readiness to counter threats are important factors in expenditures for the CIP market in North America.

Asia Pacific Critical Infrastructure Protection Market

The Asia Pacific market is expected to grow at the fastest pace, with a CAGR of 4.7% from 2026 to 2034. The market is driven by rapid urbanization, industrialization, and the adoption of digital technologies, which increase expansion opportunities. Governments and enterprises in the region are working to update critical services, such as energy, transportation, and water infrastructure, to improve reliability and safety. Increased incidences of cyberattacks and natural disasters have also shifted the focus to developing resilient infrastructure networks with smart monitoring and response systems. The growing adoption of smart technology and IoT-based infrastructure solutions has changed the way the region thinks about and understands both physical and digital protection. Collectively, these factors signify that the Asia Pacific will be one of the most dynamic markets for the enhancement and protection of critical infrastructure. China, India, Japan, South Korea, and Australia are the key emerging markets where investment in critical infrastructure resilience, spending on industrial cybersecurity, and smart city development are converging.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis Report

The competitive landscape of the critical infrastructure protection (CIP) sector is characterized by diverse vendor strategies and investments aimed at securing sustainable value chains. The top critical infrastructure protection market players are leveraging competitive intelligence and strategy to adapt to economic and geopolitical shifts across the world, in both developed and emerging markets. Continuous advancements in cybersecurity technology and the integration of physical security remain the leading factors driving the sector's growth. In addition, vendors are currently pursuing expansion opportunities through mergers and acquisitions and/or strategic alliances to increase their regional footprint and product portfolio, which they can capitalize on for sustained growth. The process of consolidation and insights from experts on development strategies will continue to shape an ecosystem across industry, where scale, the ability to innovate, and one's capacity to manage supply chain disruption will be essential factors for establishing competitive positioning and sustainable growth opportunities into the future.

For buyers evaluating CIP vendors, evaluation factors are evolving and heavily depend on the integration of physical and cybersecurity tools for OT, as well as on the processing of related reports and responses. There are different categories of vendors. These include physical, OT, or ICS cybersecurity providers specializing in SCADA monitoring, and those offering combined solutions for cyber and physical security. Major companies operating in the critical infrastructure protection industry include Assa Abloy AB, Dormakaba Holding AG, Genetec, Honeywell International Inc, iLOQ Oy, Johnson Controls, LenelS2, LOCKEN, SALTO Systems, and SimonsVoss.

Key Players

- Assa Abloy AB

- Dormakaba Holding AG

- Genetec

- Honeywell International Inc

- iLOQ Oy

- Johnson Controls

- LenelS2

- LOCKEN

- SALTO Systems

- SimonsVoss

Industry Developments

April 2026: ESET expanded its XDR platform with Cloud Workload Protection. Designed for securing virtual machines in AWS, Azure, and GCP. (Source: eset.com)

April 2026: Nokia and Cinia launched a managed DDoS protection service. Uses Nokia Deepfield Defender for network security. (Source: samenacouncil.org)

April 2025: Forcepoint launched a Data Security Cloud platform. It focuses on securing hybrid environments and improving data protection. (Source: forcepoint.com).

Critical Infrastructure Protection Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021–2034)

- Solution

- Hardware

- Software

- Services

- Professional Services

- Managed Services

By Solution Type Outlook (Revenue, USD Billion, 2021–2034)

- Physical Safety and Security

- Physical Identity and Access Control Systems

- Perimeter Intrusion Detection Systems

- Video Surveillance Systems

- Screening and Scanning

- Others

- Cybersecurity

- Encryption

- Network Access Controls and Firewalls

- Threat Intelligence

- Others

By Vertical Outlook (Revenue, USD Billion, 2021–2034)

- Financial Institutions

- Government & Utilities

- Defense

- Transport & Logistics

- Energy & Power

- Oil & Gas

- Commercial Sector

- Telecom

- Chemical & Manufacturing

- Water

- Mining

- Others

By Regional Outlook (Revenue, USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Critical Infrastructure Protection Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 151.8 billion |

| Market Size in 2026 | USD 157.4 billion |

| Revenue Forecast by 2034 | USD 224.5 billion |

| CAGR | 4.4% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Critical Infrastructure Protection Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Critical Infrastructure Protection Market FAQ's

The global critical infrastructure protection market is projected to reach USD 224.5 billion by 2034, growing at a 4.4% CAGR.

Critical infrastructure protection includes solutions and services for physical security, cybersecurity, and threat intelligence systems.

Energy and power, defense, and government utilities heavily rely on CIP solutions for security.

AI enhances threat detection speed and enables predictive security analytics. It also automates incident response and monitors complex systems.

North America leads with 36.5% market share due to advanced digital systems adoption and strong regulatory frameworks.

The cybersecurity segment is expected to witness the fastest growth during the forecast period.

Integrating legacy systems with modern cybersecurity solutions is the primary challenge, as many aging infrastructure systems are prone to inefficiency and security vulnerabilities, making modernization complex and costly for organizations.

Download Sample Report of Critical Infrastructure Protection Market

Please fill out the form to request a customized copy of the research report.