Global Cyber Warfare Market Share Size, Share Analysis Report, 2024-2032

REPORT DETAILS

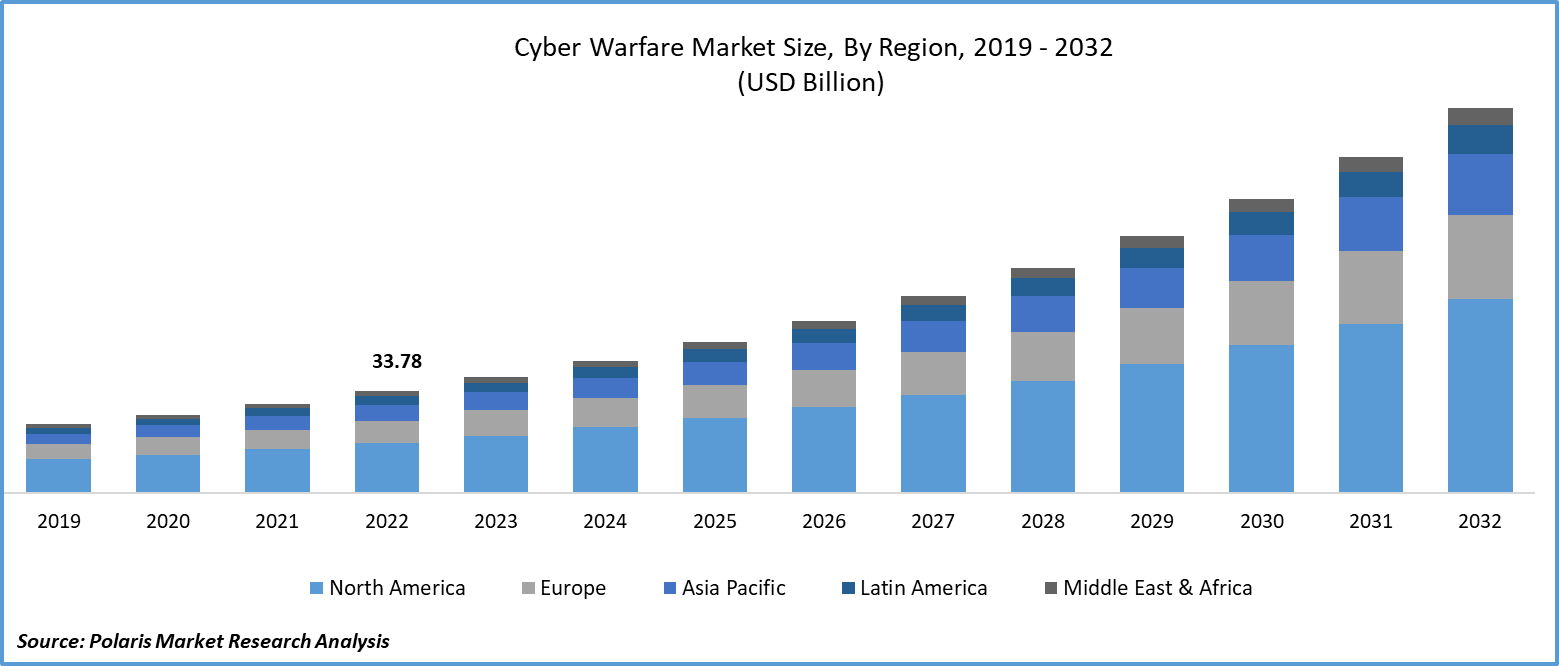

The global cyber warfare market was valued at USD 38.51 billion in 2023 and is expected to grow at a CAGR of 14.3% during the forecast period.

Governments and international organizations are increasingly prioritizing cybersecurity due to the rising security threats emerging from cyberspace. These challenges have sparked significant concerns about national security, underscoring the urgent need for a strong cybersecurity framework. As a result, government entities, military forces, and various agencies are taking extensive measures to safeguard their digital infrastructure and internet-connected devices in order to prevent potential cyber-attacks.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The process of digitization has gained momentum in emerging nations. However, it has also led to an increase in cyber warfare, which poses a significant challenge to their growth. In response, several countries have invested in cybersecurity, creating dedicated units to combat cyber espionage and data breaches, especially in the military and defense sectors. This growing demand for cybersecurity is expected to drive the cyber warfare market in the near future.

The U.S. Federal Government has taken on various initiatives to counter cyber-attacks and consistently showcases its capabilities in cyber warfare to deter potential adversaries from sophisticated attacks. The government is actively strengthening its cyber capabilities by planning to establish 133 teams for its "cyber mission force" between 2018 and 2027.

Additionally, it is engaged in proactive training and development programs for military personnel through institutions like the U.S. Army Cyber Center of Excellence (CCoE), which focuses on cyberspace operations, signal/communications networks, and information services. Furthermore, the increased defense budget allocated to safeguard cyberspace protect Federal networks, and critical infrastructure from cyber-attacks is expected to drive market growth in the foreseeable future.

Source: Polaris Market Research Analysis

Industry Dynamics

Growth Drivers

-

The increasing significance of cyber warfare in global defense and security

The adoption of cyber warfare systems worldwide is expected to be primarily driven by the rise in defense expenditure aimed at enhancing government efficiency and cybersecurity capabilities. The market growth is also anticipated to be propelled by agendas that focus on government IT infrastructure modernization, facility upgrades, and addressing cybersecurity vulnerabilities in the coming years.

The global threat landscape is being reshaped by continuous progress in IT technology and the increasing capabilities of cyber weapons, which pose a significant threat to national security. Cyber-related threats are now recognized as some of the most prevalent risks worldwide. Cyber warfare has emerged as a substantial threat to nations, surpassing even terrorism in its significance. Reducing losses caused by rising cyber-attacks, which often lead to economic disruptions in countries, has become a major concern.

Report Segmentation

The market is primarily segmented based on component, type, application, and region.

| By Component | By Type | By Application | By Region |

|

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report: Request Customization

By Application Analysis

-

Defense segment accounted for the largest share of the market in 2022

The defense segment held the largest share. The military and defense industry's heavy reliance on communication and information technology has made it susceptible to cyber risks. Recognizing this vulnerability, the defense sector has increased its funding for cybersecurity units to counter and deter potential threats posed by national and state hackers.

The introduction of new technologies and the integration of the Internet of Things (IoT) in defense operations are pivotal factors driving the adoption of cyber warfare systems in the defense sector. These advancements not only enhance the efficiency of military operations but also introduce new avenues for cyber threats. As a result, there is a pressing need to implement robust cybersecurity measures, including cyber warfare systems, to safeguard sensitive military data, critical infrastructure, and communication networks from cyber-attacks.

Additionally, the ongoing development of existing cybersecurity technologies and posture is anticipated to boost further the application of cyber warfare systems in the defense sector. As cyber threats continue to evolve, the defense industry is actively striving to stay ahead by investing in innovative solutions and strategies to protect national security interests. Consequently, the integration of advanced cyber warfare systems becomes crucial in ensuring the defense sector's resilience against ever-changing and sophisticated cyber threats.

The government segment will grow at a substantial pace. The rise in cyber threats has prompted developed nations to focus on building resilience and implementing comprehensive national cybersecurity strategies. These strategies are multifaceted, involving robust policies, advanced technologies, and stringent regulations aimed at safeguarding government systems, critical infrastructure, and sensitive data from cyber-attacks. Such efforts are vital in ensuring the security and stability of the nation, especially considering the increasing frequency of cyber-attacks, which can have far-reaching consequences on both the public and private sectors.

As the threat landscape continues to evolve, governments are investing significantly in enhancing their cybersecurity capabilities. This includes developing innovative solutions, fostering international collaborations, and promoting cybersecurity education and awareness among citizens and businesses. By adopting these proactive measures, governments aim to mitigate cyber vulnerabilities, strengthen their digital defenses, and ensure the resilience of their critical systems in the face of growing cyber threats.

Source: Polaris Market Research Analysis

Regional Insights

-

The demand in North America garnered the largest share in 2022

The North America region dominated the global market. There has been a notable increase in the cyber defense budget in the region. The governments in this region are allocating substantial resources to enhance their cyber capabilities, recognizing the critical importance of protecting digital infrastructure from evolving cyber threats. Concerted effort by governments in the region to safeguard their digital assets. These efforts encompass strengthening cybersecurity approaches, implementing advanced technologies, and enforcing stringent regulations to fortify the resilience of digital systems against cyber-attacks.

Additionally, the establishment of specialized cybersecurity units and the deployment of robust cybersecurity frameworks within government agencies, military organizations, and the defense sector are contributing significantly to market growth. These dedicated units and frameworks are essential in mitigating cyber risks, ensuring data security, and defending against potential cyber threats, bolstering the overall cybersecurity posture of the region.

Asia Pacific will grow at a rapid pace throughout the forecast period. The region's rapid growth in the market can be attributed to proactive government initiatives, economic expansion, technological advancements, and the growing necessity to defend against cyber-attacks. These factors collectively create a conducive environment for the adoption and development of cyber warfare applications, leading to the region's remarkable growth in this sector.

Furthermore, the region is experiencing a swift pace of technological advancements in cyberspace. These advancements include innovative cybersecurity tools, threat intelligence systems, and data protection technologies. As the cyber landscape evolves, nations in the Asia Pacific are investing in cutting-edge solutions to stay ahead of potential cyber-attacks and secure their digital domains.

Another crucial factor fueling the market growth in the region is the increasing frequency of cyber-attacks. Governments are recognizing the urgency of bolstering their cyber defenses due to the rising threats. Consequently, these cyber-attacks are influencing defense budget allocations, prompting governments to invest substantially in cyber warfare solutions. This heightened focus on cybersecurity is expected to drive the market in the foreseeable future.

Source: Polaris Market Research Analysis

Key Market Players & Competitive Insights

Some of the major players operating in the global market include:

- AIRBUS

- BAE Systems

- Booz Allen Hamilton Inc.

- DXC Technology Company

- General Dynamics Corporation

- Intel Corporation

- IBM Corporation

- Leonardo S.p.A.

- Lockheed Martin Corporation.

- Northrop Grumman

- Raytheon Technologies Corporation

- L3Harris Technologies, Inc.

Recent Developments

- In February 2026: Northrop Grumman got a USD 1.2 billion deal with the U.S. Air Force for an AI cyber tool that handles both attacks and defense for military missions.

- In January 2026: Palantir won a five-year, USD 480 million deal with U.S. Cyber Command to grow its Gotham and Apollo tools to help find and track secret digital threats.

- In December 2025: Poland’s defense team gave a EUR 850 million (USD 920 million) deal to Leonardo and Thales groups to build a center that runs the nation's cyber defense.

- In November 2025: Lockheed Martin started its Cyber Resilience Platform, a high-safety cloud tool for the U.S. Navy that helps keep their data safe and ready for action.

- In May 2025: The U.S., U.K., France, Germany, and other NATO allies issued a warning about a Russian cyber campaign targeting defense systems bound for Ukraine and NATO tech sectors. This shows rising cross-border cyber threats and is driving higher investment in allied cyber defenses and supply chain protection.

- In July 2025: St. Paul, Minnesota, faced a coordinated ransomware attack by the “Interlock” group, disrupting city services, payment portals, and internal systems. The attack prompted a state of emergency and deployment of the National Guard, highlighting how local infrastructure is now a target in cyber warfare.

Cyber Warfare Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 43.92 billion |

| Revenue forecast in 2032 | USD 127.63 billion |

| CAGR | 14.3% from 2024 – 2032 |

| Base year | 2023 |

| Historical data | 2019 – 2022 |

| Forecast period | 2024 – 2032 |

| Quantitative units | Revenue in USD billion and CAGR from 2024 to 2032 |

| Segments covered | By Component, By Type, By Application, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

Source: Polaris Market Research Analysis

Gain profound insights into the 2024 Cyber Warfare Market with meticulously compiled statistics on market share, size, and revenue growth rate by Polaris Market Research Industry Reports. This thorough analysis not only provides a glimpse into historical trends but also unfolds a roadmap with a market forecast extending to 2032. Immerse yourself in the comprehensive nature of this industry analysis through a complimentary Download Sample Report.

Cyber Warfare Market FAQ's

The global cyber warfare market is expected to reach USD 58.29 billion by 2030.

The market is projected to grow at a compound annual growth rate (CAGR) of 25.2% during the forecast period.

The hardware segment is anticipated to hold a major share due to demand for advanced cyber defense equipment.

North America is expected to lead the market, supported by strong cybersecurity investments by government and defense agencies.

The network security segment is a key growth driver as organizations focus on protecting critical infrastructure and communication networks.

Growth is driven by increasing government spending on cyber defense, rising incidence of cyberattacks, and the need for advanced threat mitigation solutions.

Download Sample Report of Cyber Warfare Market

Please fill out the form to request a customized copy of the research report.