Equine Healthcare Market Trends Analysis | Industry Report 2026-2034

REPORT DETAILS

REPORT DETAILS

Equine Healthcare Market Summary

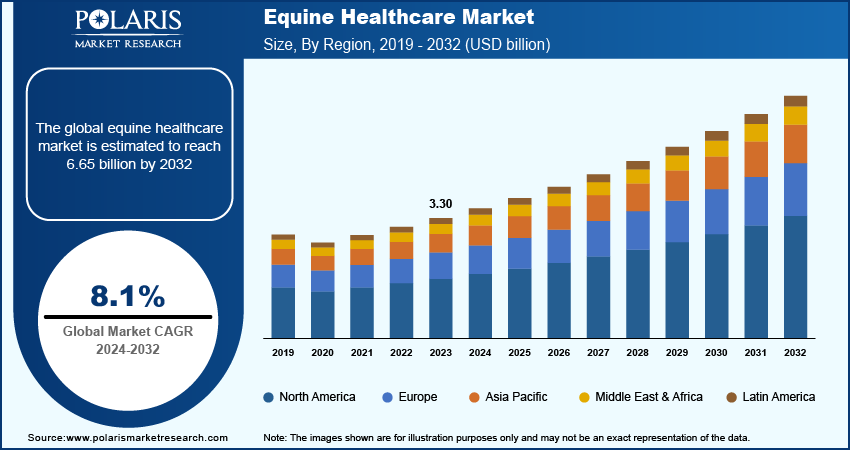

The equine healthcare market size was valued at USD 3.85 billion in 2025, and is expected to register a CAGR of 8.2% from 2026 to 2034. Rising awareness of equine wellness and broader access to advanced veterinary services drive the market growth. Also, continuous innovation in pharmaceuticals, vaccines, diagnostics, orthobiologics, and software platforms is expected to boost the market expansion in the coming years.

Market Statistics

Key Takeaways

- North America held the dominant share of 49.80% in 2025. The availability of advanced veterinary infrastructure and high level of investments in equine healthcare fueled the regional market growth.

- The Asia Pacific equine healthcare market is estimated to register the highest CAGR of 8.6% during the forecast period. The growth is attributed to the increasing investments in equine health infrastructure and the expanding equestrian industry in countries such as China and Australia.

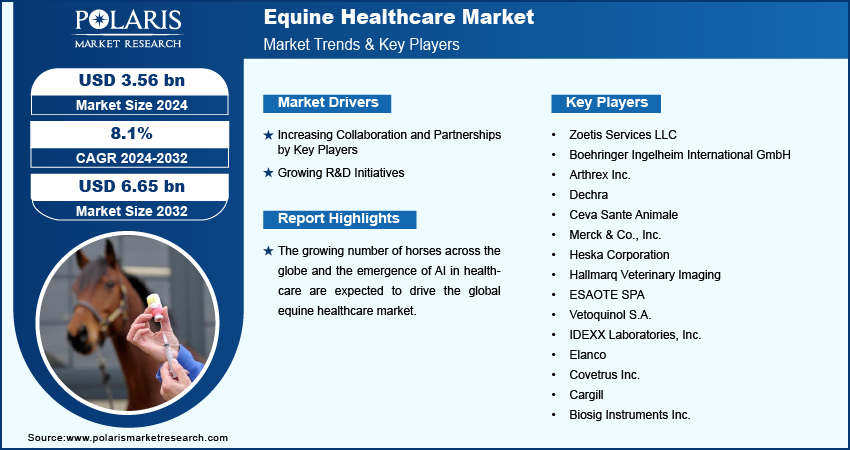

- The pharmaceuticals segment held the largest revenue share of 30.52% in 2025. Advancements in veterinary medicines and the development of new pharmaceutical products boost the segment dominance.

- The parasitic infection segment led the market revenue share with 29.98% in 2025. Increased awareness among horse owners and veterinarians about the importance of regular parasite management fuels the dominance.

- The veterinary hospitals & clinic segment held the largest share of 40.84% in 2025. The growing veterinary practices and their focus on offering high-quality and specialized services boost this segment’s dominant share.

Industry Dynamics

- Increasing spending by equine owners, veterinarians, and equestrian organizations on preventive care, diagnostics, and therapeutics drives the market growth.

- Rising innovation in diagnostics, orthobiologics, and long-acting therapies is creating commercial opportunities across equine care pathways.

- Growing disease burden and surging preference for preventive and performance-oriented care are expected to boost the market expansion during the forecast period.

- High cost associated with treatment is hindering the market growth.

To Understand More About this Research: Download Sample Report

Market Definition and Scope

The equine healthcare market includes diagnostic and treatment products and technologies used to manage equine health. The equine health ecosystem consists of interconnected stakeholders. Horse owners and breeders generate end-user demand for equine healthcare solutions. Veterinarians and specialty referral centers influence treatment selection. Manufacturers supply products and technologies. Distribution channels such as clinics, equestrian facilities, and e-commerce platforms provide access to the product and support recurring purchases.

Rising disease burden, access to veterinary infrastructure, and the growing preference for preventive and performance-oriented care propel the expansion. Increasing ownership of horses and the intensity of equestrian activity are industry trends. Growing R&D initiatives contribute to the equine healthcare industry growth. R&D results in new treatments, therapies, and diagnostic tools for equine health. For example, in August 2024, Hyloris Pharmaceuticals developed HY-095. This is a long-acting injectable proton pump inhibitor for treating Equine Gastric Ulcer Syndrome. The company claims that the formulation will improve drug delivery and minimize dosing frequency.

The increasing collaboration and partnerships among key players propel the market for equine healthcare. Collaborative efforts lead to the creation of new service models, such as telemedicine for equine care, mobile veterinary units, and abuse care. Such strategic initiatives contribute to the growth of the horse healthcare industry.

Market Dynamics

Increasing Horse Population: The population of horses is growing worldwide. According to FAO stats, there were about 56.2 million horses globally in 2024. An increased horse population can lead to health problems, such as diseases, injuries, and chronic conditions. This raises the need for diagnostic services, treatments, and specialized care. This creates a higher demand for equine healthcare professionals and facilities. Horse owners are also more willing to invest in preventive care and maintenance for performance. This results in ongoing demand for vaccinations, deworming, anti-infectives, rehabilitation products, reproductive care, imaging services, and digital monitoring tools. The effect is particularly strong in regions with active sports, breeding, or leisure-riding communities. Thus, rising horse population drives the industry growth.

Emergence of AI in Equine Health: AI in equine healthcare helps create personalized treatment plans. Horse’s specific data, including health history, genetics, and current condition, is used while planning the AI-based treatment. This level of customization improves treatment outcomes. It increases demand for tailored healthcare solutions.. In July 2024, Boehringer Ingelheim and Sleip revealed that they used AI technology for equine lameness diagnosis. Further, AI is used to improve clinical workflow. The technology helps veterinarians interpret movement patterns, imaging results, and longitudinal health data more efficiently. AI-enabled software are expected to support earlier intervention. It is used for better rehabilitation planning and stronger decision support for referral care. Such benefits could expand the adoption of equine healthcare technology in the coming years.

Restraints

High Cost Associated with Treatment: The high cost of treatment places a significant financial burden on horse owners. It affects the owners with multiple horses. It creates financial difficulties for those who have horses with chronic conditions. This financial strain discourages owners from investing in additional horses. Cost sensitivity is especially relevant for elective and premium treatments, such as advanced imaging, specialized surgery, orthobiologics, and long-term rehabilitation. High-value sport and breeding horses often justify greater spending. Thus, the demand for equine treatment is restricted by owner segments with tighter budgets.

Opportunities

Growing Emphasis on Preventive Healthcare: Preventive care is a crucial revenue pillar across the industry. Horse owners seek to reduce the risk of severe illness. They focus on avoiding costly emergency interventions. This shift propels the adoption of product categories that support regular care utilization. As a result, there is a rising demand for vaccination schedules, parasite control, and reproductive health management. Owners are also emphasizing routine diagnostics and nutritional support. Hence, increasing focus on preventive equine healthcare would create lucrative opportunities in the coming years.

Expansion of Equestrian Sports: The popularity of racing, show jumping, dressage, endurance riding, and other competitive activities is growing across the world. The growing equine sports industry is increasing demand for specialized equine care. High-performance horses often require more frequent diagnostics, imaging, rehabilitation, pain management, and injury prevention support. It creates sustained demand for advanced equine orthobiologics, pharmaceuticals, wearables, and performance-monitoring tools. Thus, expansion of equestrian sports would provide opportunities during the forecast period.

Segmentation Analysis

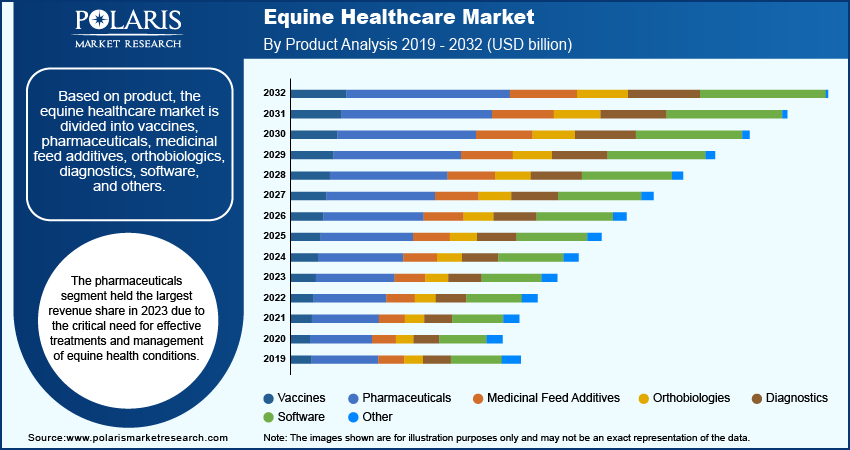

By Product Analysis

The pharmaceuticals segment held the largest revenue share in 2025. The critical need for effective treatments and management of equine health conditions propels the growth of the equine pharmaceuticals market. This segment includes medications, such as antibiotics, anti-inflammatory drugs, pain relievers, and others. These medicines are vital for treating infections, injuries, and long-term diseases in horses. The growing incidence of health problems in horses and the rising need for new and effective drug therapies contribute to this segment's leadership. Additionally, improvements in drug formulations and the creation of new pharmaceutical products targeting specific conditions enhance this strong position. Moreover, these pharmaceuticals meet the needs for both immediate and ongoing care for musculoskeletal, infectious, gastrointestinal, respiratory, and pain-related issues.

The software segment is expected to record the fastest growth rate in the coming years. Increasing use of technology in veterinary practices drives the growth. Software solutions, such as electronic health records (EHRs), practice management systems, and diagnostic software, are used widely. They provide improvements in data management, treatment planning, and overall efficiency. The AI and machine learning integration in these tools enhances their abilities. This technology allows for precise diagnostics, better disease monitoring, and improved treatment plans. Veterinary practices adopt new technologies to enhance care and operational efficiency. In this area, practice management platforms help manage scheduling, billing, inventory, and case tracking. Imaging software is used to improve diagnostic interpretation. Telehealth software supports continuity of care between in-person visits. It supports the evolution of equine healthcare beyond conventional therapeutics into data-driven care delivery.

By Indication Analysis

The parasitic infection segment dominated the market share in 2025. The widespread impact of parasitic infections in horses propels the segment dominance. Parasites such as worms, lice, and bots cause a range of issues. They can cause digestive problems, skin infections, and overall poor health. Advances in parasite control include the development of broad-spectrum dewormers and targeted therapies. These innovations drive growth in this segment. Also, increasing awareness about the importance of regular parasite management supports this growth. This factor drives the demand for preventive parasite control. The infections require repeated intervention and regular monitoring. It makes them a recurring source of product demand. Thus, the segment remain commercially important. They also reinforce the value of preventive care programs. This supports demand for parasiticides, diagnostics, and routine veterinary consultations.

The equine herpes virus (EHV) segment is expected to record the highest growth rate during 2026-2034. This is due to its serious effects on horse health, such as respiratory disease, reproductive problems, and neurological issues. Improvements in vaccine development and diagnostic tools focus on better prevention and early detection of the virus. Such advancements are fueling the segment growth. Disease outbreaks can affect competition schedules, breeding plans, and transport activities. It propels the demand for equine herpes virus treatment. This elevates the economic impact of EHV beyond direct treatment alone. As a result, faster EHV diagnostics, monitoring, and vaccination strategies are likely to remain commercially relevant.

By Distribution Channel Analysis

In 2025, the veterinary hospitals and clinics segment led the market share in 2025. Veterinary hospitals and clinics provide routine check-ups, emergency care, diagnostics, and advanced treatments. They are vital for keeping equines healthy. Horse owners seek professional veterinary care. These institutions have extensive infrastructure, specialized staff, and advanced equipment. Thus, the segment witnesses the leading share. The increasing veterinary practices and their dedication to providing high-quality and specialized services support this segment leading position.

The e-commerce segment is projected to grow at a considerable pace during the forecast period owing to the rising adoption of online platforms for purchasing equine health products and medications. E-commerce offers horse owners easy access to a variety of products, including pharmaceuticals, supplements, and diagnostic tools, without the need to visit physical stores. The growth of this segment is further driven by the increasing preference for online shopping, the availability to compare products and prices, and the convenience of home delivery. The e-commerce sector is set to capture a larger share of the market as more companies develop robust online sales channels and expand their digital presence. Digital purchasing behavior can improve price transparency. It will help brands expand their reach, especially in regions with fragmented physical distribution.

Regional Insights

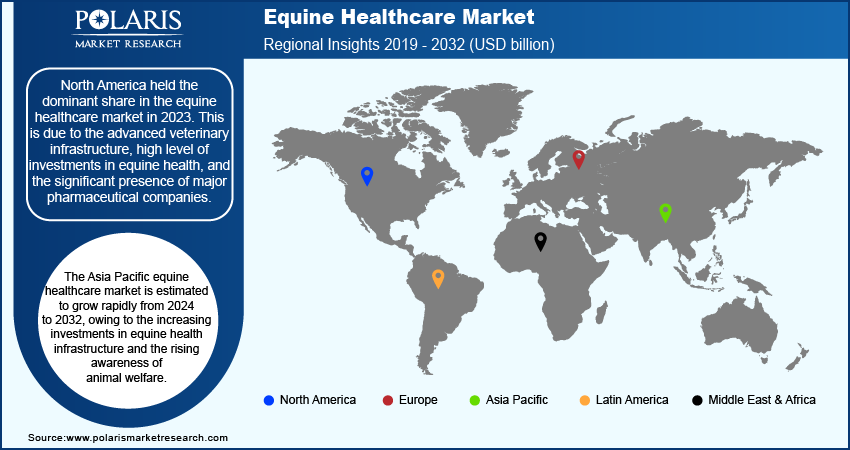

North America held the dominant share in the global market in 2025. Advanced veterinary infrastructure and the high level of investments in equine healthcare fuel the market dominance. The presence of major pharmaceutical and biotechnology companies boosts the growth. The U.S. dominated the regional market with its well-established network of veterinary clinics, hospitals, and research institutions that focus on equine care. The wide number of horse owners and the prevalence of competitive equine sports contribute to the high demand for comprehensive veterinary services and products. Additionally, strong regulatory frameworks and substantial spending on advanced treatments and diagnostics drive the North America equine healthcare market expansion.

The Asia Pacific equine healthcare market is estimated to grow rapidly during the forecast period. This is owing to the increasing investments in equine health infrastructure, rising awareness of animal welfare, and the expanding equestrian industry in countries such as China and Australia. The growing number of horse owners and the development of competitive and recreational equestrian activities in Asia Pacific contribute to the surge in demand for equine health products and services. Furthermore, improvements in veterinary care standards and increasing access to advanced treatments and diagnostics are driving market expansion in this region.

The Europe equine healthcare market is mature and strategically important. Its growth is supported by established equestrian traditions and focus on strong animal health standards. Active participation in the sport horse, breeding, and leisure segments also propels the industry growth. The region offers steady demand for vaccines, diagnostics, imaging, pharmaceuticals, and rehabilitation solutions. However, innovation-led adoption may be relevant in high-value equine care settings.

Key Market Players and Competitive Insights

Key market players are investing heavily in research and development to expand their offerings, which will fuel the equine healthcare market growth. Market participants are engaging in various activities to grow their presence worldwide. Key developments include new product launches, international partnerships, increased investments, and mergers and acquisitions among companies. A few major market players are Zoetis Services LLC, Elanco, Ceva Sante Animale, Heska Corporation, Esaote SPA, and Covetrus Inc.

A mix of pharmaceutical scale, diagnostic capability, imaging expertise, software integration, and channel reach influence the competition in the industry. Established animal health companies maintain strength in broad therapeutic portfolios. Specialized players differentiate through rapid diagnostics, imaging systems, remote monitoring, and orthobiologic innovation. With evolving market scenario, portfolio depth and the ability to support integrated care pathways would become important competitive advantages in the coming years.

List of Key Companies

- Arthrex Inc.

- Biosig Instruments Inc.

- Boehringer Ingelheim International GmbH

- Cargill

- Ceva Sante Animale

- Covetrus Inc.

- Dechra

- Elanco

- ESAOTE SPA

- Hallmarq Veterinary Imaging

- Heska Corporation

- IDEXX Laboratories, Inc.

- Merck & Co., Inc.

- Vetoquinol S.A.

- Zoetis Services LLC

Equine Healthcare Industry Recent Developments

- June 2025: bioMérieux launched VETFIRE, a ready-to-use PCR diagnostic kit. The kit is designed for the rapid detection of equine infectious respiratory diseases. The solution provides reliable results in under 20 minutes. It allows for the simultaneous identification of seven pathogens using high-sensitivity PCR technology.

- April 2025: Creative Science, a subsidiary of CIMA Animal Health, acquired Astaria Global. This acquisition will strengthen Creative Science's equine healthcare portfolio. It will expand access to innovative orthobiologic therapies for pain management and inflammatory airway disease. This will improve veterinary treatment options and support better overall horse health and wellness.

Report Coverage

The equine healthcare market report provides a structured assessment of market size, forecast trends, demand patterns, and competitive developments. It emphasizes key regions across the globe. The study provides a better understanding of the product to the users. It analyzes the technologies that are gaining traction around the globe. Furthermore, it covers an in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions. The report focuses on various key aspects such as competitive analysis, product, indication, activity, distribution channel, region, and growth opportunities. The research report is designed for CXOs, strategic planners, investors, business development teams, marketers, consultants, and industry participants. It is intended to help stakeholders identify market opportunities and benchmark competition. The report also helps them align growth strategy with shifting demand dynamics.

Report Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Vaccines

- Pharmaceuticals

- Parasiticides

- Anti-infectives

- Anti-inflammatory & Analgesics

- Other Pharmaceuticals

- Medicinal Feed Additives

- Orthobiologics

- Diagnostics

- Diagnostic Test Kits

- Diagnostic Equipment

- Software

- Practice Management Software

- Imaging Software

- Telehealth Software

- Other Software

- Other

By Indication Outlook (Revenue, USD Billion, 2021–2034)

- Musculoskeletal Disorders

- Parasitic Infections

- Equine Herpes Virus

- Equine Viral Arteritis (EVA)

- Equine Influenza

- West Nile Virus

- Tetanus

- Other

By Activity Outlook (Revenue, USD Billion, 2021–2034)

- Sports/Racing

- Recreation

- Other

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Veterinary Hospitals & Clinics

- E-commerce

- Equestrian Facilities

- Other

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Equine Healthcare Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 3.85 billion |

| Market Size in 2026 | USD 4.16 billion |

| Revenue Forecast in 2034 | USD 7.80 billion |

| CAGR | 8.2% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market was valued at USD 3.85 billion in 2025. It is projected to reach USD 7.80 billion by 2034, at a 8.2% CAGR during 2026–2034.

Rising equine sports activities and growing disease prevalence drive the market growth. The expansion is also driven by increasing horse ownership and advances in regenerative veterinary medicine. Greater awareness of preventive equine care is also a primary market growth driver.

The pharmaceuticals segment dominated the market in 2025. The dominance is driven by high demand for parasiticides, anti-inflammatories, and anti-infective treatments.

North America held the largest global market share in 2025. Its large horse population and advanced veterinary infrastructure boost the dominance. Further, significant healthcare expenditure on performance horses and strong equestrian culture fuel the regional market growth.

Arthrex Inc., Biosig Instruments Inc., Boehringer Ingelheim International GmbH, Cargill, Ceva Sante Animale, Covetrus Inc., Dechra, Elanco, ESAOTE SPA, Hallmarq Veterinary Imaging, Heska Corporation, IDEXX Laboratories, Inc., Merck & Co., Inc., Vetoquinol S.A., and Zoetis Services LLC are among the key market players.

AI is used for lameness detection, treatment planning, data analysis, and imaging support. The technology is also used in personalized health management.

E-commerce improves access to health products, supports recurring purchases, and increases price transparency. It helps brands expand beyond traditional physical distribution.

Wearables help track heart rate, movement, and training response. This enables owners and clinicians to identify health issues sooner.

Download Sample Report of Equine Healthcare Market

Please fill out the form to request a customized copy of the research report.