Global Fermentation Chemicals Market Size, Share Analysis Report, 2026-2034

REPORT DETAILS

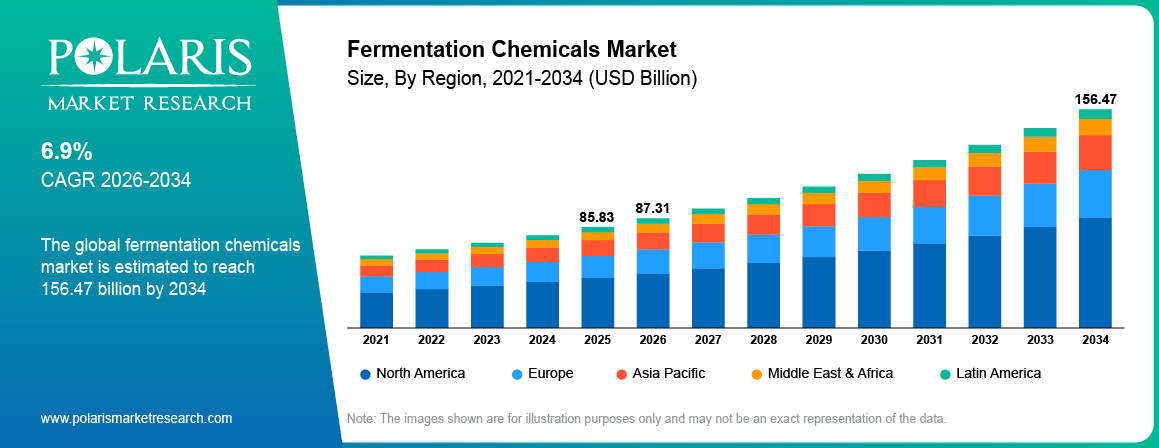

Fermentation Chemicals Market Summary

The fermentation chemicals market size was valued at USD 85.83 billion in 2025, growing at a CAGR of 6.9% between 2026 and 2034. The rising demand for bio-based products and the increasing use of fermentation chemicals in the development of essential medicines are a few of the key factors driving market growth.

Market Statistics

Fermentation Chemicals Market Key Takeaways

- Asia Pacific leads the market with 44.32% share. The regional market dominance is attributed to its robust manufacturing base, especially in emerging economies such as India and China.

- North America is expected to record significant growth rate of 35.10% CAGR during the forecast period.

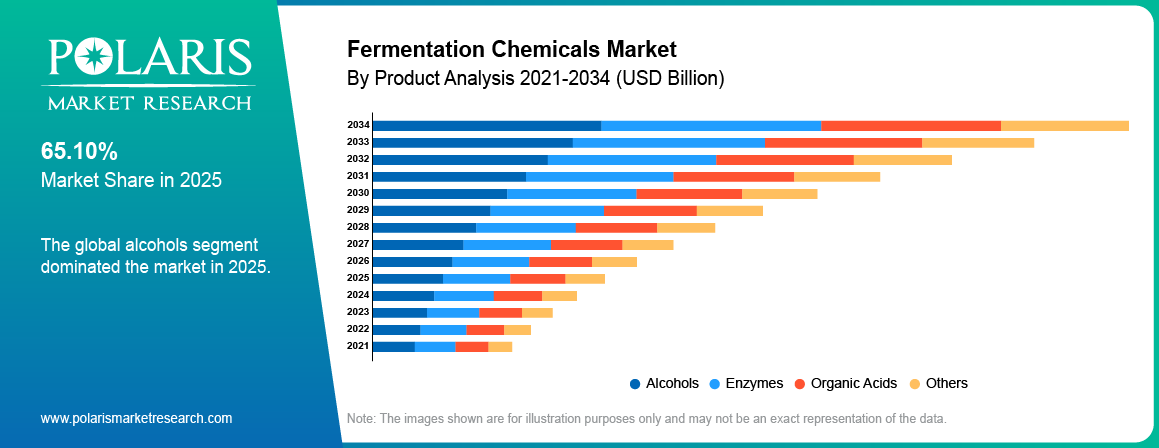

- The alcohols segment dominates the market with 65.10% share, primarily driven by its high versatility and strong bonding capabilities across various substrate types.

- The nutritional & pharmaceutical segment is projected to register the highest growth rate of 8.1% CAGR during the projection period, owing to the rising usage of fermentation-derived products across the health and wellness sectors.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The growing emphasis on the usage of sustainable and eco-friendly alternatives is driving the demand for fermentation chemicals.

- The expanding food and beverage industry, where fermentation is widely utilized for the production of various products, drives market growth.

- Technological advancements in fermentation are expected to provide several market opportunities in the coming years.

- Environmental concerns and regulatory hurdles may present market challenges.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What are Fermentation Chemicals?

Fermentation chemicals are bio-based compounds. They are produced through microbial fermentation processes. In fermentation processes, bacteria, yeast, or fungi convert raw materials such as sugars, starches, and biomass into valuable products. A few chemicals include alcohols, enzymes, amino acids, organic acids, and biopolymers. They are increasingly used across food & beverages, pharmaceuticals, agriculture, animal feed, and industrial manufacturing applications. This is due to their sustainability and high production efficiency.

The rising demand for enzymes in various industrial applications, such as food processing, and the increasing consumption of fermented foods and beverages boost the market growth.

The fermentation chemicals market focuses on the production of chemicals through the biological process of fermentation, where microorganisms break down complex compounds. This process yields various substances utilized across diverse industries, including food and beverages, pharmaceuticals, and biofuels. The market's expansion is significantly influenced by the increasing demand for bio-based products, as consumers and industries seek sustainable alternatives to traditional chemical processes. This shift is further propelled by the growing application of fermentation chemicals in the food and beverage industry, where they enhance flavor, texture, and nutritional value.

The pharmaceutical sector also contributes substantially to growth, as fermentation chemicals are increasingly used in the production of essential medicines, including antibiotics and vaccines. The sector’s reliance on fermentation for drug production, coupled with the overall expansion of the pharmaceutical, further fuels the demand for fermentation chemicals. Additionally, the inherent advantages of fermentation chemicals, such as their cost-effectiveness and eco-friendliness compared to petroleum-derived chemicals, contribute to their increasing adoption across multiple sectors.

Bio-Based vs Synthetic Chemicals

| Parameter | Bio-Based Chemicals | Synthetic Chemicals |

| Raw Mate rial Source | Produced from renewable feedstocks such as sugar, corn, biomass, and agricultural waste through fermentation processes | Manufactured using petrochemical-based raw materials derived from fossil fuels |

| Cost | Generally higher production costs due to feedstock availability, fermentation infrastructure, and processing requirements | Lower production costs owing to established large-scale petrochemical manufacturing systems |

| Sustainability | Environmentally friendly with lower carbon emissions, biodegradability, and reduced dependence on fossil resources | Higher environmental impact due to greenhouse gas emissions and non-renewable resource consumption |

| Performance | Offers high purity, biocompatibility, and suitability for food, pharmaceutical, and specialty applications | Provides consistent large-scale performance and durability for industrial applications |

| Regulatory Support | Increasing government incentives and sustainability regulations support market growth | Faces growing environmental regulations and pressure to reduce carbon footprint |

| Market Demand | Rising demand driven by clean-label products, green chemistry initiatives, and consumer preference for sustainable materials | Continues strong demand in bulk industrial and chemical manufacturing due to cost efficiency |

| Production Process | Utilizes microbial fermentation and biotechnology-based processes | Relies mainly on chemical synthesis and petrochemical refining |

| End-Use Applications | Widely used in food & beverages, pharmaceuticals, cosmetics, agriculture, and bioplastics | Extensively used in fuels, plastics, coatings, solvents, and industrial chemicals |

Source: Polaris Market Research Analysis

Fermentation Chemicals Market Trends and Growth Dynamics

Bio-based Chemicals Replace Petrochemical Inputs Across Industries

The increasing consumer and industrial preference for sustainable and eco-friendly alternatives propels the fermentation chemicals market growth. Fermentation processes utilize renewable chemicals and raw materials and often have a lower environmental impact compared to traditional chemical synthesis. This aligns with the global movement toward a bio-based economy, where industrial processes and products rely on renewable biological resources. The International Energy Agency (IEA) consistently reports on the growth of biofuels. Their Renewables 2023 report noted that global biofuel production increased by 6% in 2023, reaching 2.1 million barrels per day of oil equivalent, with a projected increase of 38% by 2028. This substantial growth in biofuel production utilizes fermentation processes for creating ethanol and other bio-based components, requiring fermentation chemicals. This shift in focus toward sustainable solutions is directly increasing the demand for fermentation chemicals across applications such as bioplastics, biofuels, and green chemicals.

Food and Beverage Demand Expands Use of Fermentation-Derived Ingredients

The food and beverage industry has long utilized fermentation for producing various products, and its continued expansion acts as a major driver. Fermentation chemicals, such as enzymes, organic acids, and alcohols, play crucial roles in enhancing the flavor, texture, nutritional value, and shelf life of food and beverage products. A report by the International Organisation of Vine and Wine (OIV) in 2022 highlighted that the global wine production amounted to approximately 258 million hectoliters, indicating a substantial demand for precision fermentation processes and related chemicals. Similarly, the rising consumption of fermented foods such as yogurt, cheese, and sauerkraut, driven by their perceived health benefits, further boosts the demand for fermentation chemicals. The continuous innovation in food processing techniques utilizing fermentation and the growing global population's demand for diverse and processed food products are significant factors propelling the growth.

Pharmaceutical Manufacturing Drives Demand for Fermentation-Derived Intermediates

The pharmaceutical industry is a significant end user of fermentation chemicals. Fermentation is employed in the production of a wide array of pharmaceuticals, including antibiotics, vaccines, vitamins, and other bioactive compounds. The World Health Organization (WHO) regularly reports on the increasing global burden of chronic diseases. For instance, the WHO estimates that cancer cases are anticipated to grow from 20 million in 2024 to 30 million by 2040, which will drastically increase the need for targeted therapies. The increasing global healthcare expenditure, the rising prevalence of chronic diseases, and the continuous research and development in novel drug formulations that often rely on fermentation processes are key factors contributing to the pharmaceutical industry's growth. As the pharmaceutical sector expands and develops new therapeutics, the demand for high-quality fermentation chemicals as crucial intermediates and active fermented ingredients will continue to rise, thereby driving the growth.

Source: Polaris Market Research Analysis

Fermentation Chemicals Market Segmentation Analysis

Product Analysis: Alcohols, Enzymes, Organic Acids and Other Fermentation Chemicals

The fermentation chemicals market, by product, is segmented into alcohols, enzymes, organic acids, and other products. Among these, the alcohols segment currently accounts for the largest share of 65.10%. This dominance is due to its exceptional versatility, cost-effectiveness, and strong bonding capabilities across a wide range of substrates, including metals, plastics, and composites. Alcohol-based adhesives are widely used in construction, automotive, and electronics industries for both temporary and permanent bonding. Their quick drying time, ease of application, and compatibility with other formulation ingredients further contribute to their dominance. Additionally, the growing demand for sustainable and low-VOC adhesives has driven manufacturers to favor alcohol-based formulations, reinforcing their leading market position.

The enzymes segment is anticipated to exhibit the highest growth rate during the forecast period. This rapid expansion is fueled by the increasing application of industrial enzymes across a multitude of sectors, such as food and beverage processing, detergents, animal feed, and pharmaceuticals. The growing demand for sustainable and efficient industrial processes, coupled with advancements in enzyme engineering and production technologies, is driving significant development in this area. The versatility and specificity of enzymes in catalyzing various biochemical reactions make them increasingly attractive for a wide range of industrial applications, positioning the enzymes segment for substantial growth in the coming years.

Application Analysis: Industrial, Food, Pharmaceutical, Plastics and Fiber Uses

The fermentation chemicals market, by application, is segmented into industrial application, food & beverages, nutritional & pharmaceutical, plastic & fibers, and other applications. Currently, the industrial application segment represents the largest share, driven by the extensive utilization of fermentation-derived chemicals in various industrial processes. These chemicals serve as crucial components in the manufacturing of a wide array of products, including solvents, detergents, and other industrial intermediates, leading to substantial demand and a dominant share for this application segment.

The nutritional & pharmaceutical segment is projected to experience the highest growth rate of CAGR 8.1% during the forecast period. This rapid growth is fueled by the increasing demand for fermentation-derived products in the health and wellness sectors. The rising consumer awareness regarding health and nutrition, coupled with the growing pharmaceutical industry's reliance on fermentation for producing vital drugs, vitamins, and other nutritional supplements, is significantly boosting the demand. The continuous advancements in biotechnology and the increasing focus on preventive healthcare are expected to further accelerate the growth of the nutritional & pharmaceutical application segment.

Fermentation Chemicals Market Technology and Process Advancements

| Technology | Advancement | Impact on Fermentation Chemicals Market |

| Advanced Bioreactors | Development of automated and high-efficiency bioreactors with improved temperature, pH, and oxygen control systems | Enhances production efficiency, product consistency, and large-scale manufacturing capabilities |

| Precision Fermentation | Use of genetically engineered microorganisms and synthetic biology techniques for targeted chemical production | Enables high-purity output, improved yield, and customized bio-based chemical manufacturing |

| Process Optimization | Integration of AI, data analytics, and real-time monitoring systems to optimize fermentation conditions | Reduces production costs, minimizes waste, and improves operational scalability |

| Continuous Fermentation Systems | Adoption of continuous production processes instead of batch fermentation methods | Increases productivity, shortens production cycles, and supports high-volume commercial operations |

| Feedstock Innovation | Utilization of alternative feedstocks such as agricultural waste, lignocellulosic biomass, and industrial by-products | Lowers raw material costs and improves sustainability in chemical production |

| Downstream Processing Technologies | Advanced separation and purification technologies improving recovery of fermentation-derived chemicals | Enhances product quality, process efficiency, and overall profitability |

| Industrial Biotechnology Integration | Increased integration of biotechnology platforms with industrial manufacturing systems | Accelerates commercialization of bio-based chemicals across multiple industries |

| Digital Fermentation Monitoring | Deployment of IoT sensors and cloud-based monitoring tools for process control | Improves predictive maintenance, reduces downtime, and enhances process reliability |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

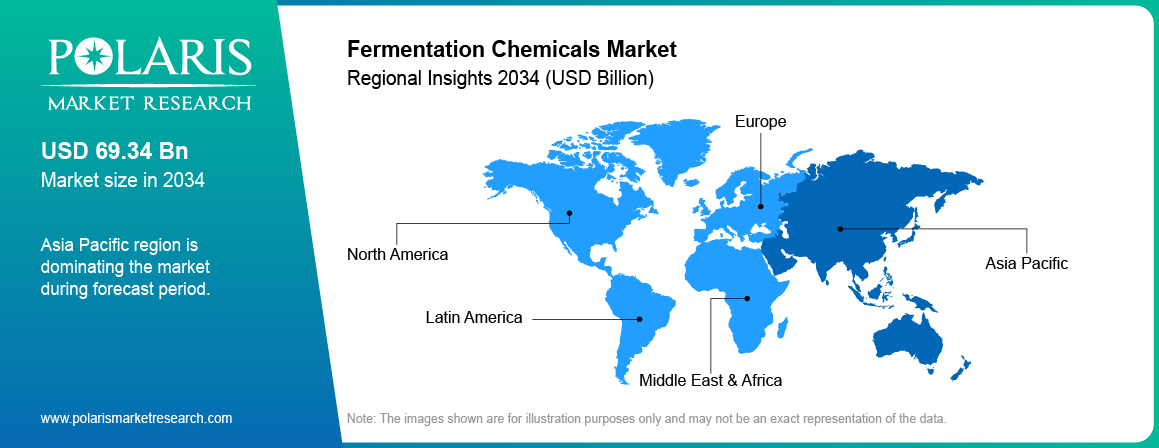

Regional Analysis

The fermentation chemicals market demonstrates a significant global presence, with key regions exhibiting distinct dynamics and growth patterns. North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa represent the major geographical segments influencing the overall landscape. Each region's market size, growth trajectory, and key drivers are shaped by factors such as industrial development, consumer preferences, regulatory frameworks, and the prevalence of end-use industries within their respective economies. Understanding these regional nuances is crucial for comprehending the global outlook and identifying potential entry opportunities.

Asia Pacific currently holds the largest share of 44.32%, owing to the presence of a large manufacturing base, particularly in countries such as China and India, which are significant consumers and producers of fermentation chemicals. The growing food and beverage industry, coupled with increasing investments in industrial biotechnology and biopharmaceuticals in this region, further contributes to its leading position. The sheer scale of industrial activities and the burgeoning population in Asia Pacific create a substantial demand for a wide range of fermentation-derived products.

Asia Pacific is also projected to exhibit the highest growth rate over the forecast period. This rapid expansion is driven by a confluence of factors, including increasing industrialization, rising disposable incomes leading to higher consumption of processed foods and beverages, and growing investments in the pharmaceutical and biotechnology sectors. Furthermore, supportive government initiatives promoting bio-based industries and the increasing adoption of sustainable practices across various applications are fueling development in this region. The dynamic economic growth and expanding end-use industries within Asia Pacific position it as a high-potential region.

Source: Polaris Market Research Analysis

Fermentation Chemicals Market Competitive Landscape

A few key players active in the fermentation chemicals market include Cargill, Incorporated; Evonik Industries AG; BASF SE; Koninklijke DSM N.V.; DuPont de Nemours, Inc.; Ajinomoto Co., Inc.; Archer-Daniels-Midland Company; Lonza Group AG; Novozymes A/S; Chr. Hansen Holding A/S; Corbion N.V.; and Kerry Group plc.

The competitive landscape is characterized by a mix of well-established multinational corporations and smaller, specialized companies. Competition is driven by factors such as product innovation, cost efficiency, application-specific solutions, and strategic partnerships. Players are increasingly focusing on developing sustainable and bio-based production methods to cater to the growing demand for environmentally friendly products. Furthermore, collaborations and acquisitions are observed as companies aim to expand their product portfolios and geographical reach.

Cargill, Incorporated, headquartered in Minneapolis, Minnesota, USA, offers a diverse range of fermentation-derived products, including organic acids, ethanol, and specialty ingredients for the food & beverage and industrial sectors. Their extensive global network and strong focus on agricultural processing provide a robust foundation for their involvement.

Evonik Industries AG, based in Essen, Germany, provides a variety of fermentation products, such as amino acids, feed additives, and biocatalysts, catering to the animal nutrition, pharmaceutical, and specialty chemicals industries. Their expertise in biotechnology and focus on developing high-performance products solidify their position as a significant participant.

List of Key Companies

- Ajinomoto Co., Inc.

- Archer-Daniels-Midland Company

- BASF SE

- Cargill, Incorporated

- Chr. Hansen Holding A/S

- Corbion N.V.

- DuPont de Nemours, Inc.

- Evonik Industries AG

- Kerry Group plc

- Koninklijke DSM N.V.

- Lonza Group AG

- Novozymes A/S

Fermentation Chemicals Market Recent Developments

-

March 2026: Amyris, Inc. completed the construction of a new production line. It is an expansion of capabilities at its precision fermentation plant in Barra Bonita, Brazil. (Source: amyris.com)

-

In July 2025, LanzaJet announced its USD 200 million ethanol-to-jet fuel plant in Georgia would begin operations by end-2025, producing sustainable aviation fuel (SAF) and renewable diesel. (Source: economictimes.indiatimes.com)

-

In May 2025, DMC Biotechnologies commercially launched fermentation-derived myo-inositol, offering high purity and lower environmental impact than chemical synthesis. (Source: dmcbio.com)

Fermentation Chemicals Market Segmentation

By Product Outlook (Revenue – USD Billion, 2021–2034)

- Alcohols

- Enzymes

- Organic Acids

- Other Products

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Industrial Application

- Food & Beverages

- Nutritional & Pharmaceutical

- Plastic & Fibers

- Other Applications

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Fermentation Chemicals Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 85.83 billion |

| Market Size Value in 2026 | USD 87.31 billion |

| Revenue Forecast by 2034 | USD 156.47 billion |

| CAGR | 6.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Fermentation Chemicals Market FAQ's

The market size was valued at USD 85.83 billion in 2025 and is projected to grow to USD 156.47 billion by 2034.

The market is projected to register a CAGR of 6.9% during the forecast period.

Asia Pacific held the largest share of 44.32% in 2025.

A few key players include Cargill, Incorporated; Evonik Industries AG; BASF SE; Koninklijke DSM N.V.; DuPont de Nemours, Inc.; Ajinomoto Co., Inc.; Archer-Daniels-Midland Company; Lonza Group AG; Novozymes A/S; Chr. Hansen Holding A/S; Corbion N.V.; and Kerry Group plc.

The industrial application segment accounted for the largest share of the market in 2025.

Following are a few of the trends: ? Growing Demand for Bio-based Alternatives: There is an increasing shift toward sustainable and eco-friendly products, driving the demand for fermentation chemicals as alternatives to petrochemical-based chemicals. ? Expansion in Food and Beverage Industry: The rising consumer preference for natural ingredients, clean-label products, and functional foods is leading to increased use of fermentation-based additives, preservatives, and flavor enhancers. The growing consumption of alcoholic and non-alcoholic beverages also contributes significantly.

Fermentation chemicals refer to a wide range of chemical compounds produced through the metabolic process of fermentation, primarily by microorganisms such as bacteria, yeasts, and fungi. This biochemical process occurs in the absence of oxygen (anaerobically) and involves the breakdown of organic substances, such as sugars and starches, into simpler molecules.

Download Sample Report of Fermentation Chemicals Market

Please fill out the form to request a customized copy of the research report.