Blood Cancer Drugs Market Demand, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

REPORT DETAILS

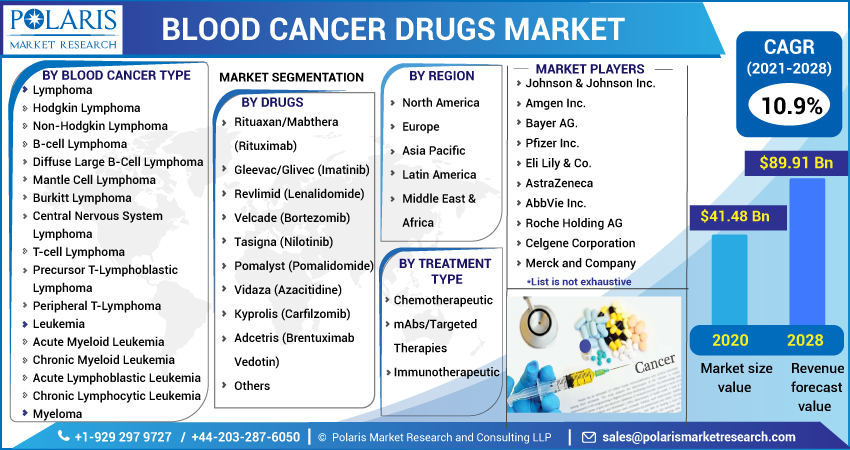

Blood Cancer Drugs Market Summary

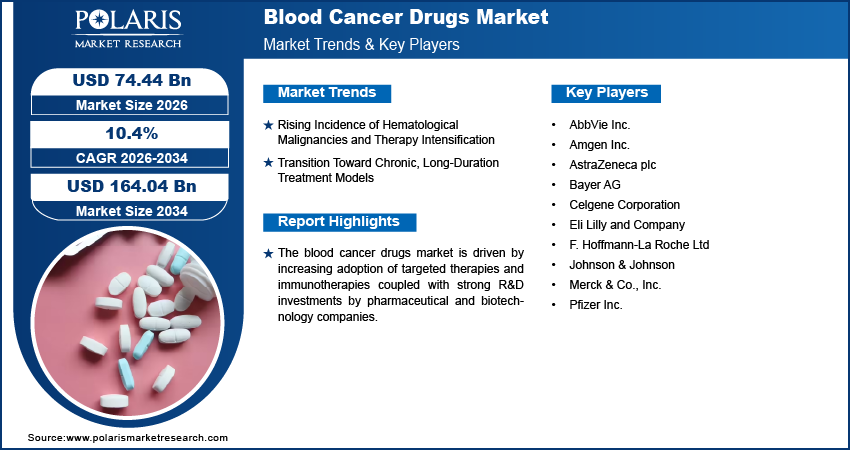

The global blood cancer drugs market is estimated around USD 67.50 billion in 2025,?with consistent growth anticipated during 2026–2034. The market is projected to grow at CAGR of 10.4% during the forecast period due to rising incidence of hematological malignancies and therapy intensification along with transition toward chronic, long-duration treatment models.

Market Statistics

Key Takeaways

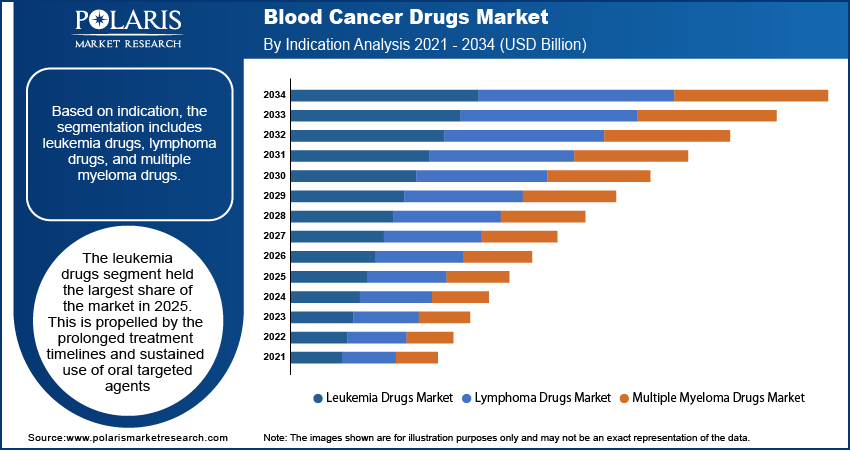

- The leukemia drugs segment held the largest share of the market in 2025 due to prolonged treatment timelines and sustained use of oral targeted agents.

- Multiple myeloma drugs is projected to grow rapidly, driven by disease chronicity, frequent relapse, and near-universal reliance on multi-drug regimens expand cumulative drug exposure per patient.

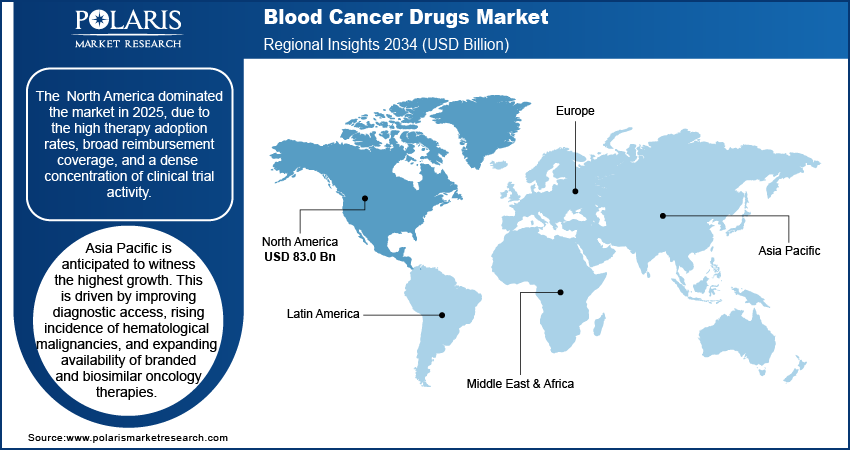

- The North America dominated the market in 2024 propelled by high therapy adoption rates, broad reimbursement coverage, and a dense concentration of clinical trial activity

- Asia Pacific is anticipated to witness the highest growth. This is driven by improving diagnostic access, rising incidence of hematological malignancies, and expanding availability of branded and biosimilar oncology therapies.

Future Demand Scenarios

- Base scenario: Demand expands steadily as diagnosis rates rise, treatment access improves, and standard chemotherapy, targeted therapies, and supportive regimens continue to see routine clinical use across major healthcare systems.

- Upside scenario: Faster adoption of targeted therapies, CAR-T cell treatments, and next-generation immunotherapies accelerates growth, supported by earlier-line approvals, expanded indications, and higher treatment uptake in emerging markets.

- Conservative scenario: Growth slows due to pricing pressure, reimbursement tightening, and delayed adoption of high-cost advanced therapies, combined with slower regulatory approvals in select regions.

Industry Dynamics

- Rising incidence of hematological malignancies and therapy intensification

- Transition toward chronic, long-duration treatment models

- Cost and reimbursement pressures limiting market expansion

- Advanced antibody platforms in hematologic oncology

What is Blood Cancer Drugs and Why It Matters

Blood cancer drugs form the core of modern blood cancer therapeutics used across leukemia, lymphoma, and myeloma care within hematologic malignancies treatment pathways. These therapies include oncology biologics, small-molecule agents, targeted therapy blood cancer regimens, immunotherapy drugs, and advanced cell-based approaches shaping the CAR-T therapy market. Precision targeting of malignant cells, guided by molecular profiling and biomarker selection, has reshaped clinical practice and extended treatment duration across disease stages. Demand is driven by rising diagnosis rates, earlier therapy initiation, and sustained use across relapse and maintenance settings. Secure access to differentiated drug platforms to preserve clinical outcomes, treatment continuity, and competitive positioning as therapeutic intensity and lifetime treatment value continue to rise.

The market for blood cancer therapeutics has been growing steadily throughout the past years with innovation and the high price point associated with these products. The market in 2024 breaks down with 41% of its oncology therapeutics sales in the North American market, followed by the European market with 29%, and then the Asia Pacific market with 22% market share. The market for blood cancer medications is expected to break the USD 145 billion mark in 2034 with increased availability of targeted therapies, higher diagnosis rates, and increased healthcare expenditure in developing countries driving the market.

Drivers & Opportunities

Rising Incidence of Hematological Malignancies and Therapy Intensification

The blood cancer drugs industry is expanding with the rising cases of hematological malignancies. The blood cancer medications industry is meeting the demands from the leukemia medications industry, the lymphoma medications industry, along with the multiple myeloma medications industry. According to the American Society of Hematology, by 2030, the total number of hematological malignancies worldwide is projected to reach about 4.63 million. Hematological cancer drugs now occupy a larger share of the oncology drugs market as diagnostic rates improve and molecular stratification sharpens treatment selection. Targeted therapy in cancer changes the way the treatment paradigm is approached, from focusing on general cytotoxic exposure to pathway-specific inhibition. This led to more use of the drug for each patient and prolong treatment duration.

Transition Toward Chronic, Long-Duration Treatment Models

The blood cancer drugs market is growing due to the increasing trend from the conventional shorter hospital-based chemotherapy courses to protracted outpatient courses. Targeted therapy blood cancer protocol and immunotherapy hematology model promotes the adoption of sustained dosing regimens with protracted administration schedules. Oral medications receive increasing acceptance along with the biologic infusion therapies that take prolonged administration schedules, leading to a paradigm shift in the usage trends. Those encompassing BTK inhibitors market the product and BCL-2 inhibitors support protracted maintenance strategies with multiple indications, resulting in the compounding of demand with structurally protracted timelines.

Restraints & Challenges

Cost and Reimbursement Pressures Limiting Market Expansion

Cost pressures and payer attention exert significant influence in the blood cancer drugs space and are responsible for some of the greatest challenges in the industry. The cost incurred in advanced modalities, particularly cell therapies, is significantly higher and is posing a challenge to the industry with the cost of CAR-T cell therapy as the major hindrance in the majority of healthcare settings. The current regulation and reimbursement environment in the industry remains uneven, with delays in oncology reimbursement and a lag in reimbursement and innovation in the majority of healthcare settings. These factors have led to the price challenges in the hematology drug space gaining attention with an increased cost of care with prolonged treatment and combination therapies.

Emerging Opportunities

Advanced Antibody Platforms in Hematologic Oncology

The rapid development of bispecific as well as trispecific antibodies is creating high-value opportunities within the blood cancer drugs market, extending beyond conventional single-target therapies. These agents are engineered to bind cancer cells and immune effector cells at the same time, creating direct immune synapses that intensify tumor cell killing. Usage patterns are rising across leukemia, lymphoma, and myeloma indications where increasingly the depth of treatment response and its durability become a proxy for success. These patterns indicate a transition to a market where a premium based on specifications are expected to drive by efficiency in engaging the immune system.

Segmental Insights

This report provides granular coverage of the Blood Cancer Drugs market by indication, drug class, therapy type, route of administration, enabling readers to identify the fastest-growing and most profitable demand pockets.

By Indication

-

Leukemia Drugs

The leukemia medications represented about 38% of the total revenue from blood cancer medications in 2025, making it the leading indication segment for hematological malignancies. The chronic leukemias, driven by the CLL medications, are the leaders in the market demand driven by the long treatment duration and the sustained oral target therapies. The acute leukemias, comprised of AML medications and the medications used to treat ALL, provide substantial revenue contributions driven by the combination regimens and the clinic-based administration of the biologics and the chemotherapies.

Targeted therapy leukemia paradigms have redefined treatment sequencing. BTK inhibitors leukemia and BCL-2 inhibitors leukemia have replaced chemotherapy in various cases of CLL, prolonging the course of the treatment, whereas in the case of AML, the rapid expansion of FLT3 inhibitors, as well as antibody-based targeted therapies for AML, are continuing with a similar trend.

-

Lymphoma Drugs

The lymphoma therapies accounted for a share of approximately 34% of the revenue in the global market of blood cancer therapies in 2025. The Non-Hodgkin Lymphoma therapies lead the way in this category due to the widespread usage of monoclonal antibodies, antibody-drug conjugates, and cocktails of immunotherapy combinations. The treatment of DLBCL contributes considerably due to the high rates of relapse and the widespread usage of CAR-T therapy in the later lines of treatment.

Bispecific antibodies lymphoma and next-generation monoclonal antibodies oncology associated advances are contributing to an increasingly diverse set of treatment alternatives for patients with relapsed lymphoma. Safety profiles and administration methods are driving a shift of care into outpatient settings in a way that is helping to fuel adoption while sustaining premium pricing.

-

Multiple Myeloma Drugs

The multiple myeloma drugs accounted for roughly 28% of total market revenue in 2025 and is projected to record one of the fastest growth rates. The chronicity of diseases, relapsing courses, and almost universal maintenance regimens drive overall drug exposure. The lack of single-line treatments in multiple myeloma maintains overall extended treatment courses in hematological malignancies.

Proteasome inhibitors market, IMiDs for cancers, and monoclonal antibodies represent the current treatment backbone, while CAR-T for multiple myeloma and bispecific antibodies for myeloma drive growth for later-line treatments. Continuous therapy rotation, driven by resistance emergence, sharply increases lifetime drug expenditure. This positions multiple myeloma as a central growth engine within the blood cancer drugs market.

Indication-wise Comparison

| Indication Segment | Revenue Share (2024) | Growth Outlook | Treatment Characteristics | Key Revenue Drivers | Commercial Implications |

| Leukemia Drugs | ~38% (Largest) | Moderate–High | Mix of chronic maintenance and acute intensive regimens | Long treatment duration in CLL, rising use of BTK and BCL-2 inhibitors, inpatient biologics for AML/ALL | High volume stability, strong oral drug penetration, sustained lifecycle value across lines |

| Lymphoma Drugs | ~34% | Steady | Line-based escalation with relapse-driven therapy switching | Monoclonal antibodies, ADCs, CAR-T in DLBCL, bispecific antibodies | Premium pricing supported by relapse frequency and expanding outpatient eligibility |

| Multiple Myeloma Drugs Market | ~28% | High (Fastest-growing) | Chronic, multi-line combination therapy with frequent rotation | Proteasome inhibitors, IMiDs, monoclonal antibodies, CAR-T, bispecifics | Highest lifetime drug spend per patient; strong pipeline-driven expansion |

The report evaluates each grade by market size, share, growth rate, and indicative pricing differentials.

By Drug Class

-

Targeted Therapies

Targeted therapies held the leading market share, accounting for more than 44% of the overall blood cancer therapeutics market in 2025. This indicates a clear shift in the targeted therapy market for blood cancer towards precision medicine. BTK inhibitors, BCL-2 inhibitors, and kinase-targeted therapies are fundamentally changing the treatment paradigms by making way for less reliance on chemotherapy. Enhanced efficacy, lower systemic toxicity, and the availability of oral dosing are the factors that facilitate their use.

-

Immunotherapies

The immunotherapy segment accounted for roughly 32% of market value in 2025, driven by growing indication and favorable reimbursement structures in prominent geographies. The immunotherapy approach for blood cancers leverages the usage of monoclonal antibodies and bispecific molecules for immune-mediated cytotoxic effects, mainly in lymphoma and multiple myeloma.

-

Cell & Gene Therapies

Cell and gene therapies accounted for a smaller but rapidly growing share of the market. The CAR-T therapies offer remarkably strong treatment responses, even in the context of refractory disease, making the CAR-T therapy market a high-impact growth driver. Despite the limited number of patients and the infrastructural intensities, the pricing structures enable these segments to make a disproportionate contribution to growth.

-

Chemotherapy & Conventional Agents

Conventional agents retain clinical relevance within induction regimens, combination protocols, and regions governed by cost-sensitive treatment access. Their role is seen where rapid reductions are needed or in areas with uneven development of innovative therapies. Despite the ongoing share erosion, traditional agents are firmly positioned within the early line or resource-limited contexts.

By Therapy Type

-

Combination Therapy

Combination therapy blood cancer protocols accounted for over 65% of total treatment regimens in 2025. Clinical preference favors multi-agent strategies that deepen response and suppress resistance emergence. Layered regimens integrating targeted agents, immunotherapies, and conventional drugs dominate across indications. Failure of a single component rarely ends therapy, instead driving substitution within the regimen.

-

Monotherapy

Monotherapy remains relevant in maintenance phases, elderly populations, and patients with tolerability limitations. Oral targeted agents are frequently selected to balance sustained disease control with manageable safety profiles, particularly in chronic blood cancers.

By Route of Administration

-

Oral Drugs

Oral oncology drugs represented the fastest-growing route of administration. Improved patient compliance, outpatient suitability, and reduced healthcare system burden accelerate adoption, especially in long-term leukemia and multiple myeloma maintenance settings.

-

Injectable Drugs

Injectable cancer drugs remain central to monoclonal antibody delivery and short-course induction protocols. Their utilization concentrates in structured clinical environments where dosing precision and real-time monitoring are required.

-

Infusion Therapies

Infusion therapy oncology formats continue to dominate acute and advanced disease settings while also representing the fastest-growing route segment. This segment is driven by biologics, antibody drug conjugates, and cell therapies, where complexity of drug administration has been balanced by high treatment response rates among relapsed and high-risk patients.

Regional Analysis

North America Blood Cancer Drugs Market Assessment

North America led the blood cancer drugs market in 2025, accounting for over 41% of total revenue, driven by strong adoption rates in therapy, favorable reimbursements, and a strong pipeline of clinical studies. The blood cancer drug market in North America is firmly rooted in the US, which has accelerated approval procedures for early market access to high-priced biologics, targeted therapies, and cell therapies. In October 2025, The U.S. FDA approved Blenrep (belantamab mafodotin-blmf) for the treatment of adults with relapsed or refractory multiple myeloma. This approval is an important regulatory step for blood cancer drugs, which received approval based on successful Phase III clinical trial outcomes. Payer acceptance and sustained therapy durations in Leukemia, Lymphoma, and Multiple Myeloma continue to fuel US Hematology drug markets.

Europe Blood Cancer Drugs Market Insights

Europe accounted for approximately 29% of global revenue in 2025, driven by to its universal healthcare programs and systematic penetration of target-specific hematology treatments. The market for blood cancer treatments in Europe also gets driven due to its systematic regulation and standardized clinical practices throughout the major European countries. The penetration of innovative oncology treatments available in Europe is gradually increasing within the settings of hospitals and specialists, even as price regulation and HTA reviews moderate market growth. The market for advanced hematology treatments in Europe also shows resilience due to rising focus on precision medicine and long-term management.

Asia Pacific Blood Cancer Drugs Market Overview

Asia Pacific is projected to register the highest CAGR during the forecast period, driven by the better access of diagnostics, growing cases of hematologic malignancies, and the growing availability of branded and biosimilar versions of anticancer therapies. In December 2025, Zydus Lifesciences introduced Zyrifa, the denosumab (120 mg subcutaneously) biosimilar, in India, which is used for the prevention of skeletal events in non-metastatic breast cancer, prostate cancer, and hormone-refractory or hormone-independent advanced malignancies. The Asia Pacific market for blood cancer drugs receives thrust from the Chinese and Indian markets, which are primarily driven by the government computing initiatives for the improvement of the overall health infrastructure of these rapidly growing nations. This makes the Asia Pacific market one of the foremost emerging markets for the changed demands for oral targeted therapies, immunotherapies, and maintenance therapy for the management of this condition.

Rest of the World Blood Cancer Drugs Market Snapshot

Latin America, the Middle East, and Africa represent smaller but progressively advancing markets within the global landscape. The blood cancer medications market in Rest of the World advances with gradual enhancements in cancer care infrastructure, specialists, and treatment accessibility. Use of targeted therapies grows selectively, representing alignment with worldwide standards for cancer medications among developing regions.

Heat Map Analysis

| Region | Demand Intensity | Therapy Adoption | Reimbursement Strength | Clinical Trial Activity | Growth Momentum |

| Asia Pacific | High | Medium–High | Medium | Medium–High | Very High |

| Europe | High | High | Medium–High | High | Medium |

| North America | Very High | Very High | Very High | Very High | High |

| Rest of the World | Medium | Medium | Low–Medium | Low–Medium | Medium |

Key Players & Competitive Analysis Report

The blood cancer drugs market is highly consolidated, with blood cancer drugs market players largely comprising global hematology pharmaceutical companies and established oncology drug manufacturers. A small group of multinational firms accounts for a substantial share of global revenue, supported by strong clinical pipelines and broad commercialization capabilities. The areas of focused competition include targeted therapies, immuno-oncology products, and next-generation biologics, with significant investment in late-stage CD development and label extensions. The intensity of competition is still high in the leukemia, lymphoma, and multiple myeloma market, where innovation and therapy optimization continue to fuel refinements in the respective products and company strategies. Collaborations and acquisitions continue to be central to enhancement and positioning in hematology franchises.

Key companies operating in the global blood cancer drugs market include AbbVie Inc., Amgen Inc., AstraZeneca plc, Bayer AG, Celgene Corporation, Eli Lilly and Company, F. Hoffmann-La Roche Ltd, Johnson & Johnson, Merck & Co., Inc., and Pfizer Inc.

Key Players

- AbbVie Inc.

- Amgen Inc.

- AstraZeneca plc

- Bayer AG

- Celgene Corporation

- Eli Lilly and Company

- F. Hoffmann‑La Roche Ltd

- Johnson & Johnson

- Merck & Co., Inc.

- Pfizer Inc.

Premium Insights: Competitive Strategy Trends

- Strong shift toward first-line label expansion for targeted therapies to capture longer treatment durations and earlier patient access

- Increasing focus on bispecific antibodies as scalable and off-the-shelf alternatives to CAR-T therapies

- Growing investment in next-generation oral therapies to improve patient compliance and enable long-term disease management

- Strategic acquisitions and licensing deals aimed at securing late-stage hematology pipelines and differentiated mechanisms of action

Future Outlook & Opportunities

The blood cancer drugs market outlook points to sustained expansion shaped by targeted therapies, biosimilars, and fast-moving immunotherapy platforms. Precision continues to tighten. Treatment selection increasingly follows molecular signals, risk stratification, and response depth, reshaping the future of hematology drugs into longer, more structured therapy pathways. Innovation velocity remains high as oncology pipeline trends favor bispecific antibodies, next-generation CAR-T constructs, and immune modulators that extend remission durability. At the same time, biosimilars are reshaping access economics, pushing price discipline into markets that were once limited by affordability. Growth will favor companies that translate scientific progress into scalable portfolios, manage cost pressure without slowing development, and align innovation cycles with payer and regulatory expectations across regions.

What to Watch Next

| Trend / Development | What to Monitor | Potential Market Impact |

| Next-generation immunotherapies | Clinical Depth of Response and Durability in Various Hematologic Disease Indications | Longer treatment cycles, higher lifetime drug spending per patient |

| Bispecific and Trispecific antibodies | Speed of regulatory approvals and entry into earlier lines of therapy | More premium pricing power and quicker market penetration |

| CAR-T platform evolution | Manufacturing scale, safety profiles, and so on: Advances | An expanded base of eligible patients, supported by improved adoption rates. |

| Biosimilar expansion | Timing of entry, price discounting, and acceptance of payers | Friction on originator margins with wider patient access |

| Personalized treatment strategies | Integration of biomarkers and molecular profiles into treatment decision-making | Increased complexity of therapies and continued demand for targeted agents |

| Reimbursement frameworks | Coverage policy and value-based pricing changes | By exerting a direct influence on the uptake speed and regional growth trajectories |

Industry Developments

- November 2025: The US FDA has approved Elahere (mirvetuximab soravtansine-gynx), the first drug derived from Broad Institute science and the first targeted cancer therapy, for the treatment of adults with platinum-resistant ovarian cancer. The approval marked the significant progress of the field of antibody-drug conjugates and the expansion of targeted therapies in oncology.

- November 2025: UVA Health announced that a new treatment for acute myeloid leukemia (AML) was initiated with a new approach that showed an improved success rate in its early-stage testing.

Blood Cancer Drugs Market Segmentation

By Indication Outlook (Revenue, USD Billion, 2021-2034)

- Leukemia Drugs Market

- Lymphoma Drugs Market

- Multiple Myeloma Drugs Market

By Drug Class Outlook (Revenue, USD Billion, 2021-2034)

- Targeted Therapies

- Immunotherapies

- Cell & Gene Therapies

- Chemotherapy & Conventional Agents

By Therapy Type Outlook (Revenue, USD Billion, 2021-2034)

- Combination therapy

- Monotherapy

By Route of Administration Outlook (Revenue, USD Billion, 2021-2034)

- Oral drugs

- Injectable drugs

- Infusion therapies

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Blood Cancer Drugs Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 67.50 Billion |

| Market Size in 2026 | USD 74.44 Billion |

| Revenue Forecast by 2034 | USD 164.04 Billion |

| CAGR | 10.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 67.50 billion in 2025 and is projected to grow to USD 164.04 billion by 2034.

The?North America region holds the largest share in the blood cancer drugs market, supported by high therapy adoption rates, broad reimbursement coverage, and a dense concentration of clinical trial activity.

Targeted therapies is the primary drug class fueled by shift toward precision medicine within the targeted therapy blood cancer landscape.

A few of the key players in the market are AbbVie Inc., Amgen Inc., AstraZeneca plc, Bayer AG, Celgene Corporation, Eli Lilly and Company, F. Hoffmann-La Roche Ltd, Johnson & Johnson, Merck & Co., Inc., and Pfizer Inc.

Key factors include rising incidence of hematological malignancies and therapy intensification coupled with transition toward chronic, long-duration treatment models.

Download Sample Report of Blood Cancer Drugs Market

Please fill out the form to request a customized copy of the research report.