Catheters Market Trends and Revenue, Industry Report, 2026-2034

REPORT DETAILS

Catheters Market Summary

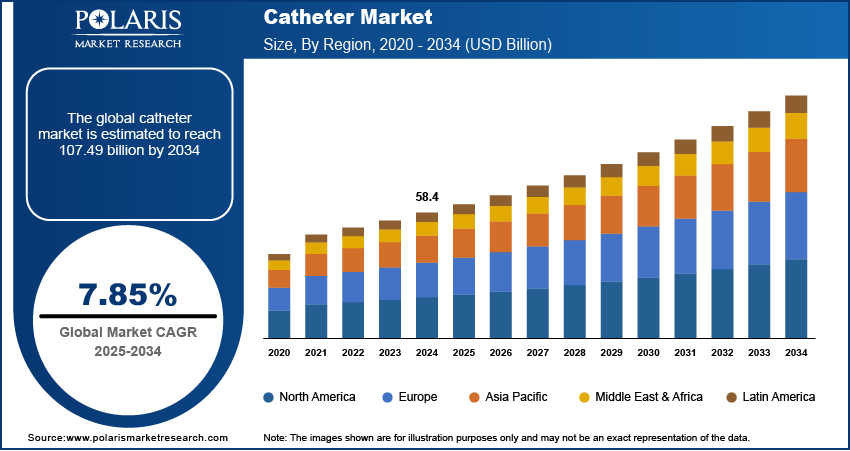

The global catheter market size was valued at USD 27.11 billion in 2025. It is expected to expand at a compound annual growth rate (CAGR) of 8.8% between 2026 and 2034. This growth is driven by the increasing prevalence of chronic diseases, rising surgical procedures, and the growing demand for minimally invasive treatments.

Market Statistics

Key Takeaways

- North America dominated the market in 2025, accounting for 30.20% share. The region has a strong healthcare infrastructure. It also has a high burden of chronic diseases. Adoption of advanced and home-based catheter care solutions is increasing.

- The Asia Pacific market is expected to account for a 11.0% CAGR. This is due to a large patient base and improving healthcare systems. Insurance access is also improving. Demand in the homecare catheter market is rising. Cost-effective treatment options are also expanding.

- The cardiovascular catheters segment led in 2025 with a 29.59% share. It plays a key role in diagnosing and treating cardiovascular diseases. This is supported by the rising global disease burden. Demand is also increasing for procedure-specific and infection-resistant catheter solutions.

- The polyurethane catheters segment is expected to grow steadily at a 9.5% CAGR. This is due to its flexibility and strong biocompatibility. It is widely used in central venous and hemodialysis procedures. Demand is also rising for safer and infection-resistant catheter materials.

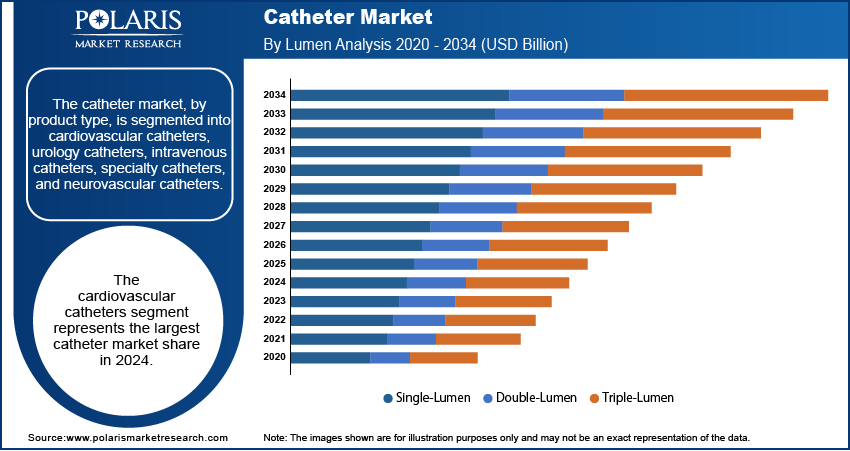

- The double-lumen segment held the largest share of 33.2% in 2025. This is mainly due to the rising demand for advanced biomaterial-based devices.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

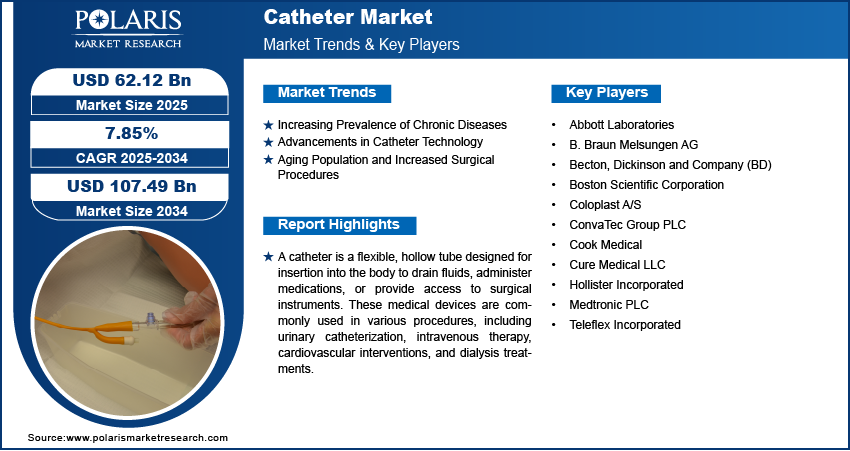

- The growth in the prevalence of chronic diseases and the increasing need for catheter-based procedures in the treatment of various medical conditions are driving the market's expansion.

- Ongoing innovations in catheter technology, including antimicrobial coatings and AI-optimized solutions, are enhancing patient outcomes, comfort, and safety, thereby driving market expansion.

- The increasing demand for less invasive methods, combined with the development of new catheter technologies, offers significant growth opportunities for the catheter market.

- The severe risk of infection and complications associated with catheter use, as well as the high price of advanced catheter technologies, are major inhibiting factors in the market.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

AI Impact on Catheter Market

- AI improves catheter design using large datasets. It helps develop safer and more biocompatible materials. This backs AI catheter design and reduces infection risk.

- AI helps select the most suitable catheter for each patient. It uses patient data for better decisions. This reflects AI in the catheter market and improves treatment accuracy.

- AI detects early signs of complications. These include infection or obstruction. This supports predictive catheter monitoring and enables faster intervention.

- AI-powered automation is improving catheter production. It enhances quality control and reduces costs. This strengthens AI catheter manufacturing processes.

- AI-integrated catheters enable real-time monitoring. They alert healthcare professionals to potential issues. These smart catheter systems provide timely care and better outcomes.

The market includes medical tubes used to deliver or remove fluids during treatment. It is also used for diagnosis and treatment access inside the body, such as checking conditions, guiding procedures, and supporting ongoing care. These devices are used across hospitals, outpatient centers, and homecare settings, depending on patient needs. Demand is rising with the shift toward outpatient care and home-based treatment models. At the same time, minimally invasive catheter procedures are becoming more common as they reduce recovery time and improve patient comfort. Healthcare professionals are also focusing on safer designs and infection control. This is supporting overall catheter market growth and influencing purchasing decisions.

This growth is driven by the increasing prevalence of chronic diseases, rising surgical procedures, and the growing demand for minimally invasive treatments. The catheter market covers medical devices. These devices are used for draining fluids, delivering medications, and performing surgical processes. These flexible tubes are used in hospitals, clinics, and even in home healthcare settings. They're important for patients dealing with long-term illnesses, struggling with mobility, or healing after an operation.

The market is expanding, fueled by increasing healthcare demands, continuous technological progress, and an aging demographic that requires extended care. Additionally, the move toward less intrusive methods is driving advancements in catheter design. This, in turn, enhances patient comfort and reduces the chances of complications arising.

The increasing prevalence of cardiovascular diseases, urinary disorders, and neurological conditions has significantly increased the need for catheter-based treatments. Improvements in healthcare infrastructure, especially in emerging economies, are expanding access to advanced medical procedures. The increasing use of home healthcare is also driving up the need for catheters, as patients look for easier and cheaper ways to get care. In addition, ongoing research and development are leading to the use of antimicrobial coatings and biodegradable materials. These new technologies are improving the safety and effectiveness of medical procedures.

This shift is also linked to rising homecare catheter demand and the use of outpatient catheter procedures. Healthcare providers are focusing on antimicrobial catheters to reduce infection risks and improve outcomes. It also helps care delivery in ambulatory centers and home settings. These changes reflect ongoing catheter market trends across lower-cost and patient-friendly care environments.

Examples of Real-World Uses

Heart Surgery: Angioplasty, heart imaging, and stent insertion are some procedures where catheters are used to restore blood flow and detect heart disorders.

Dialysis: Specialized catheters are inserted into the veins to allow blood filtration when the kidneys are not functioning adequately.

Bladder Control: A urinary catheter is used in cases where individuals need help managing their bladders after surgery, when there is difficulty holding urine, or when assistance is required.

IV Medication Administration: Intravenous catheters allow the delivery of liquids, antibiotics, nutrition, anesthesia, and emergency medications directly into the bloodstream.

Neurovascular Procedures: Catheters can be utilized in the management of stroke, aneurysm, and other neurovascular procedures by using minimally invasive techniques.

ICU Applications: Critical care patients require catheters to monitor, administer drugs, drain fluids, and provide emergency access during critical procedures.

Market Dynamics

Increasing Prevalence of Chronic Diseases

The rising prevalence of chronic illnesses, such as cardiovascular diseases, diabetes, and urological disorders, has increased the demand for catheter-based interventions. The growing patient population is increasing the use of catheters for both diagnosis and treatment. This supports the overall catheter industry growth.

Cardiovascular procedures, access for dialysis, urinary care, and neurovascular treatments are becoming more common. The increasing prevalence of chronic diseases and the aging population are driving this trend. Simultaneously, the urology catheter market is experiencing growth, reflecting greater patient requirements. This upward trajectory is, in turn, propelling the broader catheter market and creating a greater need for specialized catheters, especially in complex medical situations.

Advancements in Catheter Technology

Ongoing improvements in catheter design and the materials used have significantly improved safety, effectiveness, and patient comfort during catheterization. The introduction of antimicrobial-coated catheters has been instrumental in decreasing infections related to catheter use. The design physically blocks bacteria, a departure from conventional drug-based approaches. These advancements improve patient outcomes. They also encourage healthcare providers to adopt newer catheter models, supporting catheter market development.

Innovation is also focused on advanced catheter design features. These include better tip control, secure placement, and hydrophilic surfaces. Manufacturers are also improving kink resistance and reducing clot risks. These improvements support infection-resistant catheters and safer use. They also strengthen demand in the catheter technology market for premium catheter devices across acute and long-term care settings.

Aging Population and Increased Surgical Procedures

The global increase in the elderly population is raising the prevalence of age-related health issues. Many of these conditions require catheterization. Older adults are more prone to urinary incontinence and cardiovascular diseases. This increases the need for catheters in effective management. The number of surgical procedures among the elderly is also rising. This is increasing catheter use during perioperative care. Together, these factors are supporting catheter industry growth.

This trend is also increasing the aging population catheter demand across care settings. It supports higher geriatric catheter use in post-acute care and rehabilitation. Home-based catheter care is also growing as more patients recover outside hospitals. These changes are boosting demand for easier and safer long-term catheterization solutions.

Restraints: Infection Risk and Cost Pressure

Infection risk and cost pressures are significant challenges in the market. The high risk of infection and other problems related to catheters, combined with the high cost of advanced catheter technologies, are major obstacles.

Catheter-associated infections, blood clots, and blockages continue to be significant clinical concerns. These catheter complications affect patient safety and outcomes. Healthcare providers are cautious in device selection. High costs create pressure on catheter prices in many systems. Problems with reimbursement in the catheter market limit the use of advanced devices. These factors are major constraints on the market and influence purchasing decisions.

Source: Polaris Market Research Analysis

Segment Insights

By Product Type

The product type is segmented into cardiovascular catheters, urology catheters, intravenous catheters, specialty catheters, and neurovascular catheters. The cardiovascular catheters segment led in 2025 with a 29.59% share. These medical devices are important for diagnosing and treating various heart conditions, including coronary artery disease and irregular heartbeats. The widespread occurrence of cardiovascular diseases worldwide has led to a growing need for these catheters. As a result, the significant impact of cardiovascular diseases continues to drive the expansion of the cardiovascular catheter segment.

The cardiovascular catheters segment is also supported by the growing use of catheter-based procedures. These include interventional cardiology catheters for heart treatments and vascular catheter applications. Their use is increasing in minimally invasive procedures. Electrophysiology catheters are also widely used for managing cardiac rhythm disorders.

The specialty catheters segment is experiencing the highest growth rate. This is driven by rising demand for minimally invasive procedures. This is also supported by the increasing prevalence of conditions that require specialized catheter solutions. Advancements in catheter technology have led to the creation of devices designed for specific uses, such as wound drainage, oximetry, and thermodilution. These innovations improve patient outcomes and expand the use of catheters in various medical fields. Moreover, the specialty catheters segment is growing because standard devices cannot support complex procedures. These include neurovascular access and targeted therapy delivery. Procedure-specific catheters are essential for managing complex anatomical needs, which helps improve clinical outcomes.

Cardiovascular vs Urology vs Intravenous vs Neurovascular Catheters

| Types | Primary Application | Common Locations | Main Advantage |

| Cardiovascular | Operations on heart and blood vessels | Hospitals | Precise entry |

| Urological | Bowel emptying | Hospitals/At Home | Convenient bladder control |

| Intravenous | Administration of drugs and fluids | Clinics/Hospitals | Quick entry |

| Neurovascular | Treatments for brain and nerve blood vessels | Specialist Centers | Convenient treatments |

Source: Polaris Market Research Analysis

By Lumen

The lumen segmentation includes single-lumen, double-lumen, and triple-lumen catheters. The double-lumen segment held the largest share of the catheter market revenue in 2025. This is mainly due to the rising demand for advanced biomaterial-based devices. These devices help lower complications such as thrombosis and infections. They also support better patient outcomes and improve care efficiency. Growth in catheter technology and the increasing use of minimally invasive procedures are also supporting this segment.

Single-lumen catheters are used for basic access. Double-lumen catheters offer more flexibility and better efficiency. Triple-lumen catheters are mainly used in critical care settings. They allow multiple therapies and monitoring at the same time. These differences show the benefits of multi-lumen catheters in clinical use.

By Material

The material segment includes silicone catheters, polyurethane catheters, latex catheters, and others. The silicone catheters segment held the largest market share in 2025. Silicone is biocompatible and inert, which makes it suitable for long-term use. It helps reduce allergic reactions and improves patient comfort. Its flexibility and resistance to encrustation support its wide use in applications such as urinary and peritoneal dialysis catheters. The material is also durable and lasts longer, which reduces the need for frequent replacement. This supports better patient compliance and helps lower healthcare costs. These factors support the strong position of silicone catheters in the market.

In catheter material use, silicone is mainly preferred for long-term use and comfort. Polyurethane catheters are seeing rising demand in high-performance clinical settings. They offer strength, flexibility, and better pressure handling. These catheters are compatible with the body and are used in different medical treatments.

The polyurethane catheters segment is expected to grow steadily at a 9.5% CAGR. This is mainly due to its flexibility and good compatibility with the human body. It is widely used in medical applications such as central venous and hemodialysis catheters. Its ability to adjust to body shape and handle high-pressure conditions without losing strength makes it useful in intensive care. It also has a lower risk of thrombosis and offers good durability, which supports its wider use.

When compared to other materials, polyurethane is stronger than silicone and latex. It performs better in high-pressure and critical care use. Because of this, it is commonly used in central venous and hemodialysis catheters. These benefits are supporting the growth of the polyurethane catheter market.

By End Use

Based on end use, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and homecare settings. The hospitals segment held the largest market share in 2025. Hospitals perform a high volume of catheter-based procedures. These include surgeries and minimally invasive interventions. This creates a consistent and strong demand for various catheter types. Hospitals have advanced medical technology and skilled healthcare professionals. This supports effective use of these devices. The rising prevalence of chronic diseases is increasing hospital admissions. This further strengthens the dominance of this segment.

Hospitals handle complex and high-risk cases. These include cardiology, neurology, critical care, and urology treatments. This propels strong hospital catheter demand across departments. The use of catheters in hospitals remains common, mainly because of the need for immediate medical care and the increasing use of less invasive procedures.

The homecare settings segment is experiencing the highest growth rate. This is due to the rising preference for home-based treatments. This issue is particularly prevalent in older adults and individuals with long-term medical needs that necessitate catheterization. Recent innovations in catheter design have resulted in devices that are both easy to use and safe for at-home application. Such devices empower patients to take greater control of their own care. Consequently, this leads to increased comfort and overall contentment. It also reduces the burden on healthcare facilities. The homecare catheter market is also supported by growing self-catheterization trends. Patients are relying less on hospitals for routine care. Telehealth catheter management is improving remote monitoring and support. These factors are strengthening home-based catheter care and long-term catheter demand.

Source: Polaris Market Research Analysis

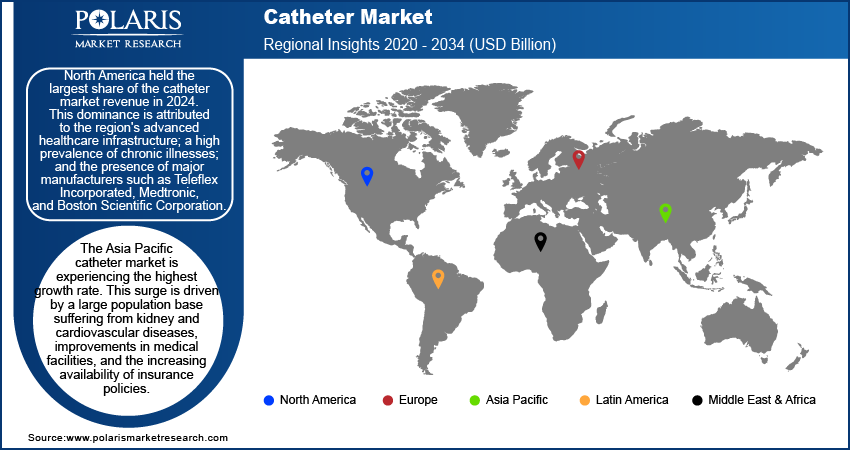

Regional Insights

The catheter market exhibits considerable regional variation, with North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa each contributing uniquely to the industry's overall profile. The specific characteristics of the industry within these regions are shaped by a variety of factors, including the prevalence of chronic diseases, the condition of healthcare systems, advancements in technology, and changes in population demographics. A global analysis of the catheter market reveals that regional demand is contingent upon several key elements. These encompass catheter reimbursement policies, the volume of procedures performed, and the availability of qualified specialists. Furthermore, local manufacturing capabilities and supply chains also play a role in determining product availability. Homecare adoption patterns further shape the market by region.

North America dominated the market in 2025, accounting for 30.20% share. This is mainly due to strong healthcare infrastructure and a high number of chronic disease cases. The North American catheter market is buoyed by the presence of industry giants like Teleflex Incorporated, Medtronic, and Boston Scientific Corporation. Growth is further fueled by a combination of advantageous regulations and a workforce of highly skilled professionals. Hospitals in the region see a high volume of procedures, which also contributes to the market's expansion. Moreover, there's a robust adoption of premium catheters, alongside the early integration of cutting-edge catheter technologies. Established purchasing systems and strong clinical acceptance support the catheter market share in North America.

The Asia Pacific market is expected to account for a 11.0% CAGR. This surge is driven by a large population base suffering from kidney and cardiovascular diseases, improvements in medical facilities, and the increasing availability of insurance policies. Government initiatives aimed at enhancing healthcare quality are certainly a catalyst for advancement. Moreover, the growing need for accessible, advanced healthcare solutions within the region presents significant opportunities. The Asia Pacific catheter market is experiencing substantial growth, fueled by the market expansion in developing areas. China, India, and Japan are key contributors to this demand. China's and India's catheter markets are experiencing growth, fueled by more procedures being performed. The Japan catheter market is being propelled by sophisticated healthcare systems and an aging population.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The catheter industry includes several major companies offering a wide range of products. Key players include B. Braun Melsungen AG, Boston Scientific Corporation, Hollister Incorporated, Medtronic PLC, Teleflex Incorporated, Abbott Laboratories, ConvaTec Group PLC, Coloplast A/S, Cook Medical, Cure Medical LLC, and Becton, Dickinson and Company (BD). The market covers both large global companies and specialized firms. All are working to support their position through innovation, partnerships, and expansion.

Companies are more focused on creating improved catheter technology to address emerging healthcare needs. This includes urology, gastrointestinal procedures, and more. Some work closely with healthcare facilities and invest in research. This helps them remain competitive. Companies are adhering to very specific regulations and are quality-focused. This helps build trust and sustain long-term market presence.

The catheter competitive landscape also depends on how companies differentiate their products. Leading catheter manufacturers compete based on product range, procedure focus, and innovation. Their geographic reach also plays an important role. Infection-prevention features and product reliability influence buying decisions. These factors help position catheter market companies as catheter innovation leaders.

List of Key Companies

- Abbott Laboratories

- Braun Melsungen AG

- Becton, Dickinson and Company (BD)

- Boston Scientific Corporation

- Coloplast A/S

- ConvaTec Group PLC

- Cook Medical

- Cure Medical LLC

- Hollister Incorporated

- Medtronic PLC

- Teleflex Incorporated

Catheter Industry Developments

- April 2026: Medtronic announced the completion of the acquisition of CathWorks. According to Medtronic, the acquisition will help enhance its portfolio in coronary diagnostics and redefine the future of cardiovascular care. (source: medtronic.com)

- December 2025: AVACEN, Inc. received a U.S. utility patent for its CATHeter STAbilization (CATHSTA) device. The company stated that the device is designed to provide angle-adaptive mechanical stabilization for large-bore arterial access and reduce catheter migration. (source: einpresswire.com)

Future of Catheter Market

The catheter market is expected to witness steady growth driven by the development of innovative biomaterials and antibacterial coating technologies. There is an increasing preference for patient safety, improved comfort, and flexible catheters. The rising adoption of home care and outpatient facilities will further drive growth prospects in the global market. In addition, innovations such as intelligent catheters are bound to provide significant advancements in this field. The expansion of healthcare infrastructure in developing nations is expected to ensure continued market growth.

Market Segmentation

By Product Type Outlook (Revenue-USD Billion, 2021–2034)

- Cardiovascular Catheters

- Urology Catheters

- Intravenous Catheters

- Specialty Catheters

- Neurovascular Catheters

By Lumen Outlook (Revenue-USD Billion, 2021–2034)

- Single-Lumen

- Double-Lumen

- Triple-Lumen

By Material Outlook (Revenue-USD Billion, 2021–2034)

- Silicone Catheters

- Polyurethane Catheters

- Latex Catheters

- Others

By End Use Outlook (Revenue-USD Billion, 2021–2034)

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Homecare Settings

By Regional Outlook (Revenue-USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest of Latin America

Catheter Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 27.11 billion |

| Market Size Value in 2026 | USD 29.40 billion |

| Revenue Forecast by 2034 | USD 58.07 billion |

| CAGR | 8.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021-2024 |

| Forecast Period | 2026-2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

How is the report valuable for an organization?

Workflow/Innovation Strategy: The catheter market has been segmented into detailed segments of product type, lumen, material, and end use. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy: The catheter market is growing through product improvement, partnerships, and expansion into new regions. Companies are making better catheters using improved materials and infection control features for safer use. They work with hospitals and research groups to build trust and reach more users. Many companies are also entering markets in the Asia Pacific and Latin America to meet rising demand. They focus on affordable and quality devices in these regions. Digital marketing and awareness campaigns help increase visibility. Regulatory approvals also support market entry and growth.

Catheter Market FAQ's

The market was valued at USD 27.11 billion. It is projected to reach USD 58.07 billion by 2034 with a growing disease burden and treatment demand.

The market is expected to grow at a CAGR of 8.8% during 2026 to 2034.

The cardiovascular segment holds the largest share, mainly due to high heart disease cases and frequent use in procedures.

Polyurethane is one of the fastest-growing materials, as it is flexible and works well in critical care use.

Homecare is becoming more important as people prefer simple, low-cost care options for long-term use.

Growth is driven by more chronic diseases, an aging population, and higher use of minimally invasive procedures.

AI is helping in better design, device selection, and monitoring, which supports safer and more efficient use.

North America leads the market because of strong healthcare systems and a high number of procedures.

Asia Pacific is likely to grow faster due to rising healthcare access and a large patient base.

The market faces limits like infection risk, blockage issues, strict rules, and high product cost.

Download Sample Report of Catheter Market

Please fill out the form to request a customized copy of the research report.